.webp)

Listen To Our Podcast🎧

Introduction

Generative AI compliance document review has moved from pilot program to production reality across major financial institutions, and the shift is happening faster than most compliance teams expected. Until recently, a compliance analyst at a mid-size bank might spend three to four hours manually cross-checking a single corporate onboarding file: passports, utility bills, corporate registrations, and beneficial ownership structures. Generative AI changes that calculus entirely. This post breaks down exactly how the technology works, where it outperforms human reviewers, and where the honest trade-offs lie for banks, insurtech firms, and supply chain operators deploying it today.

- What Is Generative AI Compliance Document Review?

- How Generative AI Is Transforming Identity Verification in Fintech

- Detecting Fraud That Human Reviewers Miss

- Digital Identity Proofing With AI Document Analysis

- Real-World Applications Across Financial Services

Onboard Customers in Seconds

What Is Generative AI Compliance Document Review?

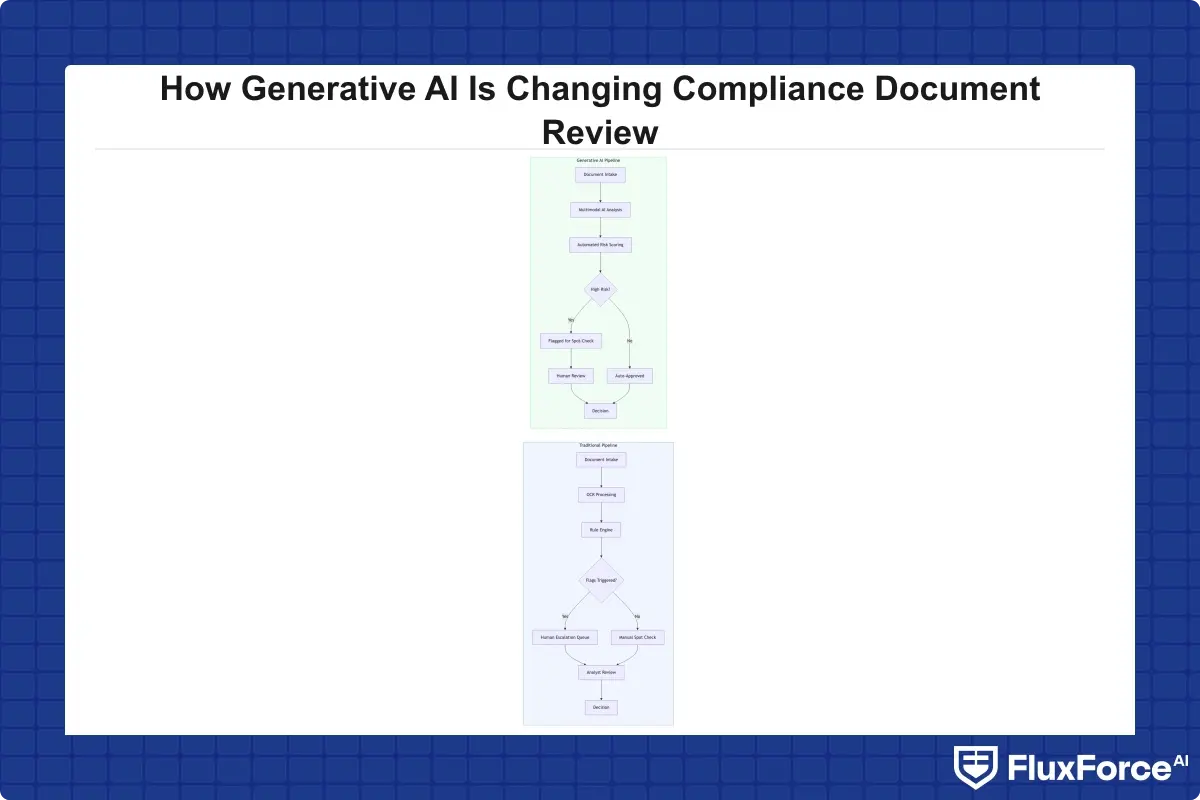

Generative AI compliance document review is the application of large language models (LLMs) and multimodal AI to interpret, extract, classify, and validate regulatory documents in real time. Rather than pattern-matching against fixed templates, the way older OCR and rules-based systems do, generative AI actually understands document context. It can read a corporate registration from any jurisdiction, identify the relevant beneficial ownership fields, and flag discrepancies against KYC/AML requirements without needing jurisdiction-specific templates built in advance.

