.webp)

Listen To Our Podcast🎧

Travel rule compliance crypto is one of the most operationally demanding obligations in financial regulation today. If your institution handles virtual asset transfers, wires, or cross-border payments on behalf of customers, you are almost certainly subject to rules requiring you to collect, verify, and transmit originator and beneficiary data alongside every transaction. Getting this wrong carries real regulatory consequences, and enforcement posture from agencies like FinCEN, the FCA, and MAS has tightened considerably since 2023. This guide covers what the Travel Rule actually requires, how it intersects with your existing AML compliance program, and what practical steps banks, fintechs, and virtual asset service providers need to take before the next examination cycle.

What Is the Travel Rule and Why Does It Apply to Crypto?

The Travel Rule gets its name from the way financial data must travel alongside a transaction. Originally codified in the United States under 31 CFR 103.33 as part of the Bank Secrecy Act, the rule required banks to pass identifying information about wire transfer originators to receiving institutions. FATF expanded this concept globally with Recommendation 16, which extends the same obligation to virtual asset transfers and places compliance responsibility squarely on virtual asset service providers.

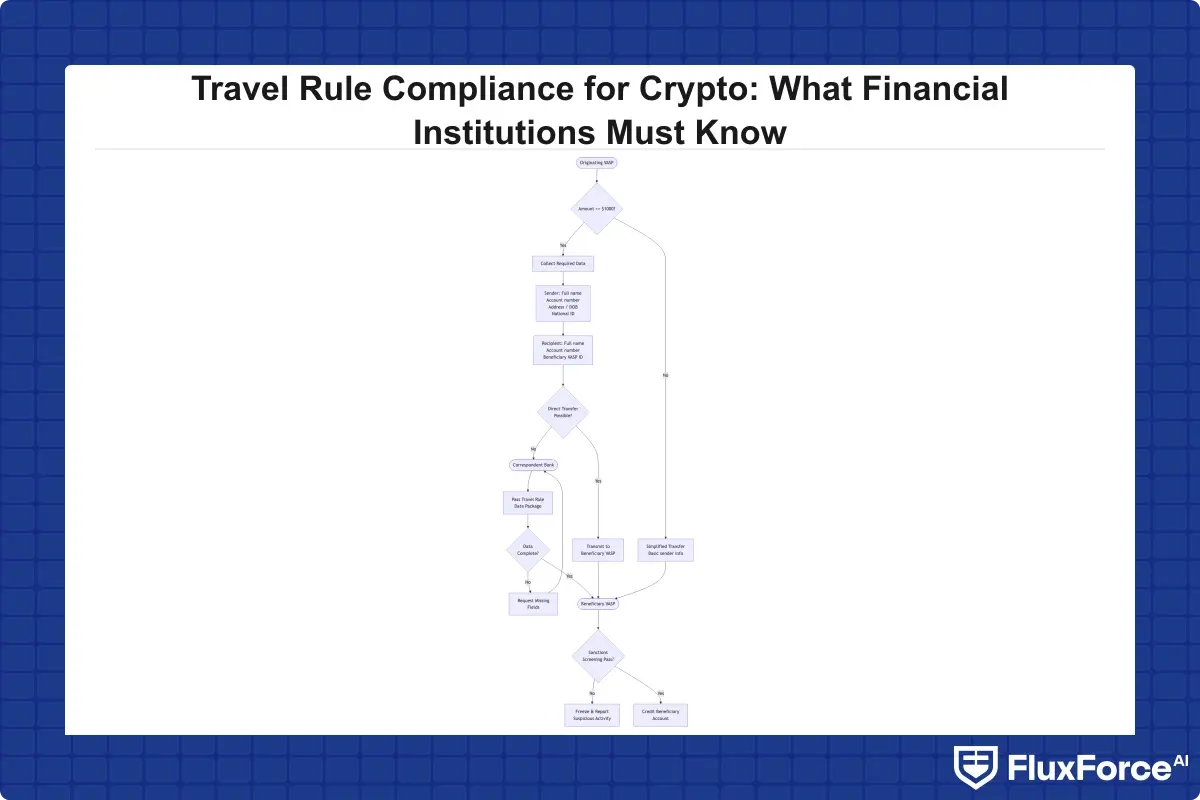

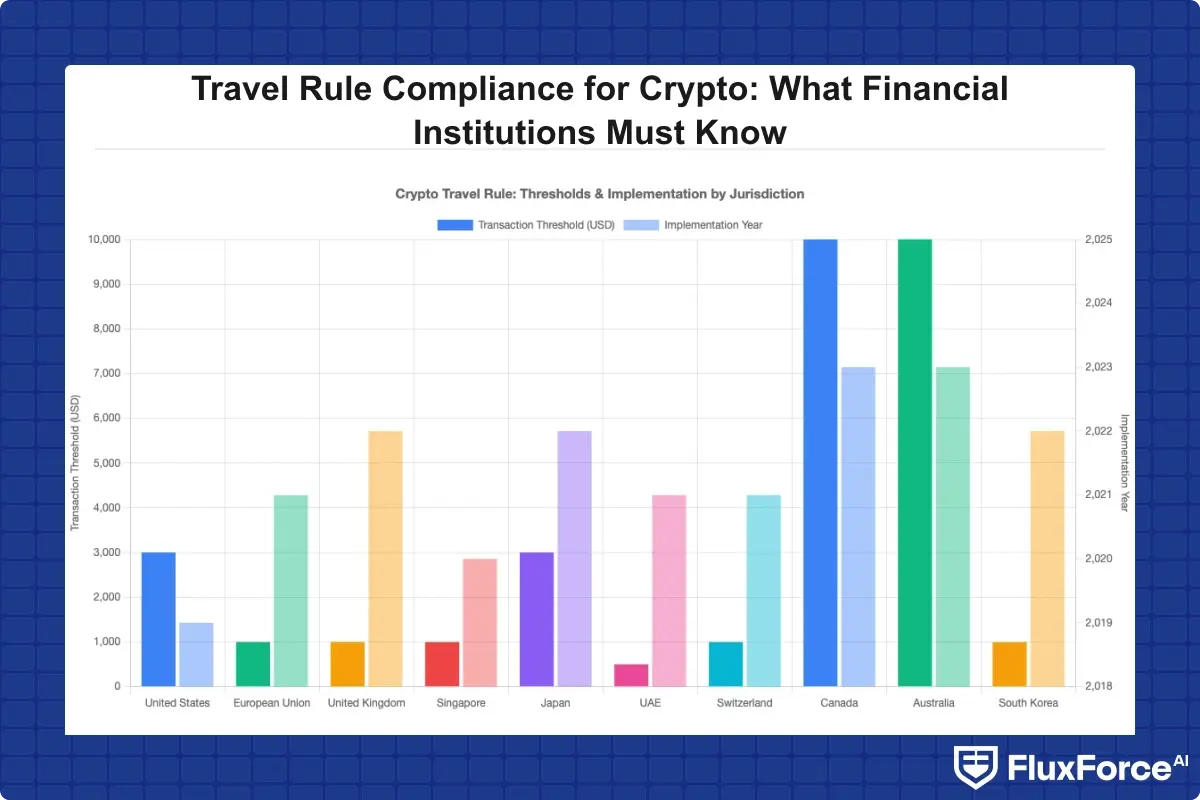

The core requirement: when a virtual asset transfer exceeds the applicable threshold (USD 1,000 in the US, EUR 1,000 in the EU under AMLD6), the originating VASP must collect and transmit originator and beneficiary data to the receiving VASP in real time, before or simultaneously with the transaction.

The FATF Recommendation 16 Framework

FATF's Recommendation 16 applies the same logic as traditional wire transfer rules to crypto transactions. Originating VASPs must obtain and hold originator information and transmit it to receiving VASPs. The receiving VASP must then verify the beneficiary information before crediting the account. Key originator data required includes full legal name, account number or wallet address, and a physical address, national identity number, or date and place of birth. This sounds straightforward on paper. In practice, most compliance teams discover the implementation gaps only after they attempt to build the process.

Which Entities Must Comply with the Travel Rule?

