.webp)

Listen To Our Podcast🎧

Passkeys banking FIDO2 is no longer a pilot program for tech-forward credit unions. It is the authentication standard that tier-one banks are actively deploying in 2026 to stop account takeover attacks that cost the industry an estimated $11 billion annually. Unlike passwords, passkeys use public key cryptography tied to a user's device and biometric identity verification, meaning there is no shared secret to steal, phish, or brute-force. This post breaks down how FIDO2 works inside a banking context, why it matters for compliance and fraud teams already fighting synthetic identity fraud and deepfake-driven attacks, and what your security architecture needs before rolling out passkeys at scale.

What Are Passkeys and How Does FIDO2 Work in Banking?

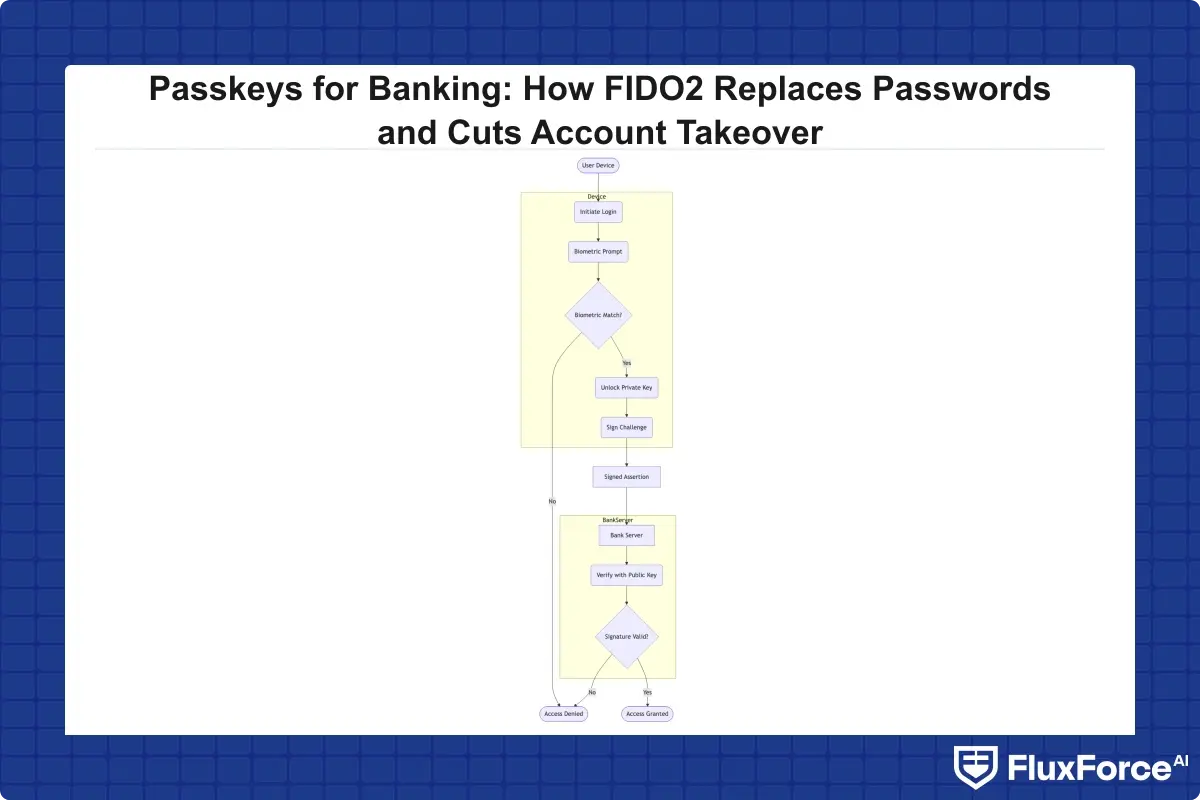

Passkeys are cryptographic credentials stored on a user's device: a phone, laptop, or hardware key. When a customer logs in, the device generates a digital signature using a private key that never leaves the hardware. The bank's server verifies the signature against a stored public key. No password is transmitted. No shared secret sits on the server that an attacker can breach.

