.webp)

Listen To Our Podcast🎧

Bust-out fraud detection sits at the top of most credit risk agendas in 2026, and for good reason. Organized fraudsters are no longer relying on stolen card numbers. They are building credit identities from scratch, maintaining spotless payment histories for 12 to 18 months, then draining every available credit line in a coordinated burst before disappearing. The FBI estimates that financial crime costs U.S. institutions hundreds of billions annually, with bust-out schemes among the hardest loss categories to prevent. For compliance officers and fraud operations teams, the question is no longer whether your institution will be targeted. It's whether your detection stack will catch it before the write-off hits the ledger.

What Is Bust-Out Fraud and Why Does It Keep Scaling?

Bust-out fraud is a type of credit fraud where an individual or organized ring deliberately builds creditworthiness over time, then rapidly maxes out credit lines with no intention of repaying. The term "bust-out" refers to the final phase: a sudden, high-velocity spend pattern that signals the fraudster is exiting the scheme.

What makes bust-out schemes particularly difficult to catch is the patience involved. Unlike a stolen card used immediately, bust-out accounts look identical to healthy accounts for months. They pay minimum balances, avoid large cash advances, and keep utilization within normal ranges. Fraud teams focused on transaction-level anomalies often miss these accounts entirely during the buildup phase.

The Profile of a Bust-Out Fraudster

Bust-out fraudsters fall into two categories. Individual fraudsters typically use their own identity but manipulate their credit profile through authorized user accounts, credit washing schemes, or dispute abuse. Organized rings, which cause far greater losses at scale, manufacture or steal complete identity profiles to open multiple accounts across lenders simultaneously.

The organized ring model is where synthetic identity fraud intersects with bust-out schemes. Fraudsters fabricate identities using real Social Security numbers, often belonging to children or elderly individuals, combined with manufactured name and address data. These synthetic profiles can sit dormant on credit bureau files for years before being activated for a bust-out run.

Why Synthetic Identity Fraud Makes This Worse

Synthetic identity fraud is the supply chain for modern bust-out operations. A single ring can manufacture hundreds of viable credit identities, seed them across multiple lenders, build their scores in parallel, and execute a coordinated bust-out event within days. According to the Federal Reserve's analysis of synthetic identity fraud, it is one of the fastest-growing financial crime categories, causing estimated losses in the tens of billions annually.

For bust-out fraud detection, this means your KYC checks at account opening are not sufficient on their own. An identity that passes every document verification check can still be synthetic, and a synthetic identity can behave impeccably for 18 months before draining a $30,000 credit line in 48 hours.

