.webp)

Listen To Our Podcast🎧

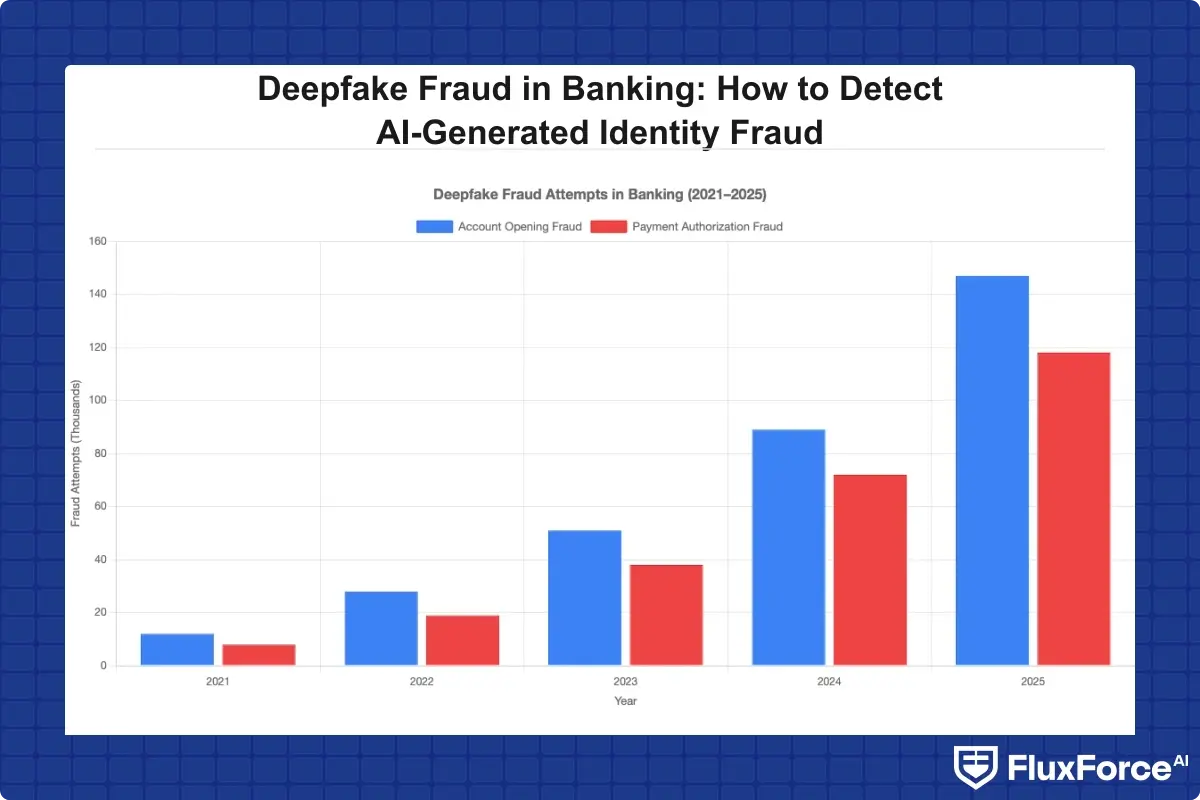

Deepfake fraud banking detection is no longer a future-state concern. In 2024, financial institutions reported a 700% year-over-year increase in deepfake-based identity fraud attempts, with attackers using AI-generated faces and voices to pass video KYC checks, open fraudulent accounts, and authorize high-value transfers. For CISOs, compliance officers, and fraud operations teams, this shift requires a fundamental rethink of how identity is verified and how AI-generated threats are caught before they cost the institution. This guide breaks down how deepfake attacks work, where traditional defenses fail, and what ai fraud detection in banking actually looks like when built to handle generative AI threats.

What Is Deepfake Fraud in Banking?

Deepfake fraud refers to the use of AI-generated or AI-manipulated media, including video, audio, images, and documents, to impersonate a legitimate individual during banking processes. The most common attack vectors include video KYC spoofing, voice-cloned phone authentication, AI-generated identity documents, and synthetic face injection into liveness detection checks.

