.webp)

Introduction

AI in banking 2026 is generating more noise than almost any technology shift the industry has seen in the past decade. Every major bank claims to be "AI-first." Every vendor promises 10x efficiency gains. But if you talk to the compliance officers and risk heads actually running these systems day-to-day, a more complicated picture emerges.

For financial institutions looking to address these challenges, core banking modernization & security solutions offer a proven path forward.

Some AI deployments in banking are working well. Others have burned budgets and produced dashboards that nobody reads. The difference between success and failure is rarely the sophistication of the underlying model. It's whether the deployment fits the operational reality of a regulated institution and whether success was defined before the contract was signed.

This post cuts through the noise. We examine where ai automation banking is producing verified results, what the honest ROI on fraud and compliance tools looks like, and what financial institutions should actually evaluate before signing another vendor contract.

- What the Headlines Get Wrong About AI in Banking 2026

- Where AI Automation in Banking Is Actually Delivering Results

- The Real Cost of Compliance: Why Manual Processes Can't Scale

- How Agentic AI Banking Is Changing Risk Operations

- Fraud Prevention ROI: What the Numbers Actually Show

Onboard Customers in Seconds

What the Headlines Get Wrong About AI in Banking 2026

AI in banking 2026 looks very different from the glossy conference presentations. The hype says every bank will be autonomous and self-healing by year's end. The reality is messier, and that's acceptable because "messy but measurable" is what regulated institutions actually need.

The Hype Cycle vs. Reality in Financial Services

The ai in banking hype vs reality gap is widest in three areas: conversational AI for customer service, generative AI for document processing, and autonomous trading systems. Banks that rushed into chatbot deployments without grounding them in proper data governance found themselves managing customer complaints about hallucinated account information. A McKinsey analysis of AI in financial services estimated that only 30% of financial institutions had moved beyond proof-of-concept on their AI initiatives as of 2024, meaning most banks are still in early deployment stages rather than operating at scale.

A McKinsey analysis of AI in financial services estimated that only 30% of financial institutions had moved beyond proof-of-concept on their AI initiatives as of 2024, meaning most banks are still in early deployment stages rather than operating at scale.

The institutions doing well with AI are not the ones chasing the newest model releases. They are the ones who picked one or two specific workflows, measured baseline performance honestly, and deployed AI against that specific problem with proper human oversight built in from the start.

Why "AI-Powered" Doesn't Always Mean AI-Driven

A pattern that keeps showing up in vendor evaluations: a platform is labeled "AI-powered" because it uses a rules engine with a machine learning scoring component layered on top. That's not inaccurate, technically, but it's also not what most compliance or risk officers think they're buying.

Before evaluating any platform, ask vendors to show you exactly which decisions the AI makes autonomously, which ones it flags for human review, and what the escalation path looks like when it's uncertain. Vendors who cannot answer those questions clearly are selling a wrapper, not a working system.

Where AI Automation in Banking Is Actually Delivering Results

The areas where ai automation banking shows consistent, measurable results are not the glamorous ones. They are transactional, repetitive, and high-volume: exactly the kind of work where human teams burn out and errors accumulate over time.

KYC and AML Automation: Measurable Wins

Know Your Customer (KYC) onboarding used to take anywhere from three to fifteen days at mid-sized banks, depending on customer type. AI-driven identity verification with automated document classification and sanctions screening has cut that to under 24 hours in production deployments. The speed improvement is significant, but the error reduction often matters more: human transcription errors on manual data entry drop substantially when the system captures fields directly from source documents rather than relying on human input.

