.webp)

Listen To Our Podcast🎧

Introduction

Agentic AI financial services is changing how fraud teams and compliance officers think about risk. Instead of waiting for analysts to review alerts, autonomous AI agents now query data sources, verify identities in real time, and escalate only the cases that need a human decision. The result: faster onboarding, fewer false positives, and compliance workflows that run around the clock without burning out your team. This post breaks down what agentic AI actually does in a financial services context, where it delivers the clearest gains, and what fraud and compliance teams need to know before deploying it.

- What Is Agentic AI in Financial Services?

- How Agentic AI Changes KYC Onboarding Speed and Identity Verification

- Biometric Identity Verification and Liveness Detection Fraud Prevention

- Synthetic Identity Fraud Detection: The Agentic AI Advantage

- Deepfake Detection Banking and Digital Identity Proofing

Onboard Customers in Seconds

What Is Agentic AI in Financial Services?

How Agentic AI Differs from Traditional Rule-Based Systems

Traditional fraud detection systems work on rules. A transaction exceeds a threshold? Flag it. An IP address matches a watchlist? Block it. Rules are fast, auditable, and simple to explain to regulators. But they are also brittle. Fraud patterns evolve faster than rule sets get updated, and every new rule added to a legacy stack increases false positive rates.

Agentic AI is different because it acts. An agentic AI system does not just score a transaction and stop. It queries additional data sources, runs document checks, compares behavioral signals, and decides whether to approve, escalate, or block, all within a single workflow that takes seconds rather than days. According to NIST's AI Risk Management Framework, agentic systems are characterized by their ability to plan and execute multi-step tasks with minimal human intervention, which is exactly what financial risk workflows need.

The Role of Identity Verification API in Agentic Workflows

The identity verification API is the connective tissue in an agentic workflow. It lets the AI agent pull document data, biometric scores, sanctions checks, and device signals into a single decision context. When an agentic system can call an identity verification API mid-workflow, it resolves ambiguity that would otherwise route to a human analyst.

For example: a new account application scores medium-risk on initial behavioral signals. Instead of automatically queuing it for manual review, the agentic AI calls the identity verification API, requests a liveness check, and cross-references the document data against a sanctions list. If everything checks out, the account opens. If there is a mismatch, the case escalates with full context attached. Analysts get fewer cases, but every case they receive is genuinely worth their attention.