Unlike traditional identity fraud, where a stolen document or account credential is the primary tool, deepfake attacks create convincing synthetic representations of real or fictional people. This makes rule-based detection nearly useless because the fraud artifact genuinely looks authentic to both humans and older automated systems.

According to the Financial Crimes Enforcement Network (FinCEN), identity-related fraud is the leading precursor to money laundering and financial crime across U.S. financial institutions. Deepfake technology lowers the barrier to entry for these schemes considerably.

How Deepfakes Bypass Traditional Identity Checks

Standard liveness detection asks a user to blink, turn their head, or smile. Early versions of this technology were defeated by replaying a pre-recorded video. Modern deepfake toolkits now generate real-time synthetic faces that respond to liveness prompts dynamically, making the threat far harder to catch at the point of onboarding.

Voice authentication faces the same problem. With as little as three seconds of recorded audio, commercially available AI tools can clone a person's voice convincingly enough to defeat voiceprint-based authentication. Several European banks reported voice-cloning attacks in 2023 that successfully authorized transfers by impersonating verified customers.

The Scale of the Deepfake Threat in Financial Services

The NIST AI Risk Management Framework flags generative AI misuse as a top-tier risk category for critical infrastructure, which includes banking and financial services. Industry estimates put deepfake-related financial losses at over $25 billion globally in 2023, a figure expected to triple by 2027 as the cost of generating convincing deepfakes falls toward zero.

