.webp)

Listen To Our Podcast🎧

Credit card fraud detection methods that rely on AI now outperform legacy rule-based systems by measurable margins, and the gap widens with every new fraud vector. Global card fraud losses exceeded $32 billion in 2023, per the Nilson Report, with card-not-present fraud projected to account for nearly 75% of total losses by 2026. For risk teams at banks, fintechs, and insurers, the question is no longer whether to modernize, but which approach delivers real-world results at production scale.

This guide breaks down traditional versus AI-powered fraud detection, covers where legacy systems break, and explains exactly how machine learning models, real-time monitoring, and adaptive risk scoring change the economics for enterprise teams.

Why Traditional Credit Card Fraud Detection Methods Break Down

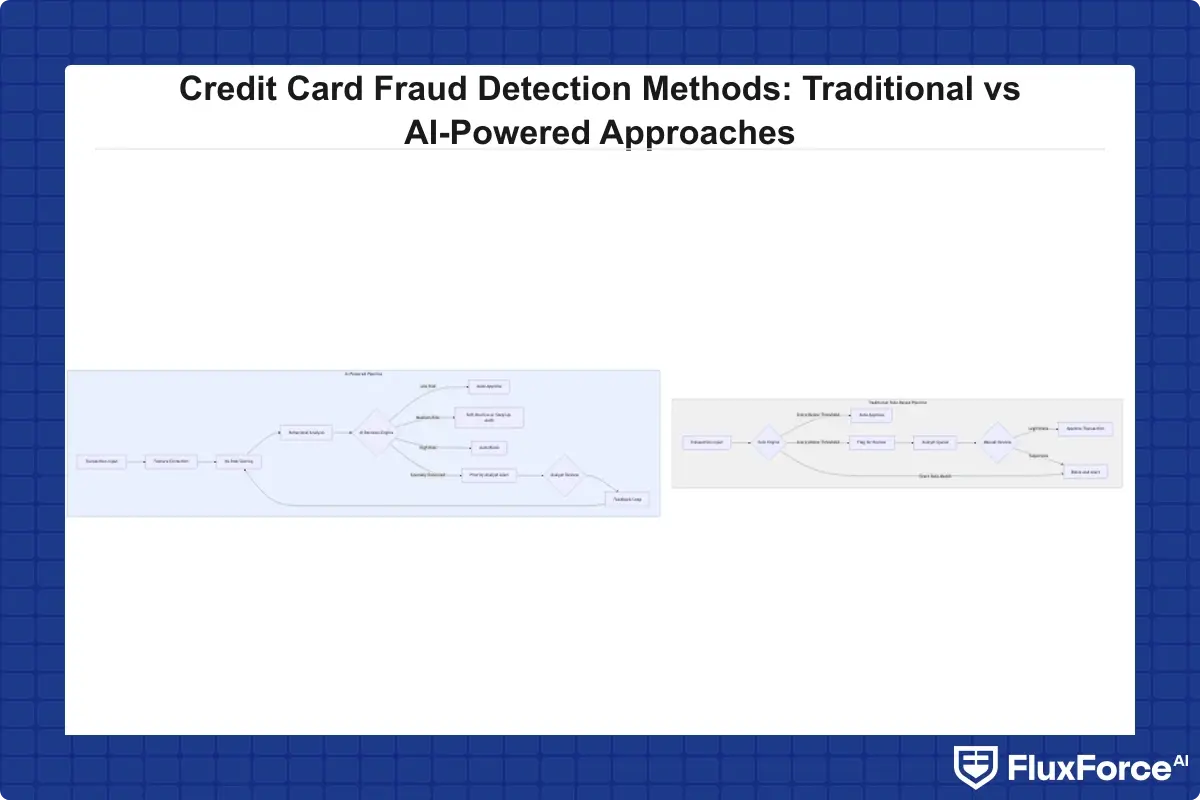

Rule-based fraud systems were designed when transaction volumes were lower and fraud patterns were more predictable. The core logic is simple: define a set of rules, flag any transaction that violates them, send alerts to analysts. That simplicity is also the problem.

The Rule-Based System Problem

A typical rule-based system for a mid-size bank might carry 200 to 500 active rules. Each rule needs manual creation, testing, and ongoing maintenance. When a new fraud pattern emerges, someone has to write a rule to catch it. By the time the rule is tested and deployed, fraudsters have usually moved on. Security teams find themselves perpetually chasing yesterday's attack patterns while today's losses accumulate.

