.webp)

Listen To Our Podcast🎧

Generative ai fraud threats are no longer a theoretical exercise for security teams; they are active, production-level attacks hitting banks, fintechs, and insurers right now, and the institutions that treat them as a future problem are already paying for that assumption. In the past eighteen months, fraud teams have documented cases where large language models generated convincing phishing campaigns indistinguishable from legitimate internal communications, diffusion models cloned executive voices for wire transfer authorization calls, and synthetic identity pipelines manufactured applicants who passed automated KYC checks on the first attempt. This post covers what is actually happening, what it costs when defenses fail, and how to build a response architecture that does not become obsolete the next time attackers upgrade their tooling.

How Generative AI Has Changed the Fraud Threat Landscape

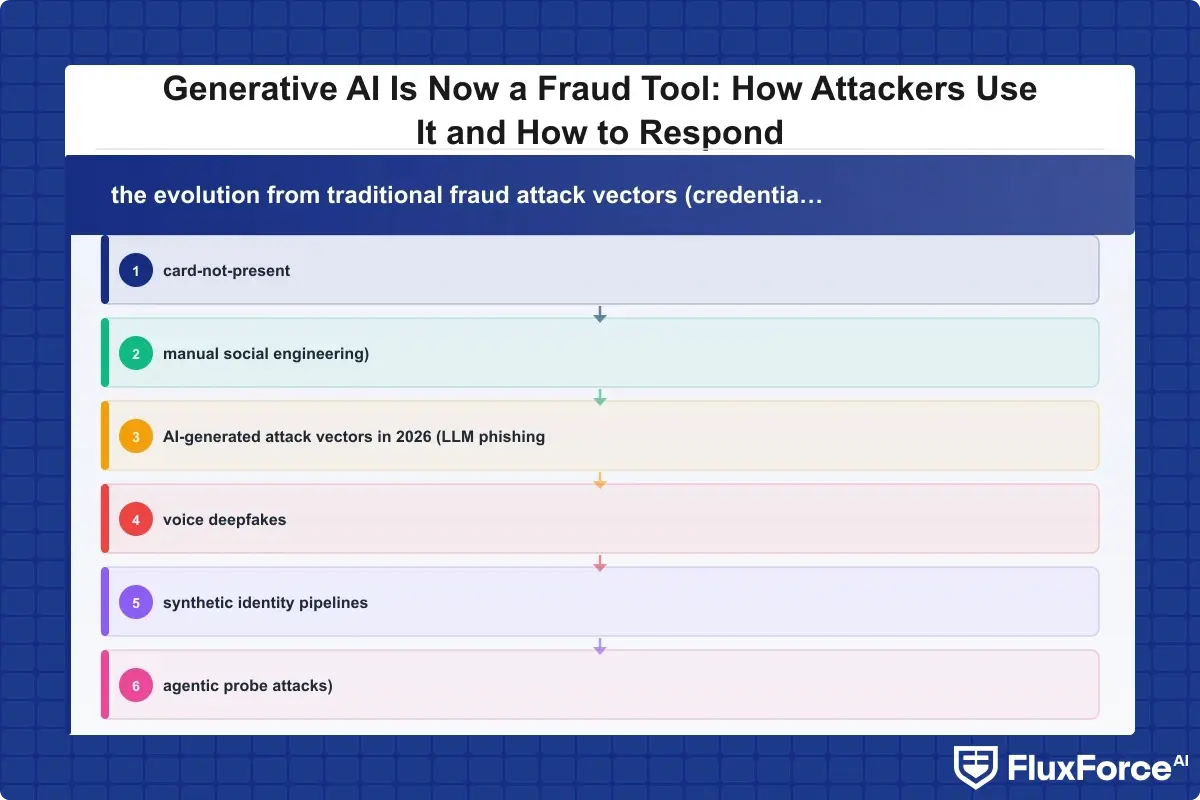

The fraud playbook was predictable for a long time: stolen credentials, card-not-present transactions, wire fraud through social engineering. Detection systems were built for that playbook. Generative AI rewrites it, and the rewrite is structural, not incremental.

