.webp)

Listen To Our Podcast🎧

Adverse media screening automation is no longer a nice-to-have for regulated firms; it is the difference between catching a high-risk customer before onboarding and explaining to a regulator why you missed an obvious red flag. Every bank, fintech, insurer, and supply-chain operator that touches money or identity has to know who they are dealing with, and negative news is one of the earliest warning signals available. The problem is that manual screening drowns analysts in noise. This guide explains why adverse media screening matters, where manual processes break, and how to automate it without losing control of your risk decisions or your aml compliance obligations.

What Is Adverse Media Screening and Why It Matters

Adverse media screening is the process of searching news, regulatory notices, court records, and other public sources for negative information about a customer, supplier, or counterparty. The goal is to surface links to financial crime, fraud, corruption, sanctions evasion, or other reputational risks before they become your problem.

Adverse media screening is the practice of monitoring public and licensed data sources for negative information that signals financial crime risk tied to a person or entity. Under a strong aml compliance program, it sits alongside sanctions checks and watchlist screening as part of customer due diligence.

Why negative news belongs in your AML program

Regulators expect adverse media checks as part of a risk-based approach. The Financial Action Task Force (FATF) recommendations on a risk-based approach make clear that firms must understand the risk a customer presents, and negative news often reveals risk that no watchlist has caught yet. A person can be named in a money-laundering investigation years before any formal sanction or enforcement action appears.

For aml compliance fintech teams especially, adverse media is where emerging threats show up first. A founder linked to a collapsed exchange, a supplier tied to forced-labor reporting, a merchant named in a fraud ring; these stories break in the press long before they reach an official list.

How adverse media differs from sanctions screening

Sanctions screening matches against defined government lists. Adverse media screening is broader and messier: it scans unstructured news content where names are spelled inconsistently, context is ambiguous, and false matches are common. The two are complementary, which is why a complete bsa aml compliance checklist treats them as separate but linked controls. For deeper context on list-based controls, our breakdown of sanctions screening automation for compliance teams covers the watchlist side in detail.

Why Manual Adverse Media Screening Breaks Down

Most compliance teams start with manual searches: an analyst types a name into a search engine or a data provider, reads through results, and makes a judgment call. This works at low volume. It collapses at scale.

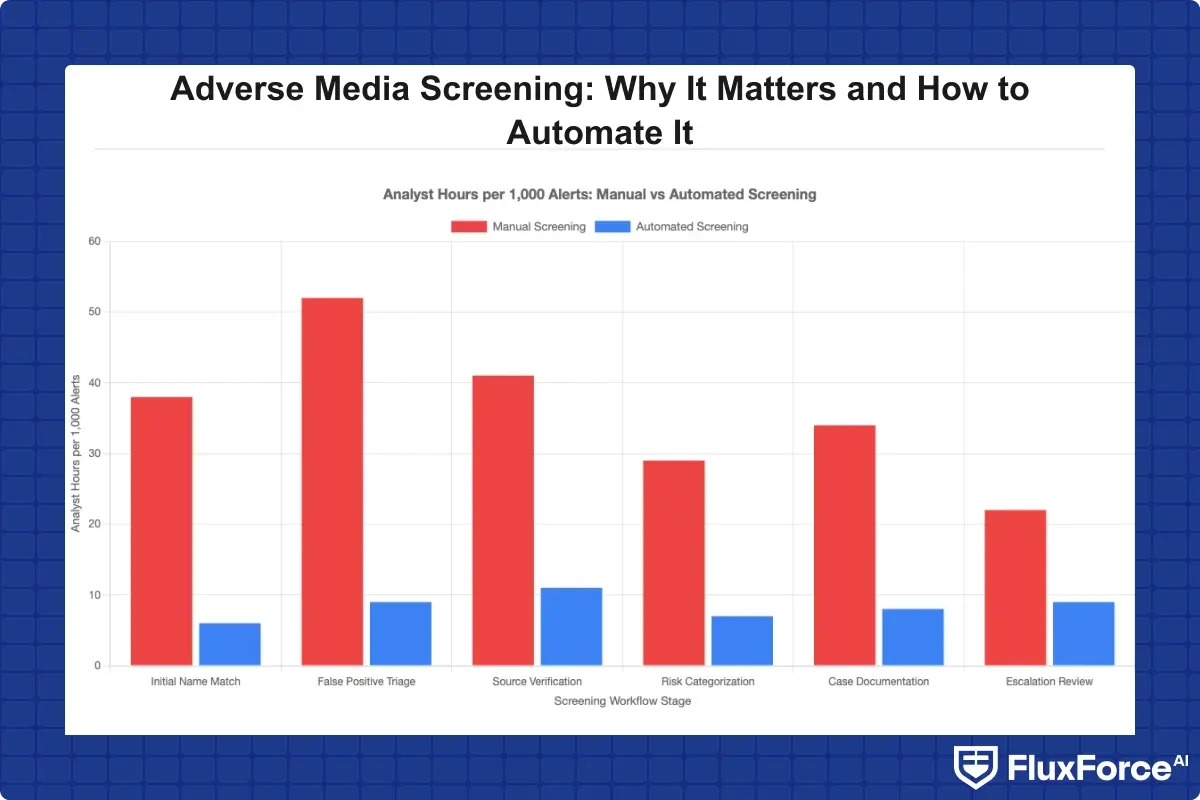

The false positive problem in transaction monitoring and screening

Common names generate hundreds of irrelevant hits. An analyst screening "John Martin" has to read through unrelated articles about athletes, politicians, and namesakes before finding the one that matters, if it exists at all. Industry estimates routinely put false positive rates in name-screening systems above 90 percent, which means analysts spend most of their day clearing noise. We covered the mechanics of this in our piece on reducing false positives with rule-based versus AI-driven systems.

