.webp)

Introduction

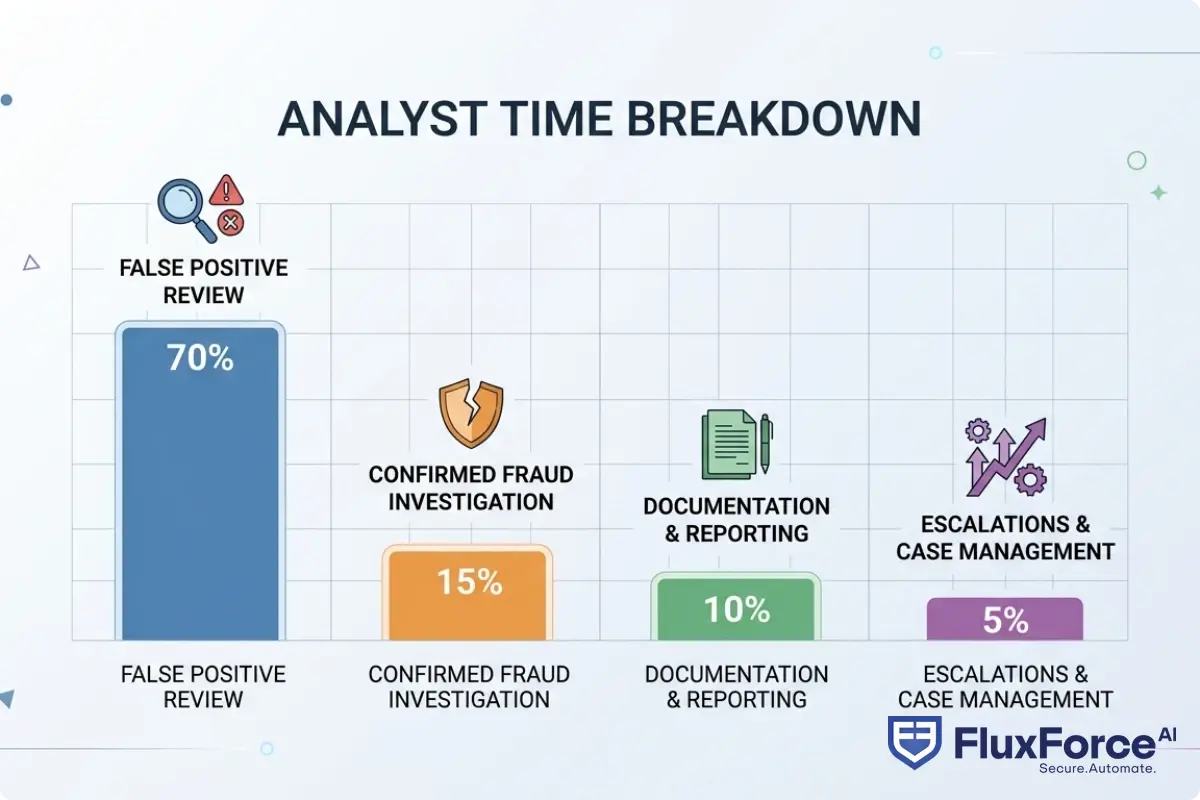

Fraud alert fatigue in financial institutions has reached a breaking point. Research shows the average fraud analyst spends more than 70% of their working day reviewing alerts that never lead to confirmed fraud, false positives generated by disconnected detection tools. That's not an operational inefficiency. It's a structural problem that gets worse as organizations add more point solutions to their stack.

Research shows the average fraud analyst spends more than 70% of their working day reviewing alerts that never lead to confirmed fraud, false positives generated by disconnected detection tools.

The irony is that more tools typically means more alerts, not fewer. Each vendor fires its own warnings using its own logic, with no shared context. By 8 AM, your analysts are already sorting through hundreds of low-confidence flags before any real threats have surfaced.

This post breaks down exactly why that fatigue happens, what makes it worse, and how a unified risk platform with explainable AI changes the math for fraud and compliance teams.

