.webp)

Introduction

OFAC screening mistakes are the compliance failure most financial institutions promise they've fixed after every regulatory cycle, and yet the fines keep coming. According to the U.S. Department of the Treasury's OFAC, civil monetary penalties for sanctions violations have remained persistently high, with many enforcement actions tracing directly back to preventable screening gaps: stale watchlists, misconfigured name-matching thresholds, and manual review queues that collapse under high transaction volumes. This post breaks down the errors compliance teams repeat most often, how AML compliance programs can close those gaps, and what your team needs to prioritize heading into 2026.

- Why OFAC Screening Mistakes Keep Happening

- How Sanctions List Management Fails in Practice

- AML Compliance Failures: When Name Matching Logic Breaks Down

- How KYC Automation Closes the Gaps in OFAC Screening

- What Your BSA/AML Compliance Checklist Must Cover

Onboard Customers in Seconds

Why OFAC Screening Mistakes Keep Happening

The honest answer is that most OFAC screening programs were designed for a different transaction environment. When a compliance team built their screening workflow five years ago, they might have been processing 50,000 transactions a day. Today that number could be 500,000. The matching rules, false positive thresholds, and manual review capacity didn't scale with volume.

AML compliance, at its core, is a data quality problem disguised as a process problem. Teams focus on whether the screening tool ran, not whether the underlying data was accurate or the thresholds were correctly calibrated for their current customer population.