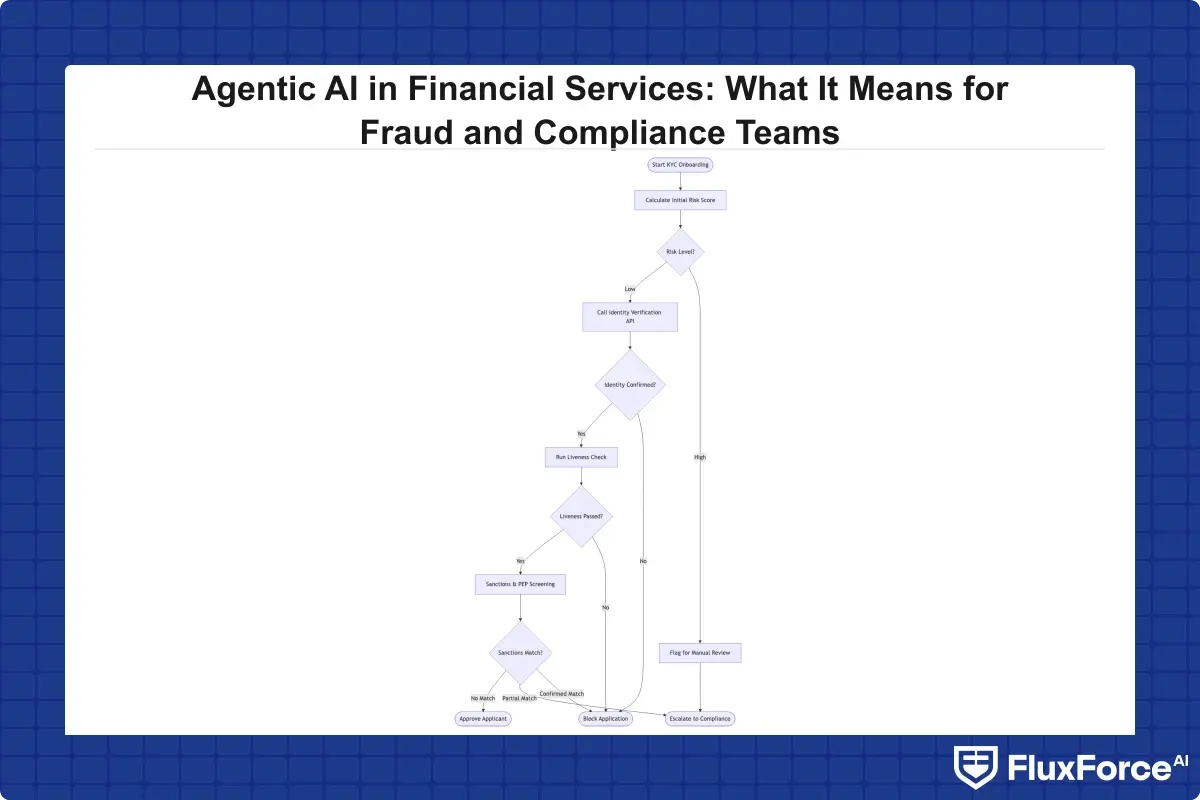

How Agentic AI Changes KYC Onboarding Speed and Identity Verification

How KYC Onboarding Speed Affects Customer Conversion

KYC onboarding speed is a business metric, not just a compliance checkbox. Research from financial services consultancies consistently shows that onboarding abandonment rates spike when verification takes longer than three minutes. Agentic AI cuts this time significantly because it runs multiple checks in parallel rather than sequentially.

A traditional KYC flow might look like this: document upload, manual review request, liveness check request, customer response, analyst review, decision. Each step introduces latency, and latency loses customers. An agentic AI flow runs document analysis, biometric comparison, and sanctions screening simultaneously, returning a decision in under 60 seconds for the majority of applicants. For identity verification fintech companies building their first digital product, this difference directly affects the cost of customer acquisition.

Digital Identity Proofing at Scale

Digital identity proofing is the process of confirming that a person is who they claim to be using digital evidence: government ID documents, selfies, device signals, and behavioral data. Agentic AI makes digital identity proofing scalable because the agent adapts its verification depth based on real-time risk signals rather than applying the same fixed process to every applicant.

A low-risk applicant applying from a known device in their home country gets a streamlined check. A high-risk applicant applying from an unfamiliar IP with a freshly registered email address gets a deeper check with additional document challenges. This adaptive approach is something static verification flows cannot replicate, and it is why digital identity proofing with agentic AI achieves higher accuracy with lower friction than fixed-depth checks.

The FATF Guidance on Digital Identity explicitly supports risk-based approaches to identity verification, which aligns precisely with what agentic AI enables: a layered, proportionate response to identity risk rather than a one-size-fits-all check.

