.webp)

Introduction

Real-time fraud detection banks rely on has changed fundamentally in the last five years. Global payment card fraud losses exceeded $33 billion in 2022, and the rise of instant payment rails has made traditional batch-based detection effectively useless against sophisticated attacks. Legacy systems flag fraud hours after funds have moved. Modern AI fraud detection systems stop suspicious transactions before they clear, returning a risk decision in under 300 milliseconds. This post breaks down how real-time fraud detection works at a technical level, why false positive rates cost banks far more than most teams realize, and what criteria actually matter when evaluating transaction monitoring software for payment fraud prevention.

Global payment card fraud losses exceeded $33 billion in 2022, and the rise of instant payment rails has made traditional batch-based detection effectively useless against sophisticated attacks.

- What Is Real-Time Fraud Detection?

- How AI Fraud Detection Works in Banking

- Why False Positives Are the Hidden Drain on Fraud Teams

- What to Look for in Transaction Monitoring Software

- Payment Fraud Prevention in the Age of Synthetic Identities

Onboard Customers in Seconds

What Is Real-Time Fraud Detection?

Real-time fraud detection is the automated analysis of financial transactions at the moment they occur, returning a risk decision before the payment settles. The core distinction from older methods is timing: decisions happen in milliseconds, not after overnight batch runs.

This timing matters because fraud is time-sensitive. A compromised card used at 11 PM can produce dozens of fraudulent transactions before a batch job flags the first one at 6 AM. Real-time systems stop the second transaction before it clears.

How Real-Time Systems Differ from Batch Processing

Batch fraud detection pulls transaction logs on a schedule, typically overnight, runs rule sets or models against the accumulated data, and surfaces a list of suspicious transactions for analyst review. By the time analysts see those flags, funds have usually moved.

Real-time systems treat every transaction as an event. The moment a payment is initiated, it enters a scoring pipeline that evaluates behavioral patterns, device signals, velocity metrics, and geographic context before returning a decision. No waiting, no accumulation.

The Core Components of a Real-Time Detection System

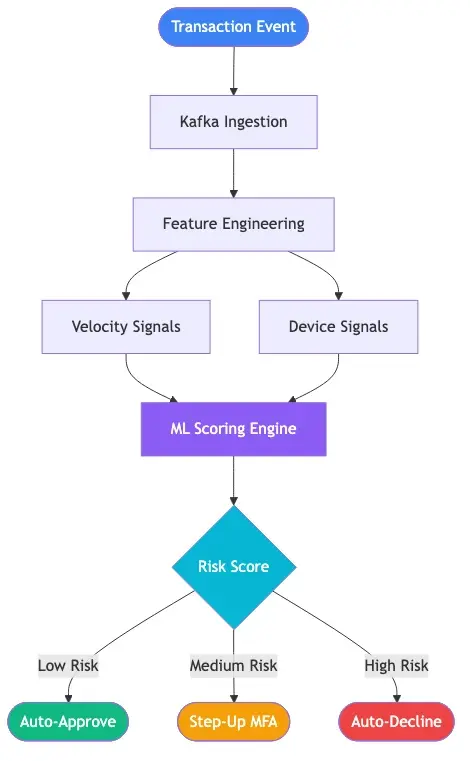

A real-time fraud detection system has four functional layers:

- Data ingestion: Event streaming infrastructure (Apache Kafka is common) that captures transaction events the instant they occur

- Feature engineering: Computes fraud signals in real time, including velocity, device fingerprint matches, geographic distance from the last transaction, and time-of-day patterns

- Scoring engine: ML model inference that produces a fraud probability score

- Decision layer: Routes the transaction to approve, decline, or step-up authentication based on score thresholds configured by product and customer segment

How AI Fraud Detection Works in Banking

AI fraud detection in banking replaces static rule sets with machine learning models trained on historical transaction data. A rule might say "flag any wire over $10,000 from a new device." An ML model learns that a $10,000 wire from a long-tenured business customer on their registered desktop at noon on a Tuesday is low risk, while the same amount from a new device in a foreign country at 2 AM is genuinely suspicious.

That precision is why ai fraud detection explained as simply "replacing rules with ML" undersells the actual benefit. The real gain is fewer false alarms without missing more fraud, which directly affects both operational cost and customer experience.

