.webp)

Listen To Our Podcast🎧

Insurance claims fraud detection AI is changing how insurers and financial institutions fight back against a problem costing the industry hundreds of billions annually. The old approach, manual review queues, static rule engines, and reactive investigation teams, was never designed for modern fraud speeds. This post covers how AI detection works, why false positives drain more resources than most teams track, and what to evaluate when choosing platforms.

The True Cost of Insurance Fraud

According to the FBI, non-health insurance fraud costs the U.S. over $40 billion annually, adding $400 to $700 to average household premiums. When health insurance fraud is included, industry-wide losses exceed $300 billion. Even modest detection improvements produce measurable bottom-line impact.

The harder challenge is not detecting fraud after the fact. It is catching it before payment clears, without flagging thousands of legitimate claims in the process.

What the Numbers Actually Tell Us

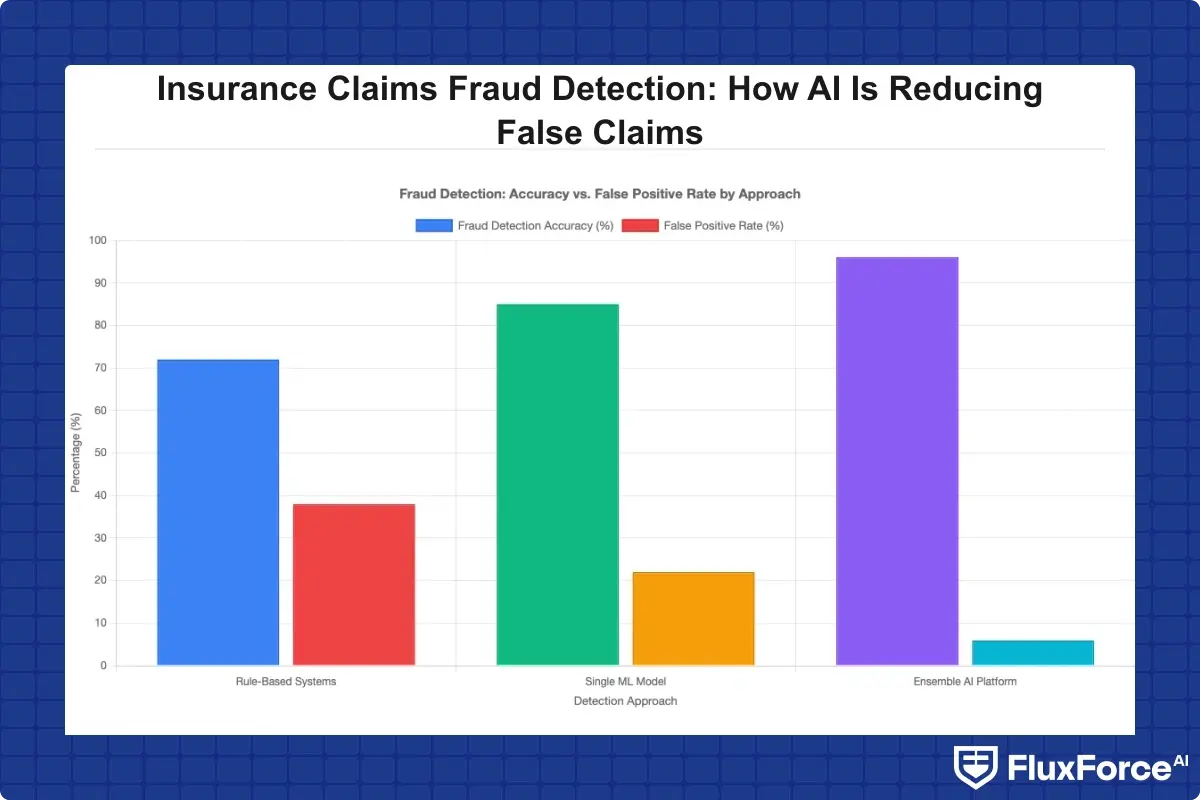

The false positive rate in fraud detection at traditional insurers typically runs 70-90%. For every 10 alerts generated, 7 to 9 belong to legitimate claims incorrectly flagged. Each manual review costs $25-75 in analyst time. At 1,000 weekly reviews with an 80% false positive rate, teams spend $40,000 per week confirming legitimate claims are legitimate. That is the false positive cost fraud calculation most operations teams have never actually done.