Deepfake-Driven Identity Fraud

Deepfake audio can now be generated from as little as three seconds of voice sample, sourced from a LinkedIn video, a public earnings call, or a podcast appearance. Attackers use this to impersonate CFOs on wire transfer authorization calls, branch managers on account modification requests, and compliance officers on regulatory waiver approvals. In documented 2024 and 2025 incidents, firms lost between $250,000 and $35 million in single events before callbacks exposed the deception. For ai in banking 2026, voice-based authentication is no longer a safe fallback channel without additional liveness detection and behavioral verification layered on top.

The same diffusion model technology that generates audio can generate video. Real-time video deepfakes are not yet trivially accessible, but they are available to well-resourced fraud operations, and the cost curve is dropping. Security architects who are designing identity verification workflows in 2026 need to plan for video liveness checks that are resistant to real-time generation, not just static image fraud.

AI-Generated Phishing at Industrial Scale

Traditional phishing was detectable partly because of its volume and uniformity. Mass campaigns used the same template, the same grammatical errors, and the same sender domain patterns. LLM-generated phishing is different: each message is personalized using scraped LinkedIn, company website, and news data, tailored to the recipient's role and recent activity, written in flawless prose, and delivered at a cadence that mimics legitimate business communication. Fraud teams relying on signature-based email filtering will miss most of these campaigns. The FBI's Internet Crime Complaint Center documented over $12.5 billion in business email compromise losses in 2023, a figure that has risen as generative tools have lowered the barrier to entry.

The organizational impact goes beyond the direct loss. Each investigation pulls analysts off other work. Each incident triggers a regulatory notification review. The manual compliance cost of a single sophisticated BEC campaign, including investigation hours, legal review, and reporting, often exceeds the direct fraud loss for mid-market institutions.

Synthetic Identity Manufacturing at Scale

Synthetic identity fraud combines real data elements with fabricated ones to create identities that have credit history, address history, and behavioral patterns consistent with legitimate applicants. Generative AI accelerates this by producing plausible supporting documents, photo IDs that pass automated OCR quality checks, and social media histories that predate the loan application by years. Detecting synthetic identity fraud in real-time requires behavioral analytics that go well beyond document verification, because the documents themselves are increasingly indistinguishable from genuine ones when examined by legacy verification systems.

What Generative AI Fraud Costs Financial Institutions

Before discussing defense strategies, it is worth being direct about what is at stake financially. Fraud losses are the visible line item, but they are not always the largest cost for institutions with active fraud programs.