Biometric Identity Verification and Liveness Detection Fraud Prevention

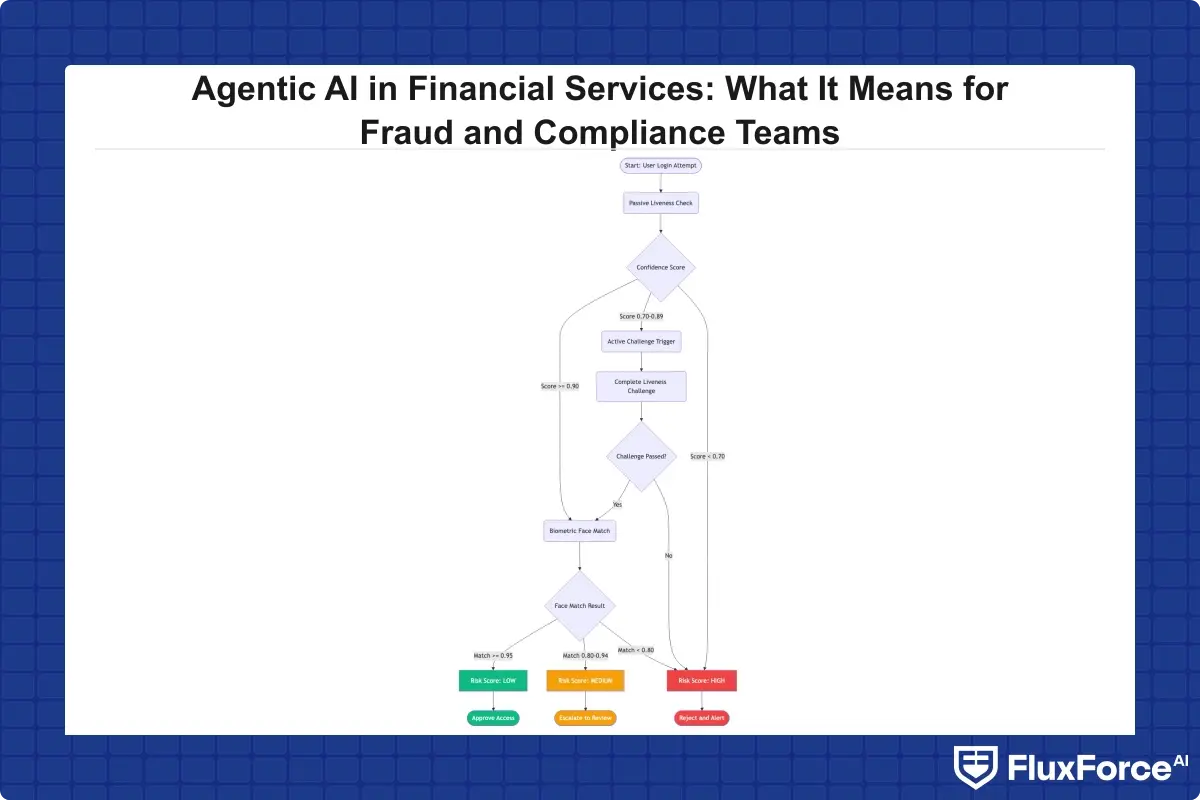

How Liveness Detection Fraud Prevention Works

Liveness detection fraud is the practice of using a photo, video replay, or 3D mask to spoof a biometric check. It is one of the most common attacks on digital onboarding flows, and it is growing more sophisticated as deepfake technology becomes accessible to low-skilled attackers.

Liveness detection systems work by analyzing micro-movements, texture, and depth cues that a flat image or video replay cannot replicate convincingly. Modern systems use active liveness, asking the user to perform a specific action like blinking or turning their head, and passive liveness, analyzing the submitted image without requiring any action. Agentic AI integrates both modes, choosing the appropriate level of challenge based on the risk profile of the current session rather than applying the same challenge to every user indiscriminately.

Biometric Identity Verification in Practice

Biometric identity verification goes beyond liveness. It includes face comparison between a live selfie and the photo on a submitted ID document, checking that face geometry, skin texture, and lighting are consistent. It also includes behavioral biometrics: how a person types, swipes, and navigates within an app over the course of a session.

For banking institutions, biometric identity verification serves two distinct purposes. At onboarding, it confirms the applicant is genuinely the document holder. At step-up authentication, it re-confirms identity for high-risk transactions without forcing the user through a full KYC flow again. Agentic AI manages both contexts, pulling from the same biometric profile and applying different confidence thresholds depending on what is at stake. This is the kind of continuous verification that a zero trust security architecture for banking explicitly requires at every access point.

Synthetic Identity Fraud Detection: The Agentic AI Advantage

Synthetic identity fraud is one of the costliest fraud types affecting financial institutions today. The Federal Reserve has identified it as the fastest-growing financial crime in the United States, with losses across the industry running into billions annually.

