.webp)

Listen To Our Podcast🎧

Fraud detection platforms community banks can realistically deploy have finally reached a level of capability that matches the scale of the threat. In 2026, purpose-built transaction monitoring software exists for institutions with $300 million to $5 billion in assets, not just national banks. If you want ai fraud detection explained in terms your compliance team can act on: AI systems replace static rule sets with statistical models that score every transaction based on context, device behavior, account history, and network relationships simultaneously. The result is fewer missed fraud cases and far fewer false positive alerts burying your analysts.

This guide covers five platforms consistently appearing in community bank RFPs, how they handle ai fraud detection in banking, what they cost at community bank scale, and how they address the two issues dominating compliance conversations in 2026: synthetic identity fraud and fraud alert fatigue.

Why Community Banks Face a Different Fraud Problem

Community banks operate with leaner compliance teams, more concentrated customer relationships, and far less transaction data than national banks. Fraud models built on millions of large-bank transactions do not translate cleanly to a bank with 40,000 accounts. At the same time, fraud networks increasingly target community banks because their authentication stacks tend to be weaker and their fraud response times slower.

The FDIC's community banking research shows that community banks represent more than 90% of all U.S. banking institutions by count, yet their collective fraud prevention budget is a fraction of the industry total. That imbalance creates real exposure that purpose-built fraud detection platforms community banks can now address without enterprise-grade infrastructure.