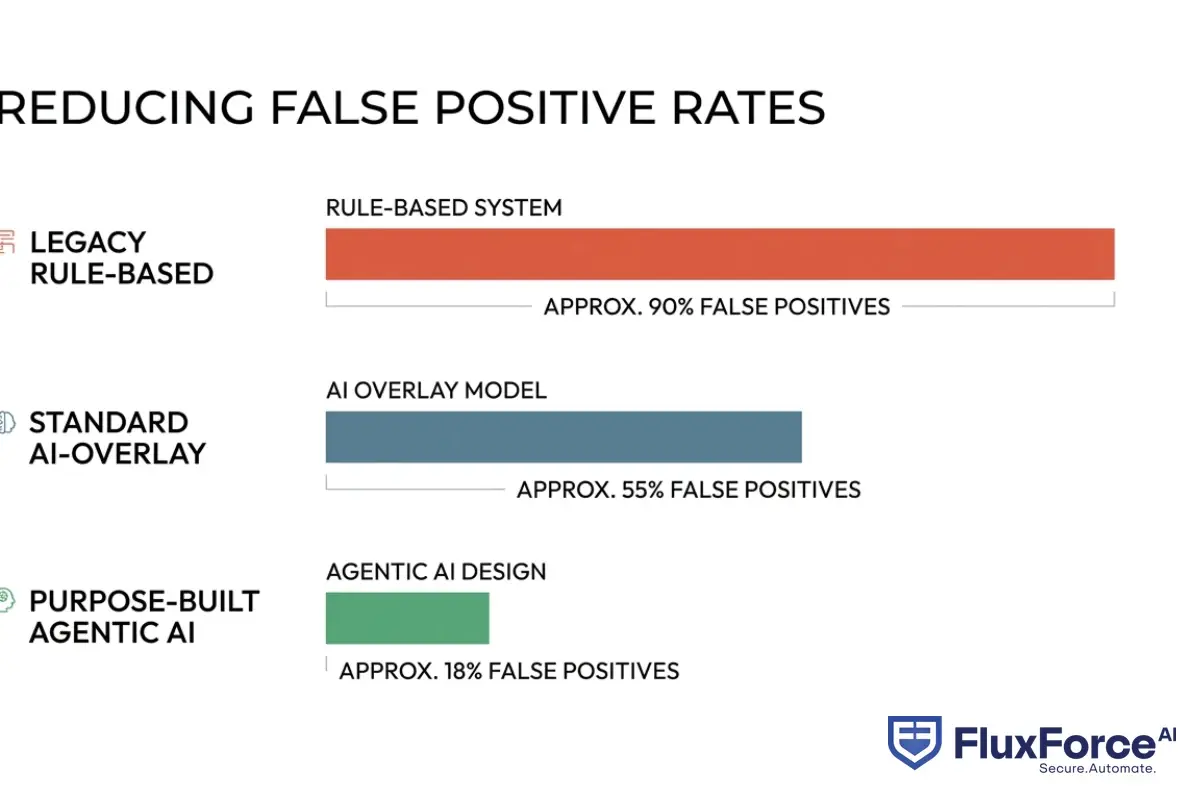

For AML transaction monitoring, the pattern is similar. Rule-based systems generate high false positive rates, sometimes flagging 95% of alerts as legitimate transactions on closer review. AI models trained on institution-specific transaction patterns bring that false positive rate down materially, which directly reduces the analyst hours burned per alert. We cover the mechanics of this shift in our post on AI-powered fraud detection strategy for risk heads.

How the Hype vs. Reality Gap Shows Up in Fraud Detection

The honest answer on fraud detection is that results vary significantly by starting point. A bank with a sophisticated rules-based fraud system will see smaller percentage gains from adding AI than a bank running legacy batch-processing systems. But in both cases, the gains are real and trackable.

The key metric to track is not "AI detects more fraud." Track the ratio of fraud detected to false positives generated. A system that catches 20% more fraud but generates 40% more false alerts has made the compliance team's job harder, not easier. This is where agentic ai banking approaches diverge meaningfully from traditional AI bolted onto legacy infrastructure.

A system that catches 20% more fraud but generates 40% more false alerts has made the compliance team's job harder, not easier.

The Real Cost of Compliance: Why Manual Processes Can't Scale

The cost of compliance financial services is not just a line item on a budget. It's a structural drag on growth. With DORA, Basel IV reporting, and evolving AML directives all active simultaneously in 2026, the volume of compliance work is increasing, not decreasing.

Cost of Compliance Financial Services: A Growing Burden

According to the Bank for International Settlements, compliance costs for major financial institutions have grown consistently since 2020, with the number of regulatory changes requiring operational response increasing year over year. For a mid-sized bank with a compliance team of 50 people, that trajectory means adding staff every year just to maintain the same coverage level, before accounting for any growth in transaction volume.

