.webp)

Listen To Our Podcast🎧

Regulatory change management compliance is now a moving target that few teams feel they have under control. Rules shift across jurisdictions, deadlines arrive without warning, and the cost of falling behind shows up as fines, failed audits, and reputational damage. For banks, fintechs, insurers, and supply chain operators, the question is no longer whether regulations will change but how fast your team can absorb each change without breaking operations. This guide lays out a practical approach to staying ahead, covering how to track new rules, build an aml risk assessment guide into daily work, and use automation to turn reactive scrambling into a predictable process.

What Is Regulatory Change Management Compliance?

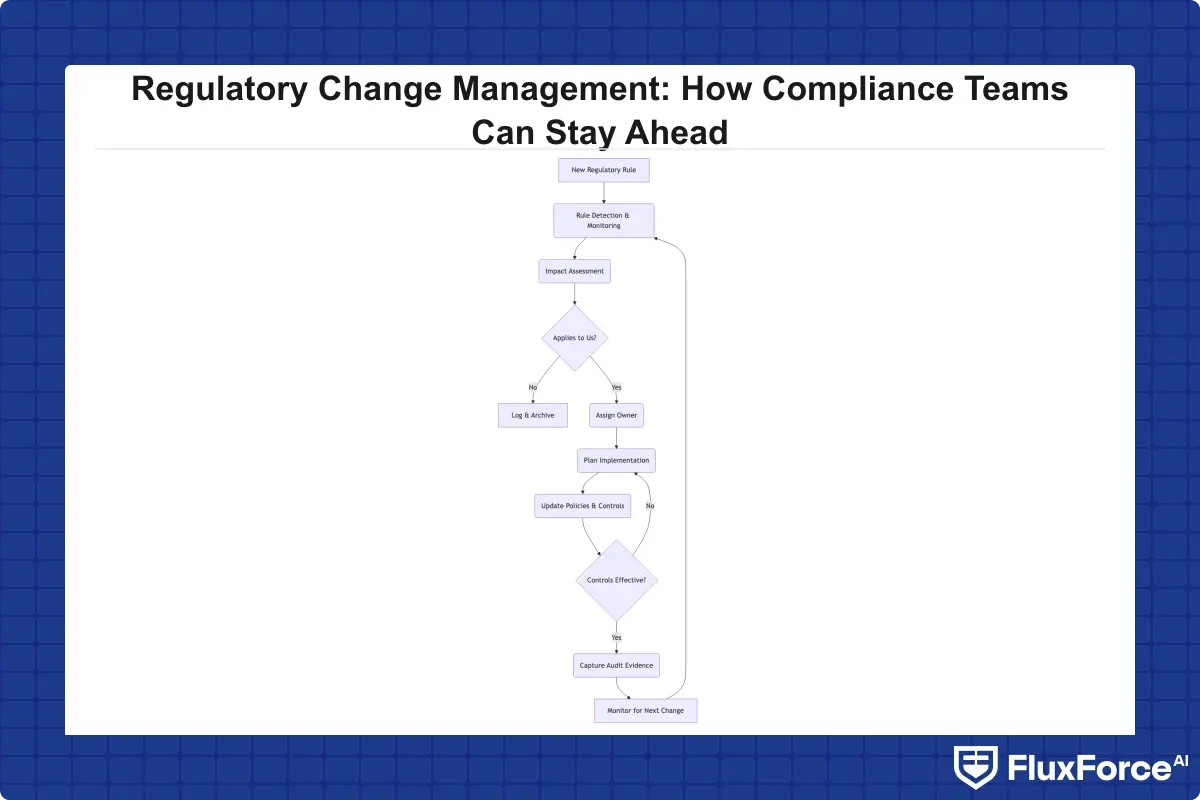

Regulatory change management compliance is the structured process of identifying, assessing, and implementing new or amended regulations before they create exposure. It connects rule-tracking, impact analysis, and operational rollout into one repeatable workflow.

Most teams handle change reactively. A regulator publishes an update, someone forwards a PDF, and a frantic interpretation effort begins. The teams that stay ahead treat regulatory monitoring as a continuous function, not an emergency response.

Why reactive compliance fails

When a rule lands and you start from scratch, you lose the two things that matter most: time and context. A 2023 study from Thomson Reuters found that compliance professionals spend a growing share of their week tracking regulatory developments, with many citing the volume of change as their top concern. Manual review delays mean changes get implemented late, partially, or inconsistently across business units.