Why Traditional Detection Methods Are Falling Short

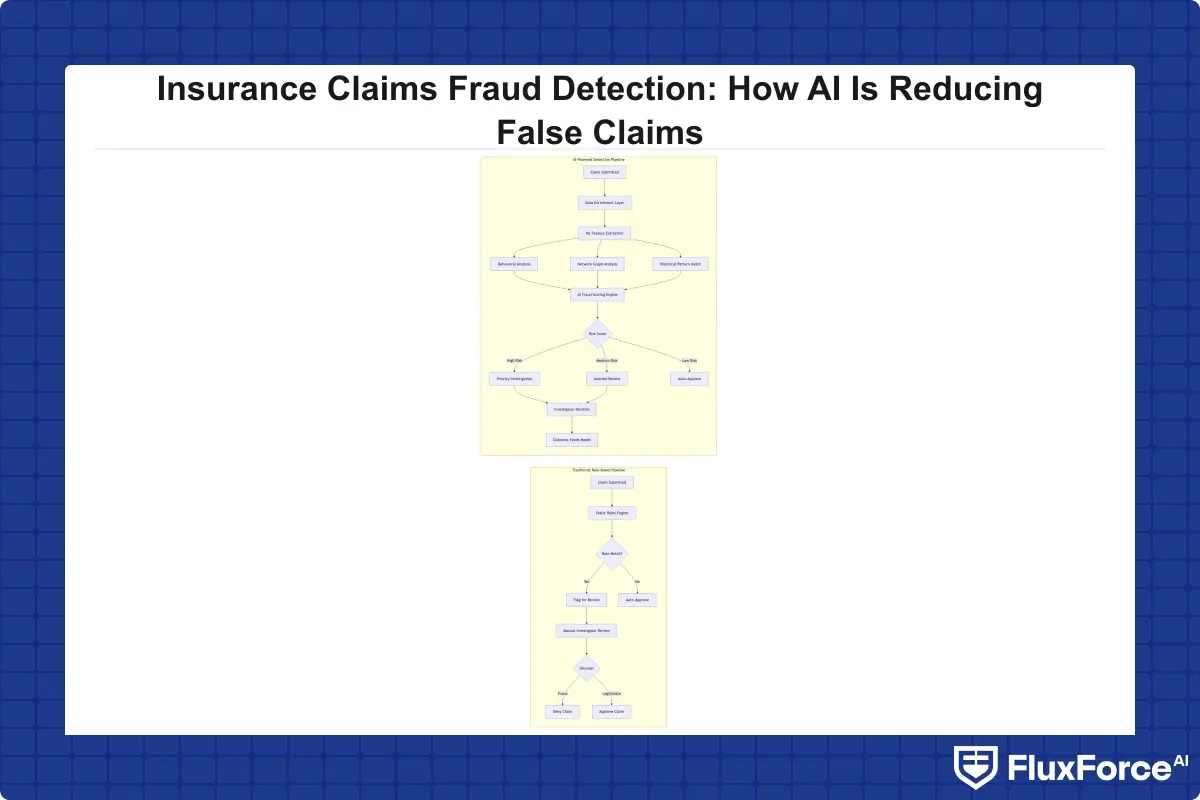

Rule-based systems check claims against fixed conditions: amount thresholds, policy age limits, specific diagnosis codes that historically correlate with fraud. These rules are auditable but age badly. Fraudsters learn the thresholds and stay under them. Organized rings rotate providers and billing codes. Static rules keep catching the same old patterns while newer schemes pass through undetected. Most insurers today run a hybrid of AI scoring layered on legacy rules, which often produces worse outcomes than either approach alone because the two systems can contradict each other on which alerts to prioritize.

How Does Insurance Claims Fraud Detection AI Work?

Insurance claims fraud detection AI analyzes each claim against thousands of contextual signals simultaneously, not just the handful of variables a static rule checks. The system learns from both confirmed fraud cases and legitimate claims, continuously updating its model of what normal looks like across different claim types, regions, and customer profiles.

The AI Detection Process in Four Stages

How does AI detect fraud in insurance claims? The process runs through four stages:

- Data ingestion: Pulls structured data (claim amounts, dates, provider IDs, policy history) and unstructured data (adjuster notes, medical records, images) into a unified feature set.

- Anomaly scoring: Each claim receives a fraud probability score based on its deviation from expected patterns for similar claims.

