.webp)

Listen To Our Podcast🎧

Business email compromise detection banks deploy today is the last line of defense against one of the most expensive payment fraud schemes in modern banking. According to the FBI Internet Crime Complaint Center's 2023 Annual Report, BEC and email account compromise collectively generated over $2.9 billion in reported losses, making them the highest-loss cybercrime category for the fifth consecutive year. The attack does not rely on malware or stolen credentials. A fraudster impersonates a CEO, a supplier, or an attorney, convinces an accounts payable employee to reroute a wire transfer, and by the time anyone spots the problem, the funds have cleared through multiple accounts. For banks sitting at the payment authorization layer, catching a BEC-driven wire before settlement is a matter of seconds, not hours, and it requires automated transaction monitoring that can flag behavioral anomalies without burying analysts in false alerts. This guide explains how the best detection systems work, where genuine gaps remain, and what implementation actually looks like in a commercial banking environment.

What Is Business Email Compromise and Why Banks Face the Hardest Job

BEC fraud does not look like most payment fraud at the transaction level. There is no stolen card number, no account takeover flag, no failed authentication attempt. The payment instruction arrives from a verified customer, through a legitimate channel, and matches the customer's profile in most standard rule-based checks. From a bank's perspective, the transaction is indistinguishable from a legitimate corporate wire until you examine the behavioral context around it.

Banks handling commercial payments are the final checkpoint between a fraudulent instruction and an irreversible loss. Once a wire settles, reversal options narrow fast, which is why business email compromise detection banks have invested in is heavily concentrated on the pre-settlement authorization window.

How a BEC Attack Unfolds in Practice

Most BEC attacks follow a predictable sequence. A threat actor either compromises a vendor's email account directly or registers a near-identical domain (acme-invoices.com instead of acmeinvoices.com). They monitor the correspondence long enough to understand payment cadence, invoice formats, and the names of trusted contacts. Then they send a credible payment instruction to the buyer's finance team, swapping the real bank routing details for a mule account.

The buyer's accounts payable team, recognizing familiar language and sender names, approves the wire. The buyer's bank receives a legitimate instruction from a verified customer. Without detection at the transaction layer, nothing in that payment raises a flag in a standard rules engine.

Why Wire Fraud Is So Hard to Reverse

Wire transfers move fast. ACH recalls are sometimes possible within 24-48 hours, but SWIFT international wires often clear within hours of initiation. FinCEN advisory guidance on business email compromise has consistently directed financial institutions toward pre-payment controls rather than post-payment recovery, because once funds reach a mule account and get forwarded, recovery rates drop sharply. This is why real-time fraud detection in banking has to operate before settlement, not after it.

How Business Email Compromise Detection at Banks Has Evolved

For years, banks relied on static rules to flag suspicious payments: wires above a certain threshold, alerts on first-time payees, holds on transactions to elevated-risk countries. These rules catch obvious cases. They miss BEC almost entirely because the fraudulent payment conforms to every expected parameter. The customer is legitimate, the amount is within their normal range, and the payee, while new, clears basic OFAC and sanctions screening.

Machine learning fraud detection changes this fundamentally. Instead of checking whether a transaction matches predefined rules, ML models evaluate whether it fits the customer's behavioral history and the network context around the receiving account.

Behavioral Baselines and Anomaly Scoring

AI fraud detection in banking builds a behavioral model for every account over time. If a corporate treasury account typically initiates domestic ACH transfers on Tuesday and Thursday mornings, a Friday evening wire to a newly created foreign account scores as a high-risk anomaly, even if the amount sits within the customer's normal range. The model weighs timing, channel, device, destination country, payee account age, and dozens of additional signals simultaneously.

This is what "ai fraud detection explained" means in practical terms: the system learns the shape of normal behavior for each entity and scores deviations against that baseline. It does not need explicit rules for each new BEC variant. A novel attack pattern, a previously unseen mule account structure, or an unusual timing sequence gets caught because it diverges from baseline, not because someone anticipated that exact scenario in advance.