Rules are also blind to context. A $3,000 purchase at an electronics retailer flags as suspicious for most cardholders. But for a small business owner who buys inventory there every week, it is completely normal. Rule-based systems cannot distinguish between these two scenarios without adding so many exceptions that the original rule becomes nearly useless.

How Fraud Alert Fatigue Drains Operations

Fraud alert fatigue is one of the most underreported operational costs in financial services. When analysts receive hundreds of alerts per day, most of which turn out to be legitimate transactions, they start cutting corners. Review quality drops, genuine fraud slips through, and analyst burnout leads to turnover. Onboarding new reviewers costs roughly 3-6 months of productivity loss per seat.

According to the Association of Certified Fraud Examiners, the average organization loses 5% of annual revenue to fraud. A false positive rate in the 90-95% range, which is common in rule-based systems, means analysts spend the majority of their day reviewing legitimate transactions rather than actual fraud.

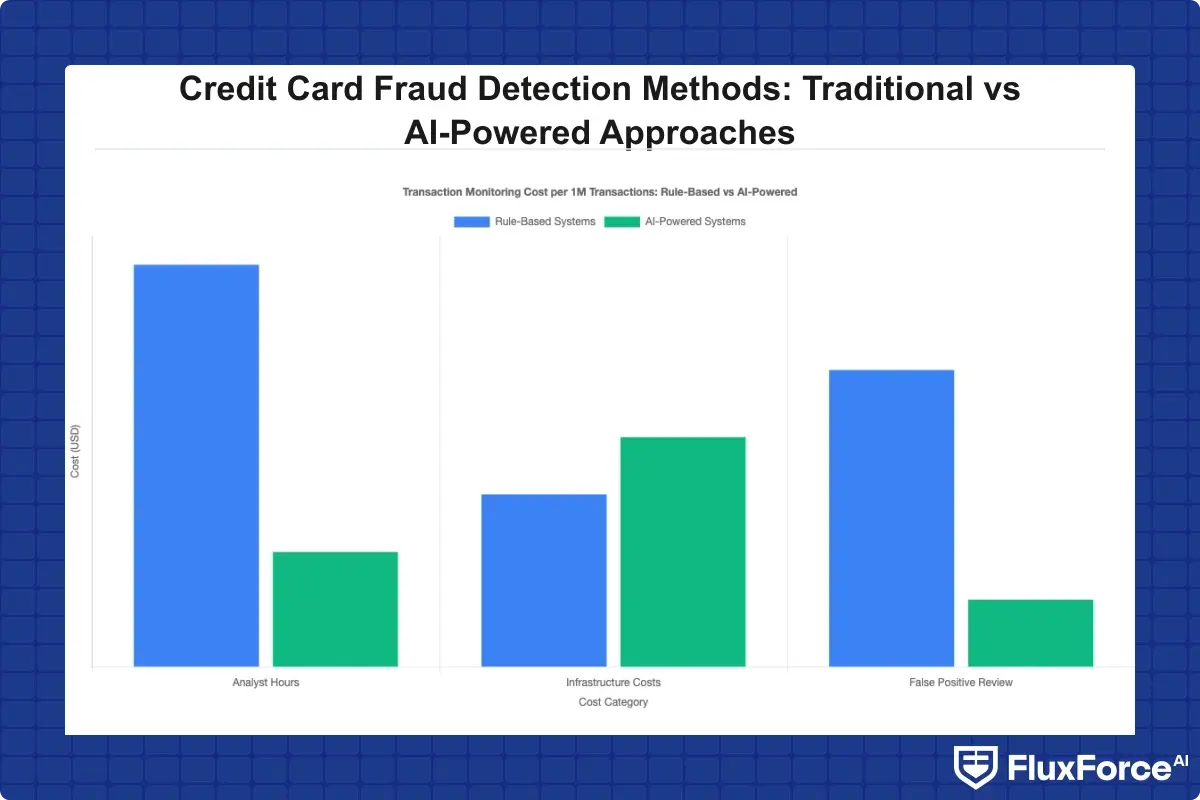

Transaction Monitoring Cost at Scale

Transaction monitoring cost grows faster than transaction volume. Adding more rules requires more analyst capacity to review the resulting alerts. Adding more analysts requires management overhead, training time, and quality assurance infrastructure. By the time a bank reaches 10 million transactions per month, manual review is both economically unsustainable and operationally unreliable.

