.webp)

Listen To Our Podcast🎧

Introduction

Understanding fraud detection benchmarks 2026 starts with a hard truth: most financial institutions still measure their defenses by metrics that no longer reflect how attacks actually happen. Response time, accuracy, and cost are the three numbers that decide whether a fraud program protects revenue or quietly bleeds it. In our work with banks, fintechs, insurers, and supply chain firms, we have watched teams chase a single number, usually accuracy, while ignoring the latency and operational expense that determine real-world outcomes. This guide breaks down what good looks like across all three dimensions, why a unified risk platform now outperforms stitched-together point tools, and how to read vendor claims without getting fooled by lab numbers that never survive production traffic.

- What Are Fraud Detection Benchmarks 2026 Actually Measuring?

- How Fast Should Fraud Detection Respond in 2026?

- Accuracy Benchmarks: Beyond the False Positive Trap

- Cost Benchmarks and the Case for Vendor Consolidation Fintech Teams Need

- Why Explainable AI Finance Teams Trust Beats Black Box Accuracy

Onboard Customers in Seconds

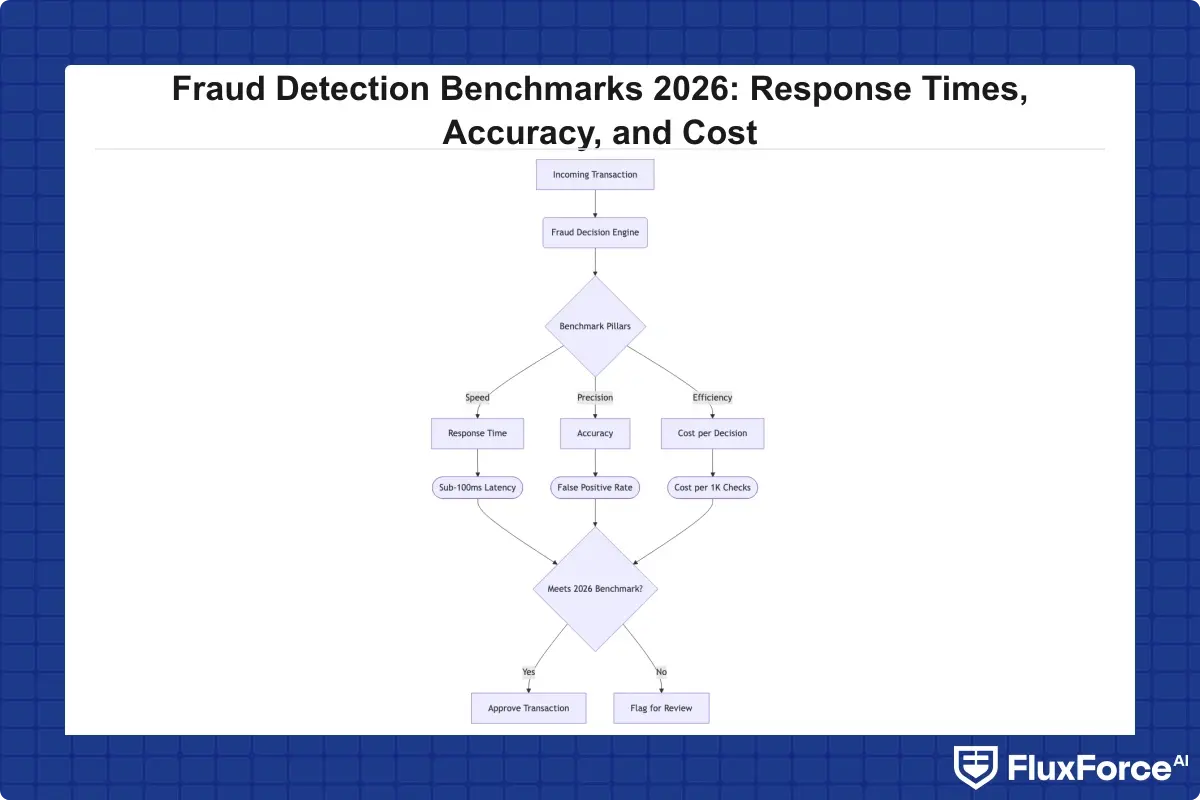

What Are Fraud Detection Benchmarks 2026 Actually Measuring?

Fraud detection benchmarks 2026 measure three linked variables: how fast a decision is returned (response time), how often that decision is correct (accuracy), and what it costs to run at scale (cost per decision plus operational overhead). A system that scores well on one and poorly on the others is not a good system, it is an unbalanced one.