- The Real Cost of Fraud Alert Fatigue in Financial Institutions

- Point Solutions vs Platform Financial Services: Where the Noise Starts

- What a Unified Risk Platform Does to Fraud Alert Fatigue

- How Explainable AI Finance Changes Alert Triage

- Why Fraud Alert Fatigue Gets Worse Without Explainable AI Compliance

Onboard Customers in Seconds

The Real Cost of Fraud Alert Fatigue in Financial Institutions

Fraud alert fatigue in financial institutions isn't just an operational inconvenience. It's a compliance and revenue risk that shows up quietly in audit findings, analyst turnover rates, and missed fraud losses. When investigators spend the majority of their day clearing low-confidence alerts, several things happen at once:

- Real fraud slips through because analysts are too fatigued to scrutinize edge cases

- Alert queues back up, pushing review times past regulatory SLAs

- Experienced analysts burn out and leave, taking institutional pattern recognition with them

- The institution adds more detection rules to "improve" coverage, which generates even more alerts

That last point is where things spiral. Reducing false positives has always been the hardest part of fraud detection, but adding rules to an already noisy system is like fixing a leaky bucket by adding more buckets.

Why False Positives Dominate the Alert Queue

Most alert queues are dominated by false positives for a specific reason: legacy rule-based systems are calibrated for recall, not precision. The goal was always to catch every possible fraud event, and the side effect is that legitimate transactions get flagged constantly.

A customer using their card abroad after booking a flight online? Alert. A business making a large invoice payment to a new supplier? Alert. A retiree changing direct deposit instructions? Alert. Each requires a human to confirm it's fine. Multiply that across millions of transactions per day and you understand exactly where the 70% figure comes from.

The Analyst Burnout No One Budgets For

Turnover in fraud operations is rarely discussed in budget planning, but it deserves more attention. When an analyst who has reviewed thousands of alerts per week for two years leaves, that calibrated pattern recognition doesn't transfer to their replacement. The new hire is slower, less accurate, and needs months to reach the same judgment level.

The hidden cost isn't just recruiting and training. It's the degraded detection quality during the transition, which often shows up as fraud losses that are hard to attribute directly to the staffing gap.