Any entity qualifying as a VASP under FATF guidance must comply, and that definition is broader than many institutions expect. It covers crypto exchanges, custodial wallet providers, DeFi platforms with centralized governance, and traditional banks that offer crypto custody or trading services. Financial institutions that process wire transfers involving VASPs are also affected, even if they do not offer crypto products directly. If your bank runs the rails for a crypto exchange's customer payouts, you have Travel Rule exposure.

How Travel Rule Compliance Crypto Works in Practice

Travel rule compliance crypto implementation is messier than the regulation implies. FATF guidance assumes that both originating and receiving institutions have compatible technical systems and have agreed on a data transmission protocol. Neither assumption holds universally in today's fragmented market, where hundreds of VASPs operate across dozens of jurisdictions with different implementation timelines.

Data Fields Required for Travel Rule Transfers

The minimum data set for travel rule compliance varies by jurisdiction, but the fields required across major regimes are consistent enough to plan around. The table below shows the core requirements:

| Data Field | Required By |

|---|---|

| Originator full legal name | US (FinCEN), EU (AMLD6), FATF Rec. 16 |

| Originator account or wallet address | All major jurisdictions |

| Originator physical address or date of birth | US, EU, Singapore MAS |

| Beneficiary full legal name | All major jurisdictions |

| Beneficiary account or wallet address | All major jurisdictions |

The practical challenge is that crypto wallet addresses are pseudonymous by design. Confirming that a wallet address belongs to a specific individual requires additional KYC steps, which is where kyc automation becomes operationally significant. Institutions still running manual KYC processes face a volume problem: crypto transactions settle in seconds, and manual identity checks cannot keep pace with that throughput.

The Sunrise Problem and Cross-Border Gaps

The "sunrise problem" describes a situation where two VASPs operate in jurisdictions with different Travel Rule implementation timelines. If your institution is fully compliant but the counterparty VASP is in a jurisdiction that has not yet enacted the rule, you cannot transmit to a non-compliant receiver and cannot verify what you receive from them. This creates a compliance catch-22 that no amount of internal policy can fully resolve.

Most compliance programs address this by applying risk-based controls to counterparty VASPs, treating unverified counterparties as higher risk and applying enhanced due diligence accordingly. Your aml risk assessment guide should address VASP counterparty risk as a distinct risk category, separate from standard customer risk ratings, with defined escalation thresholds for unverified counterparties.

AML Compliance Requirements for Crypto-Active Financial Institutions

AML compliance for institutions that touch crypto is more complex than for pure fiat-only institutions, because crypto introduces transaction monitoring challenges that traditional anti money laundering technology was not designed to handle. On-chain activity is public but pseudonymous, transaction speeds are measured in seconds rather than days, and the counterparty landscape includes thousands of VASPs with widely varying compliance standards.

AML Risk Assessment Guide for Virtual Asset Providers

A proper aml risk assessment guide for crypto-active institutions must address at least five dimensions. Counterparty risk covers whether the VASP you are transacting with is licensed and compliant in its home jurisdiction. Transaction pattern risk asks whether on-chain activity shows layering behavior, rapid consolidation, or mixing service exposure. Geographic risk addresses whether the wallet or counterparty has exposure to sanctioned jurisdictions or high-risk countries. Product risk covers whether you offer privacy coin conversions, DeFi integrations, or self-custody options. Customer risk asks whether the customer's crypto activity has changed materially from the profile established at onboarding.

For community banks with limited staff, a bsa aml compliance checklist adapted for crypto exposure is a practical starting point. At minimum, it should include a VASP due diligence questionnaire, a blockchain analytics integration requirement, and a defined escalation process for transactions flagged by on-chain monitoring. Institutions that have already built AML screening into policy issuance workflows can reuse much of that structure for crypto customer onboarding.

Anti Money Laundering Technology 2026 in Crypto Monitoring

Anti money laundering technology 2026 is increasingly blockchain-native. Providers now offer real-time on-chain monitoring that tracks fund flows across wallets and flags exposures to darknet markets, sanctioned addresses, and known mixing services. This capability is no longer optional for any institution with significant crypto transaction volume. The practical minimum stack for 2026 includes a blockchain analytics provider for on-chain monitoring, a Travel Rule solution for compliant data transmission, and an integrated aml compliance software platform that connects transaction alerts to your case management and sar filing workflows.