The mistake we see most often is treating these as separate scorecards. They are not. Pushing accuracy higher usually adds model complexity, which raises latency and compute cost. Cutting latency often means simpler models that miss subtle fraud. The real benchmark is the tradeoff curve, not any single point on it.

Why single-metric scoring misleads buyers

A vendor quoting 99.5% accuracy tells you almost nothing without the false positive rate, the decision latency, and the traffic volume that number was measured against. According to the U.S. Federal Trade Commission, fraud losses reported by consumers continue to climb year over year, and most of that leakage happens not because models fail to flag fraud but because they flag too much legitimate activity and overwhelm review teams. High accuracy with a 6% false positive rate can cost more than moderate accuracy with a 0.5% rate.

A vendor quoting 99.5% accuracy tells you almost nothing without the false positive rate, the decision latency, and the traffic volume that number was measured against.

The three benchmark pillars defined

- Response time: end-to-end decision latency under production load, measured at the 95th and 99th percentiles, not the average.

- Accuracy: precision and recall together, with the false positive rate stated explicitly.

- Cost: total cost per decision, including compute, licensing, and the human review hours each false positive generates.

How Fast Should Fraud Detection Respond in 2026?

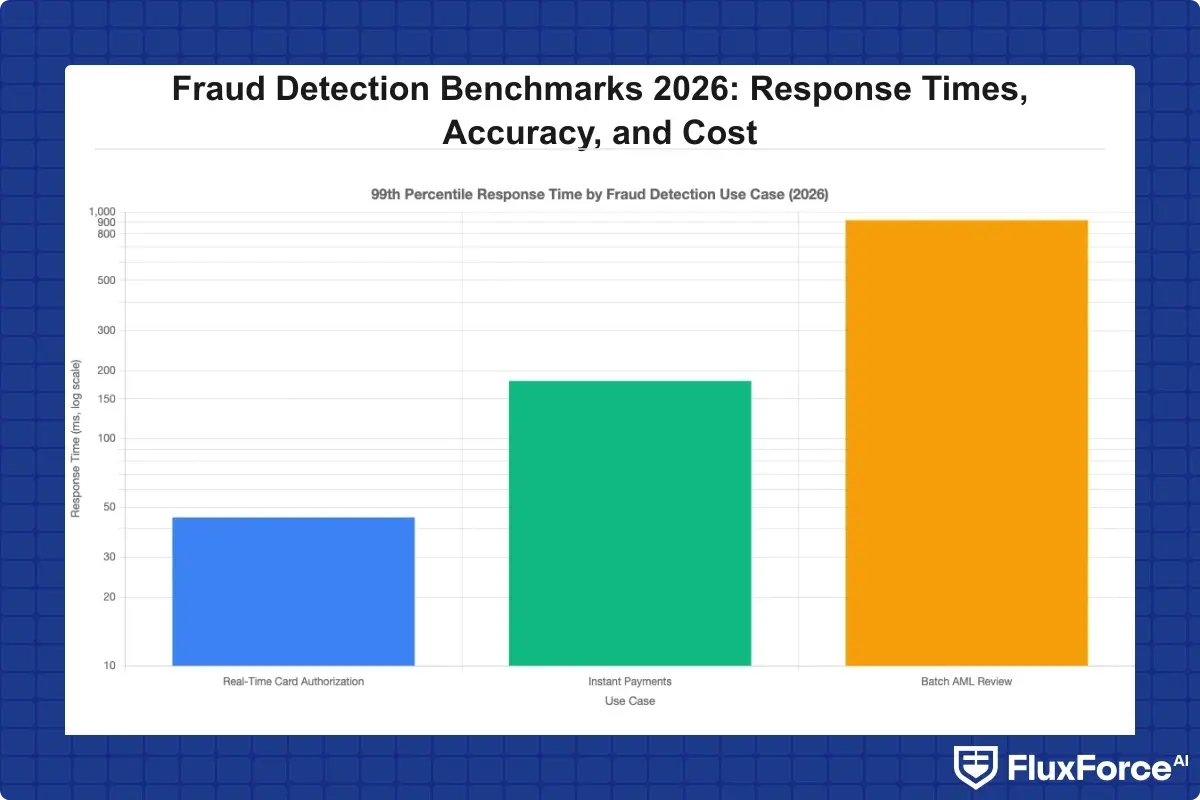

For real-time payments and card authorization, a competitive fraud decision should return in under 100 milliseconds at the 99th percentile. Anything slower starts to degrade the customer experience and, in instant payment rails, can miss the settlement window entirely.