Why Traditional Systems Miss Synthetic Identities

A synthetic identity is built from a mix of real and fabricated data: a real Social Security number, often sourced from a child or credit-thin individual, combined with a fake name, address, and date of birth. Traditional credit bureau checks and document verification often miss these because the underlying SSN is legitimate and the identity has been carefully cultivated over months with small, on-time payments before the eventual bust-out.

The fraud emerges when the criminal rapidly maxes out all available credit lines before disappearing entirely. By the time it is detected, the synthetic identity may have held accounts across multiple institutions for years. Detecting synthetic identity fraud in real-time requires a fundamentally different set of signals than traditional document and credit checks provide.

Synthetic Identity Fraud Detection with Agentic AI

Synthetic identity fraud detection requires cross-referencing signals that no single data source contains. An agentic AI system can query device fingerprints, email account age, social graph signals, cross-institution velocity patterns, and behavioral anomalies simultaneously. The agent builds a coherent risk picture from these disparate signals and flags synthetic identity patterns that appear perfectly normal when any single data point is examined in isolation.

The key capability here is graph analysis. Agentic AI can trace how identity attributes cluster across applications. A phone number appearing across twelve recently opened accounts is suspicious. An email domain registered two days before the application is suspicious. An address matching a mail-forwarding service is suspicious. None of these signals alone triggers a block, but an agentic system that considers all of them simultaneously identifies synthetic identity fraud before the bust-out happens, which is precisely what zero trust financial services architecture demands of any verification layer deployed at the access boundary.

Deepfake Detection Banking and Digital Identity Proofing

Deepfake Detection Banking: The Growing Threat

Deeepfake detection banking is no longer a theoretical concern. In 2024, a finance worker at a multinational firm was reportedly tricked into transferring 25 million dollars following a deepfake video call impersonating the company's CFO. In financial services, the same attack vector applies to account takeovers, fraudulent wire transfers, and unauthorized loan applications where voice or video is used to verify identity.

Agentic AI addresses deepfake detection banking by combining multiple signals: micro-expression analysis, audio-visual synchronization inconsistencies, metadata analysis of submitted media files, and cross-referencing with known generative model artifacts. No single detector is reliable in isolation against modern deepfake tools, but an agentic system that aggregates multiple detection signals performs significantly better than any standalone check.

Digital Identity Proofing Against AI-Generated Attacks

As deepfake generation improves, digital identity proofing systems need to evolve at the same pace. The challenge is that deepfake generators and detectors exist in an adversarial loop: each improvement in generation forces a corresponding improvement in detection. Agentic AI handles this dynamic more effectively than static rule systems because the agent's detection logic can be updated with new signals without rebuilding the entire verification pipeline from scratch.

For compliance teams, this has a practical implication. When a new attack technique is identified, the response time with an agentic AI system is hours rather than weeks. The agent's decision logic updates, and every subsequent verification immediately benefits from improved detection capability. Static rule systems require formal change management, testing cycles, and deployment windows, intervals during which attackers can operate with reduced friction against your identity verification fintech stack.

Zero Trust Financial Services: Integrating Agentic AI with Security Architecture

Zero Trust Security Framework for Financial Institutions

A zero trust security framework operates from the principle that no user, device, or session should be trusted by default, regardless of whether they are inside or outside the network perimeter. In financial services, this principle is increasingly mandated by regulatory guidance and security standards. NIST's Zero Trust Architecture specification provides the technical foundation that many financial institutions reference when designing their access control policies.