Real-Time Fraud Detection at the Transaction Layer

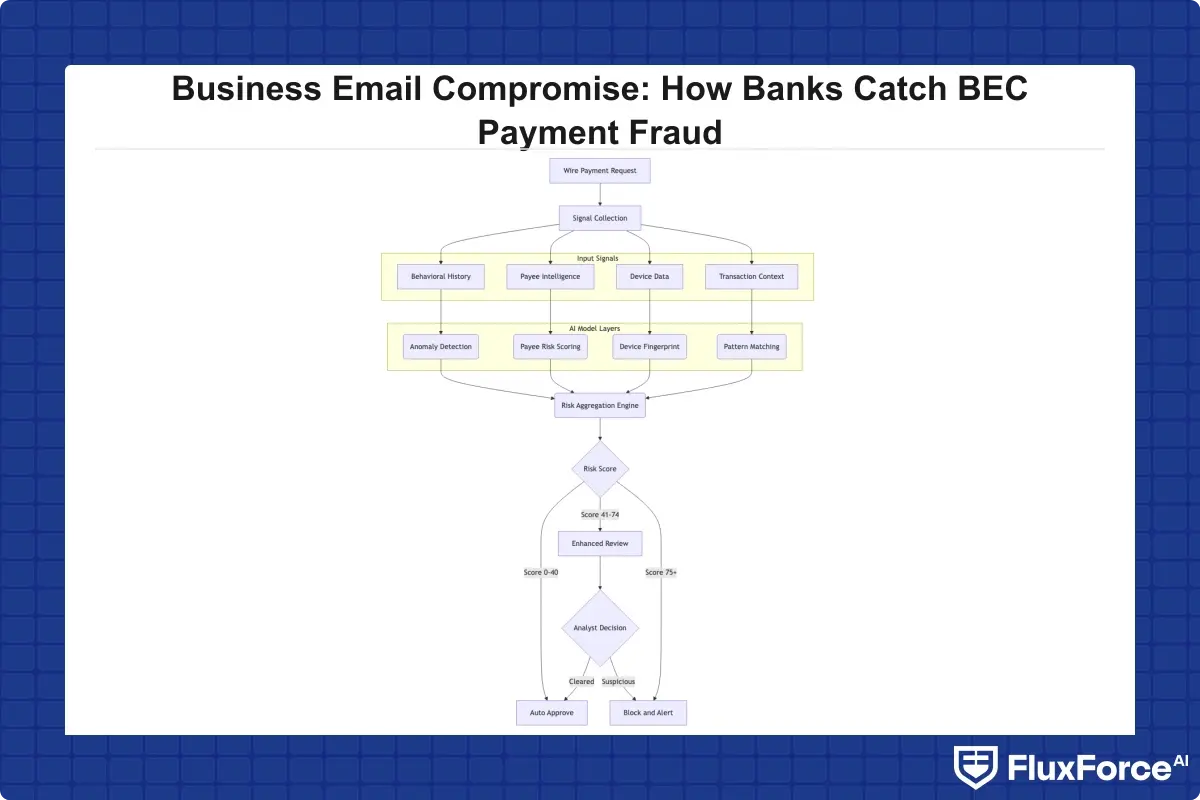

Real time fraud detection banks rely on today typically scores each payment within 200-500 milliseconds during the authorization step. The model pulls simultaneously from transaction attributes, customer behavioral history, payee network intelligence (how old is this account, has it appeared on cross-institutional fraud networks), device signals, and IP geolocation.

Banks using modern fraud detection software route high-risk transactions to one of three paths: auto-decline for the highest-risk scores, human review queue for medium-risk transactions, or automated call-back verification for high-value wires above a configurable threshold. Sub-second scoring preserves the payment experience for legitimate transactions while still intercepting the anomalies that matter.