The core components of a change workflow

A working program has four parts: a monitoring layer that captures new rules, an assessment layer that scores impact, an implementation layer that assigns owners and deadlines, and an evidence layer that records what you did. Skip any one and audits become guesswork.

Who owns regulatory change in your organization

Ownership is the quiet failure point. In small fintech teams, one compliance officer often carries the whole load, while in banks the work spreads across legal, risk, and operations. Either way, you need a named owner per change, not a shared inbox where accountability evaporates.

How Can Compliance Teams Stay Ahead of Regulatory Change?

Staying ahead means shortening the gap between when a rule changes and when your controls reflect it. The fastest teams combine continuous monitoring, pre-built response playbooks, and aml compliance software that flags affected processes automatically.

Build a continuous monitoring habit

Set up structured feeds from primary sources rather than relying on secondhand summaries. For US institutions, that means the Financial Crimes Enforcement Network for BSA updates and federal banking regulators for examination guidance. For European operations, watch for developments tied to the eu ai act financial services provisions, which will reshape how automated decisioning is governed.

Map every rule to a control

A rule you cannot trace to a specific control is a rule you cannot prove you follow. Maintain a living matrix that links each regulatory requirement to the policy, system, and report that satisfies it. When something changes, you instantly see the blast radius. This same discipline underpins solid regulatory compliance reporting in banking, where traceability decides whether an exam goes smoothly.

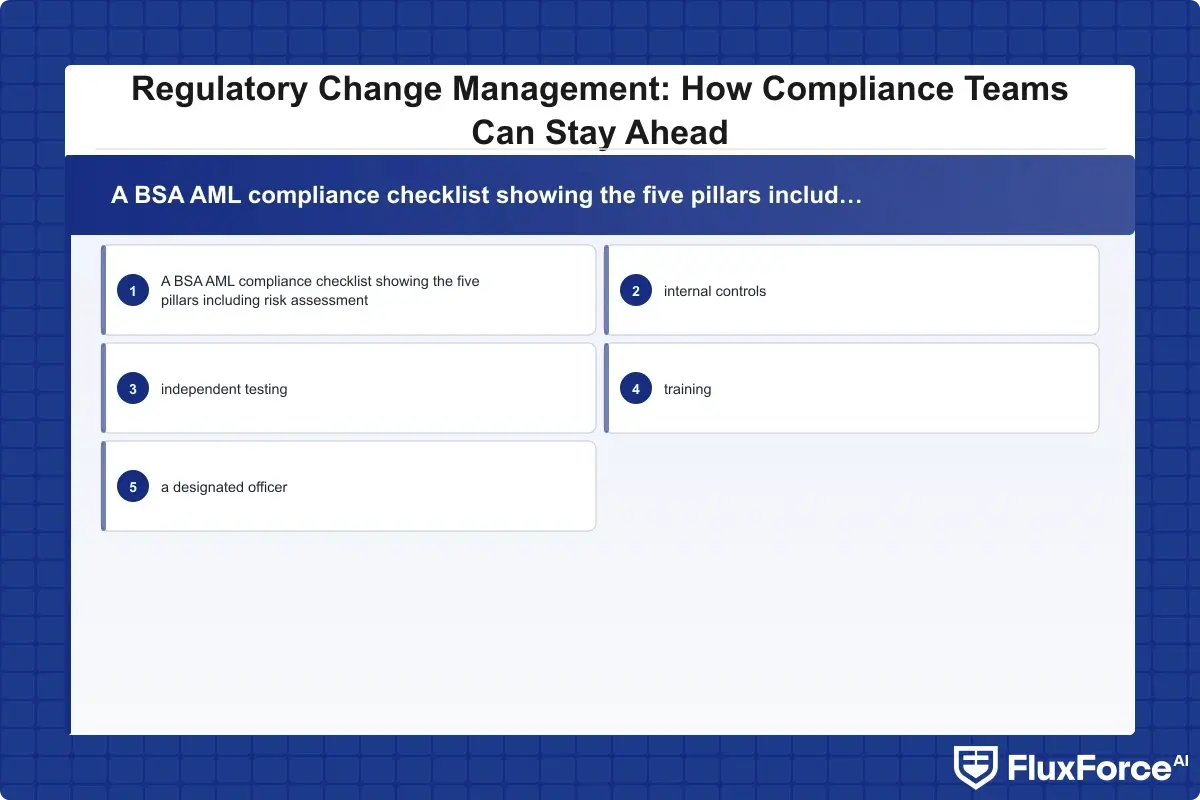

Use a bsa aml compliance checklist as a baseline

A standing bsa aml compliance checklist gives you a stable reference point so each new rule becomes an edit rather than a rebuild. For bsa aml compliance community banks especially, a documented checklist keeps a lean team aligned without depending on one person's memory.