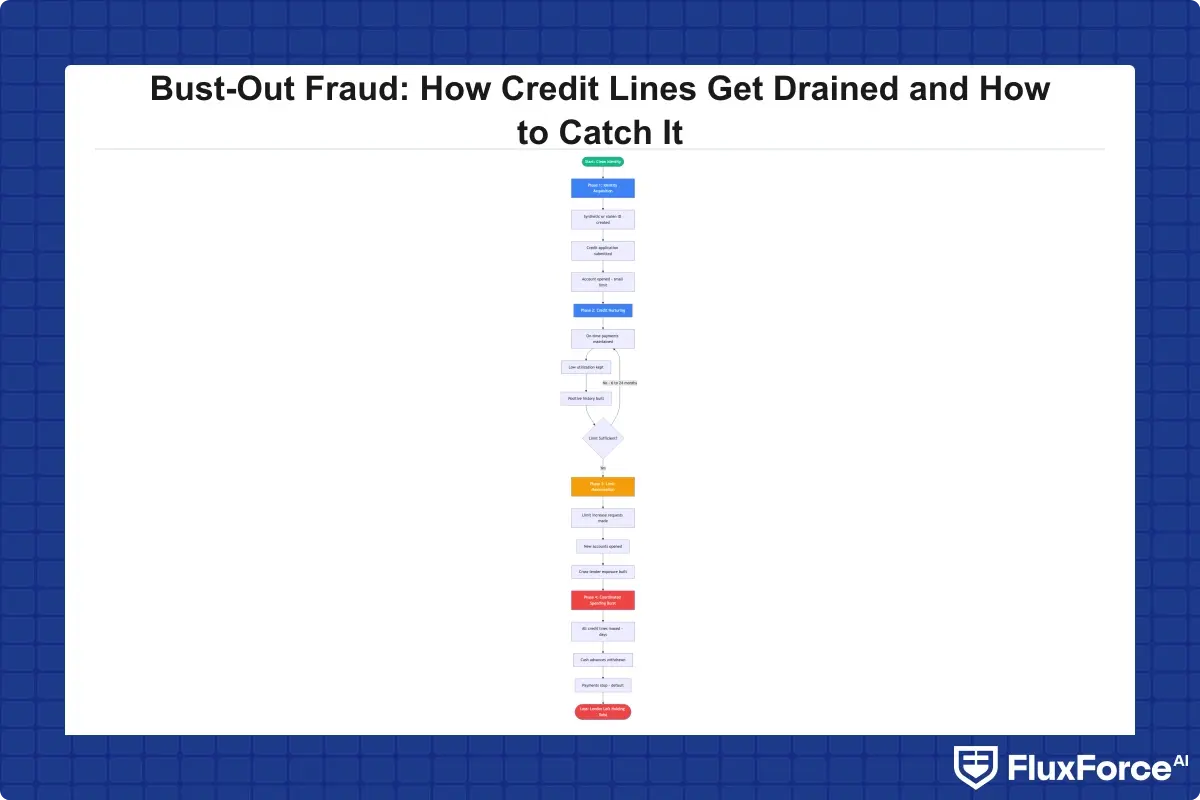

How Bust-Out Fraud Actually Works

Understanding the mechanics is the first step in building detection that holds. Bust-out schemes follow a recognizable arc even when individual executions look different on the surface.

The Four Stages of a Bust-Out Scheme

- Identity Acquisition. Fraudsters either create synthetic identities or assume real identities through data breaches, social engineering, or dark web purchases.

- Credit Building. Over 6 to 18 months, the account behaves normally: on-time payments, steady utilization, zero delinquencies. Some rings deliberately keep balances low to trigger automatic credit limit increases from lenders.

- Limit Maximization. Before the bust-out, fraudsters request limit increases across all linked accounts. This phase often looks like normal customer behavior, which is precisely the intent.

- The Burst. In a window of 48 to 72 hours, the fraudster maxes out all available credit through retail purchases, cash advances, wire transfers, and gift card transactions. Then the account goes silent permanently.

Behavioral Signals That Banks Miss

The signals are present during stages one through three, but they are subtle. Velocity of credit inquiries across multiple lenders, shared device fingerprints across ostensibly unrelated accounts, thin-file patterns despite a multi-year credit history, and geographic inconsistencies in spending all point to elevated risk. Traditional rule-based transaction monitoring software catches the burst in stage four, which is already too late. The credit has been disbursed and the fraudster is gone.

Why Traditional Transaction Monitoring Software Misses Bust-Out Patterns

Most transaction monitoring software was built to catch discrete transactional fraud: a stolen card at a point of sale, an unauthorized wire transfer, or a phishing-triggered account takeover. Bust-out fraud is structurally different because harm accumulates across time, not within a single transaction.

Rule-Based Systems and Their Blind Spots

Rule-based systems look for threshold violations: transactions above a set dollar amount, unusual merchant categories, or geographic outliers. A bust-out account in stage two triggers none of these. Payments are small and regular. Merchant categories are ordinary. Geographic patterns match the stated address on file.

The core problem is that rule-based systems are static. Fraudsters learn the thresholds and design their behavior to stay just beneath them. As a direct comparison of rule-based systems versus AI transaction monitoring shows, institutions relying solely on static rules face a widening detection gap as fraud tactics adapt faster than compliance teams can update alert configurations.

The Transaction Monitoring Cost of Manual Reviews

There is also a practical operational problem that compounds the detection gap. Manual review queues grow faster than analyst capacity. The transaction monitoring cost per SAR filing at a mid-sized bank can exceed $1,500 when analyst time, escalation workflows, and documentation are included. Fraud alert fatigue sets in quickly when analysts spend the majority of their queue on false positives that go nowhere.