How the FIDO2 Protocol Works

FIDO2 is the umbrella standard published by the FIDO Alliance that combines two specifications: WebAuthn (a W3C standard for browser-based authentication) and CTAP2 (Client to Authenticator Protocol, which lets external hardware keys communicate with devices). Together they allow browsers and native apps to call the device's authenticator, whether Face ID, a fingerprint sensor, or a hardware security key, without routing credentials through the server.

The authentication flow works like this:

- The user navigates to their bank's login page or mobile app.

- The app sends a cryptographic challenge to the device.

- The device prompts for biometric verification (face or fingerprint).

- On success, the private key signs the challenge.

- The signed response goes back to the server for verification.

- The server checks the signature against the stored public key and grants access.

No password was typed. No OTP was sent via SMS. No phishing page can intercept a credential that was never transmitted.

Public Key Cryptography Explained Simply

Think of it as a padlock system. The bank holds the open padlock (public key). The customer holds the only key that can lock and unlock it (private key). Even if someone steals the padlock, they cannot open it without the customer's private key, which never leaves their device. The W3C WebAuthn specification formalizes this model for web and app developers building authentication into banking products.

How Passkeys Banking FIDO2 Eliminates Account Takeover Risk

Account takeover attacks rely on one fundamental weakness: shared secrets. Passwords can be phished, leaked in data breaches, or purchased on dark web marketplaces. One-time passwords sent via SMS are vulnerable to SIM-swapping. Passkeys banking FIDO2 removes these attack vectors entirely because there is nothing to steal from the server side.

Why Passwords Are the Primary Attack Vector

According to NIST Special Publication 800-63B, memorized secrets remain the most commonly exploited authentication factor. Credential stuffing attacks succeed because an estimated 65% of users reuse passwords across multiple services. A single breach at a retail site can cascade into banking fraud within hours.

Passkeys are phishing-resistant by design. The cryptographic binding between the credential and the origin URL means a passkey registered for your bank's domain will not respond to a lookalike phishing domain. That attack surface simply does not exist with FIDO2.