The Real Cost of Compliance in Financial Services

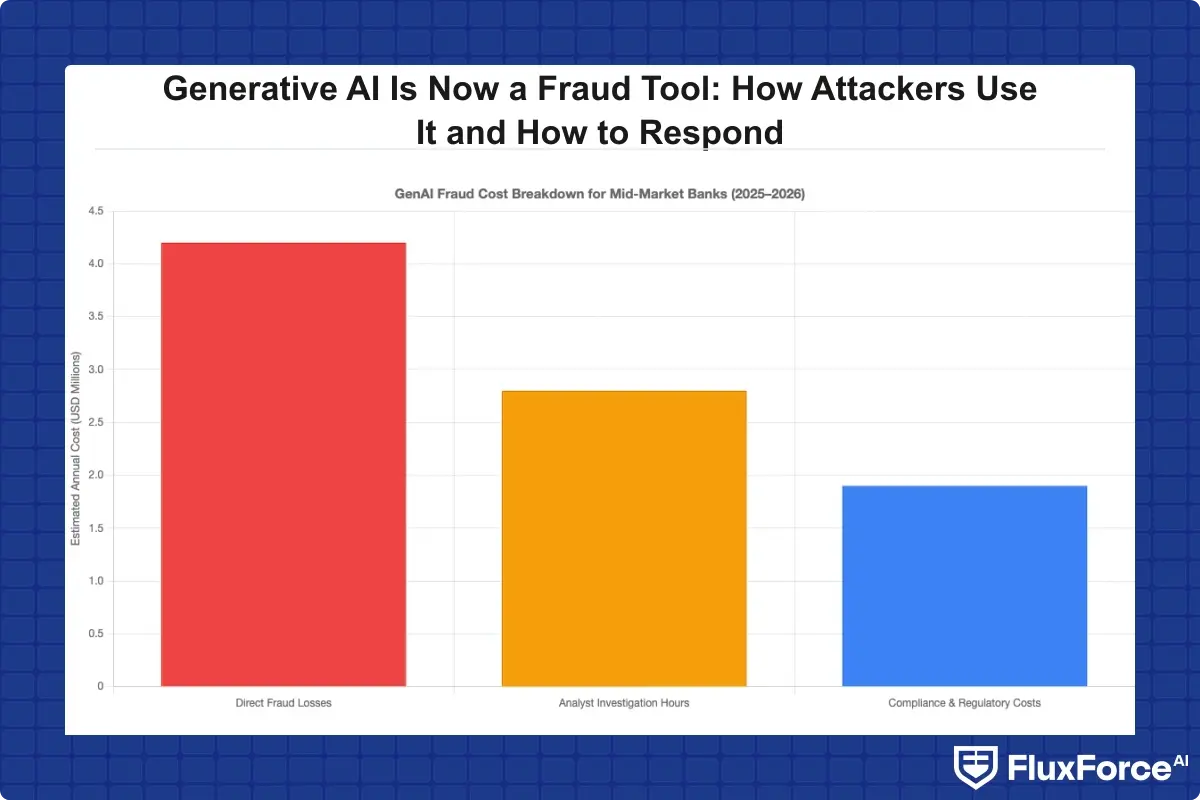

The cost of compliance in financial services runs to an average of $10,000 per employee annually at large institutions, according to estimates from compliance consulting and advisory firms. For a 500-person compliance department, that is $5 million per year in baseline manual compliance cost before any fraud-related remediation. When a generative AI attack generates a wave of suspicious activity that requires case-by-case analyst review, those costs spike because the volume of alerts exceeds what human teams can triage at reasonable accuracy.

Ai automation banking directly addresses this problem. Automated triage, pattern clustering, and case prioritization can reduce analyst workload by 40 to 60 percent on high-volume alert queues. The compliance automation roi is measurable within two to three quarters: fewer analyst hours per case, lower false-positive rates, and faster escalation on genuine threats reduce both the direct cost and the regulatory risk of slow response.

Total Cost of Ownership for a Fraud Platform

When evaluating any response strategy, the total cost of ownership fraud platform calculation matters as much as the headline licensing cost. A platform that requires 18 months of model tuning before it catches AI-generated synthetic identities is not a $200,000 investment. It is a $200,000 investment plus the cost of every fraud case that passes through during that tuning period, plus the analyst time spent managing false positives from an undertrained model.

Point-solution vendors consistently undercount integration complexity, retraining overhead, and the internal headcount required to manage model drift. Platforms with pre-built data connectors, automated retraining pipelines, and explainable AI outputs reduce that hidden cost substantially. Any vendor evaluation that does not include a total cost of ownership analysis across a 36-month horizon is likely to produce a misleading comparison.