- Network analysis: Maps relationships between claimants, providers, attorneys, and witnesses to flag organized fraud rings that single-claim review would never surface.

- Decision support: High-scoring claims route to investigators with the specific signals that drove the score, not just a risk number.

The most important architectural choice is whether the platform evaluates claims individually or in a network context. Individual scoring catches single-actor fraud. Network analysis catches organized rings, which account for a disproportionate share of total fraud losses. Both are necessary for complete coverage.

Machine Learning Models That Power Detection

Machine learning fraud detection uses a stack of model types: gradient boosting models (XGBoost, LightGBM) for tabular claim data, neural networks for documents and images, graph neural networks for relationship mapping. The strongest ai fraud detection software platforms combine all three, aggregating outputs into a unified risk score rather than relying on any single algorithm.

What Is AI Fraud Detection? A Clear Explanation for Risk Teams

AI fraud detection explained simply: instead of an analyst reviewing a claim against a checklist, an AI system scores the claim in milliseconds using hundreds of variables, surfaces only the highest-risk cases, and shows the analyst exactly which signals drove the score. This is the core difference between AI and traditional fraud detection that compliance teams need to understand before evaluating vendors.

Supervised vs. Unsupervised Learning in Claims Fraud

Supervised learning trains on labeled data: confirmed fraud cases alongside confirmed legitimate claims. The model learns distinguishing features and applies those patterns to new claims. It works well for established fraud types but needs labeled historical data to get started.

Unsupervised learning needs no labels. It identifies statistical outliers, claims that do not fit any known pattern, making it the early-warning layer for novel schemes before they appear in training data. Most enterprise ai fraud detection in banking and insurance platforms use both: supervised models handle known patterns at volume while unsupervised models catch what is new. Behavioral models require time and claims volume to calibrate, which is worth asking vendors about directly when historical data is limited.

Behavioral Analytics and Pattern Recognition

One capability rules cannot replicate is behavioral analytics over time. Real time fraud detection systems track how claimant behavior changes: a sudden spike in claims after years of silence, slight variations in document signatures across submissions, timing patterns consistent with staged incidents. These longitudinal signals often carry more weight than any single data point on an individual claim, and they grow more accurate as the model accumulates more data about a specific claimant or provider.

The False Positive Problem in Claims Review

The goal is not just catching more fraud. It is catching more fraud while reducing the time spent on legitimate claims.

False Positive Rate and Its Business Impact

Every flagged legitimate claim delays a customer's payment. In personal lines, a homeowner waits for storm repair funds. In health, pre-authorization for a procedure stalls. Most U.S. states have prompt payment laws that create regulatory exposure for delays beyond defined windows.

The false positive cost fraud math is direct: 1,000 weekly reviews at $50 each is $50,000. At an 80% false positive rate fraud detection environment, $40,000 of that confirms legitimate claims are legitimate. That is not a productivity inconvenience; it is a capital allocation problem with a measurable cost that most fraud budgets never explicitly track.

How Fraud Alert Fatigue Damages Investigation Quality

Agentic AI approaches to false positive reduction address a downstream risk most CFOs miss: fraud alert fatigue produces approval bias. When analysts see mostly false alerts, they process them faster and less carefully. Borderline alerts get cleared to reduce queue depth rather than investigated. The alert count looks healthy; review quality has degraded without any visible metric showing it. Real fraud slips through not because the system missed it, but because the reviewer stopped trusting the alerts.

How to Reduce False Positives in AML and Claims Processing

How to reduce false positives in AML and insurance fraud detection follows the same logic: replace binary flag or no-flag decisions with probability-ranked alert queues, and give reviewers enough context per alert to decide quickly and accurately.

Reduce False Positives in Transaction Monitoring

Reduce false positives in transaction monitoring by stacking multiple signals before triggering an alert. A single transaction over $10,000 is required reporting under FinCEN Bank Secrecy Act rules, but not inherently suspicious. A well-calibrated AI asks: Is this consistent with the customer's transaction history? Is the counterparty high-risk with no prior relationship? Does this activity match the account's stated business purpose?

Setting confidence thresholds per claim type rather than one enterprise-wide threshold also matters significantly. Property damage and disability claims have different fraud profiles; a single threshold calibrated for one systematically over-flags the other. One practical calibration approach: layer thresholds by claim dollar value, since a $500 claim with a 65% fraud score may not warrant the same review cost as a $50,000 claim with the same score.