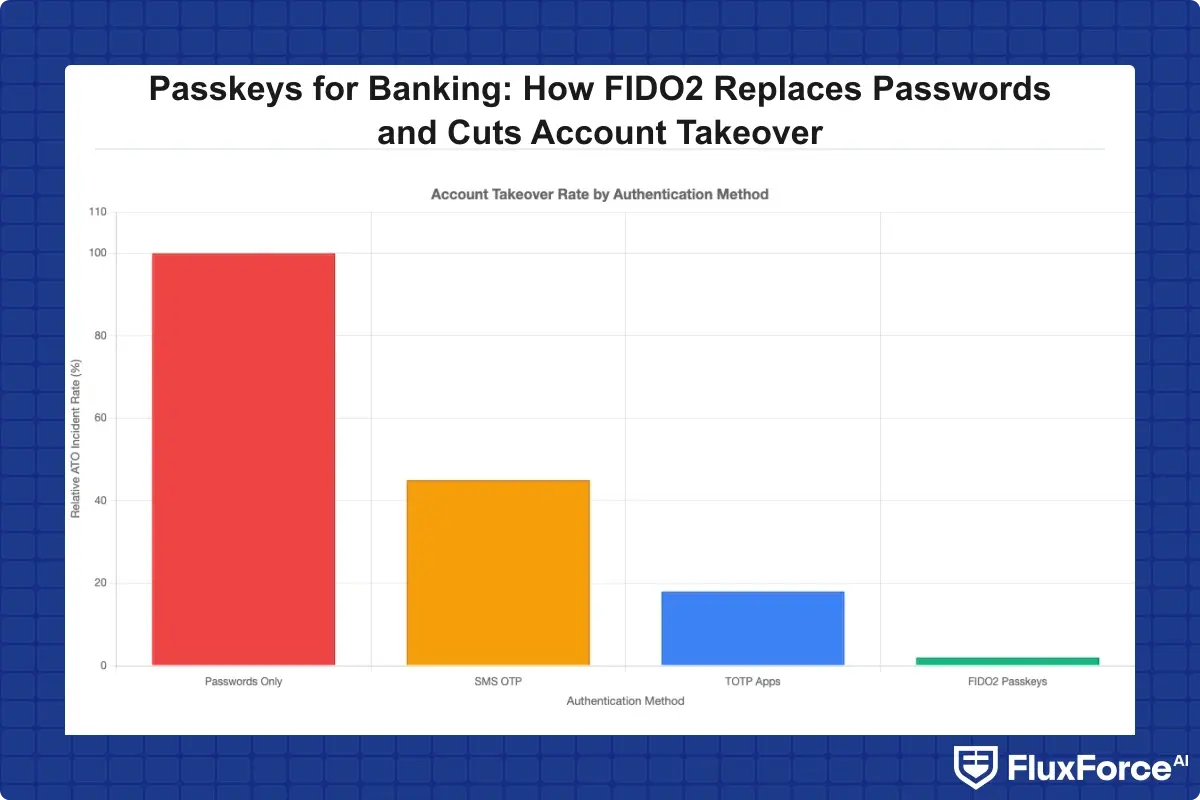

Account Takeover Statistics in Banking

The scale is significant. ATO losses in US banking exceeded $11 billion in 2023. Financial institutions that have deployed FIDO2 authentication report up to 99% reductions in phishing-based account takeovers in pilot cohorts. The economics are compelling: preventing one ATO incident typically saves between $1,500 and $8,000 in investigation, remediation, and customer restitution costs.

For CISOs evaluating authentication infrastructure, the total cost of ownership for passkeys is also lower than maintaining legacy MFA systems that require SMS gateway contracts, OTP delivery infrastructure, and helpdesk support for locked-out users.

Biometric Identity Verification: The Engine Behind Passkeys

The reason passkeys feel fast and frictionless is biometric identity verification. On most modern devices, a fingerprint scan or face recognition completes in under 500 milliseconds. The biometric never leaves the device. It is used locally to unlock the private key, not to authenticate against a remote database.

Biometric Identity Verification on Mobile Devices

Mobile banking is where the biometric advantage is most visible. When a customer opens their banking app, Face ID or a fingerprint sensor handles authentication in a single gesture. There is no typing, no waiting for an SMS, no authenticator app to open. Login drop-off rates, a metric that directly affects customer retention, fall significantly when friction decreases.

This local biometric model also has compliance benefits. Because biometric data is processed on-device and never sent to the bank's servers, institutions avoid storing biometric templates, which are subject to stringent regulations in states like Illinois (BIPA) and Texas (CUBI Act). That reduces regulatory exposure while improving the customer experience.

How Does Biometric Verification Prevent Credential Theft?

Biometric identity verification in the FIDO2 model is not a replacement for the cryptographic key. It is the gatekeeper that unlocks it. Even if an attacker has physical access to a user's phone, they cannot use the passkey without passing the biometric check. This creates true two-factor authentication in a single gesture: something you have (the device) and something you are (biometric).

For enterprise financial institutions concerned about liveness detection fraud, most modern device authenticators include anti-spoofing measures that reject static photos or 3D masks. But device-level liveness is not sufficient for high-risk transactions or account opening, which is where layered digital identity proofing becomes necessary.

Why KYC Onboarding Speed Improves with FIDO2

One of the underrated benefits of passkeys is the measurable improvement in KYC onboarding speed. Traditional onboarding flows require customers to set a password, enroll in MFA, verify their email, and sometimes call a support line when locked out. Each additional step cuts conversion rates.