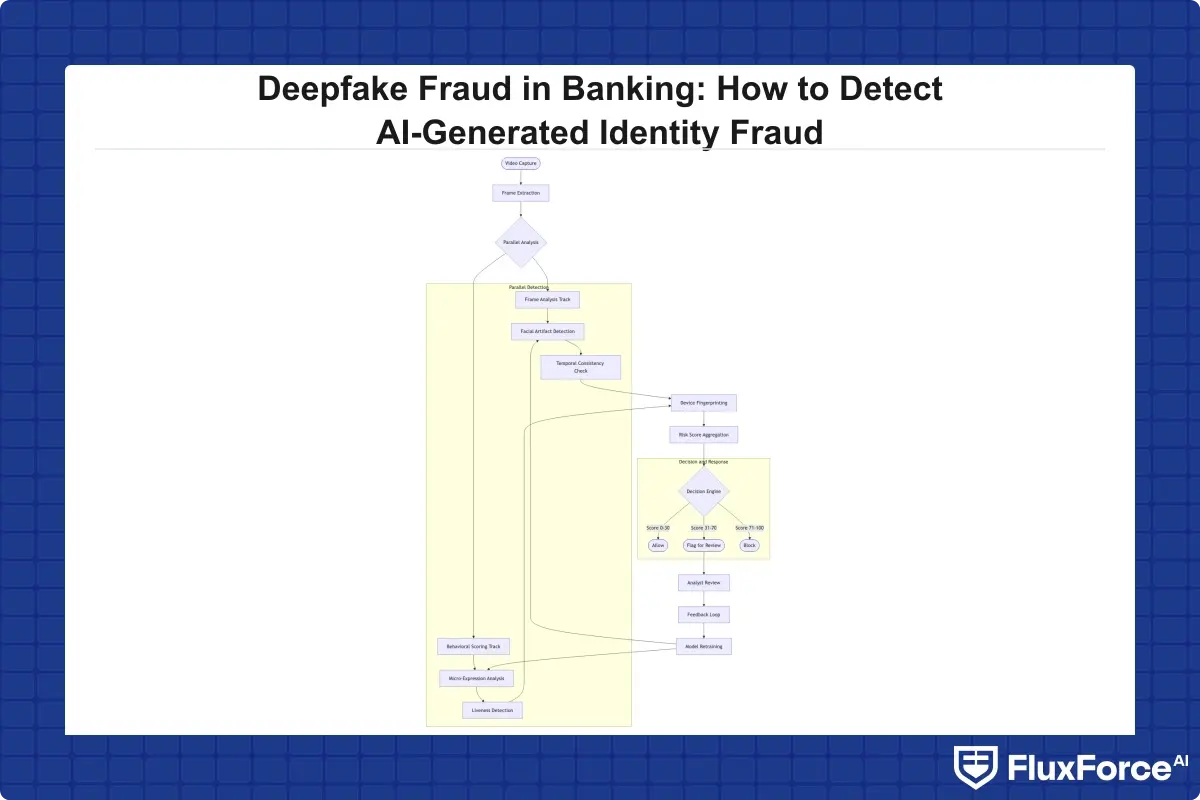

How AI Fraud Detection Works Against Deepfake Attacks

How does AI detect fraud differently from a rule-based system? AI fraud detection explained simply: instead of matching transactions against fixed rules, machine learning models learn the statistical patterns of fraudulent behavior and score every event against those learned patterns in real time. AI fraud detection in banking applies this approach across identity verification, behavioral signals, and transaction events simultaneously.

Where a rule-based system checks "does the face match the ID photo?", an AI system asks "does the behavioral pattern of this onboarding session match any known-good user cohort, and are there micro-inconsistencies in the video stream suggesting synthetic generation?" That difference in question is the difference between catching 20% of deepfakes and catching 80%.

Machine Learning Fraud Detection Models

Machine learning fraud detection relies on anomaly detection, classification models, and graph analysis working together. For deepfake detection specifically, the relevant model types include:

- Artifact detection models that look for compression artifacts, unnatural lighting gradients, and edge inconsistencies around facial boundaries characteristic of GAN-generated images.

- Behavioral biometric models that track mouse movement speed, keypress cadence, scroll patterns, and session duration against known-good baselines for real human users.

- Graph network analysis that maps relationships between account identifiers, devices, IP addresses, and phone numbers to surface identity clusters suggesting synthetic identity fraud at scale.

The honest answer is that no single model catches every deepfake. The combination matters more than any individual algorithm, and institutions that treat deepfake defense as a single-point problem consistently underperform those that layer signals.

Real-Time Fraud Detection in Banks

Real time fraud detection is the operational requirement that separates effective deepfake defense from theoretical defense. A video KYC session lasts three to five minutes. If the AI system takes 20 minutes to flag an anomaly, the fraudulent account is already open.

Modern real time fraud detection banks deploy models at inference endpoints with sub-100ms response times. These models score each frame of a video stream, each authentication event, and each form interaction in parallel, surfacing risk scores before the session concludes. This is a fundamentally different architecture than batch-mode fraud review and requires transaction monitoring software capable of ingesting streaming event data rather than processing end-of-day files.

Behavioral Biometrics and Liveness Detection

The most effective anti-deepfake layer in current ai fraud detection software is passive behavioral biometrics combined with next-generation liveness detection. Passive liveness does not ask the user to perform an action. Instead, it analyzes the micro-movements present in a real human face, including involuntary eye movement, subtle skin texture changes, and pulse-visible color variation, all of which are absent in a synthetic face.

The Gartner Market Guide for Identity Verification consistently lists passive liveness as a required capability for financial institutions conducting video-based identity verification. Institutions still relying on active liveness alone face a significant detection gap against current-generation deepfake tools that can dynamically respond to prompted actions.

Why Traditional Transaction Monitoring Software Falls Short

Most banks still run transaction monitoring on rule-based systems built in the 2000s and 2010s. These systems were designed to catch wire fraud, check kiting, and structured cash deposits. They were not built to detect the behavioral signatures of an AI-generated identity completing its first transaction.

The result is a dual failure: deepfake accounts slip through because the patterns do not trigger existing rules, while legitimate customers get flagged at high rates because the rules are poorly calibrated. Both failures are expensive, and the combination creates an environment where fraud alert fatigue makes genuine threat detection even harder over time.

The Problem of Fraud Alert Fatigue

Fraud alert fatigue is what happens when analysts receive so many low-quality alerts that they begin to treat all alerts as noise. In a 2023 survey of compliance teams at U.S. mid-size banks, analysts reviewed an average of 400 alerts per day with a true positive rate under 5%. At that ratio, missing a genuine deepfake attack is nearly inevitable, not because of incompetence but because the volume makes careful review impossible.