The manual compliance cost problem gets worse when you factor in error costs. A missed suspicious activity report (SAR) filing carries regulatory penalties that dwarf the cost of the analyst time that would have caught it. AI automation removes the human fatigue variable from this equation and creates an auditable trail that regulators can examine directly.

What Manual Compliance Really Costs Per Year

Most institutions do not calculate compliance cost per transaction, which is the number that actually matters for scaling decisions. If your compliance workflow costs $2.40 per transaction at current volume, what happens when volume doubles? Manual processes scale linearly with volume. AI-driven processes scale more favorably, with marginal cost often dropping as volume increases because the fixed cost of the model is already paid.

A useful planning framework: calculate your current per-transaction compliance cost, then model what happens at 2x, 5x, and 10x volume. If the number becomes operationally unworkable at 5x, you have a scaling problem that cannot be solved by hiring. That's the point where compliance automation roi moves from theoretical to urgent.

Our detailed comparison of manual compliance vs. AI automation walks through this cost modeling approach with specific numbers and scenario planning frameworks.

How Agentic AI Banking Is Changing Risk Operations

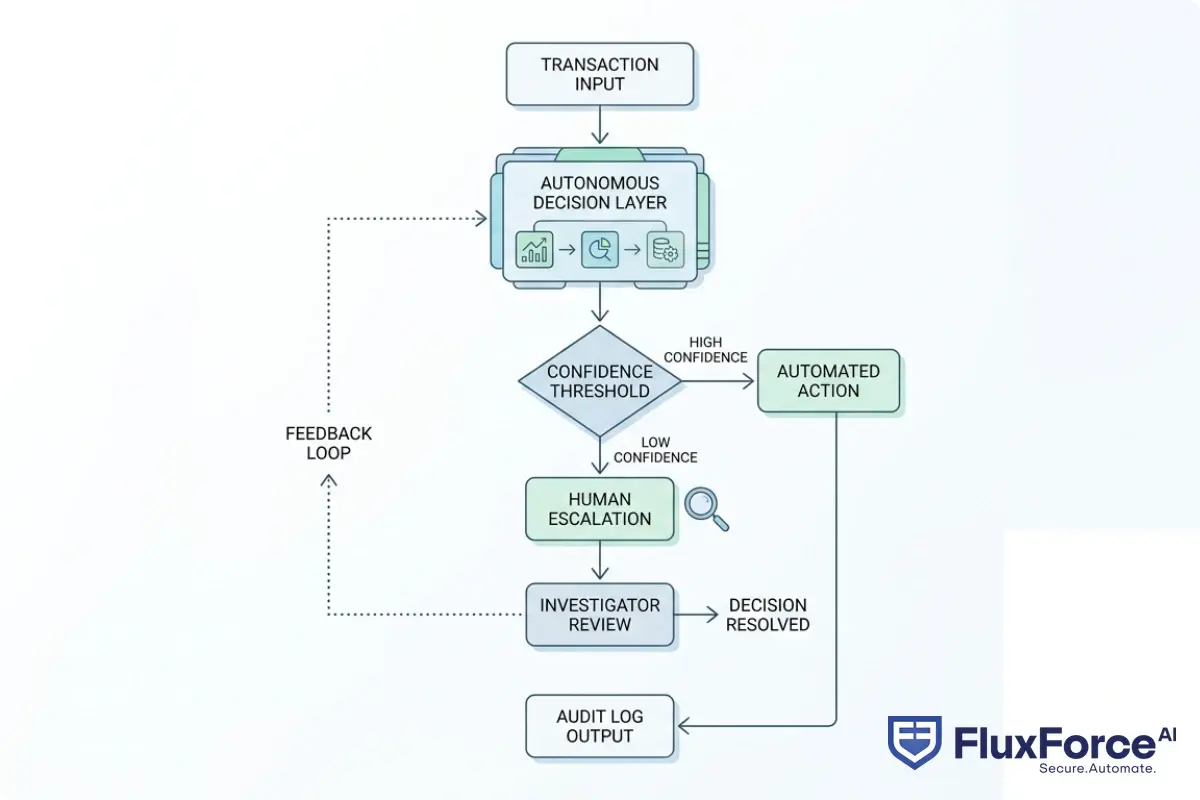

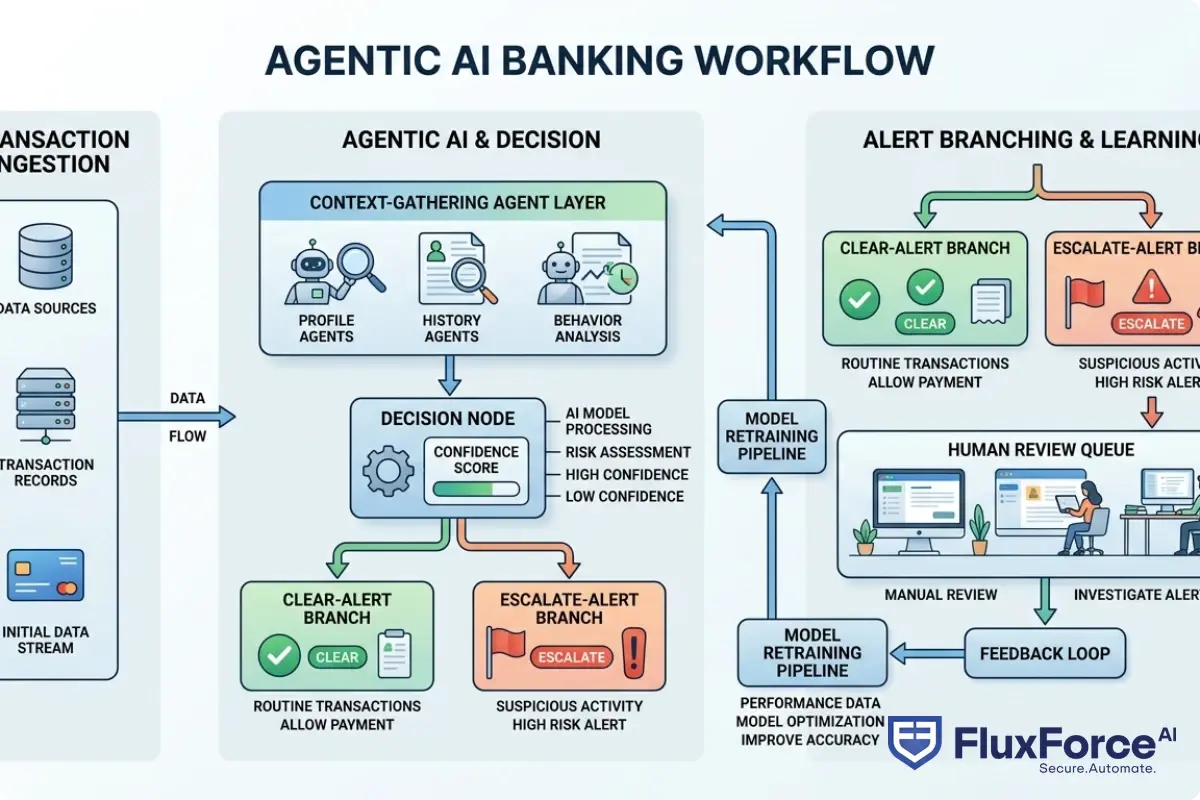

Agentic ai banking describes a specific architecture, not just a marketing term. An agentic system takes multi-step actions, maintains context across a workflow, and makes or escalates decisions based on defined rules without requiring human input at each stage. This is meaningfully different from a static AI model that classifies transactions and stops there.

Agentic AI Financial Services: Beyond Simple Automation

In agentic ai financial services, a single agent might: receive a transaction flag, pull the customer's full transaction history, check against current watchlists, assess the pattern against known fraud typologies, and either clear the alert or escalate it with a pre-drafted SAR narrative. All of that happens without a human touching the workflow until escalation is required.

That sequence used to take an analyst 45 minutes. With a properly configured agentic system, the same workflow completes in seconds for clear-cut cases. The analyst only sees escalated cases that require genuine judgment. The result is that the same team covers significantly more ground without adding headcount, which directly affects manual compliance cost calculations when building a business case.