The distinction matters because financial institutions deal with documents from 180-plus countries, each with different formats, languages, and regulatory expectations. A traditional system trained on a German Handelsregister extract fails when it encounters a Cayman Islands corporate structure for the first time. A generative AI model does not.

How Traditional Document Review Works

Traditional compliance document review relies on three components: OCR to extract text, rule-based engines to classify fields, and human reviewers to make final judgments on ambiguous cases. The process is sequential and slow. A document enters the queue, gets OCR-processed, gets matched against pre-defined field maps, and then either passes automatically or escalates to a human analyst. Average processing time for a complex corporate onboarding packet runs 48 to 72 hours at most major banks.

The bigger problem is consistency. Two analysts reviewing the same document often reach different conclusions, particularly on politically exposed persons (PEP) screening and source-of-funds documentation. Regulatory audits frequently surface these inconsistencies as control failures.

Where Manual Review Breaks Down

Volume is the first problem. A single mid-tier bank in a growth market might process 800 to 1,200 new business accounts per month. Scaling that manually requires hiring linearly, and compliance talent is expensive and scarce. The second problem is velocity: fraudsters submit documents faster than human teams can review them, which is exactly why synthetic identity fraud has become one of the fastest-growing financial crime categories globally.

The third problem is document sophistication. Generative adversarial networks can now produce forged identity documents that fool the naked eye and basic OCR systems. Catching them requires AI that can analyze micro-features: font consistency, metadata integrity, printing artifacts, and biometric data alignment. That is precisely what generative AI models trained for compliance document review deliver.

How Generative AI Is Transforming Identity Verification in Fintech

The most immediate impact of generative AI on identity verification fintech operations is speed. Processes that previously required human-in-the-loop review at every step can now run end-to-end in minutes, with human intervention reserved for genuine edge cases. That matters enormously for customer experience and for revenue, because account abandonment during slow onboarding directly costs banks customers.