This cost curve is a primary driver pushing enterprise teams toward automated transaction monitoring. If AI handles 80% of alert triage automatically, teams need a fraction of the analyst headcount and can redeploy skilled reviewers to genuinely complex cases.

How AI Fraud Detection Actually Works

AI fraud detection explained simply: rather than matching transactions against fixed rules, AI models learn the statistical signature of normal behavior for each cardholder and flag deviations from that baseline. The model updates continuously as new transaction data arrives, which means it adapts to new fraud patterns without manual rule writing.

Machine Learning Fraud Detection Models

Machine learning fraud detection typically uses a combination of supervised and unsupervised techniques. Supervised models are trained on labeled datasets of confirmed fraud and legitimate transactions. They learn which features (transaction amount, merchant category, time of day, device fingerprint, and geographic location) correlate with fraud. Gradient boosting and neural network models are the most common choices at this layer.

Unsupervised models handle the harder problem: detecting fraud patterns the training data has never seen. Anomaly detection algorithms like isolation forests and autoencoders flag behavior that deviates significantly from historical norms without needing a fraud label. This matters especially for synthetic identity fraud and novel attack vectors that supervised models would miss entirely.

How Does AI Detect Fraud in Real Time?

How does AI detect fraud during a live transaction? The answer involves several parallel signals processed in milliseconds. When a cardholder initiates a payment, the fraud detection engine pulls behavioral biometrics (typing speed, device tilt, swipe patterns), device intelligence (browser fingerprint, IP reputation, VPN flags), transaction history (typical spend patterns, known merchants, usual locations), and network graph data (connections to flagged accounts or merchants). All of this is scored against the live model, producing a risk decision typically within 50 to 200 milliseconds.

What separates mature AI fraud detection in banking from basic ML implementations is the behavioral and relational intelligence layered on top of the core scoring engine. Network graph analysis maps relationships between accounts, devices, and merchants to identify fraud rings. If three accounts that never interacted before suddenly all transact with the same new merchant, the graph flags the cluster for review. This approach is critical for catching synthetic identity fraud rings early. For a deeper look at detection strategies for this specific threat, see Detecting Synthetic Identity Fraud in Real-Time.

Real-Time Fraud Detection: Speed as a Competitive Requirement

Payment fraud prevention now requires sub-second decision making. The shift to instant payments, buy-now-pay-later, and cross-border digital wallets means fraud windows are measured in seconds, not hours. A fraud check that takes 3 seconds is not usable in a real-time payment rail.

Real-Time Fraud Detection Banks Are Deploying

Real-time fraud detection at banks like JPMorgan, HSBC, and Revolut involves streaming architectures where every transaction event is processed through a scoring engine before authorization. The technical stack typically involves event streaming platforms like Apache Kafka feeding into a model serving layer that returns risk scores in under 100 milliseconds.

The business impact is concrete. Barclays reported a 35% reduction in fraud losses after deploying a real-time scoring layer. HSBC cited an 80% reduction in manual review volume for low-risk transactions after deploying adaptive thresholds. These are not edge cases. They represent the typical range of outcomes for banks that make the transition with proper model governance in place.

How Automated Transaction Monitoring Reduces Decision Latency

Automated transaction monitoring removes the human bottleneck from low-risk decisions. The model handles straightforward cases: low-risk transactions auto-approve, clearly fraudulent transactions auto-block, and only genuinely ambiguous cases route to analysts. This triaging layer is where the economic case for AI becomes concrete. A team of 20 analysts can cover the same transaction volume that previously required 80, with better detection accuracy and faster response times.

The catch: model quality degrades if it is not retrained regularly. Fraud patterns shift faster than annual retraining cycles can track. Effective automated transaction monitoring requires continuous feedback loops where analyst decisions on escalated cases feed back into model updates, typically on a weekly or biweekly basis.

The False Positive Problem: Numbers That Should Concern Every Risk Team

False positives in fraud detection are not just an annoyance. They carry measurable costs across customer experience, analyst productivity, and revenue.

False Positive Cost Fraud Teams Actually Bear

False positive cost in fraud operations includes the analyst time to review each false alert (typically 15-25 minutes for complex cases), the customer friction from declined legitimate transactions, and the churn from customers who switch cards after repeated false declines. Card issuers lose an estimated $118 billion annually in declined sales attributable to false positives, per industry research. For a bank processing 5 million transactions per day at a 1% false positive rate, that is 50,000 alerts per day requiring human review.