The Scale Problem in Modern Transaction Volumes

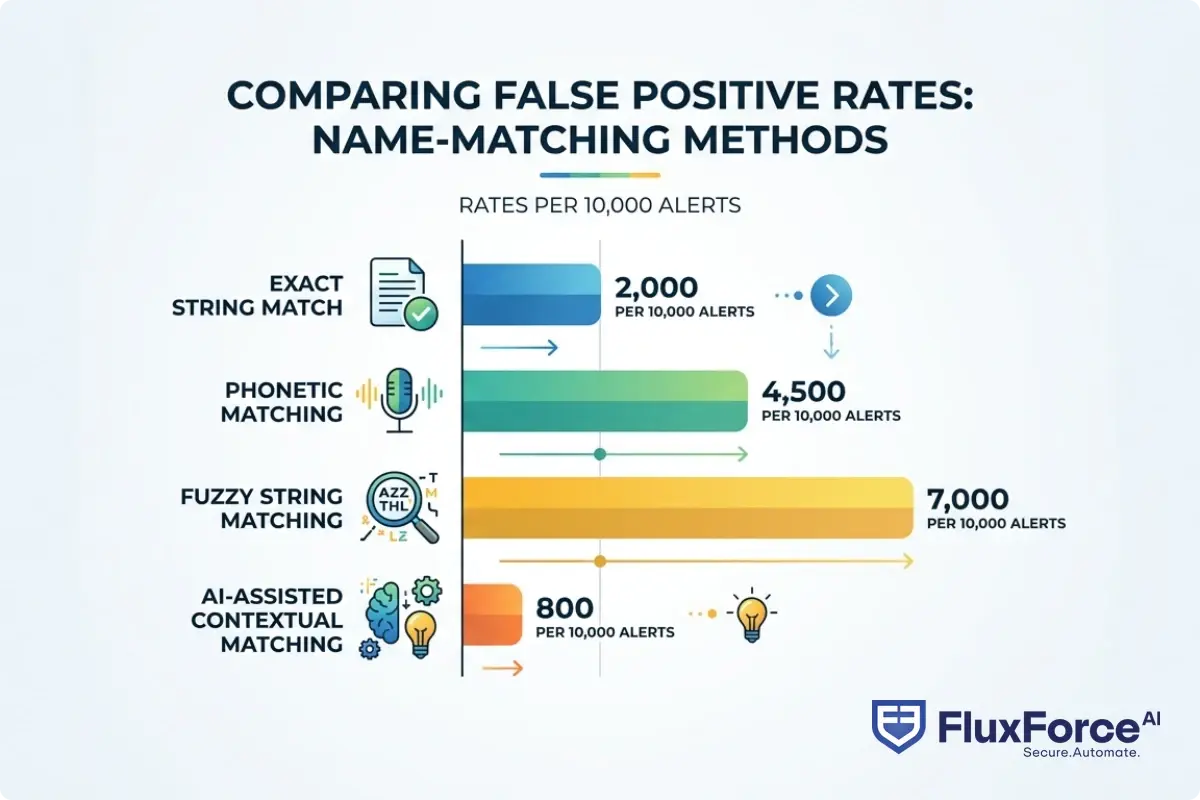

Most legacy screening systems generate alerts based on name-similarity scores set years ago by a compliance analyst who no longer works at the firm. Nobody revisited those thresholds when transaction volumes tripled. The result is false positive rates that bury real hits under noise, and real hits that slip through because the threshold was set too loose in the opposite direction.

A compliance officer at a mid-size digital bank shared that their team was reviewing 1,200 manual alerts per day, of which fewer than 0.3% led to a genuine match. That's not a screening program; that's a manual sorting exercise. Agentic AI systems can cut false positive rates by up to 80% by adjusting match scores dynamically based on transaction context, not just name similarity alone.

A compliance officer at a mid-size digital bank shared that their team was reviewing 1,200 manual alerts per day, of which fewer than 0.3% led to a genuine match.

Organizational Gaps That Let Errors Persist

OFAC screening mistakes also persist because of how compliance teams are structured. The person who configures the screening software is often different from the person who reviews alerts, who is also different from the person who updates the SDN list feeds. Each handoff is a potential failure point with no clear accountability.

Fintechs face this challenge differently than banks. A fintech BSA/AML small team might have one compliance generalist covering screening, SAR filing, and customer due diligence simultaneously. That kind of coverage gap is exactly what regulators document in enforcement actions, and it's a structural problem that technology can partially address.