AI-Driven Approaches to Alert Calibration

Automated transaction monitoring platforms with active feedback loops reduce false positives over time. When an analyst closes an alert as a false positive, the AI adjusts future feature weighting based on which signals drove that score. Most platforms show 30-50% false positive reductions within 90 days of feedback activation, with no loss in true positive detection.

The NIST AI Risk Management Framework recommends that AI systems in high-stakes environments include human feedback mechanisms as a quality improvement mechanism, not just a governance requirement.

Real-Time Fraud Detection: Speed Changes the Math

Batch fraud detection, reviewing yesterday's claims today, is a structural advantage for fraudsters. By the time a suspicious claim surfaces in a nightly run, payment may have cleared and the fraud network moved on.

Real-Time Fraud Detection in Banks and Insurance

Real time fraud detection banks have built around instant payments: when transfers clear in seconds, detection must work in milliseconds. Insurance faces the same pressure with the growth of instant claim settlement programs. Some auto insurers now offer same-day payment for minor collision claims through AI photo assessment, which means fraud scoring must fit the same processing window.

Real time fraud detection systems require streaming data infrastructure rather than batch databases. Claims enter the detection pipeline the moment they are submitted. Scores update continuously as new information arrives: a provider's fraud risk changes, an industry pattern is flagged across multiple carriers, a new claim appears from a known high-risk network node.

Automated Transaction Monitoring at Scale

For institutions running both insurance and banking products, automated transaction monitoring is the connective layer. A claimant who is also a bank customer leaves behavioral signals across both channels. A claim submission two days after a large cash withdrawal, combined with a new beneficiary account recently added to the policy, is a combined pattern no single-channel system catches.

Transaction monitoring cost calculations favor automation at volume. A rules-based system processing 500,000 transactions daily requires constant manual tuning and still misses novel patterns. An AI-driven system processes the same volume with a smaller analyst team focused on genuine exceptions rather than routine false positives.

Synthetic Identity Fraud: The Growing Threat AI Catches Early

Synthetic identity fraud is now the fastest-growing financial crime in the U.S. A synthetic identity combines a real Social Security number, often sourced from a child or deceased person, with a fabricated name and address. These identities build credit history over months before being deployed for fraud, making them invisible to point-in-time identity checks at claim submission.

How AI Detects Synthetic Identities at Claim Time

Detecting synthetic identity fraud in real time requires cross-referencing signals that traditional underwriting never collected: velocity of identity element changes across applications, address history inconsistent with credit bureau records, device fingerprints linking multiple applicants to the same origination device, and behavioral biometrics captured during the application process.

Most insurance underwriting systems were not built to catch identity fraud because underwriting and fraud teams historically operated in separate silos. AI integration across those channels is closing that gap, and it is one of the clearest areas where insurers can recover losses that were previously structurally invisible.

Payment Fraud Prevention in the Insurance Context

Payment fraud prevention in insurance differs from banking: the primary vector is the claims payout, not the premium payment side. Fraudsters want illegitimate claim settlements, not stolen payment credentials. AI scoring at claim submission should therefore connect directly with disbursement workflows to flag high-risk payments before they clear.

For insurers evaluating platforms, purpose-built fraud detection software should cover the full policy lifecycle, from underwriting to claims submission to disbursement, rather than operating only at the point of claim review. End-to-end visibility separates enterprise-grade platforms from point solutions.

Evaluating AI Fraud Detection Software for Insurance

Choosing a platform goes beyond detection accuracy. Transaction monitoring software for insurance must integrate with existing claims management systems, support regulatory reporting, and produce explainable outputs that satisfy internal audit and external examiners. Black-box models that return a score with no explanation are increasingly unacceptable to state insurance regulators.

Sardine vs Unit21: A Brief Comparison

For teams comparing platforms, sardine vs unit21 is a common starting point. Sardine focuses on real-time identity and behavioral fraud prevention, with particular strength at the onboarding phase. Unit21 covers case management, transaction monitoring, and SAR filing, making it more relevant for institutions with AML compliance requirements alongside fraud detection. Neither was designed specifically for insurance claims workflows. Insurance-specific document analysis, including medical records, repair estimates, and adjuster notes, typically requires capabilities beyond what either platform provides at the transaction scoring level.