Machine Learning Fraud Detection Models That Flag Anomalies

Machine learning fraud detection in production systems uses an ensemble approach. No single model type wins across all fraud categories:

- Gradient boosted trees (XGBoost, LightGBM): Excellent on tabular transaction data, fast inference, interpretable outputs

- Neural networks: Handle high-dimensional feature spaces well, particularly for behavioral biometrics

- Graph neural networks: Map relationships between accounts to detect mule networks and money laundering rings

- Unsupervised anomaly detection: Catches novel fraud patterns without requiring labeled training data

Production teams typically run two or three of these in combination, using a meta-model to aggregate scores into a single risk decision.

How Does AI Detect Fraud in Practice?

How does AI detect fraud in a live banking environment? The decision runs in under 300 milliseconds, automatically, in this sequence:

- Customer initiates a payment

- Transaction event is published to the event bus

- Feature service computes 50-200 real-time signals (device match, velocity, behavioral drift, geolocation)

- ML model scores the transaction from 0 (clean) to 1 (certain fraud)

- Score is compared against configurable thresholds by product and customer segment

- Decision is returned: approve, decline, or step-up to MFA

- Outcome is logged and fed back into the model for continuous learning

The feedback loop in step 7 separates good systems from great ones. Models that learn from analyst dispositions stay accurate as fraud tactics shift.

AI Fraud Detection Software: Key Capabilities

When evaluating ai fraud detection software, look beyond raw detection accuracy. The capabilities that determine operational fit include:

- Sub-300ms scoring API latency (required for faster payment rails)

- Explainability outputs showing the top features driving each score

- Configurable thresholds by product, channel, and customer risk segment

- Built-in analyst case management workflow

- Model retraining pipelines with governance controls

- Audit-ready logging for regulatory examination

Explainability is the most commonly underweighted capability during procurement. Analysts who cannot understand why a transaction was flagged cannot work cases efficiently, and regulators increasingly expect documented reasoning for automated decisioning.

Why False Positives Are the Hidden Drain on Fraud Teams

False positives fraud detection generates is not a minor nuisance. It is the primary operational cost driver in most fraud programs, and most institutions dramatically underestimate it.

A manually reviewed false positive costs $6-10 per case once you factor in analyst time, tooling overhead, and customer service calls when a declined legitimate transaction triggers a complaint. At 100,000 alerts per month with an 85% false positive rate, that is $510,000 to $850,000 per month in wasted analyst work, before counting revenue lost from declined legitimate transactions.

False Positive Rate in Fraud Detection: The Numbers

The false positive rate in fraud detection across rule-based systems typically runs between 70% and 95%. That means fewer than 1 in 5 alerts an analyst reviews is actual fraud. The rest is noise.

The false positive rate in fraud detection across rule-based systems typically runs between 70% and 95%.

Organizations that have moved to ensemble ML models with feedback loops report false positive rates dropping to 15-30%. The difference between a 90% false positive rate and a 20% false positive rate is not just operational efficiency. It determines whether your fraud team can scale with the business or becomes a compliance bottleneck that blocks growth.

How to Reduce False Positives in AML

How to reduce false positives in AML is a question most compliance teams overcomplicate. The practical steps are:

- Segment your customer base. Apply different thresholds to different risk profiles. A threshold tuned for retail customers will over-alert on business accounts.

- Retire stale rules. Any rule older than 12 months with a false positive rate above 80% should be reviewed and almost certainly removed.

- Close the feedback loop. Analyst dispositions must feed back into model training. Without this, models drift as fraud patterns evolve.

- Add behavioral baselines. Flag deviations from a customer's own history, not just population-level thresholds.

- Use network analysis. Catching mule account networks early reduces downstream transaction alert volume significantly.

Reducing false positives in transaction monitoring also directly reduces the false positive cost of running a compliance function. This is where the business case for better tooling becomes straightforward to make to finance leadership.

For a detailed breakdown of how AI-driven approaches outperform rule-based systems on this metric, reducing false positives: rule-based systems vs. AI-driven solutions provides a direct comparison with real-world benchmarks.