Digital Identity Proofing at Enrollment

The critical moment in passkey deployment is not login. It is the initial digital identity proofing step. Before the bank creates a passkey credential for a customer, it must verify that the person enrolling is who they claim to be. This is where identity verification fintech solutions do the heavy lifting: document verification, liveness checks, and database cross-referencing happen in one orchestrated flow.

Done well, this enrollment step takes 2 to 3 minutes and replaces weeks of back-and-forth document submission in legacy onboarding. The customer creates their passkey during enrollment, and every subsequent login takes under a second. The one-time investment in digital identity proofing pays dividends across every future session.

How Passkeys Reduce Drop-Off Rates in Onboarding

Onboarding abandonment in digital banking typically runs between 40% and 60%. Password fatigue, SMS OTP delays, and document upload friction are the primary causes. When KYC onboarding speed improves because the authentication method itself is frictionless, completion rates climb. Some digital banks report 30% improvement in onboarding completion after switching to passkey-first flows.

For compliance officers, this is also a risk reduction story. Faster, cleaner onboarding means fewer customers using workarounds like shared passwords or skipping MFA enrollment entirely, which creates audit gaps that examiners flag.

Liveness Detection Fraud and Deepfake Detection Banking Challenges

Passkeys solve the credential problem. They do not automatically solve the identity problem at enrollment. This is where liveness detection fraud prevention and deepfake detection banking capabilities become non-negotiable for any institution opening accounts digitally.

What Is Liveness Detection and Why Does It Matter?

Liveness detection determines whether the face presented to a camera is a live human being or an artifact: a printed photo, a video replay, or a 3D mask. Passive liveness detection analyzes subtle cues, including micro-movements, skin texture, and depth, without asking the user to perform any action. Active liveness detection prompts the user to blink, turn their head, or smile to confirm presence.

In banking, liveness detection fraud occurs when attackers use deepfake-generated faces or high-quality photos to bypass selfie verification during account opening. A system without certified liveness detection can be fooled in minutes by anyone with access to a target's social media photos.

Deepfake Detection Banking: The Growing Threat

Deepfake technology has reached a level of sophistication where AI-generated faces can fool basic selfie-capture systems. The deepfake detection banking challenge is that these tools are now commercially available and require minimal technical skill to deploy in an attack sequence.

Effective deepfake detection banking systems use a combination of passive liveness, injection attack detection (catching synthetic video streams injected directly into the camera API), and behavioral signals collected during the onboarding session. No single technique is sufficient on its own. Layering multiple detection methods raises the cost of attack to a point where most fraudsters move to easier targets.

For institutions thinking about where deepfake threats intersect with broader fraud vectors, the post on detecting synthetic identity fraud in real-time covers the full detection pipeline in more depth.

Synthetic Identity Fraud Detection in a Passkey-First World

Passkeys close the authentication gap. But synthetic identity fraud detection addresses a different threat: fraudsters who create entirely fictitious identities, combining real Social Security numbers with fabricated names and addresses, to open accounts that will never be used for legitimate purposes.

Synthetic Identity Fraud Detection: Closing the Loopholes

Synthetic identity fraud detection requires analysis at enrollment, not at login. The fraud pattern is: open an account with synthetic credentials, build a credit history over months or years, then max out credit lines and disappear. By the time the synthetic identity fraud is detected, the loss has already occurred.

FIDO2 passkeys do not prevent synthetic identity fraud on their own. If a fraudster completes enrollment using a convincing synthetic identity, they will successfully create a passkey. What stops synthetic identity fraud is the quality of the identity verification API and the data signals checked during onboarding.