Transaction Monitoring Cost and Total ROI

Transaction monitoring cost varies widely: SaaS platforms run $5,000 to $100,000+ monthly depending on volume, case management depth, and integration complexity. The meaningful evaluation metric is total cost, not platform cost in isolation. That includes analyst headcount for current alert volumes, fraud losses passing through existing detection, and regulatory penalties from missed SAR filings.

Teams responsible for claims auditing and compliance consistently find that a 50-60% reduction in false positives covers platform cost within the first year through analyst time savings alone.

Onboard Customers in Seconds

Conclusion

Insurance claims fraud detection AI is not a future investment. It is a present operational necessity. Fraud losses are growing, schemes are more sophisticated than static rules can handle, and the cost of high false positive rates quietly drains analyst capacity every month. Better detection accuracy, fewer wasted reviews, and faster claim resolution for legitimate policyholders are measurable outcomes achievable with the right AI approach.

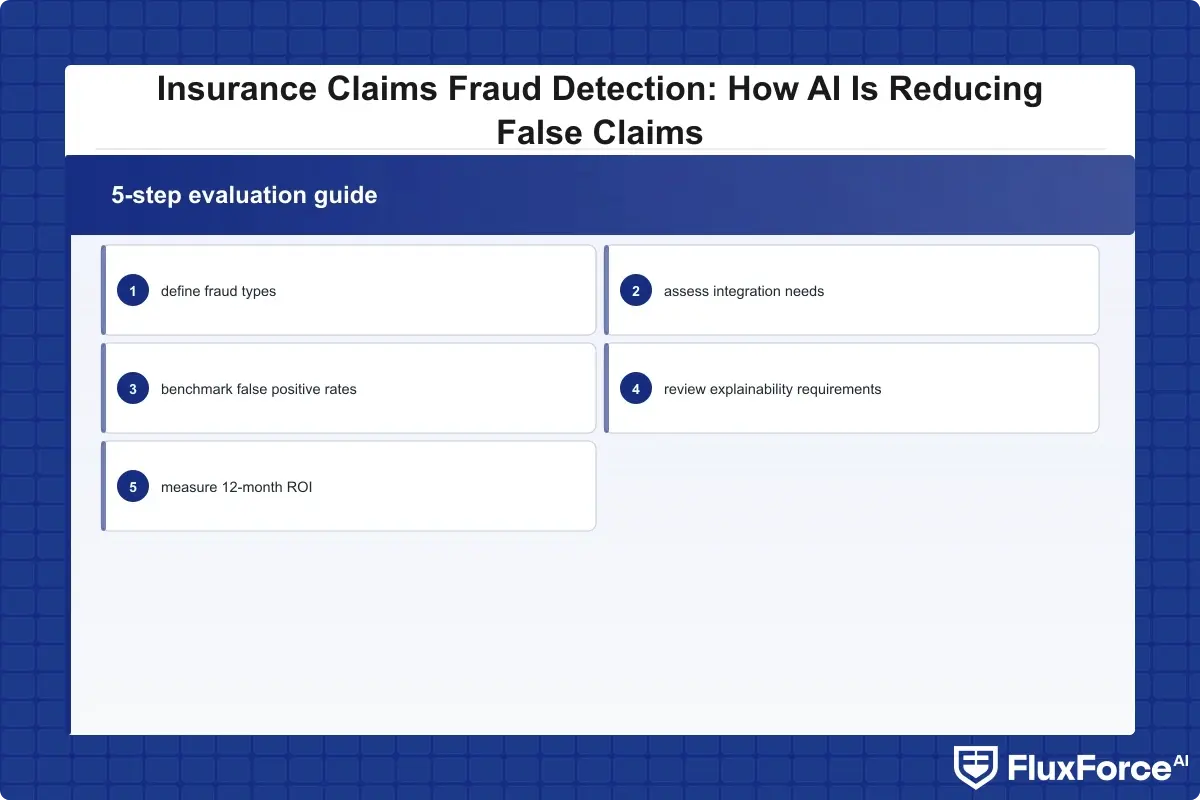

The starting point for most teams is an honest audit: what is the current false positive rate, what is the alert-to-investigation conversion rate, and what does each false positive cost in analyst time and customer friction? Once those numbers are on paper, the case for ai fraud detection becomes straightforward to make to any board or CFO.

Share this article