Accelerating KYC Onboarding Speed

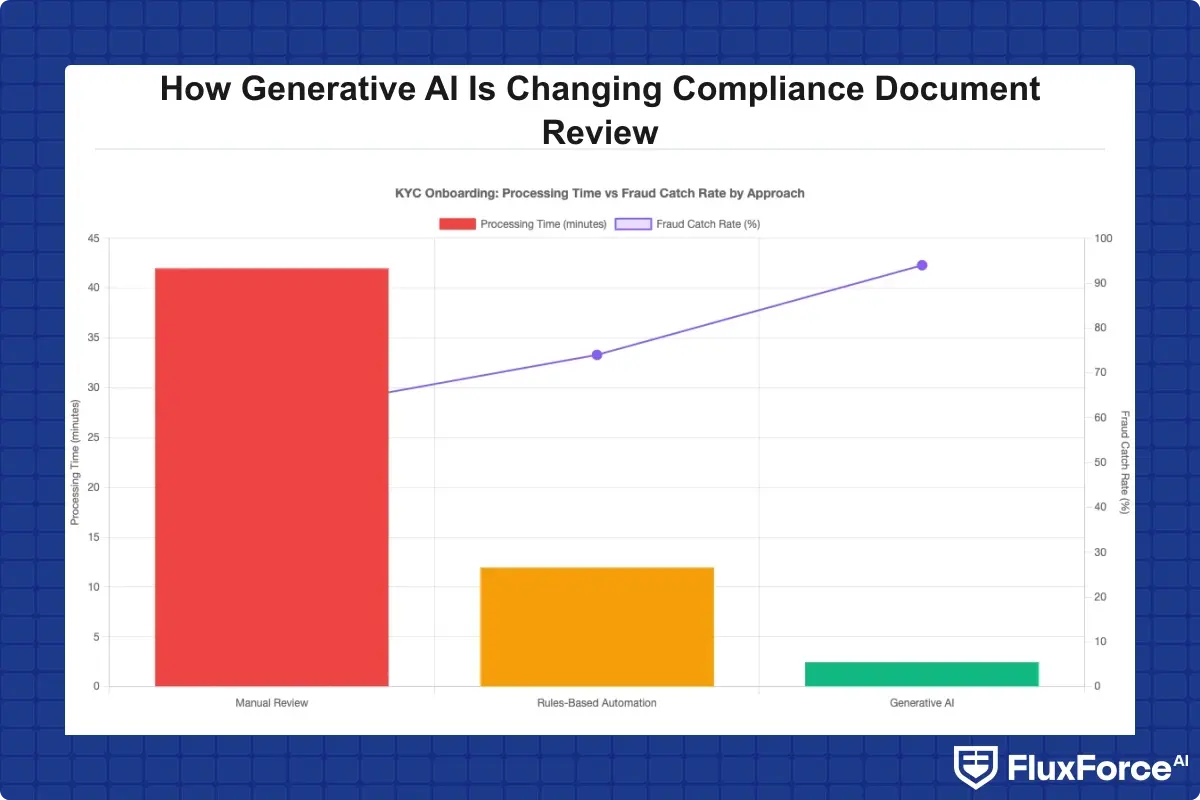

KYC onboarding speed is one of the most-tracked metrics in retail and commercial banking right now. Research from McKinsey indicates that top-quartile digital banks complete individual KYC onboarding in under three minutes, while the median for traditional banks sits at 24 hours or more. The difference is almost entirely explained by AI-assisted document processing.

Generative AI handles the heavy lifting: extracting name, date of birth, address, and document number from any government-issued ID regardless of format; cross-referencing against sanctions and PEP databases; and generating a risk score with a plain-language explanation. The compliance officer sees a clean summary with flagged anomalies, not a raw document stack. That friction reduction also cuts abandonment rates during onboarding, which typically run 20 to 30 percent when KYC processes take longer than 10 minutes.

That friction reduction also cuts abandonment rates during onboarding, which typically run 20 to 30 percent when KYC processes take longer than 10 minutes.

Biometric Identity Verification at Scale

Biometric identity verification adds a layer of assurance that document analysis alone cannot provide: confirming the person submitting the document is the person depicted in it. Modern systems combine document intelligence with facial recognition and liveness checks, running the full sequence in under 30 seconds.

The challenge is accuracy at scale. A false accept rate of 0.1 percent sounds reassuring until you process 100,000 verifications per month, at which point you are letting through 100 fraudulent identities. Leading providers in the identity verification fintech space have pushed false accept rates below 0.01 percent by combining multiple AI signals: document authenticity scoring, facial match confidence, and behavioral biometrics captured during the session.

A false accept rate of 0.1 percent sounds reassuring until you process 100,000 verifications per month, at which point you are letting through 100 fraudulent identities.

Detecting Fraud That Human Reviewers Miss

This is where generative AI compliance document review moves from a convenience to a necessity. The fraud vectors growing fastest, specifically deepfake-based identity fraud and synthetic identity construction, are designed to defeat human review and older automated systems. Building defenses here requires AI operating on signals that humans literally cannot perceive.

Liveness Detection and Fraud Prevention

Liveness detection fraud prevention addresses a specific attack: submitting a photo or video of a legitimate identity document alongside a pre-recorded or AI-generated face video to spoof facial verification. Until 2022, passive liveness detection, checking that the face appears natural, was sufficient for most fintech applications. It is not sufficient now.

Active liveness detection, which asks the user to perform random actions like blinking or turning their head, became the standard approach, but sophisticated deepfake systems can now mimic those actions convincingly. The current frontier is behavioral analysis: assessing micro-expressions, skin texture, lighting consistency, and physiological signals like pulse estimation from facial video. These signals are invisible to human reviewers but detectable by models trained specifically for liveness detection fraud prevention.