Point Solutions vs Platform Financial Services: Where the Noise Starts

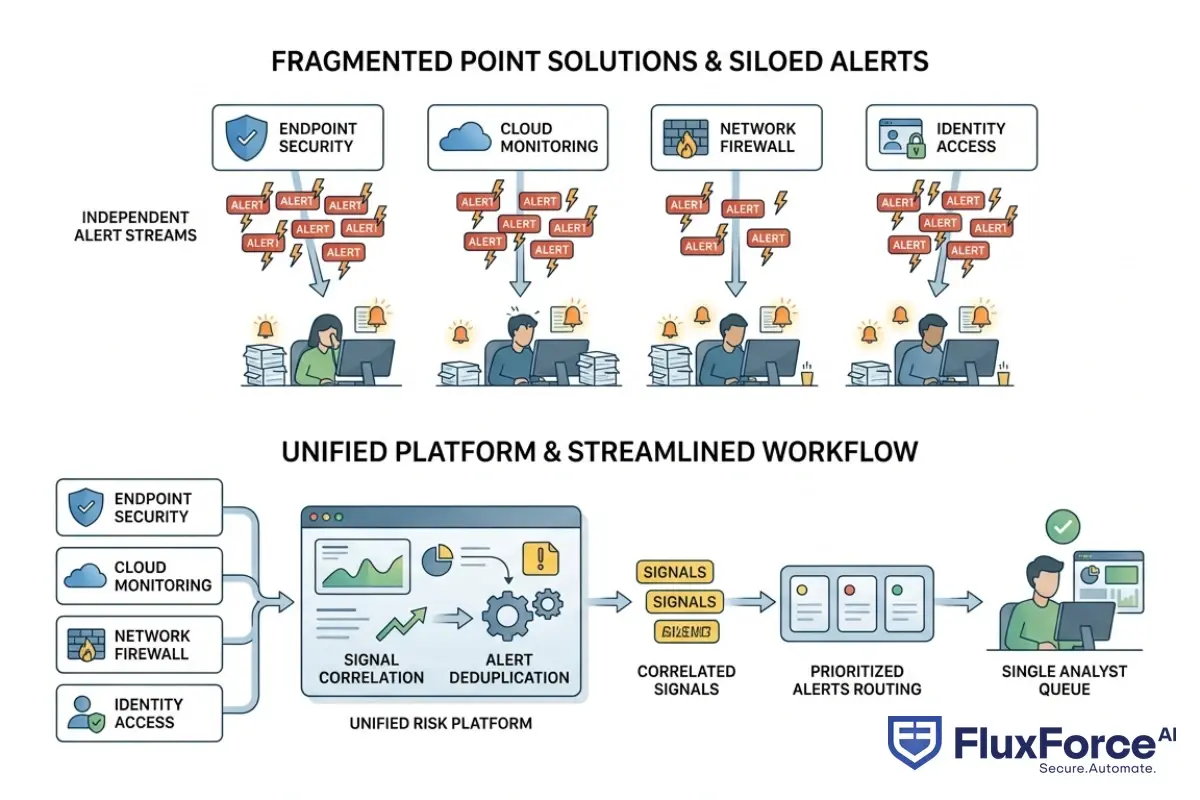

The point solutions vs platform financial services debate has a clear practical answer when you look at alert volume. Most financial institutions have accumulated four to eight separate tools over the past decade: one for card fraud, one for AML, one for identity verification, one for account takeover, one for ACH monitoring. Each fires its own alerts.

The overlap is significant. A single suspicious transaction can generate separate alerts from the fraud detection engine, the AML monitoring tool, and the identity layer simultaneously. The analyst sees three different notifications about the same event, reviews them in three different interfaces, and documents the outcome three times.

How Tool Sprawl Creates Duplicate Alerts

When different systems share no data context, they can't de-duplicate. The card fraud tool doesn't know the identity tool already flagged the same customer twenty minutes ago. The AML system doesn't know the fraud analyst cleared the transaction earlier that morning. Each system operates on its own data slice, and the result is redundant work throughout the team.

This is the structural problem that vendor consolidation in fintech addresses, not just to reduce licensing costs but to share context across risk signals that currently live in isolated silos. When signals are shared, the correlation layer can suppress alerts that don't need human review.

Vendor Consolidation Fintech: The Financial Case

The financial argument for vendor consolidation fintech goes beyond license fees. Every additional point solution adds integration maintenance, a separate vendor relationship, separate SLA negotiations, and separate API upgrade cycles. Security certifications need to cover each tool. Compliance audits need to document each one.

When you factor in the analyst time lost to context-switching between interfaces, the true cost of a five-tool stack versus a unified platform is rarely as close as it appears. Research comparing AI-driven and traditional fraud detection approaches consistently shows that unified approaches outperform fragmented stacks on both precision and total operational cost.

What a Unified Risk Platform Does to Fraud Alert Fatigue

A unified risk platform is a single system that ingests signals from fraud detection, identity verification, AML, and behavioral analytics, correlates them in a shared data layer, and surfaces one context-rich alert to the analyst instead of four separate notifications. The analyst sees a single event with all relevant signals attached: device fingerprint, transaction history, identity verification result, behavioral anomalies, and the model confidence score with an explanation.

That's a fundamentally different experience than toggling between tabs. More importantly, it produces a different accuracy level. When the system can see all signals together, it can de-duplicate, cross-correlate, and suppress alerts that don't meet a combined confidence threshold. That suppression step is where the actual alert volume reduction happens.

How a Fraud Compliance Identity Platform Reduces Noise

A fraud compliance identity platform specifically addresses the three-way overlap between fraud detection, KYC compliance, and identity verification. These three domains generate separate alerts in most institutions, but they share enormous context. A customer who passed full KYC but shows unusual transaction velocity is a different risk profile than one who showed KYC friction at onboarding. A platform that connects these signals suppresses alerts that don't warrant investigation while elevating the ones that do.

Teams working on AML risk checks and identity verification workflows see the biggest workload reductions here: not fewer total events, but far fewer events requiring manual review because context is already shared across the system.