Why False Positives Are the Real Operational Problem

Here is an uncomfortable reality about fraud detection in banking: false positives are often a larger daily operational burden than actual fraud losses. A system that flags every unusual wire for manual review sounds safe until you calculate the alert volumes it generates for a commercial bank with tens of thousands of corporate accounts.

False positives fraud detection systems produce translate directly into analyst hours, customer friction, and delayed payments. When a legitimate vendor payment is held for 36 hours because an alert fired, the corporate client does not understand the detection logic. They call their relationship manager and ask what is wrong with the bank.

The Cost of Fraud Alert Fatigue

Fraud alert fatigue is what happens when analysts work through hundreds of low-quality alerts daily. The false positive cost fraud operations teams carry is both direct and indirect. Direct costs are measurable: analyst salary time spent on alerts that resolve as legitimate transactions. Indirect costs are often larger: the real fraud that gets missed because analyst attention is saturated, the SAR filings delayed under load, and the customer churn from repeated payment holds.

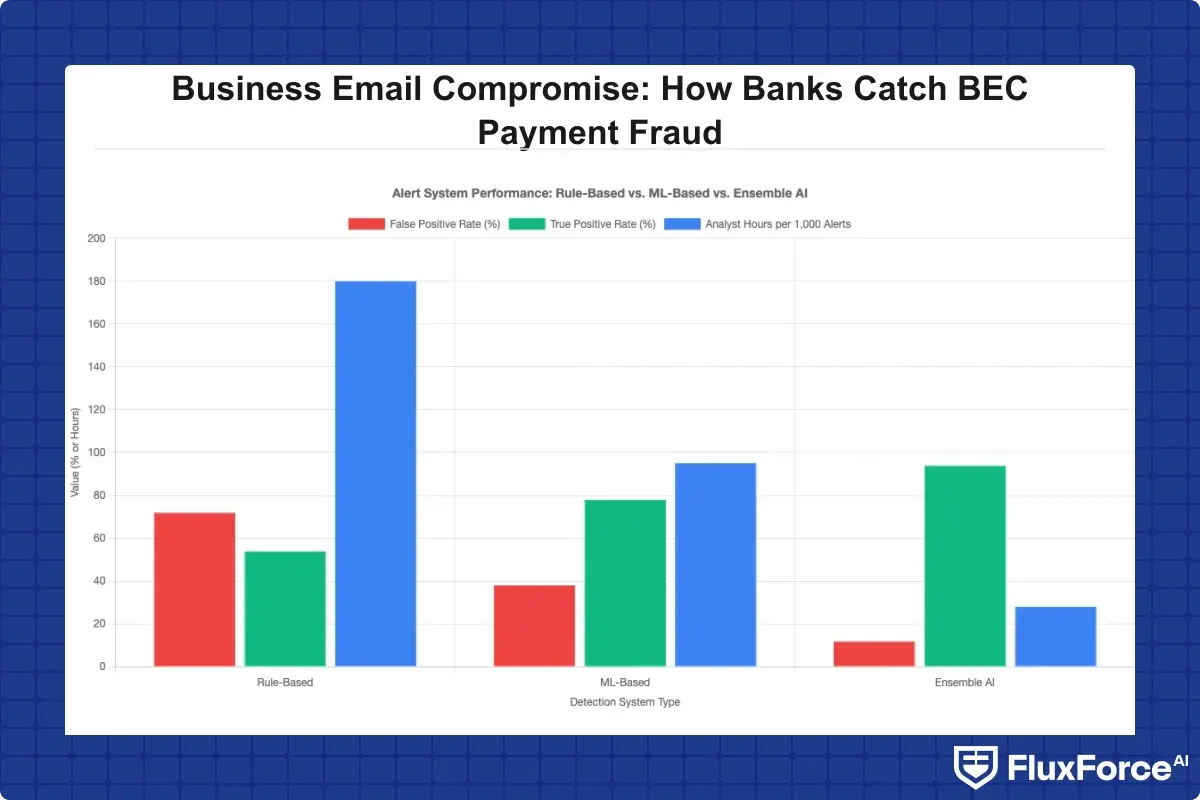

The false positive rate fraud detection systems produce in rule-based environments often exceeds 95%, meaning fewer than 5 out of every 100 alerts represent genuine fraud. Getting that rate below 80% requires moving from threshold-based rules to probabilistic scoring models that weight contextual signals dynamically.