Fraud Alert Fatigue and Its Impact on Teams

Fraud alert fatigue is what happens when analysts work through queues of low-quality alerts day after day. It is not just inefficiency. It is a risk. When analysts rush dispositions or develop threshold blindness, genuine fraud gets dismissed.

A practical way to measure alert fatigue in your team: track time-to-disposition trends across the workday. If average disposition time increases by more than 40% between morning and afternoon sessions, alert quality is likely the problem, not analyst skill or staffing levels.

What to Look for in Transaction Monitoring Software

Transaction monitoring software selection is where many fraud and compliance teams make avoidable mistakes. They evaluate features rather than operational fit. The better framework: evaluate each tool by what it does to your false positive rate and analyst utilization in a realistic deployment, not by what appears on a vendor comparison slide.

Automated Transaction Monitoring vs. Manual Review

Automated transaction monitoring is not optional at any meaningful scale. A bank processing 300,000 transactions per day cannot manually review all of them. Automation must handle at least 90% of decisioning, routing only genuinely ambiguous cases to human analysts.

Automation must handle at least 90% of decisioning, routing only genuinely ambiguous cases to human analysts.

The most effective deployment structure:

- Auto-approve: Bottom 75-80% by risk score

- Step-up authentication: Middle 10-20% (trigger MFA or behavioral verification)

- Auto-decline: Top 1-3% by risk score

- Human review: 3-8% of ambiguous or context-requiring cases

Teams that route 20-30% of transactions to human review are creating alert fatigue and inflating their transaction monitoring cost unnecessarily.

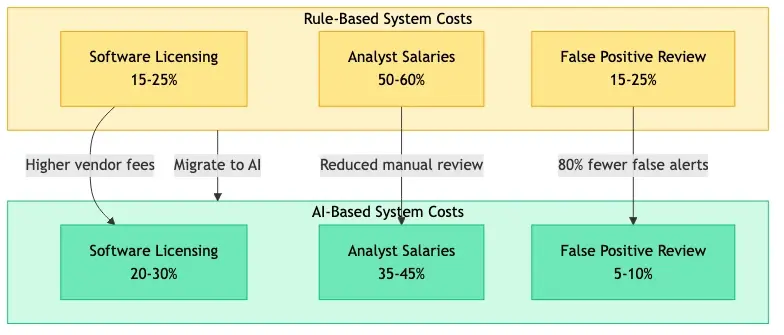

Transaction Monitoring Cost: What Drives the Bill

Transaction monitoring cost has two components that rarely get analyzed together:

- Software licensing: SaaS platforms typically charge $0.002-$0.01 per transaction plus base fees

- Analyst operations: Typically 3-5x the software cost, driven almost entirely by alert volume and false positive rate

This math explains why a $500,000 investment in better ML tooling can return $2-3 million per year in reduced analyst overhead. A 20% improvement in false positive rate translates directly to a 20% reduction in analyst queue volume. For organizations running large fraud operations, that is a material cost saving.

For a deeper look at how agentic AI approaches change this equation, how agentic AI fraud agents cut false positives by 80% covers the mechanics and real-world results in detail.

Payment Fraud Prevention in the Age of Synthetic Identities

Payment fraud prevention has gotten structurally harder because the primary threat profile has shifted. Card fraud and account takeovers remain common, but synthetic identity fraud has become one of the fastest-growing fraud categories in North American financial services, with major banks reporting it now accounts for the majority of their identity fraud losses.

A synthetic identity is not a stolen identity. It is a manufactured one: a valid Social Security number paired with a fabricated name, address, and date of birth. The fraudster builds credit history over months or years with small, legitimate-looking transactions, then "busts out" by maxing every credit line simultaneously and disappearing.

Detecting Synthetic Identity Fraud in Real Time

Synthetic identity fraud is harder to catch with traditional rules because the account behavior during the buildup phase looks legitimate. The signals that distinguish synthetic from genuine identities are subtle: a Social Security number first reported to credit bureaus recently for an applicant claiming to be 45, no utility payments linked to the stated address, an unusually thin but pristine credit file.