Regulations are catching up. The NIST Digital Identity Guidelines (SP 800-63-4) now specify liveness assurance levels, and EU financial regulators have begun referencing ISO/IEC 30107-3 for presentation attack detection standards in their KYC technical specifications.

Deepfake Detection in Banking Documents

Deepfake detection banking applications extend beyond facial verification. Generative AI models can detect synthetic text and manufactured document layouts in uploaded files. This matters because fraudsters increasingly use AI image generators to create realistic-looking bank statements, utility bills, and proof-of-address documents rather than scanning and editing physical originals.

Detection methods examine pixel-level artifacts that generative image models leave behind: boundary inconsistencies, unusual compression patterns, and statistical signatures in image metadata. These artifacts are imperceptible to human reviewers but consistent enough that well-trained detection models flag them reliably. The practical recommendation for compliance teams: treat any uploaded PDF or image as potentially AI-generated and run it through generation artifact detection alongside standard optical character recognition.

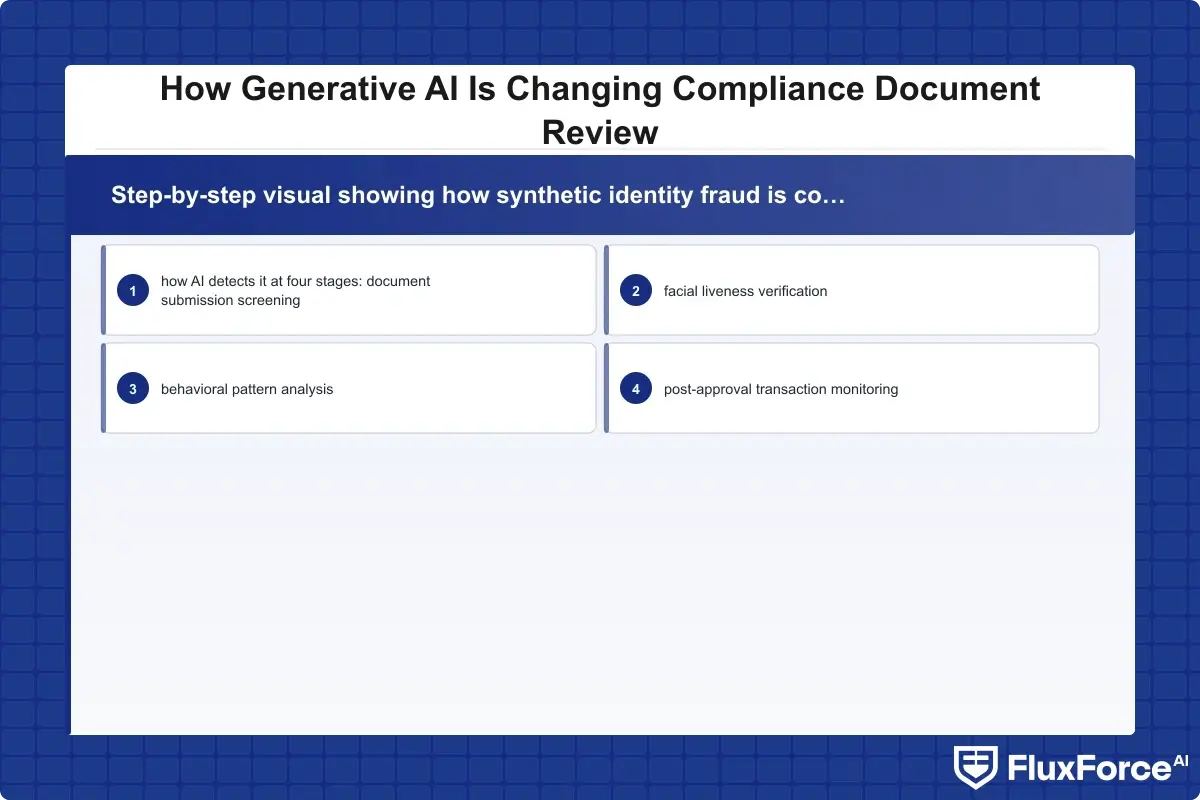

Synthetic Identity Fraud Detection

Synthetic identity fraud detection is arguably the hardest problem in compliance document review because synthetic identities, built from combinations of real and fabricated personal data, often pass initial document checks. The documents themselves may be legitimate. The identity they represent is not.