The Real Cost of Fraud Alert Fatigue

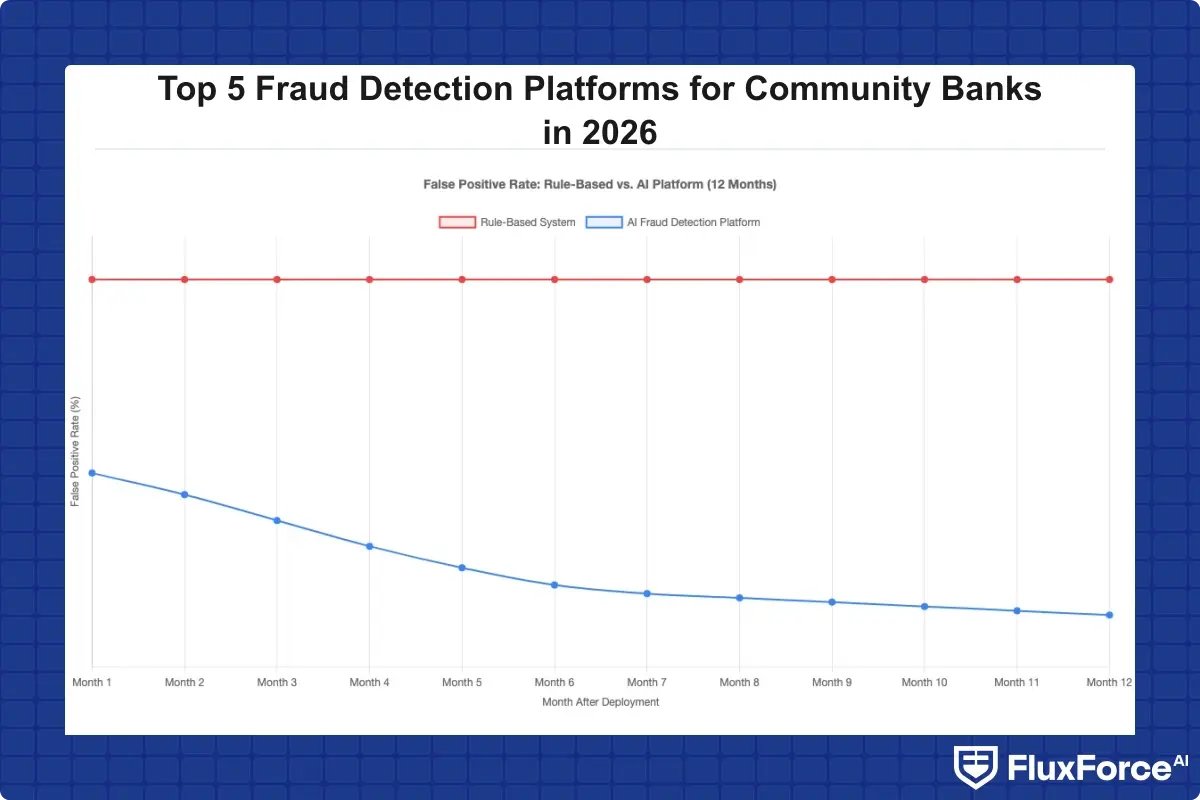

Fraud alert fatigue happens when analysts receive hundreds of alerts daily, learn through experience that most are false positives, and begin moving through queues too quickly. At community banks running legacy rule-based systems, false positive rates commonly exceed 95%. Running the math: four analysts, 400 daily alerts, 95% false positive rate, four minutes per alert, that is nearly 25 hours of wasted analyst time per day.

The practical consequence is not just cost. Analysts conditioned by fraud alert fatigue miss real fraud because every alert looks like noise. That is a compliance risk bank examiners are tracking more closely than they were three years ago.