ML models trained on identity graph features catch these patterns. Graph analysis links the Social Security number to other accounts sharing phone numbers, addresses, or devices, often revealing a ring of synthetic identities operated by the same fraudster. For a detailed breakdown of detection approaches, detecting synthetic identity fraud in real-time covers current detection methods in detail.

Sardine vs Unit21: How Leading Platforms Compare

The sardine vs unit21 comparison comes up frequently in fraud platform evaluations because both are AI-native platforms that go well beyond static rule engines, but with different operational strengths.

| Capability | Sardine | Unit21 |

|---|---|---|

| Real-time scoring latency | Sub-100ms | Sub-200ms |

| Device and behavioral intelligence | Very strong | Basic |

| AML case management | Basic | Full-featured |

| Synthetic identity detection | Strong (device + behavioral graph) | Strong (account graph analysis) |

| ML explainability | High (per-decision API) | Medium |

| Regulatory reporting | Limited | Comprehensive |

| Integration complexity | Low (REST API) | Medium (event-based) |

The honest answer: most mid-to-large banks should not treat this as a binary choice. Sardine performs better for real-time payment fraud on digital channels. Unit21 performs better for AML case management and regulatory reporting. Many teams run both in parallel, using Sardine for real-time fraud scoring and Unit21 for AML investigation workflows.

For teams also evaluating AI-powered approaches across card fraud specifically, card fraud analytics and AI-powered fraud detection strategy for risk heads provides a practical decision framework.

Why Real-Time Fraud Detection Matters for Banks Right Now

The urgency around real-time fraud detection banks face is driven by three converging forces: faster payment networks that eliminate settlement buffers, rising synthetic identity fraud that defeats rule-based detection, and regulatory expectations that now explicitly address AI-based controls.

Real-Time Fraud Detection Banks Need for Faster Payment Networks

FedNow (launched 2023) and the UK's Faster Payments system have removed the settlement window that traditional fraud detection used as a buffer. When money moves in 5 seconds, a detection system that takes 5 minutes is not a fraud control. It is a post-incident reporting tool.

Real time fraud detection banks deploy must operate at sub-second latency without exceptions. This is also why fraud detection needs to integrate directly with authentication signals, device intelligence, and behavioral biometrics. It does not operate in isolation from access controls. For context on how these systems connect, banking access controls and zero trust security architecture for banking operations covers the security layer that feeds directly into fraud scoring decisions.

The Regulatory Angle: AI Fraud Detection in Banking

AI fraud detection in banking is increasingly expected by regulators, not just permitted. FinCEN has published guidance encouraging financial institutions to use innovative technologies for AML compliance, with explicit acknowledgment that AI-based systems can satisfy regulatory requirements when proper governance is in place. The EBA in Europe has updated internal governance guidelines to allow AI-based transaction monitoring, provided banks document model explainability and maintain human oversight.

The FATF risk-based approach guidance for the banking sector also explicitly supports technology-driven controls as part of a sound AML framework. For compliance officers managing the documentation requirements of this transition, AI vs. traditional fraud detection: key differences every risk officer should know provides a framework that maps directly to regulatory examination criteria.

- Real-time fraud detection is the automated analysis of financial transactions at the moment they occur, returning a risk decision before the payment settles.

- AI fraud detection in banking replaces static rule sets with machine learning models trained on historical transaction data.

- False positives fraud detection generates is not a minor nuisance.

- Transaction monitoring software selection is where many fraud and compliance teams make avoidable mistakes.

- Payment fraud prevention has gotten structurally harder because the primary threat profile has shifted.

Onboard Customers in Seconds

Conclusion

Real-time fraud detection banks deploy today needs to do three things well: catch fraud before settlement, keep false positive rates low enough that analyst teams remain effective, and produce explainable outputs that regulators can review. AI fraud detection, specifically ML-based systems with continuous feedback loops, outperforms rule-based alternatives on all three dimensions. The evidence is consistent across institutions that have made the transition.

The practical starting point for most teams is not a full platform replacement. Start with the false positive problem. If your team reviews 10,000 alerts per month and 8,500 are legitimate transactions, fixing that single metric will fund the broader AI investment through analyst cost savings alone. To understand what modern approaches can achieve, AI vs. traditional fraud detection is the logical next read for any risk officer evaluating where to invest first.

Share this article