How Sanctions List Management Fails in Practice

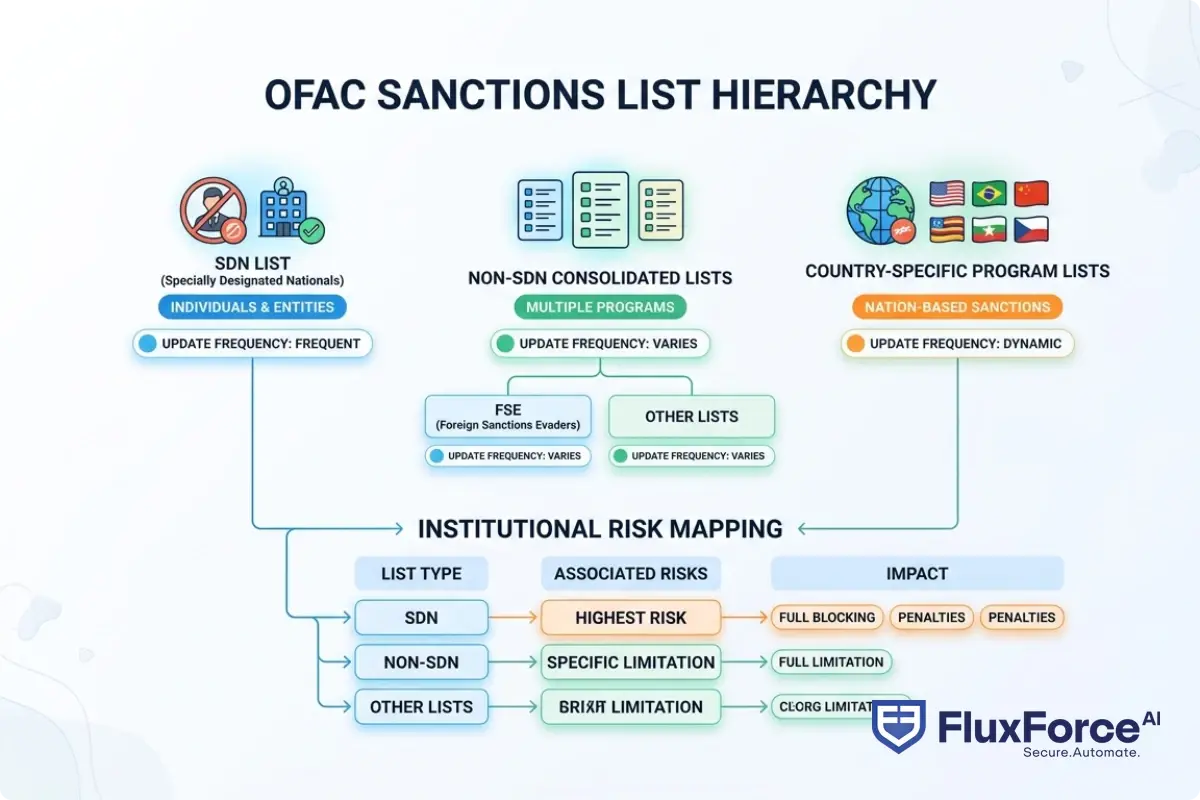

One of the most consistent OFAC screening mistakes is treating the Specially Designated Nationals (SDN) list as a static file rather than a live feed. OFAC updates its sanctions lists multiple times per week. Some organizations sync their screening databases nightly. That's a 24-hour window where transactions can clear against an outdated list.

This is part of a broader BSA/AML compliance checklist failure: teams document that they use OFAC screening but don't document the update frequency, version control, or reconciliation process for the lists themselves. A thorough aml risk assessment guide should inform which customer segments get screened more frequently and with tighter thresholds, based on their inherent risk profile and transaction patterns.

Using Stale or Incomplete Watchlists

The SDN list is only one of several OFAC consolidated sanctions programs. Many institutions screen against the SDN list but fail to also incorporate the Non-SDN Consolidated Sanctions List, the FSE List (Foreign Sanctions Evaders), and country-specific program lists. A transaction involving a party on the FSE list that clears because the screening tool only checked the SDN list is still a sanctions violation.

For community banks, this gets tricky. A bsa aml compliance community banks program often relies on a core banking vendor's built-in screening module, which may not cover all OFAC list variants. It's worth confirming with your vendor exactly which lists are checked, how often they update, and whether you receive any notification when a list update fails.

How Fuzzy Matching Thresholds Create False Negatives

The opposite problem from too many false positives is false negatives: matches that should trigger a hit but don't because the similarity score falls just below the configured threshold. This is where OFAC screening mistakes become genuinely dangerous, because the institution processes a transaction it should have blocked.

A name like "Ahmad Karimi" might score below threshold against "Ahmed Karami" if the matching algorithm weights exact character matching heavily. These could be the same individual, particularly in contexts where transliteration from Arabic or Farsi produces multiple valid romanizations of the same name.

AML Compliance Failures: When Name Matching Logic Breaks Down

Name matching is the technical core of OFAC screening, and it's where most programs have the weakest documentation. AML compliance programs typically specify that screening must occur, but rarely specify how the matching algorithm was selected, validated, or calibrated for the institution's specific customer population.

For AML compliance in fintech, this gets more complicated because fintech customer bases often include high proportions of non-Western names, dual citizens, and customers who entered their own names inconsistently across multiple onboarding flows or account types.

Why Transliteration Errors Cause OFAC Screening Mistakes

A customer might appear in your system as "Mohammed Al-Rashid" but on the SDN list as "Muhammad al-Rasheed." Both are valid transliterations of the same Arabic name. Without phonetic matching or transliteration normalization, your screening system won't connect them, and a genuine hit will be processed as a clean transaction.

This is a documented challenge in the industry. The Financial Action Task Force (FATF) has published guidance on name-matching in digital identity contexts that compliance teams can use as a starting framework for calibrating their matching logic against their specific customer population demographics.

Handling Aliases, Name Variants, and Non-Latin Scripts

The SDN list includes aliases for listed individuals. A proper screening system checks against all listed aliases, not just the primary name entry. Some AML compliance software products handle this automatically; others require manual configuration of alias matching at implementation, which teams often skip.

For institutions with customers who provide names in non-Latin scripts (Cyrillic, Arabic, Chinese characters), the screening program needs to either transliterate those names before matching or maintain a parallel screening process against non-Latin versions of the relevant lists. This is an area where anti money laundering technology has improved significantly, with modern platforms supporting multi-script matching natively.

How KYC Automation Closes the Gaps in OFAC Screening

KYC automation changes the OFAC screening equation in two important ways. First, it standardizes how customer identity data is collected and formatted at onboarding, reducing the downstream matching problems caused by inconsistent name entry. Second, it enables continuous screening rather than one-time checks at account opening.