Effective checks include:

- Cross-referencing the provided SSN against credit bureau records for age-of-file anomalies

- Checking whether the identity document shows signs of tampering or AI generation

- Running behavioral biometrics during the onboarding session to detect bot-driven form filling

- Comparing device fingerprints against known fraud ring profiles

Institutions that deploy KYC/AML automation alongside passkey enrollment see material reductions in synthetic account opening rates. The identity verification layer does the work before the passkey credential is ever created, which means the downstream authentication channel stays clean.

Zero Trust Financial Services: Where Passkeys Fit

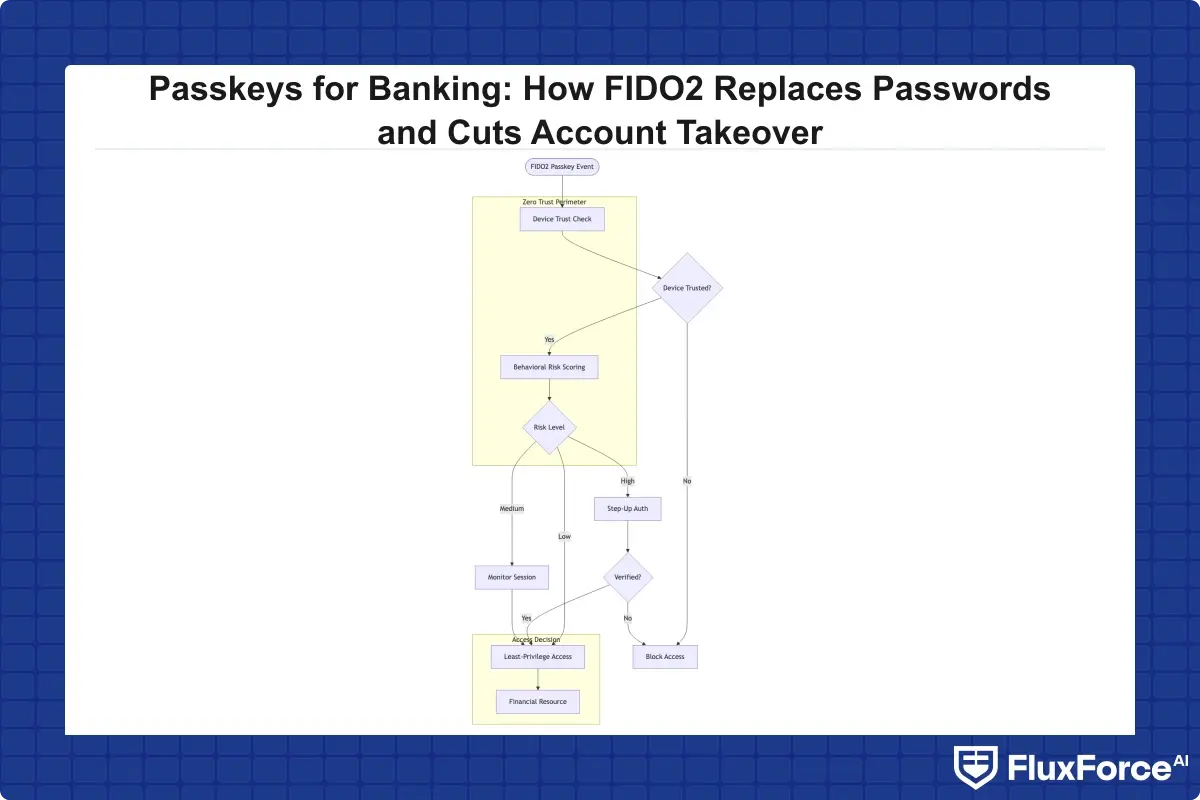

Passkeys are a natural fit for the zero trust security framework because they provide cryptographic proof of identity at every authentication event. Zero trust financial services architectures operate on the principle that no user, device, or session is trusted by default. Every access request must be verified continuously, not just at initial login.