Why Traditional Fraud Detection Fails Against Generative AI Attacks

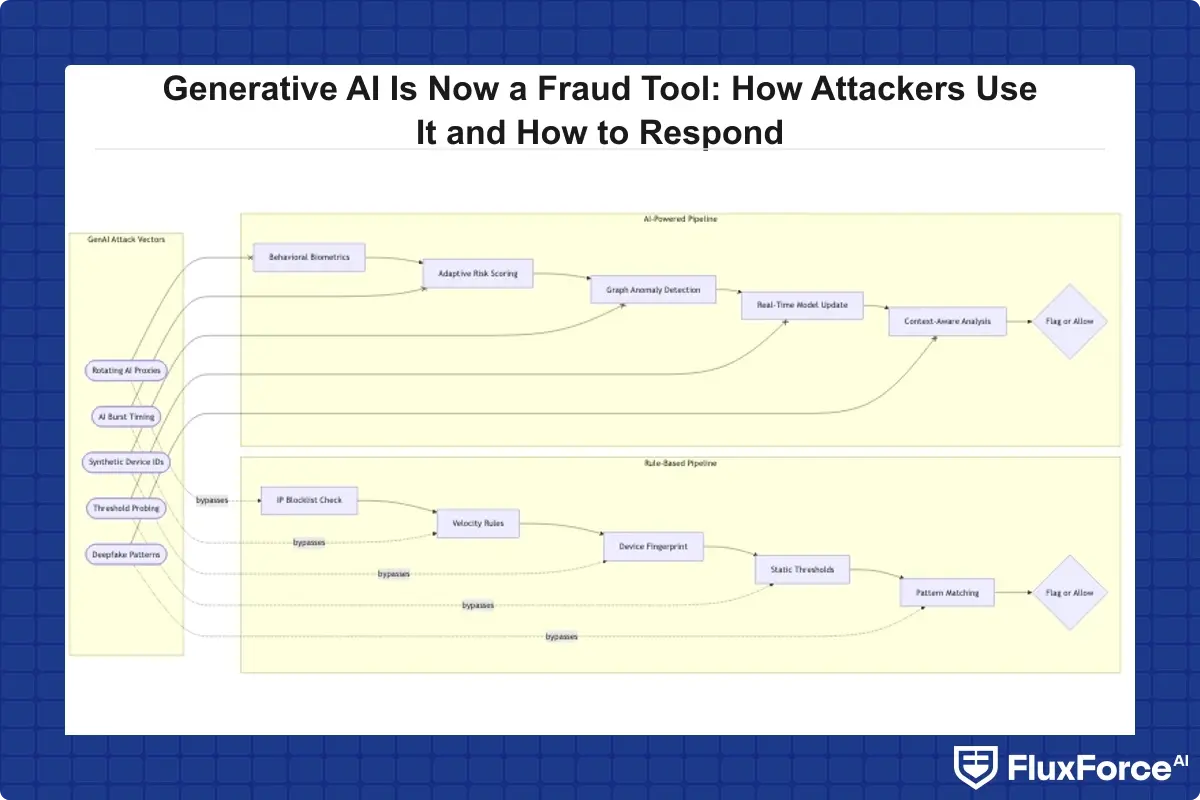

The core problem is a mismatch between detection architecture and attack velocity. Rule-based fraud systems are designed to catch patterns that human analysts identified in past campaigns. Generative ai fraud threats create novel patterns on demand, faster than rule libraries can be updated, and with built-in evasion logic that targets the detection gaps most systems leave open.

Rule-Based Systems Cannot Keep Up

A rule-based system flags a wire transfer because it exceeds a threshold, originates from an unusual IP address, or occurs outside business hours. A well-constructed agentic fraud attack avoids each of these triggers: it initiates the transfer during business hours, from an IP in the correct geographic region, for an amount below the threshold, after spending two weeks establishing behavioral history through smaller transactions that mimic the target's normal activity pattern.

AI vs. traditional fraud detection has been debated in the industry for years, but the emergence of generative AI attacks has made the outcome clear. Rule-based systems are not just less effective against these attacks; they are actively gameable by adversaries who can probe detection logic through automated trial-and-error at machine speed, iterating on attack variants until one passes through.

The False Positive Trap

There is a less visible failure mode that compounds the problem: false positives. When a fraud system is tuned conservatively to catch more attacks, it flags legitimate transactions. Analysts burn hours reviewing genuine activity. Operational cost grows. In response, institutions loosen detection thresholds, and the true positive rate falls. Generative AI attacks exploit this cycle by generating noise that forces threshold adjustments, then operating in the newly created blind spots.