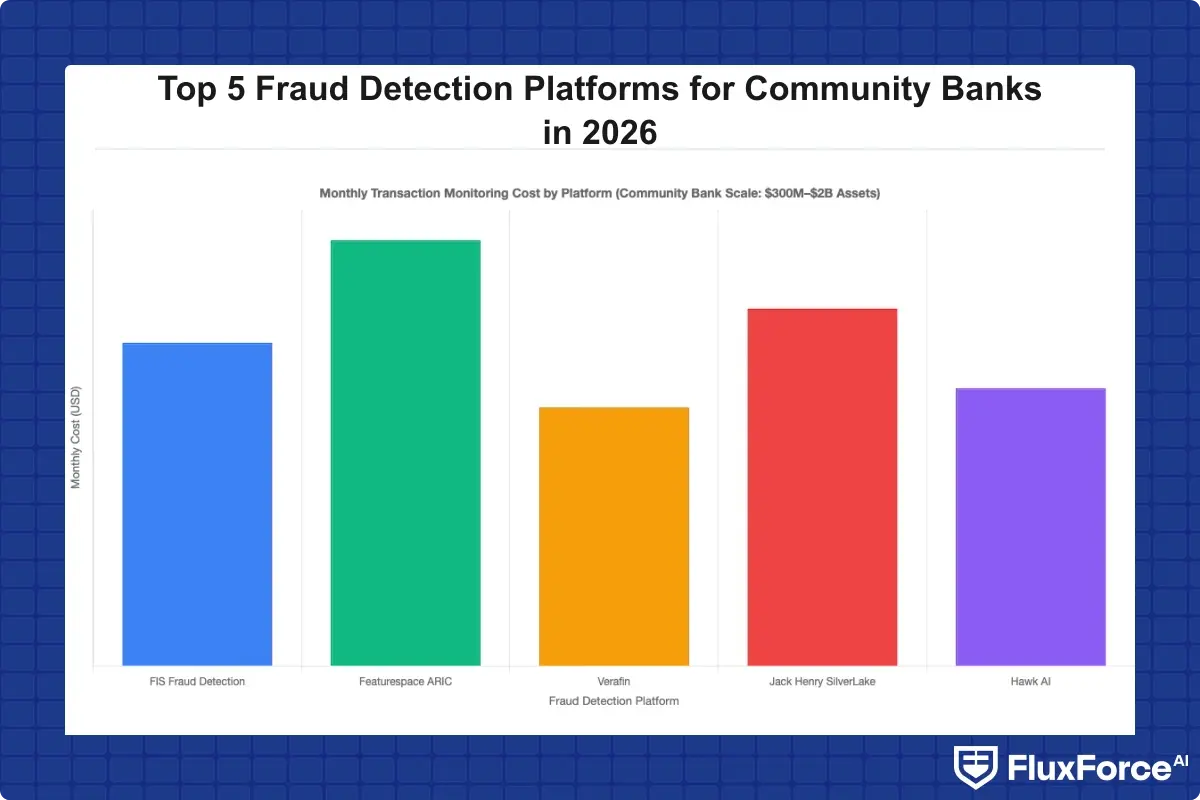

Transaction Monitoring Cost at Community Bank Scale

Transaction monitoring cost is the second pressure point. Legacy platforms priced for enterprise banks charged per-transaction fees that compound as digital banking increases volume. A community bank processing two million transactions per month on a $0.003 per-transaction model pays $6,000 per month in base fees before implementation or integration costs.

Newer SaaS-native platforms have shifted to flat monthly fees or asset-based tiers. The five platforms in this guide price between $2,000 and $15,000 per month for community bank tiers, with implementation costs ranging from $15,000 to $80,000 depending on core system complexity.

How Does AI Detect Fraud in Community Banking?

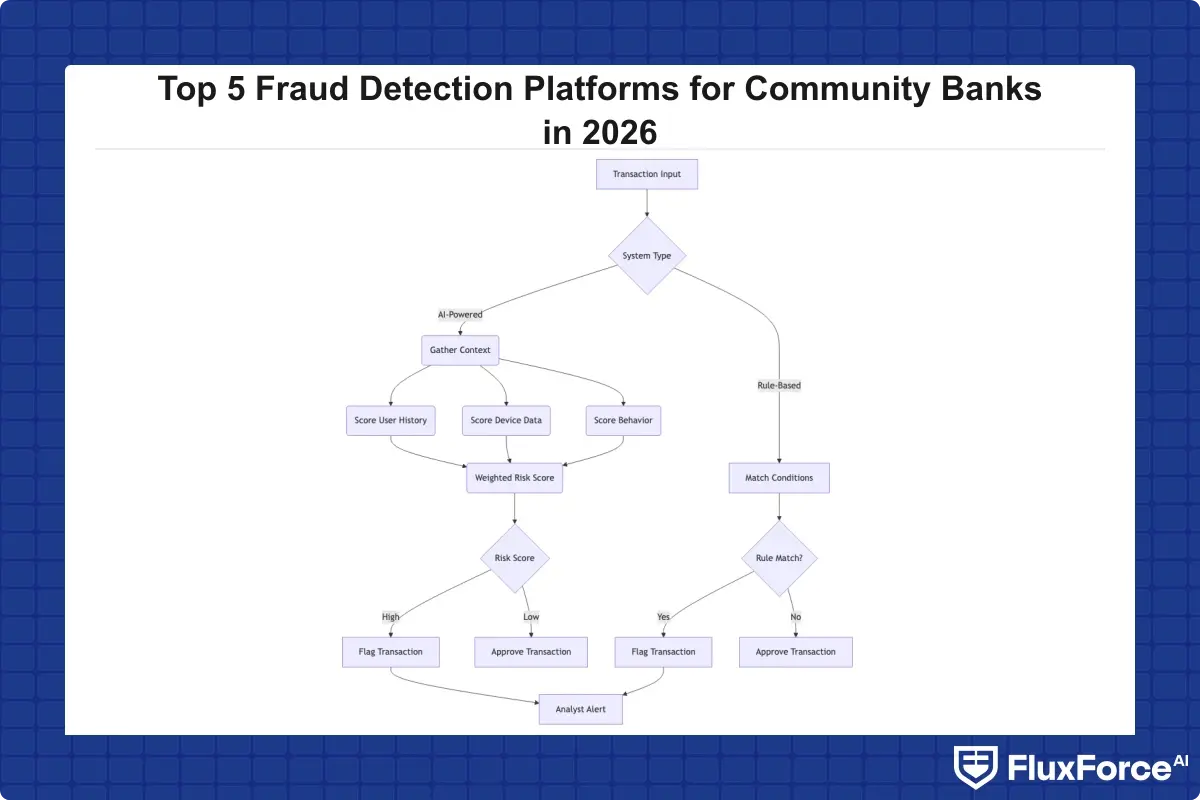

AI fraud detection in banking works by building statistical models of normal behavior at the account, device, and network level, then flagging deviations from that baseline. Unlike rule-based systems that fire when a transaction matches a predefined condition, AI systems score each transaction based on dozens to hundreds of contextual features simultaneously.