How to Reduce False Positives in AML and Transaction Monitoring

The most effective way to reduce false positives transaction monitoring generates is through layered model architecture. Instead of a single model scoring every transaction with identical logic, banks are deploying ensemble approaches where behavioral models, graph network models, and document intelligence models each contribute a score that a meta-model combines.

Knowing how to reduce false positives in AML specifically matters because AML false positives carry a different cost profile than payment fraud alerts. An AML investigation takes weeks, requires documented analysis, and consumes far more analyst time per case. A 20% reduction in AML alert volume can free the equivalent of several full-time investigators. The post on how agentic AI fraud agents cut false positives by 80% covers the model architecture behind these results, including the feedback mechanisms that let models learn from analyst override decisions over time.

What Transaction Monitoring Software Should Actually Do

Not all transaction monitoring software is designed for commercial wire fraud. Many platforms were originally built for consumer card fraud and extended to commercial payments as a secondary use case. The detection logic for a $45 consumer card transaction and a $2.3 million corporate wire are fundamentally different problems, and the platforms need to reflect that distinction.

Core Capabilities for BEC Detection

Real time fraud detection banks need for BEC defense requires native integration with SWIFT message parsing, Fedwire, and CHIPS. The platform has to enrich payment messages with payee intelligence, overlay the customer's behavioral baseline, and return a risk score inside the authorization window. These are baseline technical requirements, not differentiators.

Automated transaction monitoring should go beyond scoring. The best platforms trigger automated responses: customer call-back protocols for wires above a configurable threshold, temporary payment holds with automated customer notification, or secondary authentication challenges routed to the corporate customer's verified contact. Removing human delay from the response loop is what makes automation valuable in payment fraud prevention. A payment sitting in an analyst queue for four hours while earlier alerts are worked through gives the fraudster time to move funds before the hold is reviewed.

The transaction monitoring cost question is real and often underestimated. Enterprise-grade platforms range from $150,000 to over $1 million annually in licensing before implementation and integration costs. Banks need to weigh that against actual BEC exposure. For institutions processing high volumes of commercial wires, a single large incident frequently exceeds the first year of platform costs.

Sardine vs Unit21: What the Comparison Reveals

When banks evaluate platforms for commercial fraud prevention, sardine vs unit21 is one of the most common comparisons in enterprise RFPs. Sardine's strength is in the pre-payment layer, specifically device intelligence and behavioral biometrics that can identify suspicious session behavior before a fraudulent payment instruction is even submitted. Unit21 is built around a no-code rules engine that compliance teams can modify without engineering involvement, which matters for institutions that need rapid response to emerging BEC variants.

The honest assessment is that neither platform is a complete answer to BEC on its own. Sardine addresses the behavioral precursors before payment initiation. Unit21 handles the alert workflow and case management layer after detection fires. Banks doing serious payment fraud prevention typically layer a specialist detection engine on top of their core monitoring platform rather than relying on a single vendor for both problems.

Payment Fraud Prevention Beyond BEC: Connected Fraud Vectors

Business email compromise does not always operate in isolation. Payment fraud prevention strategies that focus exclusively on BEC miss the connected patterns that precede or accompany these attacks. One of the most common is the use of synthetic identity fraud to establish a credible receiving account before the BEC campaign is executed.

Synthetic Identity Fraud as a BEC Precursor

Synthetic identity fraud in commercial payments is harder to catch than consumer variants because business identity verification is less standardized than individual KYC. A fraudster incorporates a shell company, opens a business bank account, and runs small legitimate transactions over 90-120 days to build a transaction history. When that account becomes the BEC destination, it passes basic payee checks because it has real banking activity behind it.