What an AI Security Operations Platform Handles Differently

An ai security operations platform applies machine learning at the triage layer, not just at detection. Traditional systems detect and then hand everything to humans. An AI security operations platform detects, triages, correlates, and suppresses before the analyst ever sees the alert.

The practical difference: instead of presenting 1,000 alerts per day, the system presents 200, with confidence scores and recommended actions attached to each one. Analysts spend their time on decisions, not on sorting through noise to find what actually deserves attention.

How Explainable AI Finance Changes Alert Triage

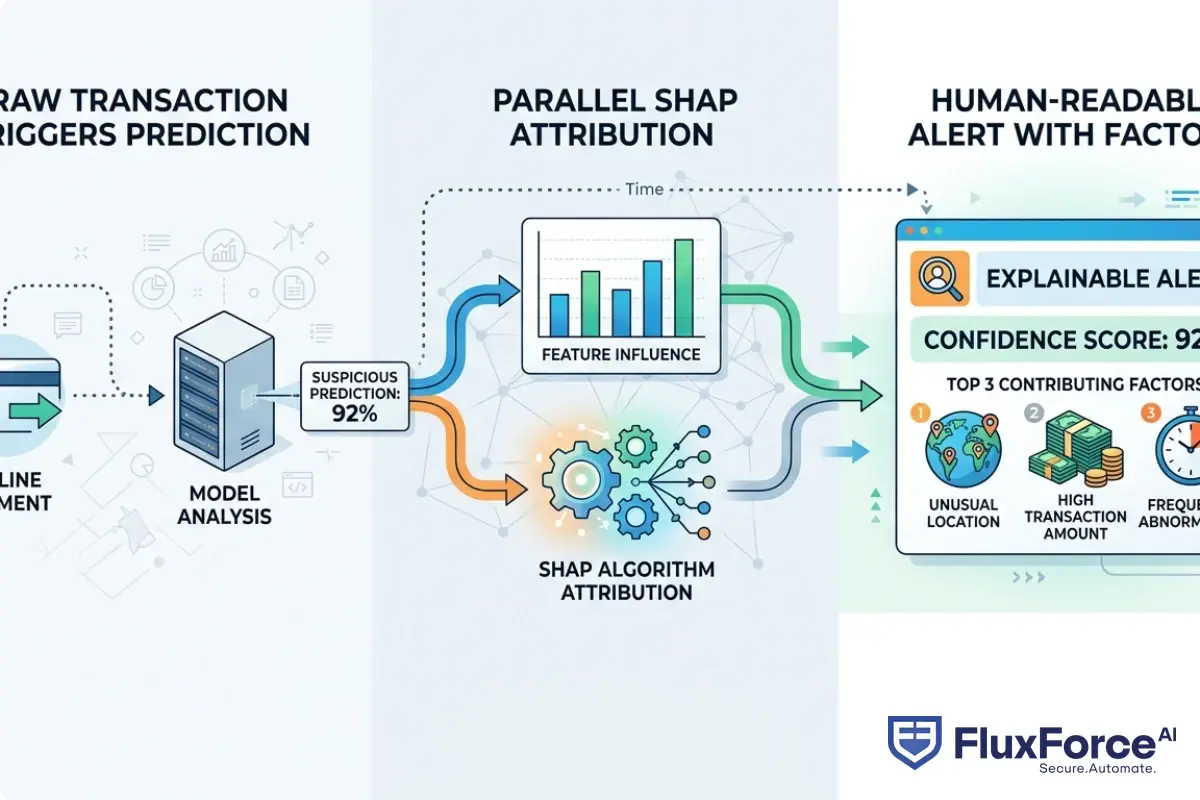

Explainable AI finance is the practice of designing detection models so that decisions come with human-readable justifications. Instead of "this transaction was flagged," the analyst sees "this transaction was flagged because the device is new, the location is 3,400 km from the last known address, and the merchant category has a 12x higher fraud rate than baseline."

That context changes how quickly analysts can act. A well-reasoned, high-confidence alert takes around 30 seconds to confirm. A black-box flag with no context takes 5 minutes of additional research. Multiply that across 500 alerts per day and the math speaks for itself.