For a detailed technical breakdown of how these detection pipelines work, see the analysis on detecting synthetic identity fraud in real-time. The key architectural point is that effective synthetic identity fraud detection requires analyzing behavioral patterns across the identity lifecycle, not just at the point of document submission. Generative AI enables this by correlating signals across time: application behavior, device fingerprints, transaction patterns, and network relationships with other accounts.

Digital Identity Proofing With AI Document Analysis

Digital identity proofing is the formal process of establishing that a person or entity is who they claim to be before granting access to financial services. The generative AI shift in this area makes high-assurance proofing economically viable at consumer scale, which was not possible before.

Previously, high-assurance identity proofing required in-person verification or lengthy manual review, restricting it to high-value banking relationships. A mortgage applicant might get rigorous scrutiny; a prepaid card applicant typically would not. That inconsistency created obvious fraud vectors. Institutions that have deployed AI-driven KYC/AML automation now deliver IAL2-equivalent quality checks across all customer segments at a cost that makes it viable even for low-value transactions.

How the Identity Verification API Processes Documents

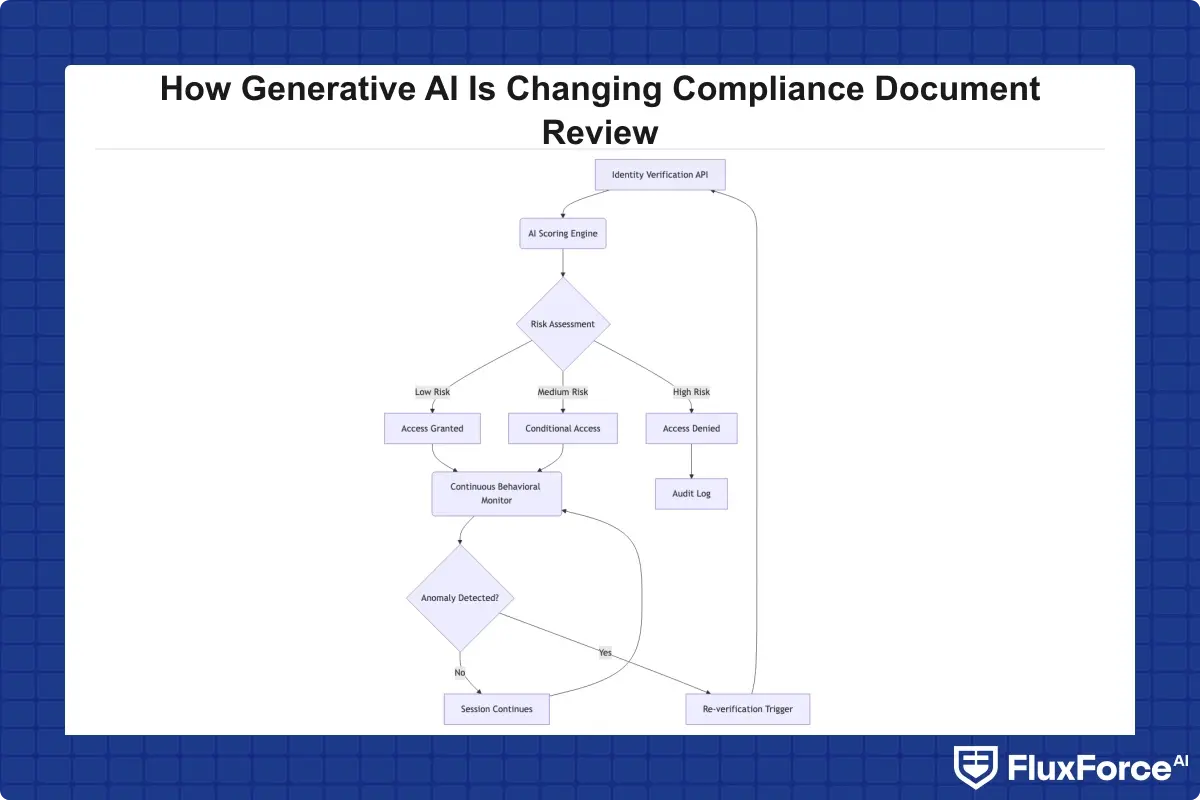

An identity verification API in a modern generative AI stack does considerably more than older document verification services. The API call sends the document image and any supplementary data, such as a facial image, device fingerprint, or IP address, to the AI system, which runs multiple parallel checks: optical character recognition, field extraction, format validation against issuing authority templates, authenticity scoring, and biometric match if a selfie is included.

The response returns a structured confidence score for each component, a combined risk rating, and a plain-language explanation of any anomalies that a compliance officer can audit. This auditability matters for regulatory purposes: a decision to reject or escalate needs a documented rationale that regulators can review. Generative AI provides that rationale natively, whereas older systems typically returned only a binary pass/fail with an error code.

Zero Trust Financial Services Integration

Connecting generative AI document review to a zero trust financial services architecture changes how institutions think about document trust. In a traditional perimeter model, once a customer is onboarded and their documents accepted, they are trusted implicitly for the duration of the relationship. A zero trust security framework rejects that assumption entirely.

Under zero trust principles, identity verification is continuous, not one-time. A customer who passed document verification at onboarding may still trigger re-verification if their behavioral profile changes, if they access services from an unfamiliar device, or if their account shows transaction patterns inconsistent with their stated business profile. Generative AI makes this continuous verification practical because re-verification runs fast enough that customers barely notice it, typically under 10 seconds for a liveness check. For a detailed look at how zero trust and AI combine in banking security architecture, the analysis in our post on Zero Trust and Agentic AI for banking security covers the implementation details that compliance and security teams need to coordinate on.