The post on detecting synthetic identity fraud in real-time covers how graph-based models surface these patterns by analyzing the relationship between entity creation dates, transaction velocity, and inflow-only account behavior. For compliance officers responsible for vendor onboarding controls, high-risk supplier validation is directly relevant to closing this gap before the fraudulent wire arrives.

How AI Connects BEC to Broader Fraud Patterns

AI fraud detection software generates its clearest advantage in multi-vector attacks by evaluating relationships between entities across a network, not just the attributes of individual transactions. If a newly created business account is receiving wires from three unrelated corporate clients in the same week with no corresponding outflows, that cross-entity pattern identifies a potential mule network, even without a direct link to a known BEC campaign.

This network-level analysis is where machine learning fraud detection goes beyond what rules can achieve. Rules flag individual transaction anomalies. Graph models surface coordinated fraud patterns operating across accounts and payment rails simultaneously, which is the architecture that catches BEC-adjacent schemes before they escalate.

What BEC Detection Implementation Looks Like at Banks

Purchasing ai fraud detection software is the straightforward part of BEC defense. Integration is where most projects run into real complexity. Banks with API-first payment infrastructure can typically deploy a scoring layer at the payment hub in three to six months. Banks on legacy core banking platforms may face 18 months or more of middleware development before real-time scoring is technically feasible at the authorization layer.

Integration Challenges in Legacy Banking Infrastructure

The core problem with real time fraud detection banks on older infrastructure face is that payment authorization and fraud scoring were never designed to share data at transaction speed. A machine learning model needs to score a wire during the authorization step, which means the scoring API must sit inside the payment processing flow, not downstream in a batch reporting system. That requires engagement at the payment hub layer with core banking vendors, clearing house connections, and internal engineering teams working in parallel.

This is why the fraud detection conversation and the core banking modernization conversation cannot happen separately. Banks that have moved to API-first payment infrastructure consistently report shorter deployment timelines for fraud scoring integration. Banks still on monolithic core systems should plan for a longer integration period and build that into the business case.

Transaction Monitoring Cost and ROI

The transaction monitoring cost calculation needs to account for the full implementation lifecycle, not just annual licensing. Integration engineering, model tuning, analyst retraining, and ongoing model refresh cycles all add to total cost of ownership. For a bank starting from a rule-based baseline, budget 18-24 months to full production deployment and an ongoing model operations function.

The ROI case is usually strong enough to justify the investment. Banks that have moved from rule-based systems to ML-based automated transaction monitoring consistently report 40-60% reductions in alert volume within 12 months of production. That translates directly into analyst capacity that can be redeployed to higher-value work. A single large BEC incident intercepted before settlement often covers an entire year of platform costs, making the investment straightforward to justify in most commercial banking environments.

Onboard Customers in Seconds

Conclusion

Business email compromise detection banks have built over the past several years represents a genuine shift from reactive investigation to proactive interception at the payment authorization layer. Machine learning fraud detection, real time fraud detection at authorization, and automated transaction monitoring give compliance teams capabilities that static rule engines could not provide, and the gap between institutions that have made this transition and those that have not is measurable in loss rates.

The honest limitation is that BEC attackers adapt. As detection models improve, attackers extend reconnaissance periods, use smaller test payments to probe detection thresholds, and build more convincing email infrastructure to evade domain-based signals. Staying ahead requires continuous model retraining, threat intelligence integration, and participation in cross-industry data sharing networks.

If your institution is evaluating ai fraud detection in banking, prioritize real-time payment scoring at the authorization layer. Case management workflows, analytics reporting, and regulatory automation can be layered on top of that foundation. But if a fraudulent wire settles before detection fires, the rest of the investment in payment fraud prevention does not matter. The detection stack needs to be strongest at the moment of authorization, and that is where the business case for modernization starts.

Share this article