The false positive rate in fraud detection varies significantly by method. Rule-based systems typically run at 90-95% false positive rates on flagged transactions. Basic ML models bring that number down to 60-70%. Advanced AI systems with behavioral context and graph intelligence achieve false positive rates in the 10-30% range. That gap directly translates to analyst headcount requirements, customer satisfaction scores, and fraud loss ratios.

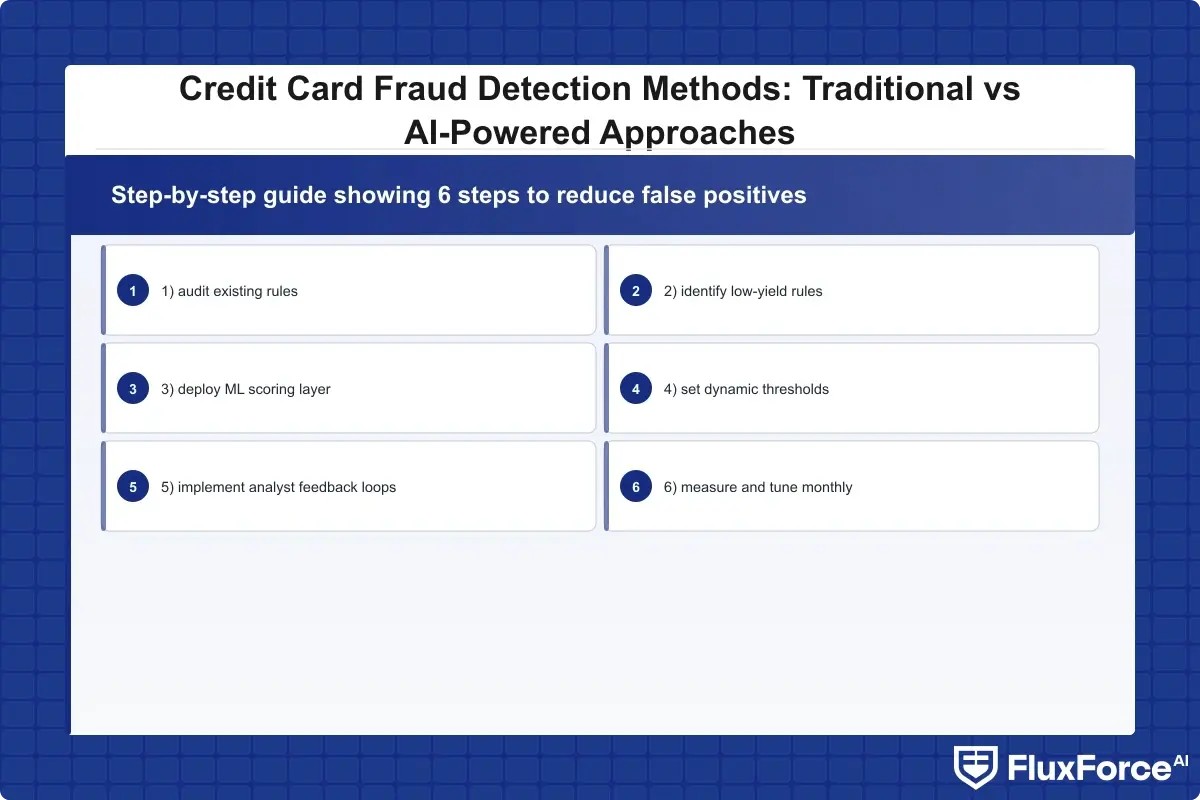

How to Reduce False Positives in AML

How to reduce false positives in AML programs requires more than switching models. The most effective approaches combine better feature engineering (adding behavioral context to each transaction record), dynamic thresholds (risk scores that adjust based on the customer's typical activity rather than a population average), and analyst feedback loops (review decisions feeding back into the model as labeled training data). Teams that implement all three typically see false positive rates drop 50-70% within 6 months of deployment.

For teams looking to reduce false positives in transaction monitoring, the practical starting point is auditing which existing rules generate the highest alert volume with the lowest confirmed fraud rate. Those are the rules to retire first and replace with ML-based scoring. FinCEN transaction monitoring guidance provides a regulatory framework for evaluating alert program effectiveness. For a detailed tactical approach, Reducing False Positives: Rule-Based Systems vs. AI-Driven Solutions covers this process in depth.