When a customer initiates an ACH transfer at 2am from a new device to an account they have never paid before, a rule-based system might not flag it because each individual element falls below threshold. An AI system sees the combination as high-risk and surfaces it immediately.

Machine Learning Fraud Detection Models

Machine learning fraud detection in financial services relies on three model types:

- Supervised learning: Trained on labeled historical fraud data. Accurate when the bank has substantial confirmed fraud examples, but it struggles at smaller institutions with thin fraud history. Most vendors supplement with consortium data from their broader customer base.

- Unsupervised learning: Detects anomalies without labeled data, catching novel fraud patterns that have not appeared in training history. The tradeoff is higher false positive rates early in deployment until the model calibrates to normal customer behavior.

- Graph analytics: Maps relationships between accounts, devices, IP addresses, and phone numbers to surface fraud rings. Particularly effective for synthetic identity fraud, where individual accounts look clean but share suspicious network connections.

Serious platforms use ensemble models combining all three, weighting their outputs into a final risk score. That ensemble approach drives meaningful gains in false positive rate fraud detection compared to any single model type.

Real-Time Fraud Detection Banks Rely On

Real time fraud detection banks depend on requires understanding actual latency requirements. Card-present authorization needs a fraud decision in 150-300 milliseconds. ACH and wire transfers allow more time but carry higher per-transaction loss potential. Zelle and RTP rails require near-instant decisions, if your system batches transactions into 30-60 minute windows, fraud has settled before your alert fires.

Ask every vendor for their p95 scoring latency on a transaction API call. That number tells you whether they can handle card-present authorization in-line or only support post-authorization review.

How Does AI Reduce False Positives?

AI reduces false positives by scoring full context rather than individual signals. A $5,000 wire from a small business account that sends payroll transfers every Friday scores very differently than the same amount from a retail account with no wire history. Rule-based systems can approximate this with enough segment-specific rules, but maintaining hundreds of those rules is exactly the operational burden most community banks want to eliminate.

The reduction in false positives compounds over time as the model learns from analyst decisions. As our analysis of how agentic AI fraud agents cut false positives by 80% explains, the closed-loop feedback cycle is what separates genuine AI fraud detection from smarter rule management.

Top 5 Fraud Detection Platforms for Community Banks in 2026

These five fraud detection platforms community banks consider most frequently in 2026 all offer cloud-native delivery, API-first integration, and pricing structures sized for banks outside the top 100 by assets. None require a dedicated fraud data science team to operate.

1. Sardine

Sardine builds fraud and compliance tooling for financial institutions that have moved to digital-first channels. Its device intelligence layer collects over 4,000 device and behavioral signals during every session, including subtle cues like how a user types, scrolls, and moves between form fields. That depth makes Sardine particularly effective at account opening fraud and synthetic identity detection, where behavioral anomalies appear before any suspicious transaction occurs.

For community banks with active online account opening, Sardine's pre-transaction risk scoring closes a gap that most automated transaction monitoring tools leave open: fraud at the application stage, not the transaction stage.

Best for: Digital-first community banks with significant online account opening volume.

Limitation: SAR workflow and case management are lighter than compliance teams with complex AML obligations typically need. Evaluate whether a separate case management layer is required.

Approximate pricing: $3,000-$10,000/month depending on event volume and modules.

2. Unit21

Unit21 targets compliance and fraud teams that want operational control without engineering dependency. Its no-code rule builder lets analysts create, test, and deploy detection rules through a visual interface without submitting development tickets. For community banks where IT headcount is limited, that independence is genuinely valuable.