Real-World Applications Across Financial Services

Banks and Credit Institutions

Commercial banks use generative AI compliance document review primarily for corporate onboarding, where the document burden is highest. A new corporate account might require 15 to 40 documents depending on jurisdiction and ownership structure. AI systems process that full package in 10 to 15 minutes, compared to two to three business days for manual review.

The secondary application is ongoing monitoring. When a corporate client files updated documentation, such as a change in directors or a new shareholding structure, AI flags whether those changes trigger enhanced due diligence requirements or sanctions screening. Manual review is notoriously inconsistent on updates because analysts often treat them as lower priority than new applications.

Insurance and Insurtech Compliance

Insurance is a high-stakes environment for document fraud. Policy applications rely on accurate disclosure of health history, property condition, and business operations, all of which fraudsters have strong incentives to misrepresent. Generative AI document review helps insurers cross-check submitted documents against third-party data sources and flag inconsistencies that suggest manipulation.

For insurers operating under GDPR, automating document review also reduces human exposure to sensitive personal data, which carries its own compliance benefits. The regulatory compliance automation framework for insurance risk officers covers how to structure this without creating new data minimization violations.

Supply Chain and Trade Finance

Trade document verification is one of the most document-intensive compliance processes in existence. A single letter of credit transaction might involve bills of lading, certificates of origin, commercial invoices, customs declarations, and insurance certificates, each from different parties and jurisdictions. Manual verification typically takes two to four business days.

AI trade document verification brings that timeframe down substantially. More importantly, it catches discrepancies that human reviewers miss when processing dozens of documents simultaneously under time pressure. Our post on AI-driven trade document verification for CISOs walks through the specific document types and how AI handles edge cases in cross-border trade finance.

How to Implement Generative AI Compliance Document Review

Building on a Zero Trust Security Framework

The implementation starting point for most institutions is not the AI model itself but the identity architecture around it. A zero trust security framework establishes the principles governing how document verification decisions connect to access controls, transaction permissions, and risk scoring. Without that architectural foundation, AI document review operates as a point solution rather than a systemic control.