The number that matters is tail latency, not the average. A system averaging 40ms but spiking to 800ms during peak traffic will time out exactly when fraud volume is highest. We benchmark at the 99th percentile because that is where customer abandonment and missed fraud actually live.

Real-time payments and the 100ms ceiling

Instant payment schemes give you a fixed window to approve or decline. An ai security operations platform that cannot hold sub-100ms latency under load forces a bad choice: slow the payment or skip the check. Neither is acceptable for a bank processing millions of transactions a day. Our team has seen institutions improve authorization speed simply by consolidating onto a fraud compliance identity platform that scores risk in a single pass rather than calling four separate vendors in sequence.

Batch versus streaming detection tradeoffs

Not every use case needs sub-second response. Anti-money-laundering reviews and suspicious-activity reporting can run in batch, where a few minutes is fine. The benchmark depends on the decision's blast radius. Match the latency target to the business consequence, and do not pay streaming prices for batch problems. For card-specific tuning, our breakdown of AI-powered card fraud analytics for risk heads covers how to set thresholds without throttling legitimate spend.

Accuracy Benchmarks: Beyond the False Positive Trap

The accuracy conversation in fraud detection benchmarks 2026 has shifted from catch rate to false positive control. Catching more fraud is easy if you do not care how many good customers you block. The hard part, and the real benchmark, is high recall with a false positive rate below 1%.

The hard part, and the real benchmark, is high recall with a false positive rate below 1%.

False positives are expensive twice over. They cost the review hours needed to clear each flagged transaction, and they cost customer trust when a legitimate purchase gets declined. We have seen teams cut false positives by double digits after moving from static rules to adaptive models, a shift detailed in our look at reducing false positives with agentic AI.

What a healthy false positive rate looks like

For card fraud, a mature program targets a false-positive-to-true-positive ratio near 5:1 or better, with leading platforms pushing below that. The benchmark is not zero false positives, which is impossible, but a ratio low enough that your review team can clear the queue within service-level targets.

Adaptive models versus static rules

Static rules age badly. Fraud patterns shift weekly, and a rule written six months ago is detecting last quarter's attack. Modern xai fraud detection pairs adaptive machine learning with explainability so analysts can see why a transaction scored high. This is the difference between a model that improves with feedback and one that decays the moment it ships. Our comparison of AI versus traditional fraud detection walks through where rule engines still help and where they actively hurt.

Cost Benchmarks and the Case for Vendor Consolidation Fintech Teams Need

Cost is the benchmark buyers underestimate most. The license fee is the visible number. The hidden cost is integration, maintenance, and the operational tax of running five point solutions that do not talk to each other. This is where vendor consolidation fintech leaders are pursuing pays off.

The point solutions vs platform financial services debate usually ends the same way once teams add up total cost of ownership. Each standalone tool needs its own integration, its own data pipeline, and its own vendor relationship. A unified risk platform collapses that overhead into one contract, one data model, and one decision layer.

Total cost of ownership, not license price

When you price a fraud program, count the people. Every false positive is a review-hour. Every disconnected tool is an engineer maintaining a brittle integration. According to Gartner, consolidating security and risk vendors is a top priority for enterprises specifically because tool sprawl inflates cost without improving outcomes. The cost benchmark that matters is cost per correct decision, fully loaded.

Point solutions versus a unified risk platform

Stitching together a fraud tool, an identity tool, and a compliance tool creates seams, and fraud lives in the seams. A fraud compliance identity platform that handles all three in one decision removes the gaps attackers exploit between systems. For teams weighing the build, our piece on manual compliance versus AI automation lays out the operational math behind consolidation.

Hidden costs of integration sprawl

The vendor consolidation fintech case is not only about license savings. It is about reducing the engineering hours lost to maintaining connectors between point solutions vs platform financial services architectures. Every integration is a failure point and a cost center. When you adopt fraud detection software that unifies signals, you cut both the attack surface and the maintenance burden in one move.

Why Explainable AI Finance Teams Trust Beats Black Box Accuracy

A model that scores well on accuracy but cannot explain its decisions is a liability in regulated finance. Explainable ai finance teams can stand behind is now a benchmark in its own right, because regulators increasingly require institutions to justify automated decisions that affect customers.

Black box ai compliance risk is real and growing. When a model declines a loan or freezes an account, the institution must explain why. Explainable ai compliance frameworks make that possible by surfacing the features that drove each decision.