Unit21's SAR filing workflow and case management are among the strongest at this pricing tier. FinCEN integration comes pre-built, and the automated transaction monitoring covers ACH, wire, card, and cash transactions with configurable rule sets analysts can maintain themselves.

Best for: Community banks prioritizing AML compliance workflow, SAR management, and analyst self-sufficiency.

Limitation: Unit21's behavioral AI is more conservative than Sardine's device intelligence layer. It is stronger on workflow than on pure AI-driven anomaly detection.

Approximate pricing: $2,500-$8,000/month. Asset-based tiers available for banks under $1 billion.

3. Hawk AI

Hawk AI builds specifically for financial crime compliance at community banks and credit unions. Its automated transaction monitoring covers AML monitoring, CTR and SAR filing support, and produces explainable alerts that describe in plain language why a transaction was flagged. That explainability matters during examinations: you can show regulators not just what the system flagged, but why.

The false positive management tooling is practical, analysts can tune thresholds by customer segment without engineering involvement, which accelerates calibration significantly.

Best for: Community banks whose primary use case is AML compliance with examiner-ready documentation.

Limitation: Payment fraud prevention coverage is narrower than Sardine or Featurespace. If card fraud or Zelle fraud is the primary concern, supplementation may be needed.

Approximate pricing: $2,000-$6,000/month for community bank tiers.

4. Featurespace

Featurespace's ARIC Risk Hub runs on adaptive Bayesian models that learn individual customer behavior continuously and score deviations in real time. The platform has a track record specifically in card fraud, and several mid-market U.S. banks have used it to reduce card-present and card-not-present fraud losses significantly.

The honest tradeoff for community banks: implementation is more complex than the lighter SaaS options. Featurespace requires substantive data engineering work to connect to core banking systems, and implementation timelines run 60-90 days. If you have internal engineering capacity and card fraud is a priority, that investment pays off.

Best for: Community banks with card processing operations and internal data engineering capacity.

Limitation: Higher implementation complexity and cost than Unit21 or Hawk AI. Not appropriate for banks needing rapid deployment.

Approximate pricing: $5,000-$15,000/month. Implementation typically runs $40,000-$80,000.

5. Alloy

Alloy approaches fraud from an identity decisioning framework rather than transaction monitoring. The platform builds a continuous risk profile on each customer identity, drawing from bureau data, government ID verification, device fingerprints, and behavioral signals during the application session. That identity-layer approach catches fraud types that transaction monitoring alone misses, particularly first-party fraud and synthetic identity fraud at account opening.

For community banks expanding into digital lending, Alloy provides a risk-scored identity decision at onboarding that prevents fraudulent accounts from being established in the first place.

Best for: Community banks with growing digital onboarding and first-party fraud exposure.

Limitation: Alloy is not a full AML transaction monitoring platform. It works best paired with a monitoring tool like Unit21 or Hawk AI.

Approximate pricing: $2,000-$7,000/month depending on decision volume.

Sardine vs Unit21: Which Is Better for Community Banks?

The sardine vs unit21 comparison surfaces in nearly every community bank fraud platform evaluation in 2026. Both are SaaS-native, priced for mid-market institutions, and require no dedicated fraud data science team. But they are built for different problem profiles, and choosing based on demo quality rather than fit is a common mistake.

Feature Comparison

| Feature | Sardine | Unit21 |

|---|---|---|

| Device Intelligence | Deep (4,000+ signals) | Basic |

| Behavioral AI | Strong | Moderate |

| No-Code Rule Builder | Limited | Strong |

| AML/SAR Workflow | Basic | Strong |

| Real-Time Scoring | Sub-second | Near-real-time |

| Implementation Time | 30-45 days | 21-30 days |

| API-First Architecture | Yes | Yes |

| Card Fraud Coverage | Strong | Moderate |

Pricing and Transaction Monitoring Cost

Both platforms price similarly at community bank scale, but the cost model differs. Sardine scales with event volume, device assessments, onboarding decisions, transaction scores, which works well for banks with high online account opening activity. Unit21 typically combines alert volume with seat-based pricing.