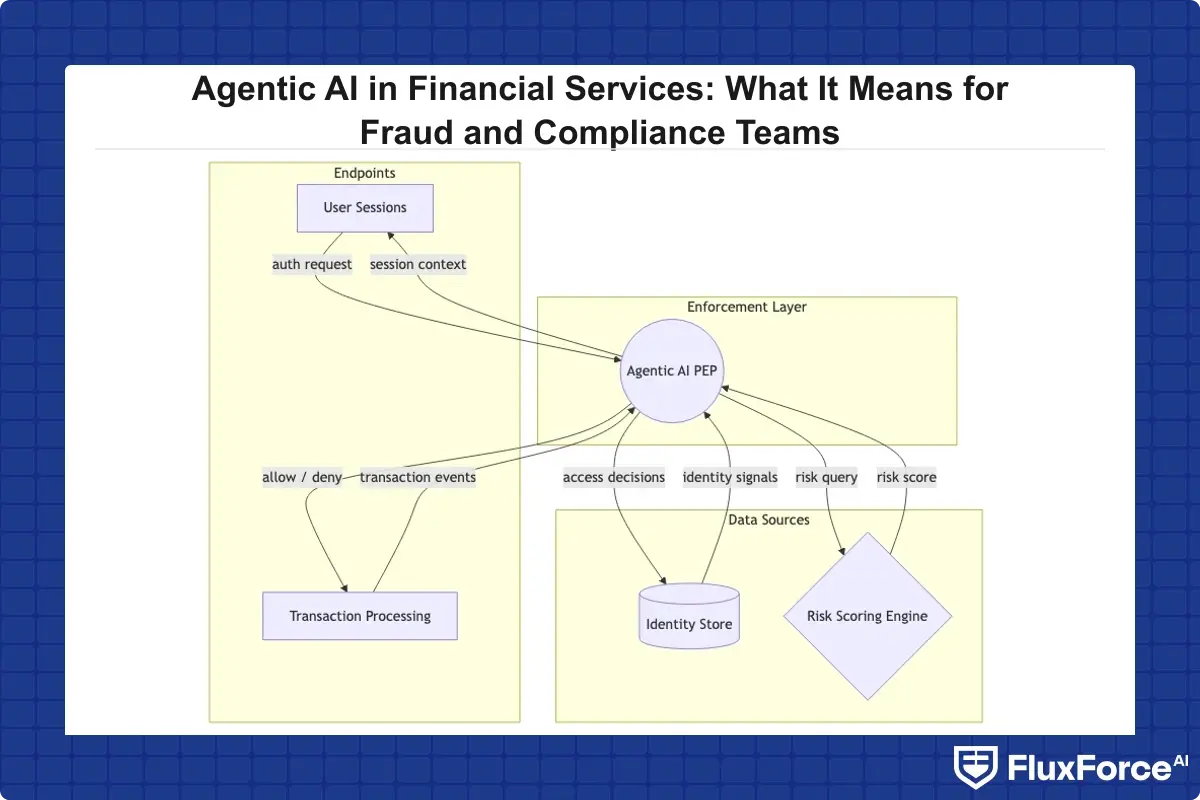

Agentic AI and zero trust financial services are complementary by design. The zero trust model demands continuous verification at every access point. Agentic AI provides the automation to make continuous verification practical at scale. Without AI automation, the never-trust-always-verify principle is operationally impossible for institutions handling millions of transactions daily. The zero trust security framework becomes a practical operating model rather than an aspirational principle only when an agentic enforcement layer handles the verification volume.

How Agentic AI Enforces Zero Trust Policies

In a zero trust security framework, agentic AI acts as the policy enforcement layer. When a user accesses a high-risk function such as a large wire transfer, the agentic system evaluates the current risk score of the session: device integrity, behavioral patterns, time of access, geolocation against historical patterns, and recent authentication events. If anything has changed since the last checkpoint, the agent requires re-verification before allowing the transaction to proceed.

This differs from step-up authentication in legacy systems, which typically triggers only on static thresholds like transaction amount. Agentic AI in a zero trust financial services architecture triggers re-verification based on contextual risk. A transaction that normally clears without challenge might require step-up authentication if the session behavioral pattern looks unusual, even if the amount falls below any defined threshold. The integration of zero trust principles with agentic enforcement is explored in detail in our post on zero trust and agentic AI as the new standard for banking security.

How Compliance Teams Benefit from Agentic AI in Financial Services

Continuous Monitoring and Regulatory Reporting

Compliance teams in financial institutions face a structural problem: regulatory requirements are expanding faster than headcount can scale. Transaction monitoring, sanctions screening, AML checks, and GDPR data handling all require ongoing vigilance across every customer account and every transaction. Agentic AI addresses this by running compliance checks continuously rather than in scheduled batch cycles, and by generating audit-ready documentation as a byproduct of every automated decision.