This is not a staffing problem that more analysts can solve. It is a signal quality problem that only better ai fraud detection software can address. As covered in our analysis of how agentic AI cuts false positives by 80%, reducing alert volume through smarter triage is achievable today with the right architecture, without increasing missed fraud rates.

False Positive Rate Fraud Detection Issues

The false positive rate fraud detection generates is a direct cost driver. Each false positive requires analyst time to investigate, risks customer relationship damage if a legitimate transaction is blocked, and consumes operational budget that could go toward genuine threat response.

False positives fraud detection creates at scale also mask the signal from real attacks. When the noise-to-signal ratio exceeds 20:1, deepfake fraud accounts can conduct multiple fraudulent transactions before the pattern becomes statistically distinguishable from the background noise of false positives.

Transaction Monitoring Cost Implications

Transaction monitoring cost is not just the software license fee. It includes analyst labor (typically $60,000 to $120,000 per analyst per year in U.S. markets), regulatory penalty risk from missed Suspicious Activity Reports, and the opportunity cost of declined legitimate transactions.

A bank processing 10 million transactions per month with a 0.5% false positive rate generates 50,000 alerts monthly. At 15 minutes per alert, that is 12,500 analyst hours. Automated transaction monitoring with an AI triage layer can reduce that to 1,000 to 2,500 hours monthly, freeing investigators to focus on genuine threats including deepfake fraud banking detection cases that require human judgment.

How to Reduce False Positives in AML Without Missing Real Threats

How to reduce false positives in AML is the practical question every compliance officer should ask before selecting a fraud platform. The answer involves three distinct changes: better feature engineering, contextual risk scoring, and feedback loops that let the model learn from analyst decisions over time.

Reduce False Positives in Transaction Monitoring

Reduce false positives transaction monitoring by moving from threshold-based rules to probabilistic risk scores. Instead of flagging every transaction over $10,000 from a new account, a machine learning model scores the transaction against dozens of features: account age, device fingerprint consistency, session behavior, network velocity, and peer group norms for similar accounts.

The comparison of rule-based versus AI-driven approaches makes this concrete: rule-based systems optimize for recall (catching all fraud), often at the expense of precision. AI systems can balance both simultaneously, which is why the false positive rate drops sharply when institutions make the transition from legacy rule engines to machine learning scoring.

False Positive Cost Fraud Impact on Operations

False positive cost fraud teams face breaks down into three categories:

- Direct investigation cost: analyst time per alert, typically 10 to 30 minutes per case

- Customer friction cost: declined transactions average $32 in goodwill cost plus potential account closure

- Regulatory exposure: under-reported genuine fraud creates SAR filing gaps that attract regulator scrutiny

A realistic calculation for a mid-size bank shows that reducing the false positive rate fraud detection generates from 95% to 80% (still industry-average) saves approximately $2 to $4 million annually in analyst labor alone, before accounting for regulatory and customer retention benefits.