Strengthening AML Compliance Across Fintech and Banking

Strong aml compliance is the backbone of regulatory change management compliance, because most high-stakes updates touch how you detect, investigate, and report financial crime. Getting this layer right makes every future change easier to absorb.

AML compliance fintech challenges for small teams

The fintech bsa aml small team problem is real: limited headcount, fast transaction growth, and the same regulatory expectations as a large bank. aml compliance fintech programs succeed when they automate the repetitive work, screening, alerting, and case documentation, so analysts spend their time on judgment calls. We have seen teams cut alert triage time roughly in half by routing low-risk alerts through automated rules first.

Choosing aml compliance software that adapts

The right aml compliance software does not just detect suspicious activity, it adapts when rules change without a six-month vendor project. Look for configurable risk rules, audit-ready logging, and clear model explainability. Embedding regulatory compliance automation into the monitoring stack lets teams update detection logic as guidance shifts, which matters as anti money laundering technology 2026 expectations push toward continuous monitoring over periodic batch reviews.

Reducing false positives without missing risk

False positives drain analyst time and bury genuine threats. Modern anti money laundering technology uses behavioral scoring and entity resolution to cut noise, an approach explored in our look at reducing false positives with AI-driven solutions. The honest tradeoff: tuning too aggressively can suppress real alerts, so every threshold change needs documented testing.

SAR Filing and CTR Requirements That Keep Changing

Reporting obligations are where regulatory change hits hardest, because errors are visible and timelines are strict. Building sar filing efficiency into your workflow protects the team when requirements shift.

SAR filing best practices and the 2026 outlook

Good sar filing best practices start with clean case narratives, complete supporting data, and a documented decision trail. Following a clear suspicious activity report guide helps analysts write filings that survive examiner scrutiny. As sar filing requirements 2026 evolve toward more structured data submission, teams that already capture standardized fields will adapt faster than those relying on free-text notes.