Transaction monitoring cost on Unit21 is more predictable month-to-month, which CFOs working on fixed annual budgets prefer. Sardine's pricing can surprise banks that underestimate their digital event volume. Get an accurate event count before signing.

Which Platform Fits Your Bank's Size?

For community banks under $1 billion in assets with small compliance teams, Unit21 delivers faster time-to-value. Analysts can maintain their own detection logic without waiting on engineering. For banks that need strong fraud prevention at account opening, Sardine's device intelligence layer goes where rule-based systems cannot follow.

The deeper architectural difference is covered in our analysis of AI vs. traditional fraud detection methods: Sardine is AI-first by design, while Unit21 is workflow-first with AI layered in. The right choice depends on whether your primary bottleneck is detection accuracy or analyst productivity.

Synthetic Identity Fraud: The Threat Community Banks Can't Ignore

Synthetic identity fraud is the fastest-growing fraud type in U.S. banking. A synthetic identity combines real data elements, often a valid Social Security number from a credit-thin individual such as a child or recent immigrant, with fabricated name, address, and contact information to create a fictitious person. Fraud rings then build credit history over months before maxing out every available credit line and disappearing.

The Federal Reserve's research on synthetic identity fraud estimated losses of more than $6 billion annually to U.S. banks and lenders, with community banks disproportionately exposed because standard credit bureau checks do not catch well-cultivated synthetic identities.

How AI Detects Synthetic Identity Fraud

Standard underwriting does not catch synthetic identities well because they are designed to pass bureau checks. AI catches them by examining signals bureaus do not see: device fingerprints shared across multiple applications, phone numbers less than 90 days old, address clusters appearing across multiple recent applications, and behavioral anomalies during the application session itself.

Graph analytics is particularly powerful here. A single synthetic identity is difficult to flag on individual attributes alone. When 40 applications share the same device or the same phone number appears across applications for different names, the pattern becomes visible across the network. Machine learning fraud detection built on graph signals surfaces these rings at volumes no manual review process can match.

Real-Time Detection in Practice

Real time fraud detection for synthetic identities has to happen at account opening, not 18 months later when the fraudster charges off. The platforms built for this, Sardine and Alloy specifically, run identity risk scores during the application session, before the bank makes a credit decision. Behavioral signals collected during the application flow add a layer of signal that bureau data cannot provide.

Our detailed post on detecting synthetic identity fraud in real time walks through the specific signal types that catch these identities before they become losses, including how device-sharing patterns surface fraud rings that look clean at the individual account level.

What to Look for in Fraud Detection Software

Evaluating ai fraud detection software for a community bank means distinguishing capabilities that matter for your specific risk profile from features that look impressive in a demo. Here is what to prioritize.

Automated Transaction Monitoring Capabilities

Automated transaction monitoring should cover your actual transaction channels: ACH credits and debits, wires, cash transactions above CTR thresholds, card transactions if applicable, and peer-to-peer flows like Zelle. Beyond channel coverage, evaluate how the automation handles alert disposition. Can analysts annotate cases and build institutional memory? Does the system learn from disposition history, or does it generate the same alert patterns regardless of how analysts have responded?

FinCEN's AML/CFT compliance guidance requires that financial institutions maintain risk-based monitoring programs and demonstrate periodic evaluation. Transaction monitoring software that cannot produce audit-ready rule performance reporting creates examination risk independent of its detection capabilities.

Payment Fraud Prevention Integration

Payment fraud prevention must cover the channels your customers actually use. For most community banks in 2026, that means ACH, wire, and at minimum Zelle. The key evaluation question for real-time rails: what is the platform's scoring latency for Zelle P2P transactions? If the answer is batch processing, fraud has long settled before your alert fires.