What regulators expect from ai model explainability

Supervisors expect ai model explainability regulators can audit, meaning a clear, reproducible account of why a decision was made. Bodies such as the Bank for International Settlements have published guidance pushing for transparency in AI-driven financial decisioning. A model that cannot answer "why" fails this test regardless of its accuracy score.

SHAP values and feature attribution in practice

Techniques like shap values explained regulators can follow turn opaque model outputs into ranked feature contributions. When an analyst can show that a transaction scored high because of device mismatch plus velocity plus geolocation, that is defensible. Xai fraud detection built on feature attribution closes the gap between model performance and regulatory accountability. This same transparency helps with GDPR compliance automation in insurance, where automated decisions must be explainable to data subjects.

How AI Agents and Configurable Autonomy Change the Benchmarks

The arrival of ai agents financial services teams can deploy shifts what benchmarks even measure. Instead of scoring one transaction at a time, a multi agent ai system coordinates detection, investigation, and response across the fraud lifecycle.

Configurable ai autonomy is the control that makes this safe. You decide how much an agent can do on its own and where a human must approve. That dial, not a fixed setting, is what lets institutions adopt automation at their own risk tolerance.

Human in the loop AI banking still requires

Full autonomy is rarely the goal in regulated finance. Human in the loop ai banking workflows keep an analyst in the decision path for high-value or ambiguous cases. The benchmark here is how cleanly the system hands off to a human and how much context it provides when it does. An ai agent fraud detection workflow should escalate with a complete evidence package, not a bare alert.

Configurable AI autonomy as a control, not a feature

Configurable ai autonomy lets a CISO set strict human review for account closures while allowing the same multi agent ai system to auto-clear low-risk transactions. This tunability is becoming a core benchmark because one-size autonomy does not fit a regulated balance sheet. Our analysis of zero trust plus agentic AI in banking covers how these controls layer onto existing security architecture.

AI audit trail automation for accountability

Every autonomous action needs a record. Ai audit trail automation captures who, or what, made each decision and why, giving compliance teams a defensible log without manual note-taking. For ai agents financial services regulators scrutinize, the audit trail is the difference between adoption and rejection.

How to Run Your Own Fraud Detection Benchmark

Vendor numbers are marketing until you reproduce them on your own traffic. The only benchmark that counts is the one run against your transaction mix, your fraud patterns, and your latency requirements.

Build a representative test dataset

Use your real traffic distribution, including the rare fraud cases that matter most. A test set skewed toward easy fraud produces flattering numbers that collapse in production. Include the edge cases your point solutions vs platform financial services evaluation will actually face.

Measure latency under production load

Run the benchmark at peak volume, not in a quiet lab. Measure the 99th percentile response time of any ai security operations platform under realistic concurrency. A system that is fast when idle and slow under load fails the only test that matters.

Score accuracy and cost together

Never evaluate accuracy without cost. Calculate cost per correct decision, fully loaded with review hours, and compare that across vendors. This is how the unified risk platform case usually proves itself: not on a single metric but on the combined tradeoff. For payment-specific testing, our guide to secure payment gateway strategy for banking ops heads shows how to stage these tests safely.

- Fraud detection benchmarks 2026 measure three linked variables: how fast a decision is returned (response time), how often that decision is correct (accuracy), and what it costs to run at scale (cost per decision plus operational overhead).

- For real-time payments and card authorization, a competitive fraud decision should return in under 100 milliseconds at the 99th percentile.

- The accuracy conversation in fraud detection benchmarks 2026 has shifted from catch rate to false positive control.

- Cost is the benchmark buyers underestimate most.

- A model that scores well on accuracy but cannot explain its decisions is a liability in regulated finance.

Onboard Customers in Seconds

Conclusion

Fraud detection benchmarks 2026 reward institutions that stop chasing a single number and start measuring response time, accuracy, and cost as one connected tradeoff. The fastest path to better outcomes is consolidating point tools onto a unified risk platform, demanding explainable ai compliance teams can defend to regulators, and using configurable ai autonomy to automate at your own risk tolerance. The vendor consolidation fintech leaders are pursuing is not a cost-cutting exercise alone, it closes the seams where fraud hides. Run your own benchmark on real traffic before you sign anything, score accuracy and cost together, and insist on an ai audit trail automation layer that proves every decision. Start by mapping your current tools against these three pillars, then decide where consolidation buys you the most.

Share this article