SHAP Values Explained for Regulators

SHAP (SHapley Additive exPlanations) values are one of the most widely used methods for explaining machine learning predictions. SHAP values answer a specific question: which features contributed most to this prediction, and by how much? If a model flags a transaction as high-risk, SHAP values show that the device anomaly contributed 42% of the risk score, the velocity pattern contributed 31%, and geographic distance contributed 27%. That's auditable and defensible in a regulatory review.

If a model flags a transaction as high-risk, SHAP values show that the device anomaly contributed 42% of the risk score, the velocity pattern contributed 31%, and geographic distance contributed 27%.

The European Banking Authority has explicitly referenced the need for financial institutions to document how AI-driven risk decisions are made, including which model features drove specific decisions. SHAP provides exactly that documentation layer.

Why Black Box AI Creates Compliance Risk

Black box ai compliance risk is real and growing. When a model declines a transaction, flags an account for review, or triggers a SAR filing without any explanation, the institution is exposed on multiple fronts. Consumer protection regulations require that adverse decisions be explainable. AML frameworks require that SAR filings document why a transaction was suspicious. A model that can't explain itself can't meet those requirements cleanly.

The honest answer is that some of the highest-performing fraud models are also the hardest to explain. The solution isn't to use weaker models. It's to layer explainability on top through xai fraud detection frameworks like SHAP, which can attribute predictions to input features without requiring the underlying model architecture to be simple.

Why Fraud Alert Fatigue Gets Worse Without Explainable AI Compliance

The connection between explainable AI compliance and alert volume is direct. When analysts can't understand why an alert was generated, they can't develop intuition about which alerts are likely real. Every alert becomes equally opaque and equally time-consuming. There's no shortcutting the review because there's no context to work from.

This is where fraud alert fatigue in financial institutions becomes self-reinforcing. Opaque models generate alerts that analysts can't quickly evaluate. Slow evaluation creates backlogs. Backlogs create pressure to clear alerts faster. Faster clearing means less scrutiny. Less scrutiny means more fraud slips through. More fraud triggers more rule additions. More rules mean more alerts.

AI Model Explainability for Regulators

AI model explainability for regulators is no longer optional in most jurisdictions. The EU AI Act, the UK PRA guidance on model risk, and the NIST AI Risk Management Framework all require that financial institutions understand and document how their AI models make decisions.

The challenge is that explainability means different things to different audiences. Regulators want audit trails and statistical documentation. Analysts want plain-language alert summaries. Compliance teams want evidence that adverse decisions were model-consistent and not discriminatory. A good xai fraud detection system needs to serve all three audiences from the same underlying explanation infrastructure.

XAI Fraud Detection in Practice

The practical implementation of xai fraud detection looks like this: every alert includes a score, the top contributing features, and a natural language summary that a non-technical analyst can read and act on in under a minute. The same underlying SHAP data is stored in the ai audit trail automation system for regulatory review. The analyst doesn't need to know what SHAP is. They just need to see "flagged because of: unusual device + high-risk merchant + velocity spike" and make a decision.

AI Agents, Multi-Agent Systems, and Human in the Loop AI Banking

AI agents financial services are purpose-built software agents that handle specific subtasks autonomously: enriching an alert with context, cross-checking against sanction lists, or querying a customer's historical transaction profile. A multi agent ai system coordinates several of these agents to handle the full alert lifecycle without waiting for human input at every step.

The result is that by the time an analyst sees an alert, it has already been enriched with everything relevant: the customer's prior alerts, any open cases, the result of a real-time sanctions check, and a risk score breakdown. That preparation work used to take 5-10 minutes per alert. Now it happens in seconds.