As covered in our analysis of AML screening in digital lending, continuous monitoring catches the cases that point-in-time screening misses: customers who were clean at onboarding but were later added to sanctions lists, sometimes weeks or months after the relationship was established.

What KYC Automation in 2026 Actually Does Differently

KYC automation in 2026 is less about automating the collection of identity documents and more about building a structured data pipeline from document capture through identity verification through watchlist screening. Modern systems extract structured name, date of birth, and nationality data from government ID documents with high accuracy, then normalize that data before it reaches the screening layer.

This matters for OFAC compliance because the garbage-in-garbage-out problem is real. If your onboarding form accepts free-text name entry with no validation, you'll have inconsistent data that degrades screening quality throughout the account lifecycle. KYC automation with document-based identity verification solves this at the source, before bad data propagates into your screening records.

Continuous Monitoring vs. Point-in-Time Checks

KYC/CDD requirements for banks increasingly specify ongoing monitoring, not just onboarding checks. But many institutions interpret "ongoing monitoring" as running a batch screening job once a month against their customer database. That's insufficient for sanctions compliance.

OFAC can designate a new SDN on any business day. A customer who was clean yesterday might be sanctioned today. Real-time or near-real-time screening against updated lists is the standard that enforcement actions are increasingly using to evaluate program adequacy. Our guide on KYC/AML identity verification for high-risk customers covers the specific monitoring frequency expectations regulators are applying in examinations right now.

Enhanced due diligence requirements for high-risk customers make continuous monitoring even more pressing. An enhanced due diligence program that runs enhanced screening only at onboarding doesn't meet the spirit of ongoing monitoring requirements, and examiners have made this point explicitly in recent enforcement actions.