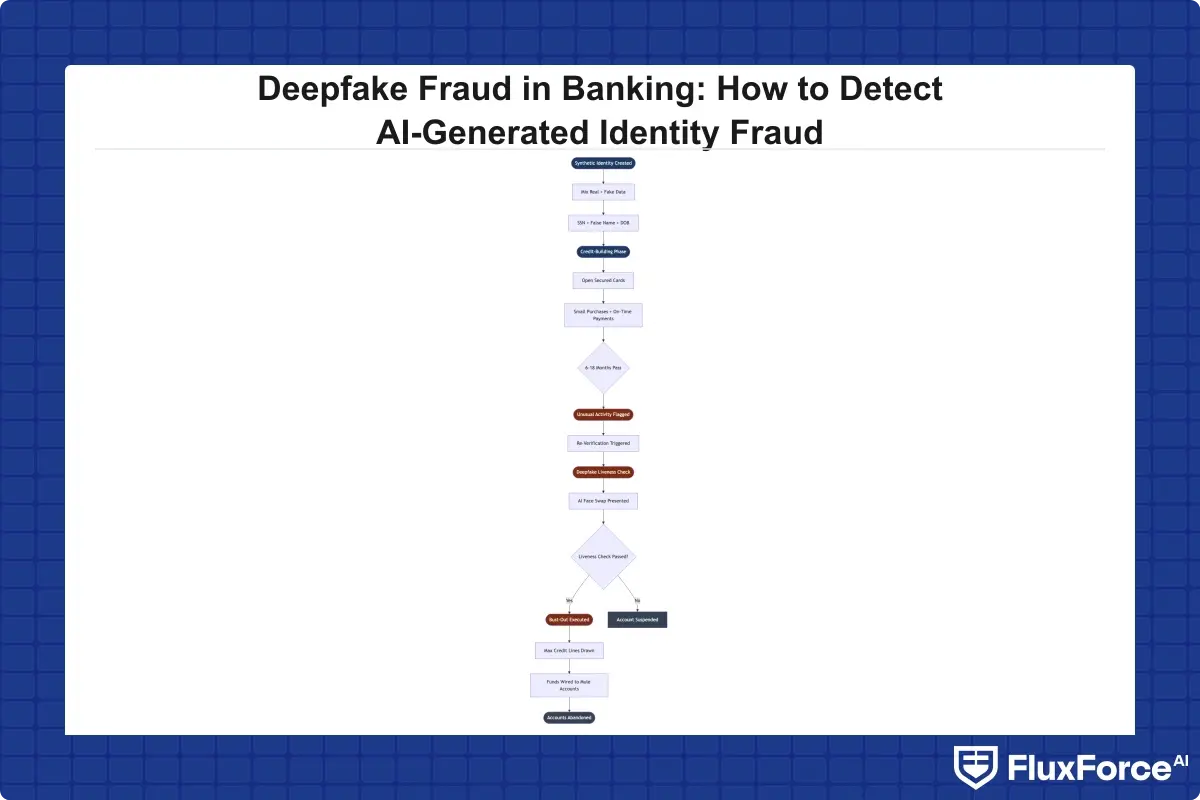

Synthetic Identity Fraud and Its Connection to Deepfakes

Synthetic identity fraud uses a combination of real and fabricated personal information to create a new identity that does not correspond to any real person. Deepfake technology adds a visual and biometric layer on top of this fabricated identity, making it possible to pass video verification that synthetic identity attacks previously could not defeat.

The combination is particularly dangerous for credit issuance and new account opening. A synthetic identity with a fabricated Social Security number and a deepfake video presentation can now pass identity verification at institutions relying primarily on document and biometric checks. Understanding how these attack types intersect is critical for KYC and AML verification strategy teams building layered defenses, because each layer alone is insufficient against a well-resourced adversary.

How Synthetic Identities Enable Deepfake Account Takeover

Account takeover via synthetic identity follows a predictable pattern: the fraudster builds credit history on the synthetic identity over six to eighteen months (known as bust-out fraud), then uses a deepfake to pass re-verification when the account is flagged for unusual activity. By the time fraud is confirmed, the account has drawn down a line of credit or moved funds to mule accounts.

Real time fraud detection at the re-verification stage, specifically checking for behavioral inconsistencies between the original onboarding session and the current session, is one of the most effective catches for this pattern. Institutions that store session-level behavioral baselines from onboarding have a meaningful detection advantage over those that treat re-verification as a one-time biometric check.

Payment Fraud Prevention in the Age of AI-Generated Attacks

Payment fraud prevention now requires that every payment event be scored in the context of the identity behind it, not just the transaction characteristics. A $500 wire transfer from an account with a deepfake-verified identity carries a fundamentally different risk profile than $500 from an account with ten years of consistent transaction history.

This is where real AI-based fraud detection software differs from theoretical models: effective systems propagate identity risk scores from the verification layer into transaction monitoring, so every payment event from a deepfake-verified account carries an elevated prior that the transaction model factors into its scoring. Understanding what AI fraud detection in banking actually detects requires looking at this cross-layer architecture, not just individual point solutions for biometrics or transaction screening.