Agentic AI fraud agents have cut false positives by 80 percent in documented production deployments by using contextual reasoning rather than threshold-based rules. That is not a vendor claim; it is a measurable outcome from institutions that have moved agentic architectures into live fraud queues.

How Agentic AI Banking Builds Effective Defenses

Agentic ai banking means fraud detection systems that do not just classify transactions but reason about them. An agent can follow a suspicious pattern across multiple data sources, build a hypothesis about what the attacker is attempting, test that hypothesis against behavioral history, and escalate with documented reasoning that satisfies audit requirements. That is qualitatively different from a scoring engine that fires when a transaction exceeds a risk threshold.

How Agentic AI Financial Services Works in Practice

Agentic ai financial services deployments typically run as a coordinated multi-agent architecture: one agent monitors transaction streams in real time, another maintains entity graphs mapping who transacts with whom and through what channels, a third tracks document authenticity signals and metadata consistency, and a supervisor agent correlates findings across all three before making a disposition decision. When the transaction agent sees an anomaly, the supervisor queries the entity graph and document agent before deciding whether to hold a transaction or pass it.

This architecture handles generative ai fraud threats differently from any previous system. A synthetic identity with clean transaction history and authentic-looking documents might fool each individual verification check. The agentic system catches it because the behavioral pattern of the entity graph looks wrong: the account was created recently, the counterparties are clustered in a way that suggests manufactured history, and the document metadata does not match the claimed issuing authority's known format conventions. No single signal triggers the flag. The reasoning across signals does.

Fraud Prevention ROI: The Numbers Behind the Promise

For institutions that have moved to agentic fraud detection, fraud prevention roi is typically calculated across three metrics: reduction in gross fraud losses, reduction in investigation cost per case, and reduction in regulatory penalty exposure. A mid-market bank processing two million transactions per month can see $3 to $5 million in annual fraud loss reduction combined with $1.5 to $2 million in operational savings from automated triage. That is a payback period under 12 months on most platform investments at those transaction volumes.

The comparison between manual compliance and AI automation is worth reviewing in detail for institutions still relying primarily on analyst-driven case review, because the gap in unit economics between the two approaches widens every quarter as generative AI attack volume grows.

AI in Banking Hype vs Reality: What Actually Works in 2026

The ai in banking hype vs reality question deserves a direct answer rather than a diplomatic one. There is genuine hype in vendor marketing, and there is genuine progress in deployed systems. The institutions that end up overpaying and underperforming are the ones that cannot tell the difference during a vendor evaluation.

What Vendors Overstate

Detection rates in controlled test environments rarely hold in production. A vendor demo that catches 99 percent of synthetic identities in a curated dataset may catch 70 to 80 percent in live traffic, where attackers have adapted to that specific model's known weak points. Any vendor who cannot show production metrics from institutions with similar transaction profiles and risk environments should be evaluated with skepticism, not enthusiasm.

Integration timelines are also routinely understated. Most enterprise fraud platforms require three to six months of integration work before they can ingest all relevant data sources at the fidelity the model needs to perform. Vendors who promise 30-day deployments are either scoping a very limited initial integration or delivering a system that does not yet have access to the full data picture. Teams conducting a FluxForce review or evaluating any other agentic fraud platform should include a detailed data integration assessment as part of the process, not as an afterthought.

What Is Actually Working in Production

Real-time behavioral biometrics are working. Systems that track how a user moves through an interface, their typing cadence, device orientation changes, and session timing patterns can detect account takeover within seconds of a compromised credential being used, before any transaction is initiated. This is particularly effective against AI-driven credential stuffing, which tends to produce device and session patterns that diverge from the legitimate account holder's baseline.