How AI Agent Fraud Detection Works in a Multi-Agent AI System

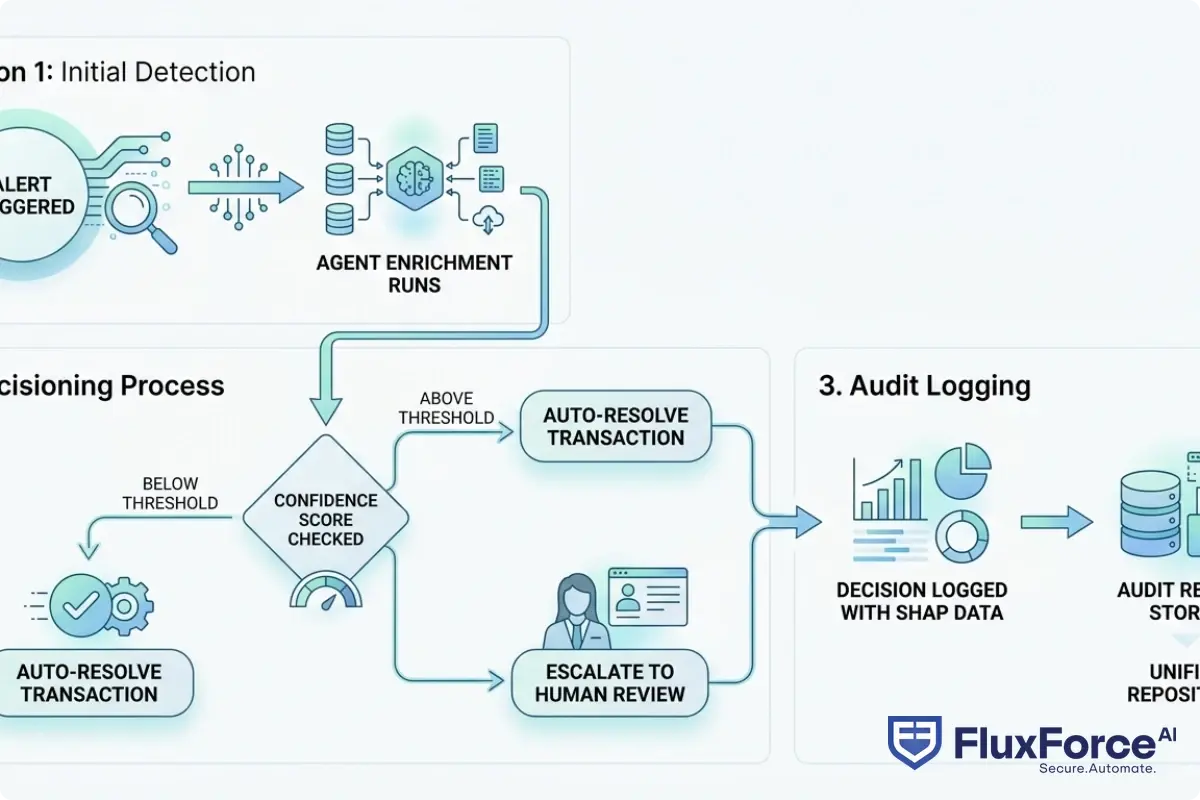

AI agent fraud detection in a multi-agent setup typically assigns one agent to transaction enrichment, one to identity cross-referencing, and one to risk scoring. A coordinating agent aggregates results and decides whether confidence is high enough to warrant human review. If not, the alert is auto-resolved with a full audit trail. If yes, it surfaces to the analyst with all context already attached.

This is what agentic AI brings to fraud operations: not automation for its own sake, but automation that handles preparation work so human judgment can focus where it actually changes outcomes.

Human in the Loop AI Banking: Who Stays in Control

Human in the loop AI banking is the principle that automation handles routine decisions while humans handle exceptions. The question most risk teams ask is: where exactly is the line? The honest answer is that it depends on confidence thresholds and regulatory context.

A transaction flagged at 95% fraud confidence by a well-calibrated model with full explainability can often be auto-declined with a full audit trail and minimal regulatory exposure. A transaction flagged at 60% confidence in a cross-border context probably needs a human to review the SHAP attribution before any action is taken. Configurable ai autonomy lets the team set exactly those thresholds rather than accepting vendor defaults.

Configurable AI Autonomy: Setting Thresholds That Match Your Risk Tolerance

The difference between an AI system that helps and one that creates new problems often comes down to who controls the configuration. A system with configurable ai autonomy lets the compliance team set the confidence threshold above which alerts are auto-resolved, above which they are escalated to senior review, and above which they trigger automatic account restriction.