For a broader view of how payment security infrastructure interacts with fraud detection, our post on payment gateway strategy for banking operations heads covers the infrastructure dependencies worth understanding before evaluating platform integration complexity.

False Positive Rate Fraud Detection

False positives fraud detection performance is the metric vendors most often gloss over in sales presentations. Every platform will show precision numbers from their best-performing customers. Ask instead for median false positive rates across their community bank customer base. The benchmark achievable with a well-configured AI platform: below 30% false positive rate within 90 days, and below 20% after six months of model calibration. Rule-based systems typically sit at 85-95%.

Also ask for false positive rate by institution size. A platform performing at 15% for national banks may perform at 40% for community banks if the models were not calibrated on institutions with your customer behavior profile.

Reducing False Positives: A Compliance Team's Priority

False positives are not just operational noise. They are a direct cost driver, a compliance risk when real fraud is buried under alert volume, and a customer experience problem when legitimate transactions get blocked. For most community banks, the false positive cost fraud generates annually exceeds total actual fraud losses, though very few institutions calculate that number explicitly.

How to Reduce False Positives in AML

How to reduce false positives in AML starts with measurement. Most community banks cannot state their current false positive rate because they have not tracked alert dispositions systematically. Pull six months of alert data, count confirmed fraud versus false positives, and calculate your baseline rate before evaluating any new platform.

Four practical steps to reduce false positives transaction monitoring, applicable regardless of which platform you choose:

- Retire stale rules: Rules accumulated without review are a primary false positive source. Any rule that has not generated a confirmed fraud case in 12 months deserves review and probable retirement.

- Implement risk-scored alert tiers: High-confidence alerts go to the front of the analyst queue; borderline cases go to a review batch. This reduces effective false positive exposure without changing the underlying detection logic.

- Close the feedback loop: Analyst dispositions, fraud confirmed, false positive, should feed back into the detection model. This is where AI systems compound their advantage over rule-based systems over time.

- Segment thresholds by customer type: Retail, small business, and commercial customers have fundamentally different transaction behaviors. A global threshold calibrated for retail generates excessive alerts on business accounts and vice versa.

Our post on reducing false positives with AI-driven solutions covers the implementation approach for each step in detail, including how to measure the impact of threshold changes before rolling them to production.

Reduce False Positives Transaction Monitoring: The Business Case

The business case is quantifiable in ways that move budget conversations forward. A community bank with four fraud analysts, 500 daily alerts, and a 90% false positive rate spends roughly 23 hours per day reviewing legitimate activity. At $75,000 fully-loaded annual cost per analyst, that is approximately $200,000 per year spent on noise.

Cut that false positive rate to 25% and you free three of those four analysts for genuine fraud investigation, SAR preparation, and customer-level risk analysis. The platform cost, typically $3,000-$8,000 per month, pays for itself in analyst hours within the first 12 months, before counting fraud losses prevented by more accurate detection.

The framing that moves budgets: this is not a compliance technology upgrade. It is a workforce efficiency investment with a measurable payback period any CFO can validate.

Onboard Customers in Seconds

Conclusion

Fraud detection platforms community banks evaluate in 2026 are substantially more capable and affordable than what was available three years ago. Sardine and Alloy lead on account opening fraud and synthetic identity detection. Unit21 and Hawk AI lead on AML workflow, SAR management, and analyst self-sufficiency. Featurespace is the right choice for banks with card fraud as a primary exposure and engineering capacity to support implementation.

The honest reality about ai fraud detection in banking: no platform reaches its performance potential without a calibration period and clean historical data. Set realistic expectations with your leadership, 60-90 days of model tuning before judging performance, and a clear baseline on your current false positive rate and transaction monitoring cost before signing anything.

For community banks ready to move past rule-based systems, evaluating fraud detection software built specifically for mid-market financial institutions is the practical next step. The technology has matured, the pricing has come down, and the operational case is clear.

Share this article