Zero Trust Security Framework and Passkey Architecture

In a zero trust security framework, authentication is one layer among several. Passkeys handle the "prove who you are" step. Beyond authentication, zero trust requires additional controls running in parallel:

- Device trust: Is this a managed, compliant device? Passkeys are bound to specific devices, so device attestation data flows naturally alongside the authentication event, giving the access control layer signal about device health.

- Continuous behavioral analysis: Post-login behavior is monitored. Passkeys can be combined with risk scoring to trigger step-up authentication for high-value actions like large wire transfers or beneficiary changes.

- Least-privilege access: Users access only what their role requires, and access rights are recalculated at each session.

For banking operations teams building out zero trust architecture, the detailed strategy in Banking Access Controls: Zero Trust Security Architecture for Banking Ops Heads shows how authentication fits into the broader control framework. The zero trust security for mobile-first banks post covers mobile-specific implementation considerations that matter when passkeys are deployed via native banking apps.

Zero trust financial services also changes how we think about session management. Traditional session tokens can be stolen and replayed. In a passkey-first zero trust model, each authentication event produces a fresh cryptographic signature tied to the transaction context, making session hijacking significantly harder without adding user friction.

Identity Verification API: Integrating FIDO2 Into Your Stack

Most institutions do not build FIDO2 from scratch. They integrate a FIDO2 server into their existing identity and access management stack and connect it to an identity verification API that handles the enrollment verification step.

Choosing an Identity Verification API for FIDO2

The identity verification API sits between the customer-facing enrollment UI and the FIDO2 server. Its job is to confirm that the person creating a passkey is a legitimate, verified individual before the credential is issued. Key capabilities to evaluate:

- Document verification: Can it verify passports, driver's licenses, and national IDs across the geographies you serve, including NFC chip reading for stronger assurance?

- Biometric matching: Does it compare the live selfie against the document photo with active anti-spoofing running?

- Liveness detection: Is it certified against ISO 30107-3 for presentation attack detection, and has it passed iBeta Level 2 testing?

- Synthetic identity signals: Does it incorporate credit bureau data, device signals, and behavioral biometrics in the risk score?

- API latency: Sub-3-second response times are achievable with modern identity verification fintech providers and are necessary for low-friction onboarding.

- Compliance coverage: Does it satisfy KYC/AML requirements across your operating jurisdictions, including BSA, FinCEN guidance, and applicable state regulations?

When integrating, ensure the identity verification API passes a verification reference token to the FIDO2 server at passkey creation time. This creates an audit trail linking the passkey credential to the verified identity, which is essential during regulatory examinations.

For teams responsible for AML compliance alongside identity proofing, the AML screening and monitoring strategy for payments risk officers outlines how identity verification and transaction monitoring should connect in a compliant architecture. For security teams protecting the API integrations themselves, the API security strategies for CISOs in banking post covers rate limiting, certificate pinning, and mutual TLS considerations that apply directly to FIDO2 server integrations.

Onboard Customers in Seconds

Conclusion

Passkeys banking FIDO2 is the most significant shift in banking authentication since two-factor authentication became standard. By replacing shared secrets with cryptographic key pairs verified through biometric identity verification, FIDO2 removes the attack surface that account takeover fraud depends on. The KYC onboarding speed improvements are real and measurable. The synthetic identity fraud detection and deepfake detection banking capabilities needed alongside passkeys are mature and deployable today.

The honest complexity is in the transition. Migrating customers from passwords to passkeys requires careful UX design, fallback authentication paths for devices that do not support FIDO2, and a reliable identity verification API at enrollment. None of these are unsolvable, and the security gains justify the integration work.

If your institution is evaluating the full identity verification stack, including passkey enrollment verification and ongoing digital identity proofing, the right starting point is assessing your current identity maturity against the FIDO2 standard you want to deploy. Combining passkeys, certified liveness detection, and a zero trust financial services architecture gives institutions a defensible, regulator-friendly security posture that is genuinely difficult to attack at scale.

Share this article