These aren't set-and-forget parameters. They change as fraud patterns shift, as regulatory guidance updates, and as operational capacity varies. When a new synthetic identity scheme emerges, the team can temporarily lower the auto-resolve threshold until they've characterized the pattern. When queue capacity is constrained, they can raise it to reduce manual volume without permanently changing the risk posture.

AI Audit Trail Automation for Compliance Teams

AI audit trail automation means every model decision, every automated action, and every threshold change is logged, timestamped, and queryable. Regulators don't just want to know what the model decided. They want to know what data it used, what the confidence level was, whether a human reviewed it, and what the outcome was.

Automated audit logging that captures all of this at decision time is far more reliable than reconstructing decisions from system logs after the fact. It also reduces the compliance team's workload significantly during regulatory examinations.

How Configurable Thresholds Reduce Review Fatigue

The most direct path from 70% false positive review time to something manageable is calibrating the confidence threshold for human review. If the model only escalates alerts when confidence exceeds 75%, and the model is well-calibrated, the analyst queue drops substantially without meaningful increases in missed fraud. Getting there requires a model that's accurate enough to trust, explainable enough to audit, and configurable enough to tune as conditions change.

The most direct path from 70% false positive review time to something manageable is calibrating the confidence threshold for human review.

What Regulators Actually Need from Your AI Models

Regulators don't object to AI in fraud and compliance operations. They object to AI that can't be audited, can't be explained, and can't demonstrate that it makes decisions consistently. The consistent regulatory requirement across jurisdictions is: document the model's purpose, its training data, how it makes decisions, how you monitor it for drift, and who reviews and overrides it.

The financial institutions that have the smoothest regulatory examinations aren't the ones with the most sophisticated models. They're the ones with the best documentation.

Building an Audit-Ready AI Documentation Framework

An audit-ready AI documentation framework for fraud detection covers four areas: model development records (training data, validation results, known limitations), decision documentation (per-decision SHAP data, confidence scores, threshold settings), override records (when a human overrode an automated decision and why), and monitoring records (how model performance is tracked over time and how the team responds to drift).

A unified risk platform that stores all four categories in a single searchable repository makes examination preparation a matter of running a report rather than stitching together evidence from five different systems.

AI Agents Financial Services: The Regulatory Perspective

Regulators are increasingly asking about ai agents financial services deployments specifically. The questions are predictable: who authorized the agent to take this action, what data did it use, was a human in the loop, and what is the escalation path when the agent makes a wrong call.

Institutions that can answer these questions with logged evidence are in a much stronger regulatory position than those who deployed agentic AI without governance documentation. The technology is the straightforward part. The governance is where most teams underinvest.

- Fraud alert fatigue in financial institutions isn't just an operational inconvenience.

- The point solutions vs platform financial services debate has a clear practical answer when you look at alert volume.

- A unified risk platform is a single system that ingests signals from fraud detection, identity verification, AML, and behavioral analytics, correlates them in a shared data layer, and surfaces one context-rich alert to the analyst instead of four separate notifications.

- Explainable AI finance is the practice of designing detection models so that decisions come with human-readable justifications.

- The connection between explainable AI compliance and alert volume is direct.

Onboard Customers in Seconds

Conclusion

Fraud alert fatigue in financial institutions is a solvable problem, but not by hiring more analysts or adding more detection rules. The path forward is a unified risk platform that correlates signals across fraud, identity, and compliance; an AI layer with genuine explainable AI compliance so analysts can make faster and more accurate decisions; and configurable automation that keeps humans in control where it matters most.

The 70% figure doesn't have to define your operations. Financial institutions that move from fragmented point solutions to a cohesive platform consistently report alert volume reductions of 50-80%, with analyst time shifting from queue management to actual investigation. That's where experience, judgment, and institutional knowledge actually get used.

If your team spends most of its day on alerts that go nowhere, the problem isn't your analysts. It's the architecture they're working with, and that's a fixable problem.

Share this article