Institutions building this capability should consider regulatory compliance automation platforms that integrate blockchain analytics, Travel Rule messaging, and AML case management into a single workflow, rather than stitching together three separate point solutions that require manual data transfer between them.

BSA/AML Compliance Checklist for Crypto Asset Transactions

Building a bsa aml compliance checklist for crypto requires more than adapting your existing wire transfer checklist. The asset class introduces unique data, counterparty, and monitoring requirements that standard BSA checklists were never designed to address. If your current checklist does not mention wallet addresses, blockchain analytics, or VASP due diligence, it needs a significant update.

BSA AML Compliance for Community Banks with Crypto Exposure

Bsa aml compliance community banks face a particular challenge: they often have modest compliance teams and limited technology budgets, but their customers are increasingly using crypto platforms. If a customer's checking account receives large, recurring deposits from a crypto exchange, the bank is responsible for assessing that activity under BSA/AML rules even if it does not offer crypto services itself. The source of funds is a compliance matter regardless of which asset class generated them.

The minimum checklist for community banks handling crypto-adjacent activity should include: adding crypto-related transaction patterns to the customer risk rating model, identifying customers who are VASPs or high-frequency crypto users and applying enhanced monitoring, updating transaction monitoring scenarios to catch ACH and wire patterns consistent with crypto exchange settlements, establishing a VASP due diligence process for any direct banking relationships with exchanges, and training the BSA officer on blockchain analytics basics so they can interpret flagged transaction reports without needing to outsource every review.

Fintech BSA AML Requirements for Small Teams

Fintech bsa aml small team programs tend to be lean by design, and that creates a specific vulnerability. A five-person compliance team serving 200,000 users cannot manually review every transaction alert. This makes fintech BSA/AML programs disproportionately dependent on automation quality. The risk is that automated systems generate too many false positives, overwhelming the small team and creating alert fatigue that eventually causes real suspicious activity to be missed.

The solution is not aggressive hiring but investment in aml compliance software that reduces the alert queue through smarter prioritization. How Agentic AI Fraud Agents Cut False Positives by 80% covers the same AI prioritization logic that applies directly to AML alert management. Institutions that have implemented AI-assisted triage report similar reduction rates in AML alert volumes, freeing small teams to focus on the cases that actually warrant human review.

KYC Automation and CDD Requirements in 2026

KYC automation is not optional for crypto-active institutions at meaningful transaction scale. The volume and speed of crypto transactions make manual KYC processes unworkable. An institution processing thousands of crypto-related account openings or transfers per day needs automated identity verification, continuous monitoring, and triggered review workflows that operate without analyst intervention for routine cases.

KYC CDD Requirements Banks Must Apply to Crypto Customers

Kyc cdd requirements banks must follow under FinCEN's Customer Due Diligence rule apply equally to crypto customers. This means collecting and verifying the identity of beneficial owners of any legal entity opening an account, and understanding the nature and purpose of the customer relationship at onboarding.

For crypto customers, this baseline must extend to include the source of funds for crypto holdings, the customer's on-chain activity profile obtained through blockchain analytics, any VASP affiliations (is the customer operating as an unregistered money transmitter?), and periodic refresh cycles that are shorter than for traditional customers. Crypto markets move fast, and a customer's risk profile can change materially within weeks.

Kyc automation 2026 tools can run continuous monitoring against on-chain activity, automatically trigger enhanced due diligence when a customer's wallet shows new exposure to high-risk counterparties, and feed alerts directly into case management without manual intervention. This closes the gap between the speed of crypto transactions and the pace of traditional compliance review cycles.

Enhanced Due Diligence Guide for High-Risk Crypto Wallets

An enhanced due diligence guide for crypto customers should address three specific scenarios. First, wallets receiving funds from known mixing services require immediate escalation, a blockchain analytics report documenting the exposure, and a customer explanation request. Second, wallets with significant exposure to sanctioned jurisdictions require a sanctions screening review and legal counsel involvement before any decision to continue the relationship. Third, wallets showing rapid consolidation patterns consistent with layering require a pattern documentation review and senior compliance officer sign-off.

For each scenario, EDD documentation should include the blockchain analytics report, the customer's written explanation, the reviewing officer's rationale, and the final disposition decision. If the explanation does not resolve the concern, sar filing requirements apply regardless of whether the customer is cooperative or the amounts seem modest.