For a technical look at how this architecture integrates with security controls, our post on Zero Trust and Agentic AI covers the combination in banking environments specifically.

Decision-Making at Scale Without Human Bottlenecks

The design principle behind agentic AI in banking is "autonomy within guardrails." The system operates independently inside a defined decision envelope. Outside that envelope, it escalates. This is not a new concept in financial services: loan approval systems have worked this way for years. What's new is the breadth of compliance and risk workflows where that model now applies, including sanctions screening, AML monitoring, and regulatory reporting.

Compliance teams that have deployed agentic systems consistently report one shift: their work stops being reactive (processing backlogs of alerts) and becomes more proactive (reviewing edge cases and refining the decision rules the agent uses). For institutions looking at deployment timelines, rolling out regulatory compliance agents in 90 days is a realistic target for a focused implementation with a clear starting workflow.

Fraud Prevention ROI: What the Numbers Actually Show

Fraud prevention roi is one of the most-cited and least-standardized metrics in financial technology marketing. Every vendor has a case study showing dramatic results. Most of those case studies select the best deployments and do not represent typical outcomes across the customer base.

Total Cost of Ownership Fraud Platform: A Realistic Framework

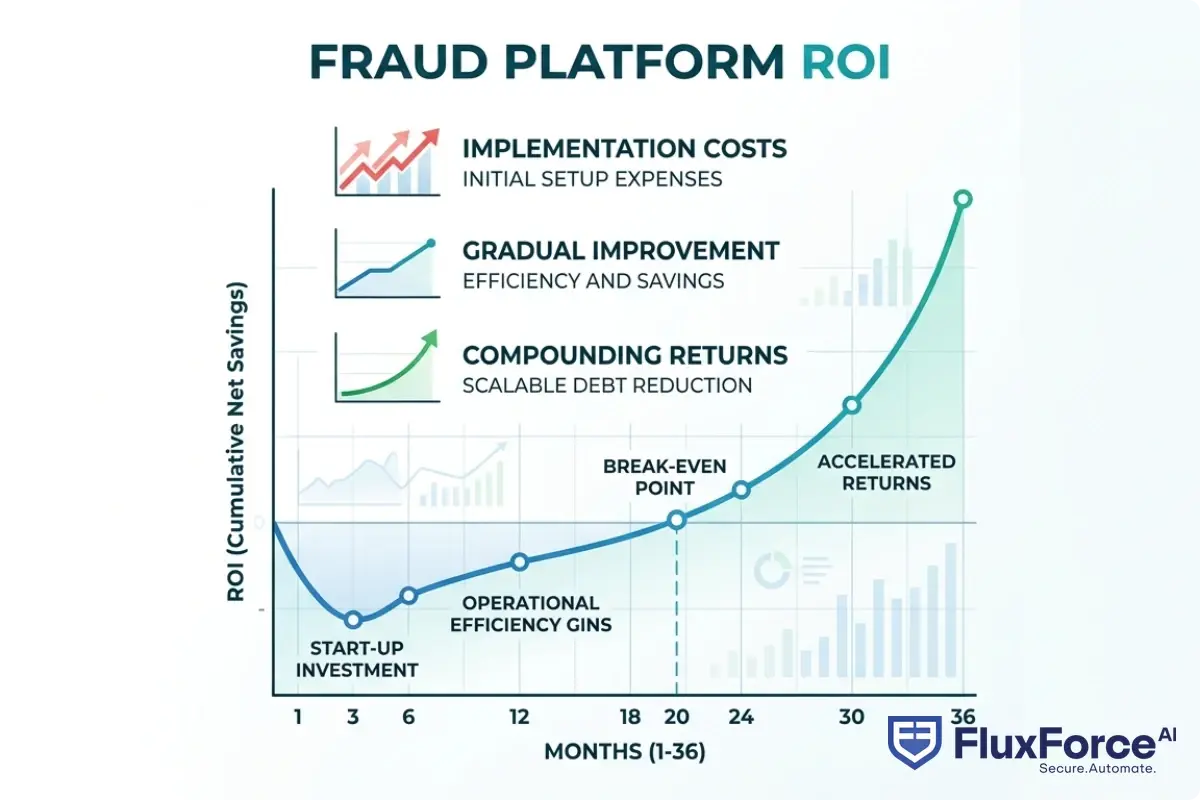

The total cost of ownership fraud platform calculation must include more than the licensing fee. Factor in: implementation costs (typically 2-3x the annual license for complex integrations), training time for the compliance team, ongoing model retraining as fraud patterns evolve, and the cost of both false negatives (fraud that gets through) and false positives (legitimate transactions blocked unnecessarily).