AI Fraud Detection in Banking: Enterprise Use Cases

AI fraud detection in banking covers a broader scope than card fraud alone. The same infrastructure that catches card fraud applies across account takeover, wire fraud, check fraud, and synthetic identity fraud schemes that target onboarding rather than existing accounts.

Synthetic Identity Fraud Detection

Synthetic identity fraud uses a mix of real and fabricated personal information to create identities that pass standard KYC checks. Traditional rule-based systems struggle because the identity elements individually look legitimate. AI models detect synthetic identities through behavioral signals after account opening: thin transaction history, rapid credit utilization, unusual usage patterns, and network connections to other synthetic accounts. Banks using AI-powered synthetic identity detection report catching 40-60% more of these schemes compared to rule-based approaches, with significantly lower investigation costs per confirmed case.

Payment Fraud Prevention Across Channels

Payment fraud prevention now spans cards, ACH, wire transfers, real-time payments, and mobile wallets. Each channel has different fraud patterns, risk profiles, and regulatory requirements. AI fraud detection software handles multi-channel risk by maintaining a unified customer risk profile that updates across all channels in real time. A suspicious mobile wallet transaction informs the risk score on the same customer's card transaction 5 minutes later. For compliance teams at banks and insurers who need to integrate fraud detection with broader AML and KYC workflows, the Card Fraud Analytics strategy guide covers this integration in depth.

Sardine vs Unit21: How to Compare AI Fraud Detection Platforms

Sardine vs Unit21 is one of the most common platform comparisons enterprise buyers run when evaluating AI fraud detection software. Both platforms offer real-time decisioning and integrate with common payment stacks. The differences matter depending on your specific use case and where your biggest operational gap sits.

Feature and Capability Comparison

Sardine is strongest in device intelligence and behavioral biometrics. It ingests over 4,000 device signals per session and is particularly effective for onboarding fraud and account takeover detection. Its rule engine allows non-technical teams to write and test fraud rules without engineering support, which reduces time-to-deployment significantly.

Unit21 is built more explicitly for AML and fraud investigation workflows. Its case management capabilities are more mature, with built-in SAR filing support, investigation timelines, and analyst collaboration tools. Teams that need both real-time detection and post-detection investigation management often find Unit21's end-to-end workflow more practical than Sardine's detection-focused architecture.

The honest assessment is that neither platform is universally better. Sardine wins on detection speed and device intelligence. Unit21 wins on investigation workflow and compliance tooling. The right choice depends on whether your biggest gap is detection accuracy or analyst productivity after detection.

Transaction Monitoring Software Decision Factors

When evaluating any transaction monitoring software, the criteria that matter most for enterprise teams are: latency (sub-200ms for real-time payment support), model transparency (can you explain a fraud decision to a regulator?), feedback loop architecture (how do analyst decisions retrain the model?), and integration flexibility (REST APIs, event streaming, pre-built connectors to your payment stack). Pricing models also vary significantly, and most platforms charge per transaction or per alert reviewed. The cost difference becomes substantial at volumes above 50 million transactions per month. For enterprise teams building the business case for AI-powered fraud detection software, the total cost of ownership calculation should include reduced analyst headcount, lower fraud loss rates, and customer retention improvements from fewer false declines, not just licensing fees.

How to Evaluate AI Fraud Detection Software for Enterprise Deployment

AI fraud detection software selection is a 6-12 month process for most enterprise buyers. The technical evaluation is only one part. Regulatory approval, vendor security reviews, and data governance assessments each add time and complexity.

Key Evaluation Criteria

The five questions that separate adequate from genuinely good AI fraud detection software for banking are:

- Model explainability: Can the system produce a human-readable explanation for each fraud decision? GDPR Article 22 and various banking regulations require explainable automated decisions.

- Latency under load: Does the system maintain sub-200ms response times at peak transaction volumes? Many vendors perform well in demos but degrade under production load.

- Retraining frequency: How often does the model update? Weekly retraining is a minimum for environments with fast-moving fraud patterns.

- False positive controls: What tools does the platform give analysts to tune thresholds by segment, channel, or customer tier?

- Regulatory alignment: Does the system support SAR filing, audit trails, and data residency requirements for your jurisdictions?