SAR Filing Requirements and Best Practices for Crypto Activity

SAR filing is where many crypto compliance programs show their weakest execution. Suspicious activity report guidance published by FinCEN provides a general framework, but crypto-specific SAR filing raises questions that standard guidance does not address clearly, particularly around how to document blockchain-specific evidence in a way that is useful to law enforcement.

SAR Filing Best Practices for Suspicious Crypto Transactions

Sar filing best practices for crypto include several conventions that differ from traditional SAR filings. Include wallet addresses involved in the subject field. Include blockchain transaction hashes where available, as these allow law enforcement to independently verify the on-chain activity. Specify the blockchain network explicitly (Bitcoin, Ethereum, and so on, rather than just "cryptocurrency"). Note whether blockchain analytics tools were used and which specific flags they raised. Document the counterparty VASP if known and whether it is a licensed and regulated entity in its home jurisdiction.

Sar filing efficiency matters because filing volumes are growing rapidly. FinCEN received over 3.6 million SAR filings in 2023, and the crypto-related share is increasing year over year. Institutions investing in aml compliance software with integrated SAR drafting tools can reduce the time from alert to filed SAR significantly, sometimes from several hours to under thirty minutes for straightforward cases. The suspicious activity report guide for your institution should be updated annually to reflect current FinCEN expectations for crypto SAR narratives and the format for documenting blockchain evidence.

SAR Filing Requirements 2026: What's Changed

Sar filing requirements 2026 bring two significant changes for crypto-active institutions. First, FinCEN's beneficial ownership reporting requirements under the Corporate Transparency Act intersect with SAR obligations, because newly registered beneficial owners may trigger suspicious activity flags if they appear on adverse media or sanctions lists during the verification process. Second, the EU's Transfer of Funds Regulation, which implements the Travel Rule in Europe, creates new SAR-triggering scenarios when Travel Rule data cannot be verified during a cross-border VASP transfer.

Institutions subject to both US and EU rules face the highest operational burden, because ctr filing rules and SAR thresholds differ across jurisdictions, and the data formats required by FinCEN and EU national competent authorities are not identical. The regulatory compliance reporting frameworks built for multi-jurisdictional payments risk environments apply directly to this challenge and provide a workable model for institutions that need to manage diverging requirements simultaneously.