When all those costs are included, the payback period for a well-implemented AI fraud platform at a mid-sized institution is typically 18-24 months, not the "6-month ROI" that vendor presentations often claim. That doesn't mean the investment isn't worthwhile. It means your business case needs realistic assumptions built in from the start. Our analysis of how agentic AI fraud agents cut false positives by 80% gives a detailed breakdown of where efficiency gains actually come from in production environments.

Our analysis of how agentic AI fraud agents cut false positives by 80% gives a detailed breakdown of where efficiency gains actually come from in production environments.

Fraud Prevention ROI in Practice

The institutions seeing the best fraud prevention roi share a few characteristics. They defined success metrics before deployment, not after. They maintained a control group to measure incremental lift from the AI system versus their existing baseline. And they committed to at least 12 months of data before drawing conclusions about performance.

Banks that skip that measurement discipline end up in an ambiguous situation: the AI system is running, fraud losses haven't spiked, but nobody can prove the AI is the reason. That ambiguity makes it harder to justify the next investment in AI automation, and it often means the organization fails to capture the full operational benefit of the system it's already paying for.

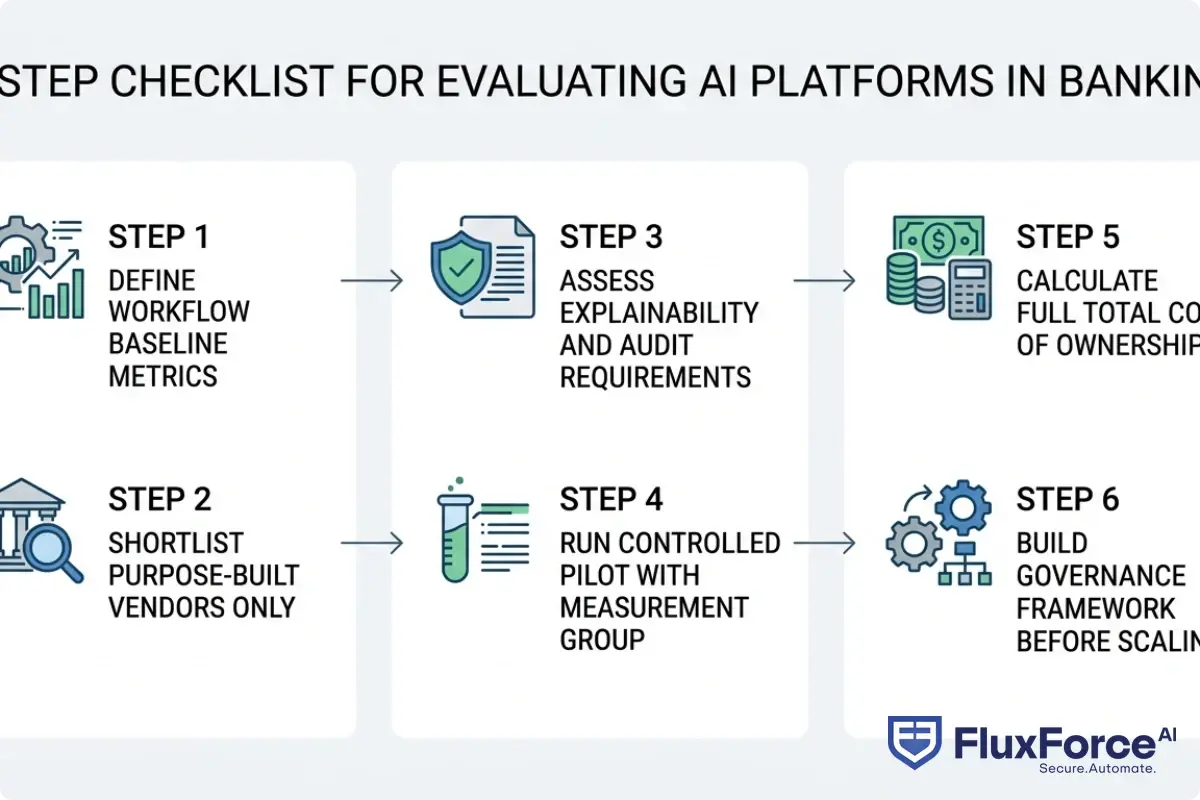

What to Look for in an AI Platform for Financial Services

The future of ai in banking is not one platform that does everything. It's a composable architecture where specialized AI agents handle specific workflows with clear data boundaries and auditability at every decision point. Evaluating platforms against that standard changes the questions you bring to vendor conversations.

When conducting your own fluxforce review or any vendor evaluation, the most important factors are explainability (can you show a regulator exactly why the system flagged a transaction?), integration depth with existing compliance workflows, and the vendor's approach to model governance and retraining as fraud patterns shift.

FluxForce AI: An Honest Assessment

FluxForce is built specifically for regulated financial services, which means it starts from a different constraint set than general-purpose AI platforms. The core design principle is that every decision the AI makes must be explainable, auditable, and reversible. In banking, that's a regulatory requirement, not a nice-to-have feature.

In practice, fluxforce ai handles workflows including transaction monitoring, KYC automation, sanctions screening, and compliance reporting. The platform operates as agentic workflows: each compliance function runs as a connected agent that pulls context, makes decisions, and hands off to the next stage without manual intervention at routine steps.

What makes fluxforce review conversations with actual users interesting is that the consistent feedback is not about feature lists. It's about reduced alert fatigue. Compliance teams that were processing 400 alerts per day with 90% false positive rates are now processing 80 escalated cases per day with materially higher true positive rates. The work is different in character, not just in volume.