Graph analytics for entity relationship mapping are working. The future of ai in banking for fraud depends heavily on the ability to map relationships between accounts, devices, IP addresses, and transaction counterparties at scale. Generative AI can manufacture a single convincing identity. It is substantially harder to manufacture a coherent relationship network spanning hundreds of entities with plausible interaction histories. Graph-based detection catches the structural implausibility even when individual signals look clean.

Multi-modal document verification that combines OCR, metadata analysis, and generative artifact detection is working. The NIST AI Risk Management Framework provides a useful baseline for evaluating the reliability of AI systems used in high-stakes fraud adjudication decisions, and institutions should reference it when assessing vendor claims about detection accuracy and model robustness.

Building Your Response Plan for Generative AI Fraud Threats

A response plan for generative ai fraud threats has two distinct phases: immediate hardening of current systems and longer-term architectural change. Most institutions need both, sequenced correctly.

Immediate Hardening Steps

Audit voice-based authentication. Any process that uses voice recognition as a primary or secondary verification factor for high-value transactions needs additional steps. Multi-factor authorization for wire transfers above defined thresholds should include out-of-band confirmation through a pre-registered channel that cannot be intercepted through a deepfake call.

Review document verification for deepfake resilience. Check whether your KYC vendor uses active deepfake detection or is still relying on passive image quality scoring. For ai in banking 2026, passive quality checks are insufficient against AI-generated documents that score highly on resolution and formatting metrics while being entirely fabricated.

Establish a generative AI incident taxonomy. Your security operations team needs the ability to classify incidents by attack vector: LLM-generated phishing, voice deepfake impersonation, synthetic identity, and AI-assisted credential stuffing each require different investigation paths and different regulatory notification timelines. Without classification, you cannot measure trend or response effectiveness over time.

Evaluate your detection architecture against the current threat model. For institutions where rule-based scoring is still the primary fraud detection layer, the agentic AI and fraud detection capabilities offered by platforms like FluxForce represent a substantive architectural upgrade rather than a marginal improvement, specifically because they address the probe-and-evade attack pattern that rule-based systems cannot close.

Long-Term Architectural Changes

The long-term answer is an adaptive detection architecture built around these four capabilities:

- Continuous model retraining on current attack data, not quarterly or semi-annual cycles. Generative AI attackers iterate faster than quarterly retraining schedules.

- Entity graph integration that maps relationships across all transaction counterparties, devices, and channels, not just individual account behavior.

- Explainable AI outputs that let analysts understand and challenge model decisions, which is an increasingly explicit expectation from banking regulators. The FinCEN innovation guidance on AML compliance sets a useful regulatory context for institutions deploying AI in compliance-adjacent fraud workflows.

- Agentic coordination across fraud, AML, and KYC systems so that a synthetic identity flagged by fraud detection is automatically cross-checked against AML screening results and KYC document history without manual handoff.

For compliance teams working on the regulatory integration side alongside fraud detection, deploying regulatory compliance agents in a structured 90-day program provides a practical sequencing framework that aligns with how most enterprise security programs actually operate.

Onboard Customers in Seconds

Conclusion

Generative ai fraud threats are an active operational problem reshaping how attacks are constructed, how they scale, and how quickly detection gaps get exploited once identified. The institutions that absorb the least damage are those that move from reactive, rule-based detection to adaptive, agentic systems capable of reasoning across behavioral, documentary, and relational signals simultaneously rather than scoring each in isolation.

Fraud prevention roi in this context is not speculative. Documented production deployments show meaningful reductions in fraud loss, investigation cost per case, and regulatory risk within the first year of deployment. The question is not whether adaptive AI fraud detection pays for itself. It is how long your institution can afford to wait before making the move.

For teams evaluating where to begin, fluxforce ai offers a modular deployment approach that addresses the highest-risk generative AI attack vectors first without requiring a full platform replacement. The ai automation banking capability set in these platforms is built for the specific threat environment described in this post, and the architecture scales as the threat does.

Share this article