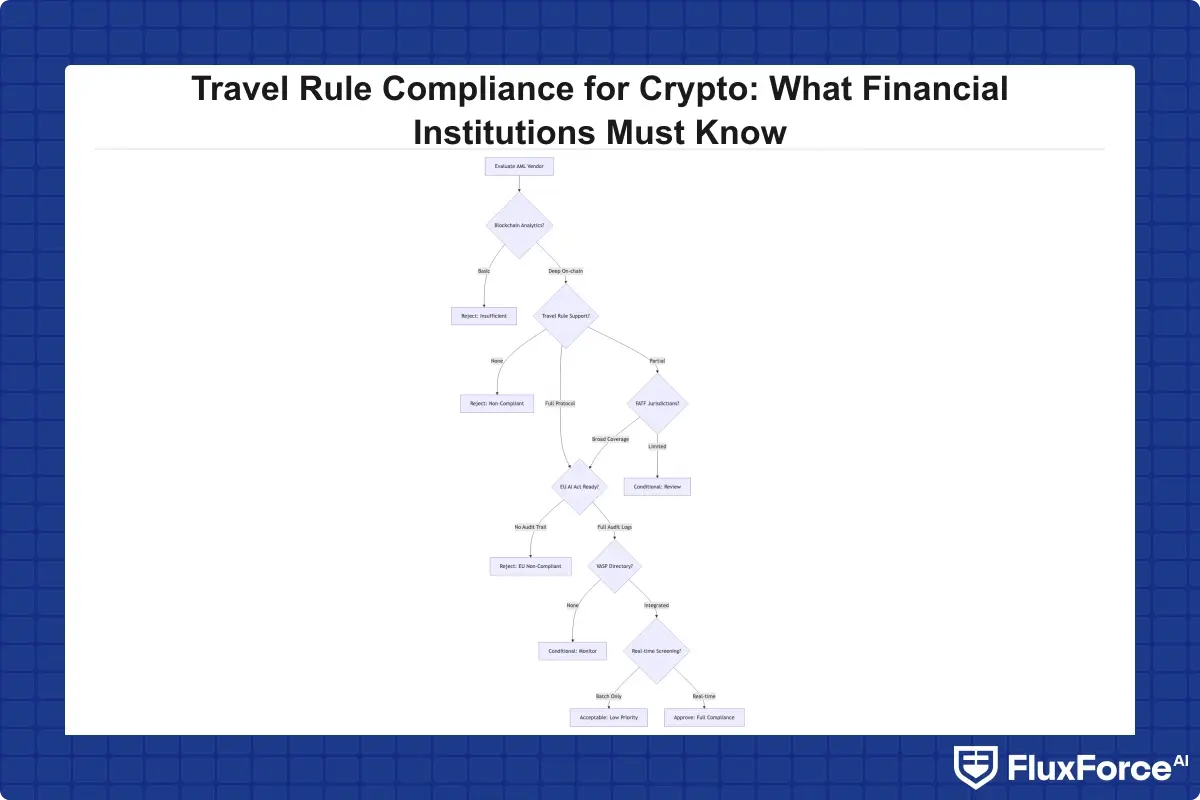

AML Compliance Software: What to Look for in 2026

AML compliance software for crypto-active institutions in 2026 needs to do more than flag transactions. The baseline features of transaction monitoring, watchlist screening, and case management are table stakes. The differentiators are blockchain analytics integration depth, Travel Rule messaging protocol support, AI-assisted alert prioritization with documented model logic, and audit trail quality that satisfies both FinCEN examiners and EU AI Act requirements.

EU AI Act Financial Services Implications for AML Tools

The EU AI Act financial services provisions that became enforceable in 2024 classify AML transaction monitoring systems as high-risk AI applications. This has direct implications for institutions using AI-driven aml compliance software: they must maintain documentation of the model's decision logic, be able to explain flagging decisions to regulators on request, and conduct regular model validation reviews with documented outcomes.

This is not a reason to avoid AI-powered AML tools. It is a reason to choose vendors who have built EU AI Act compliance into their product documentation from the start, rather than retrofitting it. The GDPR compliance automation approaches that insurers use for regulatory documentation provide a close structural parallel for what AML software vendors now need to demonstrate under EU AI Act audit requirements.

Evaluating AML Compliance Fintech Solutions

When evaluating aml compliance fintech solutions for crypto-specific use cases, the criteria should include blockchain analytics depth (does the tool provide counterparty exposure analysis at the individual transaction level, or only wallet-level flags?), Travel Rule protocol coverage (does it support TRISA, OpenVASP, Sygna, and Notabene?), SAR automation capability, demonstrated false positive rate benchmarks, and audit trail completeness.

A practical benchmark for alert-to-SAR conversion rate is under 2%. Most legacy systems run at 5-10%, meaning the vast majority of analyst time goes to alerts that never result in filings. Anti money laundering technology 2026 vendors that can demonstrate conversion rates under 2% in comparable institutions offer a materially different operational value proposition. For institutions already running sanctions screening programs, the sanctions screening automation evaluation framework provides a solid model for assessing how well a new AML tool will integrate with existing workflows.

Onboard Customers in Seconds

Conclusion

Travel rule compliance crypto is not a standalone project. It sits inside a broader AML compliance architecture that includes transaction monitoring, kyc automation, sar filing, and risk assessment, and each of those components needs to be adapted for the specific characteristics of virtual assets. Institutions that treat crypto compliance as a bolt-on to their existing wire transfer program will consistently find themselves behind the regulatory expectation curve.

The institutions handling this well in 2026 are not necessarily the ones with the largest compliance teams. They are the ones that have invested in aml compliance software designed for crypto-era transaction volumes, integrated blockchain analytics into their existing monitoring workflows, and built sar filing processes capable of handling increasing volumes without proportional headcount growth. The technology is available, the regulatory expectations are clear, and the enforcement activity is real. A concrete implementation plan, not a waiting posture, is what this moment requires.

Share this article