A fair limitation worth noting: FluxForce is not the right tool if you need general-purpose LLM capabilities or customer-facing AI features. It's a back-office compliance and risk operations platform. If that's the workflow you need to improve, it's worth a serious evaluation. If you need a customer chatbot or a generative AI writing tool, that's a different product category entirely.

What the Future of AI in Banking Looks Like

The future of ai in banking is more specific and more practical than the fully autonomous bank that press releases describe. AI handles the high-volume, pattern-based work that humans do poorly at scale. Humans retain judgment on the cases that require contextual reasoning, nuanced regulatory interpretation, or considerations that sit outside a model's training distribution.

The institutions that will be best positioned in 2027 and 2028 are the ones building that human-AI handoff carefully now: defining decision envelopes, establishing oversight models, and constructing governance frameworks that regulators will increasingly require. The NIST AI Risk Management Framework is a practical starting point for that governance work, particularly for institutions operating under US regulatory oversight.

- AI in banking 2026 looks very different from the glossy conference presentations.

- The areas where ai automation banking shows consistent, measurable results are not the glamorous ones.

- The cost of compliance financial services is not just a line item on a budget.

- Agentic ai banking describes a specific architecture, not just a marketing term.

- Fraud prevention roi is one of the most-cited and least-standardized metrics in financial technology marketing.

Onboard Customers in Seconds

Conclusion

AI in banking 2026 is neither the revolution the hype promises nor the dead end the skeptics claim. It's a set of specific tools that work well for specific problems when deployed with clear measurement, realistic expectations, and proper governance structures.

The banks seeing real returns from ai automation banking share a consistent pattern: they started with one workflow, measured it honestly, and scaled from there. They did not buy a platform and declare victory. They built the operational muscle for measuring AI performance and let that guide investment decisions over time.

If you're evaluating your own compliance automation roi or considering a fraud prevention platform upgrade, the questions that matter most are practical ones. What is your current per-transaction compliance cost? What is your false positive rate on fraud alerts today? Can your current architecture scale to 5x volume without proportionally increasing headcount?

If those answers concern you, the tools to address them are working in production at comparable institutions right now. The honest next step is not another vendor briefing. It's building a baseline so you know what you're actually measuring when the AI goes live. Explore how FluxForce approaches agentic compliance and fraud automation at fluxforce.ai.

Share this article