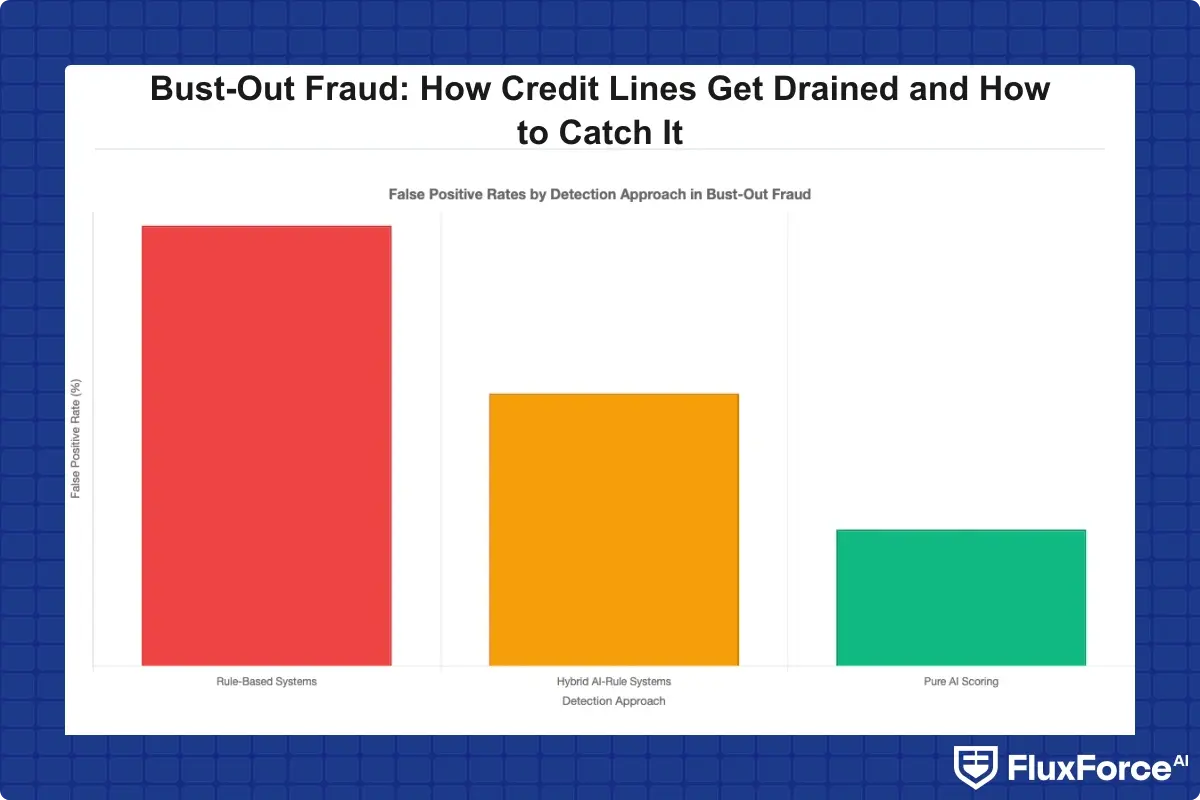

The false positive rate in traditional AML and fraud monitoring systems averages between 95% and 99%. That means for every real bust-out case in the queue, analysts wade through dozens of false alarms first. By the time the genuine signal surfaces, the fraudster has already been gone for days.

How AI Fraud Detection Catches What Rules Miss

AI fraud detection explained: machine learning models are trained on historical fraud patterns, then applied to incoming transactions and account behaviors in real time. Unlike rules that evaluate single transactions in isolation, ML models assess dozens of behavioral features simultaneously and detect patterns no human analyst could manually track at scale.

How Does AI Detect Fraud in Credit Line Abuse?