The practical steps are: map your current document review touchpoints across the customer lifecycle; identify which touchpoints carry the highest fraud risk and regulatory exposure; and prioritize AI deployment at those points first. Most institutions start with new account onboarding, then extend to high-value transaction approval and periodic customer due diligence refresh. For teams comparing manual and automated approaches before committing to a build, the analysis in manual compliance versus AI automation is a useful reference for building the internal business case with concrete numbers.

Key Metrics to Track After Deployment

The metrics that matter most after deploying generative AI compliance document review are: straight-through processing rate (what percentage of documents process without human escalation); false positive rate (how often AI flags legitimate documents); time to decision; and fraud catch rate measured against post-approval fraud events in the customer base.

A well-configured system should achieve a straight-through processing rate above 80 percent within 90 days of deployment, with a false positive rate below 5 percent. If false positives run high, the model needs domain-specific fine-tuning on your document set and customer population. Generative AI models perform significantly better with domain-specific calibration than with off-the-shelf configurations, and most enterprise vendors provide this as part of implementation.

A well-configured system should achieve a straight-through processing rate above 80 percent within 90 days of deployment, with a false positive rate below 5 percent.

What to Expect: Benefits and Honest Trade-offs

Measurable Gains From Generative AI Document Review

The benefits of generative AI compliance document review are measurable and consistent across institutions that have deployed it seriously. Processing time drops from days to minutes. Consistency improves because the AI applies the same criteria every time regardless of analyst fatigue or caseload pressure. Fraud detection improves meaningfully for document-based attacks, particularly deepfake detection in banking contexts and synthetic identity fraud cases. Compliance teams spend less time on routine review and more time on cases that genuinely require human judgment.

The cost economics work for institutions processing more than 500 documents per month. Below that threshold, implementation and integration costs may not justify analyst time savings in the short term, though fraud prevention value can tip the calculation even at lower volumes.

Where Generative AI Document Review Has Limits

The honest answer on limitations is that generative AI compliance document review is not fully autonomous for complex cases. Novel corporate structures, unusual jurisdictions, and politically sensitive accounts still require human judgment. The AI is good at structuring those cases efficiently for human review. It is less reliable at making final decisions on edge cases that require contextual reasoning about geopolitical risk or business relationship legitimacy.

There is also a regulatory acceptance question in some markets. Several regulators have not yet explicitly endorsed AI-only document review for high-risk customer segments. Compliance teams need to verify their specific regulatory context before removing human sign-off from the process entirely. The Financial Action Task Force guidance on digital identity provides a useful international benchmark for what regulators generally consider acceptable in AI-assisted customer due diligence.

- Generative AI compliance document review is the application of large language models (LLMs) and multimodal AI to interpret, extract, classify, and validate regulatory documents in real time.

- The most immediate impact of generative AI on identity verification fintech operations is speed.

- This is where generative AI compliance document review moves from a convenience to a necessity.

- Digital identity proofing is the formal process of establishing that a person or entity is who they claim to be before granting access to financial services.

- Commercial banks use generative AI compliance document review primarily for corporate onboarding, where the document burden is highest.

Onboard Customers in Seconds

Conclusion

Generative AI compliance document review is not a future capability. It is available now, performs measurably better than manual review on speed and fraud detection, and is already deployed at scale by leading institutions across banking, insurance, and trade finance. The institutions moving quickly gain real competitive advantages on KYC onboarding speed and fraud containment, not just operational efficiency numbers on a dashboard.

The implementation path is clear for teams that start with the right architecture: establish a zero trust identity framework, identify your highest-risk document touchpoints, and deploy AI verification where fraud exposure and compliance cost are highest. Expand from there as confidence in the system builds. If your team is evaluating digital identity proofing and KYC capabilities for your institution, the logical next step is an honest assessment of your current document review workflow and where AI verification delivers the fastest compliance gains.

Share this article