What Your BSA/AML Compliance Checklist Must Cover

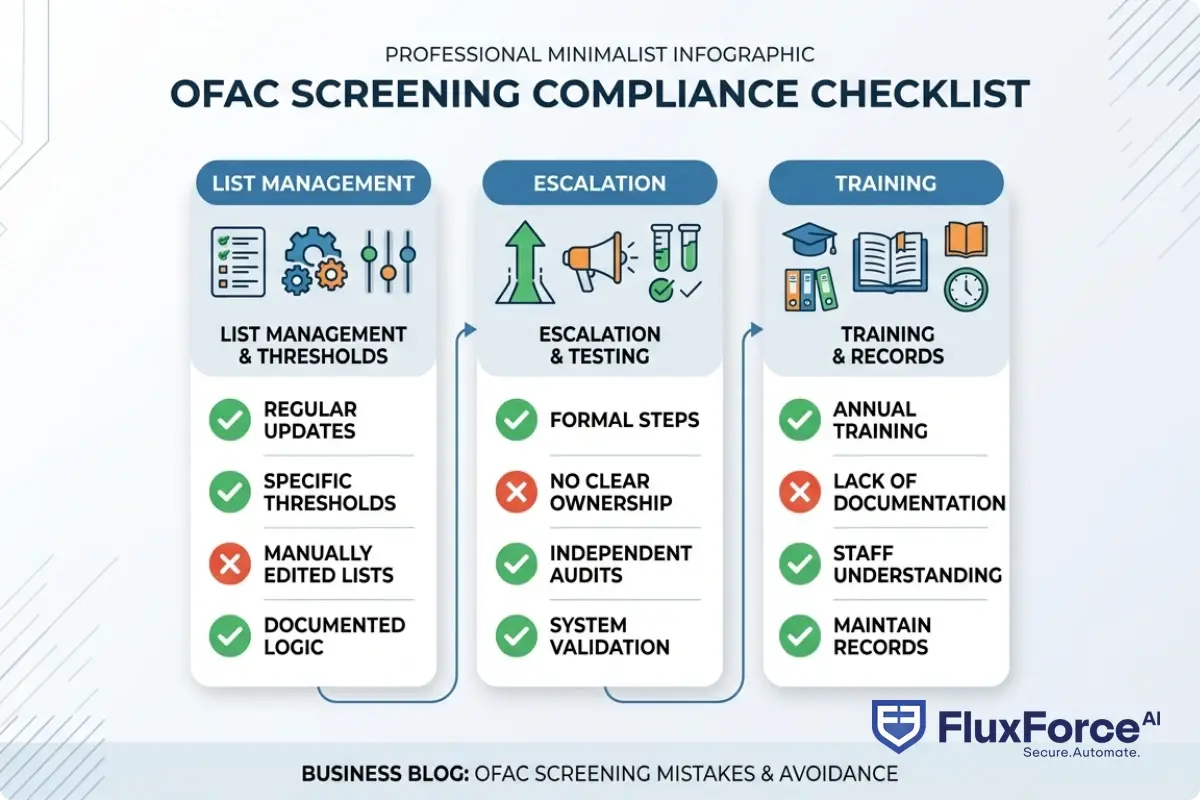

A proper BSA/AML compliance checklist for OFAC screening isn't long, but every item on it needs documentation that survives an examination. These are the gaps examiners most commonly find when reviewing screening programs:

- List coverage: Which OFAC lists are screened, and which are not (with documented rationale for any exclusions)

- Update frequency: How often the lists are refreshed in the screening system, and who is responsible for verifying successful updates

- Match threshold documentation: What similarity score triggers a manual review, who approved that threshold, and when it was last reviewed

- False positive rate tracking: What percentage of alerts are cleared as false positives, whether that rate is trending up or down, and what threshold would trigger a threshold recalibration

- Escalation procedures: What happens when a genuine match is identified, including who notifies OFAC and on what timeline

- Training records: Evidence that staff who review screening alerts understand what they're looking for and how to document their decisions

- Testing logs: Records of periodic testing using known positive and negative test cases against your live screening configuration

The anti money laundering technology you use matters less than whether you can document defensible answers to all of the above. An aml risk assessment guide that ties each checklist item to a specific risk scenario in your customer portfolio is what separates a defensible program from one that looks good on paper until an examiner asks follow-up questions.

Community Banks vs. Fintechs: Different Risk Profiles, Same Core Requirements

BSA/AML compliance for community banks and AML compliance in fintech share the same regulatory foundation but differ significantly in risk profile and resource availability.

Community banks typically have lower transaction volumes, more stable customer bases, and longer-standing vendor relationships. Their OFAC screening risks tend to concentrate in wire transfers and correspondent banking relationships. A bsa aml compliance community banks program can reasonably operate with less sophisticated matching logic because the underlying population of customers and transactions is more homogeneous.

Fintechs process higher volumes with more diverse customer populations, often in cross-border contexts with higher inherent sanctions risk. A fintech handling international remittances needs a more sophisticated screening approach than a community bank handling local business accounts. Our sanctions screening automation guide for CISOs covers how the right technology stack differs significantly across these two institution types.

The Fintech BSA/AML Small Team Problem

A fintech BSA/AML small team running a compliance program with limited headcount needs to be deliberate about where human judgment adds value and where automation should take over. Manual review of every alert is not scalable when you're processing thousands of transactions per hour. The goal is to design the screening program so that human reviewers only see alerts that genuinely require judgment.

This means investing in AML compliance software that provides context alongside alerts: transaction history, customer risk score, geographic data, and behavioral patterns. An alert that shows "possible name match: 73% similarity" is not actionable. An alert that shows "73% name match, customer sent three wire transfers to this jurisdiction in the past 30 days, wire amount exceeds account average by 400%" gives a reviewer something concrete to evaluate. The difference between those two alert formats is the difference between a screening program that works and one that generates noise.

An alert that shows "possible name match: 73% similarity" is not actionable.

SAR Filing Best Practices After a Screening Hit

When an OFAC screening match survives manual review and is confirmed as a genuine or potential sanctions issue, the SAR filing process begins. This is where many institutions make additional errors, separate from the original OFAC screening mistakes that created the alert in the first place.

SAR filing efficiency depends on having a clear protocol before you need it. Compliance teams that treat each confirmed screening hit as a novel event waste time reconstructing procedures under pressure and risk filing errors or missed deadlines. A current suspicious activity report guide tailored to OFAC-related scenarios should be part of every institution's documented procedures, reviewed at least annually.