How does AI detect fraud in bust-out schemes specifically? The core mechanism is behavioral pattern matching across time. Instead of asking "is this transaction unusual?", an AI model asks: "Is this account's behavior over the last 90 days consistent with a healthy borrower profile, or does it resemble patterns observed in confirmed bust-out cases?"

This evaluation includes features like:

- Payment timing distributions. Bust-out accounts often pay exactly on the due date, never early, to preserve available cash for the eventual burst.

- Cross-account network signals. Shared phone numbers, email domains, device IDs, or IP address clusters across accounts indicate coordinated ring activity.

- Utilization trajectory. A gradual, deliberate ramp in utilization across multiple accounts in the months before a bust-out follows a recognizable curve that supervised models can identify.

- Merchant category sequencing. Bust-out spending bursts often follow a specific order (cash advances, then gift cards, then electronics) that differs from typical high-spend customer events.

Machine Learning Fraud Detection Models That Work

Not all ML approaches work equally well for bust-out fraud detection. Supervised models trained on labeled fraud cases need a sufficient volume of confirmed bust-out examples, which smaller institutions may lack. Unsupervised anomaly detection can surface novel patterns but tends to produce more false positives fraud detection teams struggle to action without careful threshold tuning.

The most effective approach for AI fraud detection in banking combines supervised models for known bust-out patterns, graph analytics for network-level relationship mapping, and unsupervised clustering to catch emerging schemes that don't match historical templates. AI fraud detection software powering modern fraud stacks typically layers all three methods. Platforms evaluated in sardine vs unit21 comparisons and similar vendor analyses consistently show that graph-based detection, specifically the ability to map relationships between accounts sharing device IDs or phone numbers, is the single highest-impact capability for bust-out identification.

Real-Time Fraud Detection: Why Speed Is the Deciding Factor

The bust-out burst happens fast. In documented cases, fraudsters have drained multiple credit accounts within a 36-hour window. Real time fraud detection is not a luxury for bust-out prevention; it is a technical requirement. Detecting the pattern on a nightly batch run means the institution is always one morning behind a fraud event that concluded yesterday.

Real-Time Fraud Detection in Banks: Practical Architecture

Real time fraud detection banks deploy today typically involves three layers working in sequence. The first is a streaming pipeline that ingests transaction events with sub-100ms latency. The second is a scoring engine running behavioral models against incoming events, including the full account history context. The third is an alert routing system that sends high-confidence fraud signals directly to automated blocking actions rather than human review queues.

The shift from legacy systems is the move from batch scoring, running models once per night, to event-driven scoring, running models on every transaction as it occurs. For ai fraud detection in banking environments processing millions of daily transactions, this architecture demands both low-latency infrastructure and model inference pipelines optimized for speed without sacrificing accuracy.

Automated Transaction Monitoring in Action

Automated transaction monitoring changes the economics of fraud operations in a measurable way. Instead of analysts reviewing every flagged account, automation handles tier-one decisions: accounts scoring above a high-confidence threshold are flagged for immediate credit line suspension, while mid-range scores go to a prioritized review queue with full context attached.

This is how payment fraud prevention scales without linear headcount growth. A fraud team of 10 analysts can effectively monitor 500,000 accounts with the right automated transaction monitoring platform, because the system pre-filters the queue to the highest-risk items. Institutions that deploy full automation at the tier-one level consistently report 60% to 70% reductions in manual review volume without increasing miss rates.

Reducing False Positives in Bust-Out Fraud Detection

False positives fraud detection is not just an operational nuisance. Every false positive is a legitimate customer whose card gets declined, whose account gets flagged for review, or who receives an unexplained call from their bank. The reputational and churn cost of frequent false positives is significant, and it is a reason many institutions hesitate to tighten detection thresholds even when they know their current settings are too loose.

The Real Cost of a High False Positive Rate in Fraud Detection

False positive cost fraud teams in ways that don't always appear on a single budget line. Direct costs include analyst time per review, system compute, and case documentation requirements. Indirect costs include customer experience damage, account churn from frustrated legitimate customers, and the opportunity cost of analysts spending hours on non-fraud cases instead of genuine investigations.