Why small teams struggle most

A fintech bsa aml small team rarely has the headcount to screen every customer continuously. They screen at onboarding, then move on. The result is stale risk profiles: a customer who was clean at signup but got named in a fraud case six months later goes unnoticed until a transaction triggers a review. For bsa aml compliance community banks face the same constraint with even tighter budgets, which is why anti money laundering technology has become a survival tool rather than a luxury.

Inconsistent decisions and weak audit trails

Manual screening produces inconsistent outcomes. Two analysts reviewing the same hit may reach different conclusions, and neither documents their reasoning in a way that survives a regulator's scrutiny. When examiners ask why a match was cleared, "the analyst judged it irrelevant" is not a defensible answer. A proper aml risk assessment guide stresses that every decision needs a recorded rationale, and manual workflows rarely deliver that consistently.

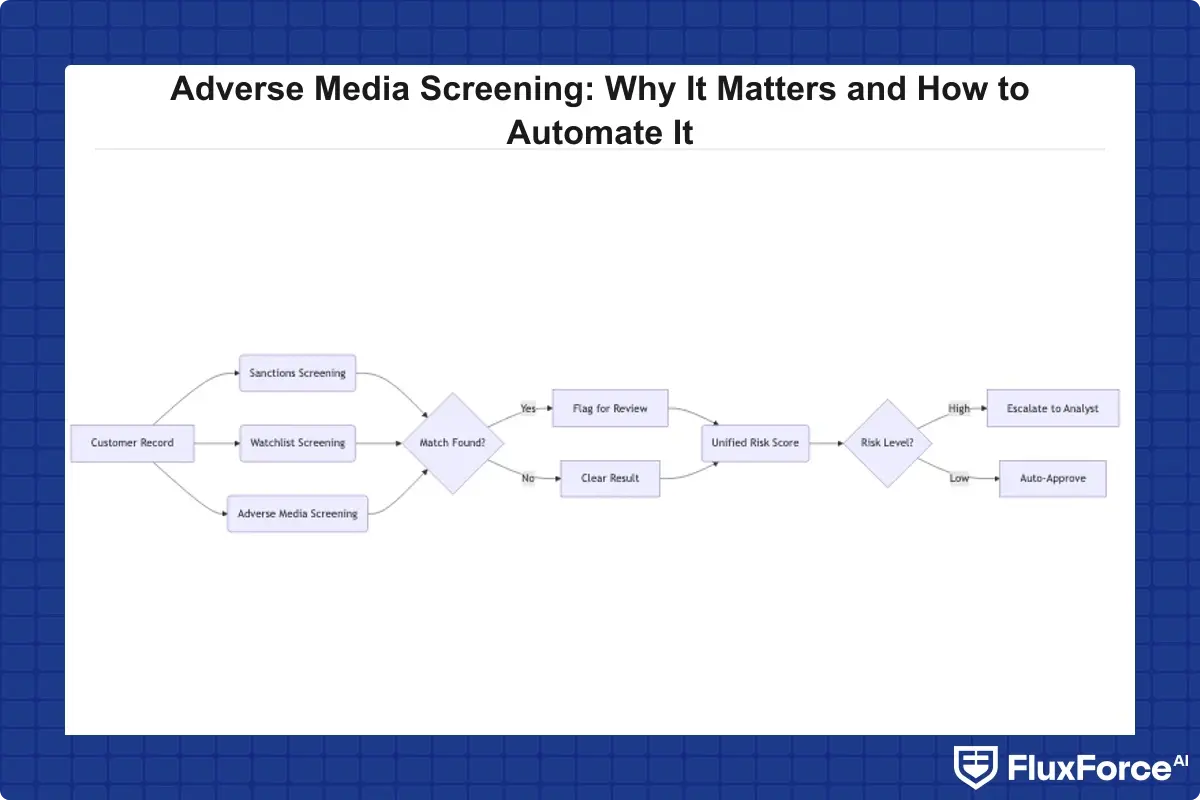

How to Automate Adverse Media Screening

Automation does not mean removing human judgment. It means letting software handle the volume, the matching, and the documentation so analysts focus on genuine risk. Here is how adverse media screening automation works in practice.

Step 1: Aggregate and structure your data sources

Start by connecting licensed news feeds, regulatory databases, court records, and structured risk data into one pipeline. Quality matters more than quantity; a few authoritative sources beat scraping the open web. Strong kyc automation depends on clean, deduplicated input.