SAR Filing Requirements in 2026: What Changed

SAR filing requirements have evolved, with FinCEN's updated guidance placing increased emphasis on narrative quality rather than just checkbox completion. Examiners are looking for SARs that tell a coherent story: why the activity is suspicious, what investigation steps were taken, what the institution knows about the parties involved, and why the institution reached the conclusions it did.

The sar filing requirements 2026 standard expects institutions to include transactional detail that supports the narrative, not just the triggering transaction. The filing timeline remains 30 days from the decision to file, with a 60-day extension available if no subject is identified at the time of the decision.

CTR Filing Rules That Interact With OFAC Matches

CTR filing rules create an interaction with OFAC screening that compliance teams sometimes overlook. If a customer conducts cash transactions over $10,000 and also has a potential OFAC match, the CTR obligation doesn't pause while the OFAC review proceeds. Both processes run in parallel, which requires coordination between the AML transaction monitoring team and the sanctions screening team.

If a customer conducts cash transactions over $10,000 and also has a potential OFAC match, the CTR obligation doesn't pause while the OFAC review proceeds.

For institutions where these are separate functions, that coordination point is a documented gap that examiners will probe. SAR filing efficiency and CTR compliance are not independent workflows when the same customer triggers both obligations simultaneously.

Anti-Money Laundering Technology in 2026: What's Actually Different

Anti money laundering technology in 2026 is meaningfully different from what was available three years ago. The regulatory requirements haven't changed fundamentally, but the AI capabilities powering screening systems have improved in ways that matter practically. The difference shows up in three areas: name matching accuracy, continuous monitoring latency, and alert triage quality.

AML Compliance Software That Reduces False Positives

Modern AML compliance software uses machine learning to learn from the historical pattern of cleared false positives at your specific institution. If your customer base includes a high concentration of Vietnamese names and your screening program historically generates high false positive rates on certain SDN entries, an ML-based system adjusts its confidence scores accordingly over time.

This is categorically different from static fuzzy matching with a fixed threshold. The comparison between rule-based and AI-driven false positive reduction shows that AI-driven systems reduce manual review burden by 60-70% in production deployments without increasing false negative rates. That's the number that should move compliance team staffing decisions and technology procurement conversations.

How the EU AI Act Affects Financial Services Compliance

The EU AI Act classifies AI systems used for financial risk assessment as high-risk, which means institutions using AI-powered AML compliance software in EU jurisdictions need to meet documentation, transparency, and human oversight requirements for those systems. The eu ai act financial services requirements make it mandatory for EU-regulated entities to document how their AI screening models work, what data they were trained on, what their known failure modes are, and how human reviewers can override their outputs.

This is good compliance hygiene regardless of jurisdiction. But for compliance teams in EU-regulated financial services, it's a formal requirement that needs to be integrated into your AML compliance software procurement and model validation process now, not when the next examination cycle arrives and you're explaining why your AI screening vendor can't answer basic questions about their model.

- The honest answer is that most OFAC screening programs were designed for a different transaction environment.

- One of the most consistent OFAC screening mistakes is treating the Specially Designated Nationals (SDN) list as a static file rather than a live feed.

- Name matching is the technical core of OFAC screening, and it's where most programs have the weakest documentation.

- KYC automation changes the OFAC screening equation in two important ways.

- A proper BSA/AML compliance checklist for OFAC screening isn't long, but every item on it needs documentation that survives an examination.

Onboard Customers in Seconds

Conclusion

OFAC screening mistakes don't happen because compliance teams are careless. They happen because screening programs are built for yesterday's transaction volumes, name matching logic isn't calibrated for the institution's actual customer population, and the gap between when lists update and when systems refresh is treated as acceptable risk until an examiner documents it as a deficiency. AML compliance in 2026 requires treating your screening program as a live system that needs ongoing calibration, documentation, and testing, not a checkbox reviewed once a year.

The most concrete steps you can take right now: audit your sanctions list coverage and update frequency, review your matching threshold documentation against your current false positive rate, and evaluate whether your current AML compliance software gives reviewers enough context to make good decisions quickly. If you're running a fintech BSA/AML small team, automation isn't optional at scale. Start with our comparison of manual compliance vs. AI automation to identify where the highest-value improvements are in your specific program. OFAC screening mistakes are preventable with the right combination of technology, documented process, and calibrated human oversight.

Share this article