For compliance officers, this changes the daily workload. Instead of reviewing raw transaction data, analysts review flagged cases with full context already assembled by the agent. Instead of compiling reports manually, they review agent-generated summaries that include the evidence trail for each decision. Teams that have deployed agentic compliance agents report the ability to roll out regulatory compliance agents in 90 days, covering AML, sanctions, and identity checks across their entire customer base without proportional headcount increases.

Reducing Manual Review Workloads

One of the most direct operational benefits of agentic AI financial services is the reduction in manual review volume. When an agentic system handles routine identity verification fintech checks and escalates only genuine ambiguity, the caseload for human analysts drops substantially. Research into agentic fraud systems has shown false positive reductions of up to 80 percent compared to rule-based systems, which directly translates to analyst capacity freed for higher-value investigation work.

Research into agentic fraud systems has shown false positive reductions of up to 80 percent compared to rule-based systems, which directly translates to analyst capacity freed for higher-value investigation work.

The honest limitation here is that agentic AI does not eliminate the need for human reviewers. Edge cases, novel fraud patterns, and regulatory judgment calls still require human expertise. What agentic AI does is filter out the noise so that human expertise is applied where it matters, rather than being consumed by routine checks that a well-designed automated system handles reliably.

Implementation Considerations for Agentic AI Fraud and Compliance Teams

Integration with Existing Systems

Most financial institutions are not starting from a clean slate. They have core banking systems, legacy fraud platforms, and compliance workflows that have been built and refined over years. The most successful agentic AI deployments are designed as an orchestration layer rather than a full replacement: the AI agent coordinates signals from existing systems, adds new data sources where needed, and provides a unified decision surface without requiring a complete infrastructure rebuild.

The identity verification API pattern is particularly useful in this context. Rather than replacing an existing KYC platform, an agentic layer can call the existing platform's API alongside new biometric and behavioral data sources, combining both into a single risk decision. For teams considering this architecture, reviewing how AI layers sit above legacy fraud infrastructure, as covered in the card fraud analytics and AI-powered detection strategy, provides a practical reference for sequencing the integration.

Governance and Auditability

Regulators expect financial institutions to explain their automated decisions. An agentic AI system that produces a decision without a clear audit trail creates compliance risk alongside the fraud risk it was deployed to reduce. Well-designed agentic AI financial services platforms produce decision logs that record every data source queried, every signal weighted, and the reasoning behind the final outcome in human-readable form.

For fraud teams, this means that when a customer disputes a declined application, the analyst can retrieve the exact decision context and explain it clearly. For compliance officers, it means that when a regulator requests documentation of the institution's AML process, agent-generated logs provide the evidence trail without manual reconstruction. Governance should be designed into the agentic AI architecture from day one, because retrofitting auditability onto a system already in production is significantly more complex and introduces its own compliance gaps.

- Traditional fraud detection systems work on rules.

- KYC onboarding speed is a business metric, not just a compliance checkbox.

- Liveness detection fraud is the practice of using a photo, video replay, or 3D mask to spoof a biometric check.

- Synthetic identity fraud is one of the costliest fraud types affecting financial institutions today.

- Deeepfake detection banking is no longer a theoretical concern.

Onboard Customers in Seconds

Conclusion

Agentic AI financial services is delivering measurable results across KYC onboarding speed, synthetic identity fraud detection, and compliance workload reduction. The institutions seeing the clearest gains are those that treat agentic AI as an orchestration layer, coordinating identity verification API calls, biometric identity verification, liveness detection fraud prevention, and deepfake detection banking signals into unified, auditable decisions.

For fraud and compliance teams evaluating where to start, the highest-volume and most repeatable checks in your current workflow are the best candidates for agentic automation first. From there, expanding into zero trust financial services enforcement and adaptive digital identity proofing is a natural progression. Deploying well-designed fraud detection software built on agentic principles reduces time-to-detection and cuts false positives without requiring a full platform replacement, giving your analysts the capacity to focus on cases that genuinely need their judgment rather than routine verification volume.

Share this article