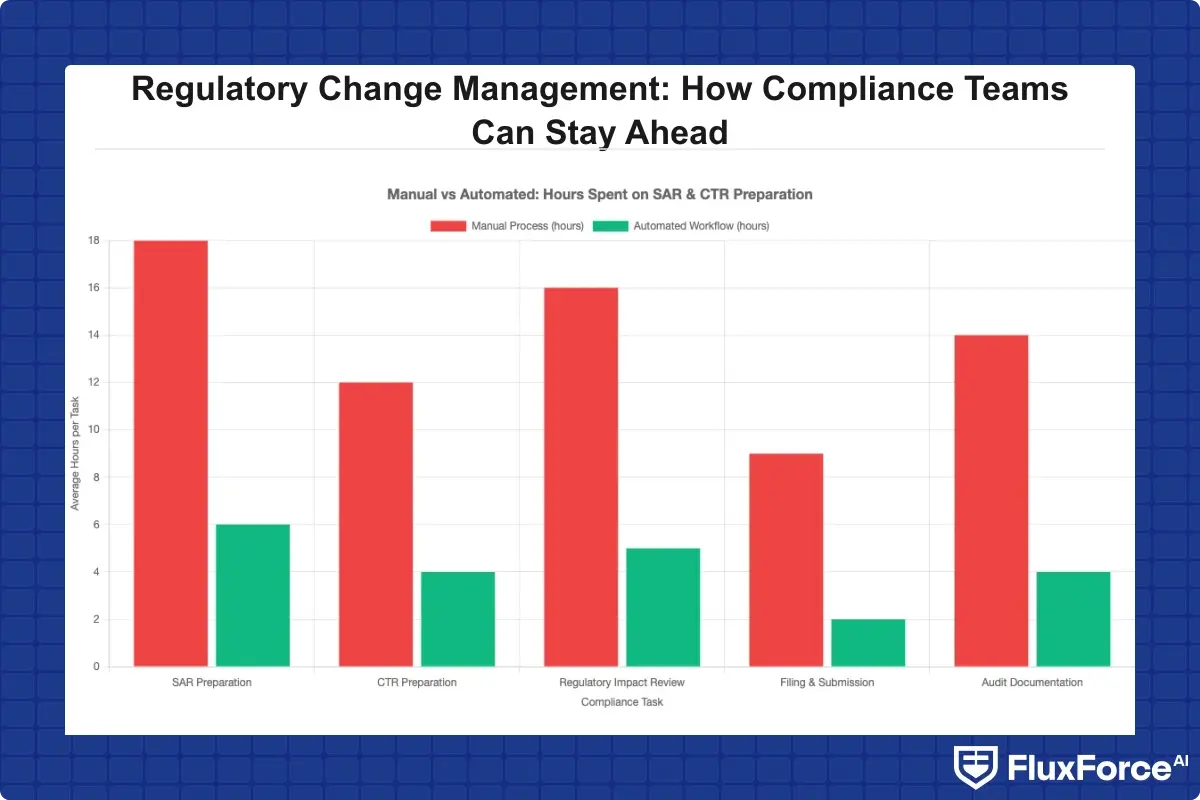

Improving sar filing efficiency with automation

Manual SAR preparation can take hours per case. kyc automation and case management tools that pre-fill fields from existing customer data improve sar filing efficiency dramatically, sometimes cutting preparation time by 60 percent. The key is keeping a human reviewer on the final decision, since automation should accelerate the work, not replace judgment.

CTR filing rules and aggregation traps

ctr filing rules require reporting cash transactions over the threshold, but the aggregation logic, multiple transactions, related accounts, same-day activity, is where teams slip. Automated aggregation that monitors across accounts catches the patterns a manual reviewer misses on a busy day.

KYC, CDD, and Enhanced Due Diligence in 2026

Customer due diligence sits at the front line of regulatory change management compliance, because onboarding is where most risk enters the system. Strong kyc cdd requirements banks must meet keep changing as identity fraud grows more sophisticated.

KYC automation 2026 and what changes

kyc automation reduces onboarding friction while improving accuracy, and kyc automation 2026 expectations lean toward continuous verification rather than one-time checks at account opening. Tying KYC into ongoing monitoring is covered well in our piece on continuous user verification with zero trust. Real-time identity signals matter especially as synthetic identity fraud becomes harder to spot at the door.

Meeting kyc cdd requirements banks face

The kyc cdd requirements banks operate under demand risk-rated customer profiles, beneficial ownership identification, and ongoing transaction monitoring. Documenting how you meet each requirement, and updating that documentation when rules change, is what separates a clean exam from a finding.

When to apply an enhanced due diligence guide

An enhanced due diligence guide kicks in for higher-risk customers: politically exposed persons, complex ownership structures, and high-risk jurisdictions. EDD is not about more paperwork, it is about proportionate scrutiny, with documented reasoning for why a customer received extra review.

Building a Future-Proof Compliance Operating Model

A durable program treats regulatory change management compliance as infrastructure, not a project. The goal is a model that absorbs change with minimal disruption.

Automate the repeatable, escalate the judgment

The winning split is simple: automate data gathering, screening, and routine filings, then escalate genuine ambiguity to experienced people. This is the same logic behind rolling out compliance agents in 90 days, where automation handles volume and humans handle nuance.

Keep an aml risk assessment guide current

Your aml risk assessment guide should be reviewed at least annually and after any material regulatory change. A stale risk assessment is one of the most common examiner findings, and it undermines every control built on top of it.

Measure what actually matters

Track cycle time from rule publication to control implementation, percentage of changes with assigned owners, and audit findings per cycle. These metrics tell you whether your program is genuinely staying ahead or just looking busy.

Onboard Customers in Seconds

Conclusion

Regulatory change management compliance rewards teams that build a steady process instead of reacting to each new rule in a panic. By combining continuous monitoring, a maintained bsa aml compliance checklist, strong aml compliance software, and disciplined sar filing and kyc automation, even a small team can keep pace with anti money laundering technology 2026 expectations. The teams that win treat change as routine: every new rule maps to a control, every control has an owner, and every action leaves an audit trail. Start by auditing your current change workflow against the four components in this guide, then automate the repetitive work so your experts can focus on the decisions only people should make. Talk to our team about putting a future-proof compliance model in place before the next rule lands.

Share this article