Automated Transaction Monitoring for Deepfake Scenarios

Automated transaction monitoring for deepfake scenarios requires event streams from the identity verification layer, not just the payment ledger. When a video KYC session is flagged as moderate risk (say, 60% confidence of synthetic face generation), that risk score should propagate to every transaction event on the resulting account for at least the first 90 days.

Most current transaction monitoring software operates in silos. The KYC system passes or fails an identity check, and the transaction monitoring system then treats the resulting account as clean regardless of how close the KYC call was. Closing this silo is one of the highest-value architectural changes a bank can make to its fraud stack against AI-generated identity attacks.

What Does Effective AI Fraud Detection Software Look Like?

Effective AI fraud detection software for deepfake scenarios does five things: it ingests multi-modal signals including video, behavioral, transactional, and network data; it provides real-time scoring rather than batch review; it maintains a feedback loop between analyst decisions and model training; it integrates with existing transaction monitoring software without requiring a full stack replacement; and it produces explainable risk scores that analysts can act on and defend to regulators.

The last point matters more than it gets credit for. If a compliance officer cannot explain to a regulator why an account was flagged or cleared, the AI system creates audit liability rather than reducing it. Explainability is not a nice-to-have for financial institutions operating under BSA/AML examination standards.

Sardine vs Unit21: Which Handles Deepfakes Better?

Sardine vs Unit21 is a common evaluation question for institutions building out their fraud stack. Both platforms offer ai fraud detection capabilities, but their approaches differ in meaningful ways.

Sardine is built around device and behavioral intelligence collected at the session level. It excels at detecting automated and scripted sessions characteristic of deepfake injection attacks, where the biometric input is not coming from a real user interacting naturally with a device. Its signal density at the session layer is a genuine differentiator for account-opening fraud scenarios.

Unit21 is built around rule orchestration and case management sitting on top of transaction data. It is strong for AML alert management and false positive reduction in transaction monitoring contexts, but it relies on partner integrations for biometric and liveness-layer signals rather than generating them natively.

Neither platform is a complete deepfake solution out of the box. The honest evaluation: choose Sardine first if deepfake account opening is your primary risk, and Unit21 first if transaction monitoring cost and alert volume are your primary pain points. Most large institutions need both capabilities or a platform that genuinely integrates both the identity and transaction layers.

Key Capabilities to Evaluate in AI Fraud Detection Software

When evaluating ai fraud detection software specifically for deepfake scenarios, score vendors on these five criteria:

- Native passive liveness detection or a certified partner integration with a published accuracy benchmark

- Sub-100ms real-time scoring at the authentication event level, not just the transaction level

- Cross-channel risk score propagation where KYC risk is visible in transaction monitoring from day one

- Analyst feedback loops for continuous model improvement as the fraud landscape evolves

- Explainable AI output satisfying BSA/AML examination standards in your jurisdiction

For risk heads evaluating their full fraud program architecture, consider how these ai fraud detection software capabilities sequence across identity, behavioral, and transactional investment layers to provide defense in depth rather than isolated point solutions.

Onboard Customers in Seconds

Conclusion

Deepfake fraud banking detection is one of the hardest problems in financial services today because the attack surface is identity itself. The tools that worked a decade ago, document verification, knowledge-based authentication, and rule-based transaction monitoring software, were not built for AI-generated threats that respond dynamically to liveness prompts and can clone a voice from three seconds of audio.

The path forward requires ai fraud detection operating across layers: passive liveness at onboarding, behavioral biometrics during session, real time fraud detection at the payment event, and automated transaction monitoring that carries identity risk scores forward into the account lifecycle. Reducing false positives fraud detection generates is not a trade-off with security; it is what makes genuine deepfake detection operationally viable by ensuring analysts focus on real signals rather than noise.

If your institution is evaluating its deepfake readiness, start with an honest assessment of where your KYC and transaction monitoring stacks share data and where they operate in silos. That gap is where deepfake attacks consistently find their footing, and closing it is the first concrete step toward a defense that holds against AI-generated identity fraud.

Share this article