Step 2: Apply entity resolution and contextual matching

This is where modern anti money laundering technology earns its keep. Instead of crude string matching, machine learning models resolve entities by cross-referencing dates of birth, locations, known associates, and roles. The system distinguishes the high-risk "John Martin" from the thousands of irrelevant ones, cutting false positives dramatically. Our analysis of how agentic AI cut false positives by 80 percent shows what contextual matching achieves at scale.

Step 3: Score, prioritize, and route alerts

Automated systems assign a risk score to each genuine match and route it to the right reviewer. A high-confidence link to an active investigation jumps the queue; a weak, dated mention drops down. This is the core of effective adverse media screening automation, and it is where building a defensible workflow around regulatory compliance automation pays off across your whole program rather than one isolated check.

Step 4: Enable continuous monitoring, not one-time checks

The biggest gain from automation is moving from point-in-time screening to continuous monitoring. The system rescreens your entire customer base against new media daily, so a customer who becomes risky after onboarding triggers an alert the next morning. This directly supports kyc cdd requirements banks must meet on an ongoing basis.

Connecting Adverse Media to SAR Filing and Reporting

Screening is only valuable if it feeds your reporting obligations. When adverse media confirms suspicious activity, it should flow directly into your suspicious activity report process.

How automation improves SAR filing efficiency

Manual SAR preparation is slow because analysts reconstruct the case from scattered notes. Automated screening attaches the source articles, the match rationale, and the risk score to the customer record, so the SAR narrative writes itself faster. This is real sar filing efficiency: the evidence trail is already assembled. Teams following sar filing best practices use this captured context to meet sar filing requirements 2026 examiners increasingly expect.

CTR filing rules and the bigger reporting picture

While adverse media feeds suspicious activity reporting, automation also helps firms stay aligned with ctr filing rules by maintaining accurate, current customer profiles that inform transaction thresholds. A complete suspicious activity report guide treats screening, monitoring, and reporting as one connected chain rather than separate tasks. For firms modernizing the reporting side, our overview of banking compliance reporting and automation connects these dots.

Documentation that survives an audit

The U.S. Treasury's FinCEN sets clear expectations for SAR filing and recordkeeping, and automated audit trails make compliance far easier to demonstrate. Every cleared alert, every escalation, and every decision is timestamped and attributed.

Choosing AML Compliance Software for Adverse Media

Not every platform handles adverse media well. When evaluating aml compliance software, weigh these factors against your risk profile and team size.

What to look for in a platform

- Contextual matching that reduces false positives rather than just flagging every name hit

- Continuous monitoring rather than one-time batch screening

- Configurable risk scoring you can tune to your appetite

- Audit-ready logging that records every decision automatically

- Integration with your existing KYC, case management, and SAR systems

Why fit matters more than feature count

A platform built for a global bank may overwhelm a fintech bsa aml small team with configuration overhead. Conversely, a lightweight tool may not satisfy the bsa aml compliance community banks need for examiner scrutiny. Match the tool to your actual volume and risk, following an enhanced due diligence guide for your highest-risk segments. Insurers and supply-chain firms have parallel needs; our KYC/AML verification strategy for insurance compliance officers shows how the same principles apply outside banking.

Preparing for AI regulation

As you adopt AI-driven screening, governance matters. The eu ai act financial services provisions classify many risk-scoring systems as high-risk, requiring transparency and human oversight. The European Commission's guidance on the EU AI Act is essential reading before deploying any black-box model. Plan for explainability now, because anti money laundering technology 2026 buyers will demand it and regulators will require it.

How Adverse Media Screening Fits a Modern Compliance Stack

Adverse media screening automation works best as one layer in a connected program, not a standalone tool. It feeds KYC, informs transaction monitoring, and triggers SAR workflows.

Building toward kyc automation 2026

The direction of travel is clear: kyc automation 2026 will combine identity verification, continuous adverse media monitoring, and behavioral analytics into a single risk view. Firms still treating these as separate manual steps will fall behind on both cost and detection. Our guide to rolling out compliance agents in 90 days outlines a realistic adoption path.

A practical bsa aml compliance checklist

Use adverse media automation to tick off recurring items on your bsa aml compliance checklist: ongoing customer monitoring, documented risk decisions, timely escalation, and retrievable audit trails. Each of these becomes far less painful when the system handles them automatically.

Onboard Customers in Seconds

Conclusion

Adverse media screening automation has shifted from optional to essential for any firm serious about aml compliance. Manual screening cannot keep pace with the volume of negative news, the false positive burden, or the documentation that regulators now expect. By aggregating quality data, applying contextual matching, scoring alerts intelligently, and monitoring continuously, you turn a reactive chore into a proactive control that feeds directly into sar filing and reporting. Whether you are a community bank, an insurer, or a fintech bsa aml small team, the path forward is the same: automate the noise, keep the judgment, and document everything. Review your current screening process this quarter, identify where manual gaps create risk, and build a roadmap toward continuous, audit-ready adverse media screening.

Share this article