The false positive rate fraud detection teams consider acceptable has dropped substantially as ML-based scoring matures. Institutions using AI-driven scoring report false positive rates of 20% to 40%, compared to the 95%+ rates common in legacy rule-based systems. That reduction represents dozens of analyst hours per week redirected to genuine investigations. The post How Agentic AI Fraud Agents Cut False Positives by 80% covers the operational mechanics in detail. Context-aware AI agents that evaluate the full account history before issuing an alert produce dramatically fewer false positives than single-transaction rule evaluations.

How to Reduce False Positives in AML Without Sacrificing Coverage

The practical question is: how to reduce false positives in AML without creating detection blind spots? The answer is model segmentation. Rather than applying a single scoring model to all accounts, effective implementations segment customers by risk tier and apply different alert thresholds to each tier.

A new account with thin history and high application velocity warrants a lower scoring threshold, meaning the system flags it earlier on weaker signals. An established customer with a five-year clean history warrants a higher threshold, only alerting on very strong signals. This segmentation approach can reduce false positives in transaction monitoring by 30% to 50% without reducing fraud catch rates, because it aligns detection sensitivity with the actual risk profile of each customer segment.

Reducing false positives transaction monitoring further requires building feedback loops into the model pipeline. When analysts dismiss an alert as a false positive, that signal should feed back into the model as a negative training example. FinCEN's guidance on risk-based AML programs explicitly supports this kind of calibrated, customer-profile-aware approach over uniform rule thresholds applied across all accounts.

Building a Bust-Out Fraud Detection Strategy That Holds

Bust-out fraud detection is not a one-time implementation project. It is an ongoing program requiring coordination across credit risk, fraud operations, compliance, and technology teams who don't always share data or objectives.

Choosing the Right AI Fraud Detection Software

When evaluating AI fraud detection software for bust-out use cases, the criteria that matter most are: ability to ingest and score behavioral signals over a 90-day to 18-month lookback window, graph analytics capability for network-level relationship mapping, real-time scoring latency under 200ms, and a demonstrated false positive rate below 30% on the institution's own historical data.

Platforms should also support model explainability so fraud analysts can understand why a specific account was flagged. Black-box scores that analysts can't interpret lead to low alert-action rates and, over time, to the fraud alert fatigue that erodes confidence in the entire detection program. AI fraud detection software without explainability is a tool your team won't trust, and a tool your team doesn't trust doesn't get used.

Payment Fraud Prevention Beyond the Card Layer

Bust-out fraud often culminates in cash advances and wire transfers, not just card purchases. Payment fraud prevention strategies focused only on card transactions miss the endgame of many bust-out schemes. Effective programs extend transaction monitoring to ACH transfers, wire requests, and digital wallet funding events where bust-out fraudsters often move the largest amounts.

For institutions underwriting lending products, bust-out patterns can even appear in loan prepayment behavior. Fraudsters sometimes pay down balances strategically before the burst to free up additional credit. Monitoring cross-product behavior closes this gap. This is also why AML and fraud functions need to share data pipelines. AML programs monitoring for structuring and layering will sometimes surface accounts that fraud teams should be watching for bust-out signals. Integrating these pipelines, as discussed in our guide to AML screening and monitoring for payments risk officers, is one of the higher-leverage improvements most institutions haven't prioritized yet.

Onboard Customers in Seconds

Conclusion

Bust-out fraud detection requires a fundamentally different approach than traditional card fraud prevention. The fraud happens over months, the signals are subtle during the buildup phase, and by the time a transaction-level alert fires, the losses are already locked in. Institutions that are catching bust-out schemes before the burst have made three specific changes: they've moved from rule-based to AI fraud detection, they've built real-time scoring infrastructure, and they've invested in reducing false positives so their analysts trust and act on the alerts they receive.

If your current fraud stack still relies primarily on static rules and nightly batch processing, bust-out fraud is almost certainly slipping through. The technology to close that gap is accessible to institutions of all sizes. The only question is whether you act before the next organized ring identifies your credit lines as a target, or after the write-off lands on the quarterly loss report.

Share this article