Integration and Implementation Considerations

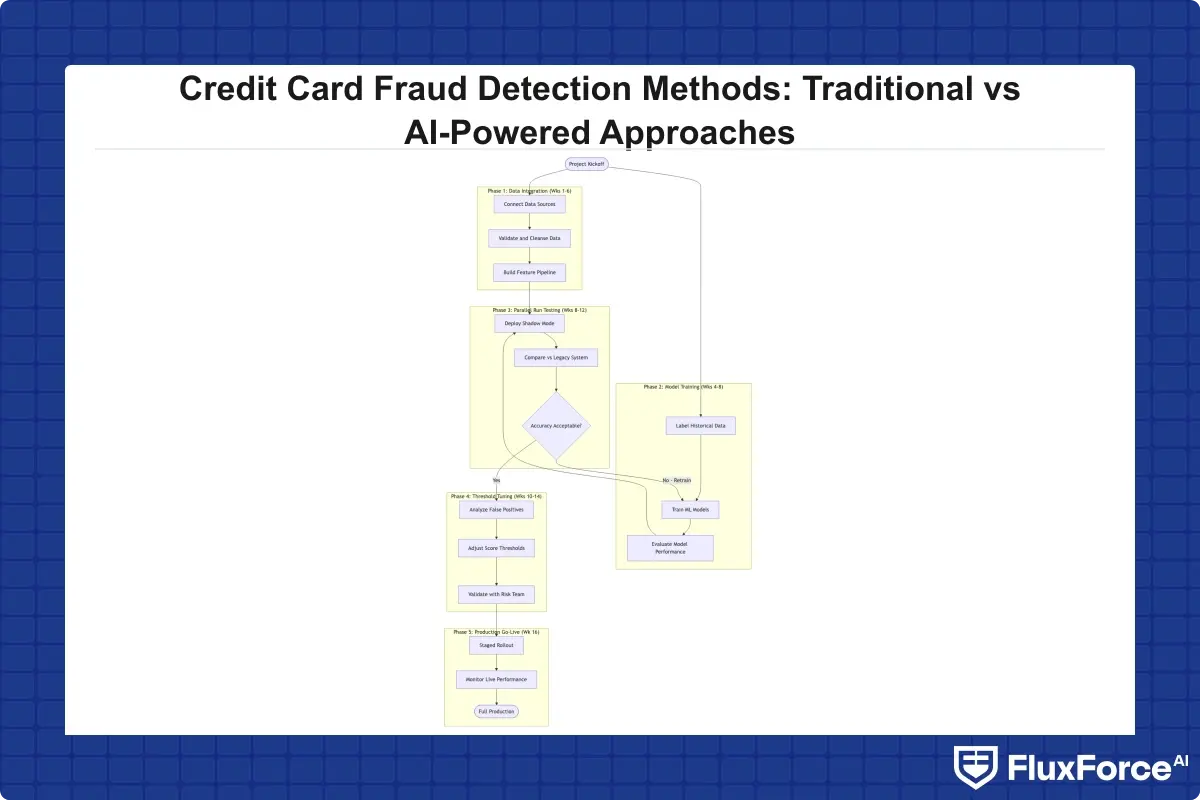

Most enterprise fraud detection deployments take 3-6 months from contract to production. The longest delays typically come from data integration: connecting the fraud system to core banking, KYC, and CRM data sources. Platforms with pre-built connectors for common banking stacks reduce this timeline significantly. Teams that have already modernized their core banking infrastructure report faster fraud detection deployments because the event streaming architecture is already in place. For context on that infrastructure dependency, see Legacy to Cloud: Core Banking Modernization Strategy for Payments Risk Officers.

Onboard Customers in Seconds

Conclusion

Credit card fraud detection methods that incorporate AI deliver measurably better outcomes than rule-based systems: lower false positive rates, faster detection, better coverage of novel fraud patterns like synthetic identity fraud, and lower total operational cost at scale. The transition requires real investment in model governance, regulatory compliance, and integration work. But the arithmetic is straightforward: teams that maintain legacy rule-based systems are paying more to catch less fraud, and the gap grows wider as transaction volumes increase.

The next step for most risk teams is identifying the highest-cost bottleneck in the current workflow (false positive volume, real-time detection gaps, or AML alert fatigue) and deploying AI-driven automation for that specific problem first. For enterprise teams starting that evaluation, AI vs. Traditional Fraud Detection provides a practical comparison framework. Payment fraud prevention at enterprise scale requires modern tooling, and the institutions that act sooner are building a measurable advantage in both loss prevention and operational efficiency.

Share this article