.webp)

Listen To Our Podcast🎧

The BSA officer responsibilities guide most compliance teams are working from was built for a simpler era. In 2026, the role demands active oversight across transaction monitoring, SAR filing, KYC automation, and vendor governance, all while FinCEN and federal examiners have raised the bar on what "reasonable" compliance looks like.

Whether you're the sole BSA officer at a community bank or leading a ten-person team at a fintech, this guide gives you a current, practical framework for every pillar of the role.

What Does a BSA Officer Actually Do?

The Bank Secrecy Act, enacted in 1970 and significantly expanded by the USA PATRIOT Act in 2001, requires every covered financial institution to designate a BSA compliance officer. The role is a legal requirement, not a title. That distinction matters because your institution can't delegate the accountability, only the tasks.

In practice, the BSA officer owns five interconnected responsibilities: building and maintaining the AML compliance program, filing regulatory reports (SARs and CTRs), overseeing KYC and CDD processes, managing staff training, and coordinating independent testing. How much time you spend on each depends heavily on your institution's size and risk profile.

The Five Core Pillars of the BSA Officer Role

1. AML Program Development and Maintenance. You're responsible for drafting, updating, and enforcing the written AML compliance program that satisfies the "four pillars" required under FinCEN regulations: internal controls, independent testing, designated officer, and training.

2. Regulatory Reporting. SAR filing and CTR filing rules are your direct ownership. Errors here attract examiner scrutiny faster than almost anything else.

3. Customer Due Diligence. This includes KYC onboarding, ongoing monitoring, and enhanced due diligence for high-risk customers. The 2016 FinCEN CDD Rule added beneficial ownership as a fifth requirement.

4. Training and Culture. Annual training for all staff, role-specific modules for frontline employees, and board-level reporting are all part of the job.

5. Independent Testing Coordination. You don't run the audit, but you own the relationship with the auditors and the remediation of findings.

Reporting Lines, Authority, and Organizational Independence

One question that comes up in nearly every regulatory exam: who does the BSA officer report to? The FFIEC BSA/AML Examination Manual is clear that the officer should have sufficient authority and independence to escalate concerns without interference from line-of-business management. In most banks, that means reporting directly to the board or a senior executive outside revenue-generating functions.

At fintechs and smaller institutions, the BSA officer sometimes reports to the CFO or General Counsel. That arrangement isn't automatically a problem, but examiners will probe whether the officer can truly act independently when business interests conflict with compliance requirements. For fintech bsa aml small team situations, the reporting structure question matters even more because the compliance function is often one person, and their independence is harder to demonstrate.

At a community bank with under $500M in assets, one BSA officer often handles everything with a single analyst. At institutions over $1B, you'd expect a full BSA/AML team with dedicated transaction monitoring analysts, a CDD/KYC unit, and a separate reporting function. The resource gap between these two scenarios is exactly why aml compliance software investment has accelerated across smaller institutions.

BSA AML Compliance Checklist for 2026

A workable bsa aml compliance checklist is one of the most practical tools a BSA officer has. Below are the program elements examiners will verify in any safety and soundness exam.

Program Requirements Under 31 U.S.C. § 5318

FinCEN's core requirements haven't changed structurally, but examiner expectations around documentation, testing, and technology governance have increased sharply since 2022. Your program must include:

- A written AML policy approved by senior management or the board

- Internal controls that are risk-based and specific to your institution's profile

- Independent testing at least every 12-18 months (annually for higher-risk institutions)

- A designated BSA compliance officer with documented authority

- Ongoing employee training with attendance records

- Customer due diligence procedures meeting the 2016 CDD Rule, including beneficial ownership verification for legal entity customers

Annual Review and Record-Keeping Standards

Every element of your program needs to be reviewed at least annually, and updated when your institution's risk profile changes materially: new products, new markets, new ownership. FinCEN's advisory notices are a reliable source for emerging typologies to incorporate into your annual review.

Record-keeping requirements generally run five years for most BSA records. CTRs, SARs, and supporting documentation have their own retention schedules, so verify the current requirements before setting your document management policy. Exam findings for record-keeping deficiencies are common and avoidable.

SAR Filing Requirements and Best Practices

The suspicious activity report guide most officers work from covers mechanics, but not judgment. SAR filing is ultimately a judgment call, and regulators have made clear in recent enforcement actions that "when in doubt, file" is the safer posture.

SAR Filing Thresholds and Timelines

SAR filing requirements 2026 remain largely consistent with prior years. Under 31 CFR 1020.320, banks must file a SAR for transactions of $5,000 or more where they know, suspect, or have reason to suspect the transaction involves funds from illegal activity. The threshold is $2,000 for certain transaction types, and money services businesses operate under their own thresholds.

On timing: SAR filing must occur within 30 calendar days of initial detection of a reportable transaction. If no suspect is identified at detection, you have 60 days. Late filings are technical violations, so tracking your detection-to-filing cycle time as a program KPI is worth building into your reporting metrics.

SAR Filing Efficiency and Narrative Quality

Manual SAR preparation is a real bottleneck. A single complex SAR narrative can take 4-6 hours to prepare properly. Multiplied across dozens of filings monthly, that's a significant resource drain. SAR filing efficiency improves substantially when transaction monitoring platforms are configured to auto-populate SAR fields from alert data. This is similar to how agentic AI systems cut false positives in financial crime detection: automation handles data assembly, and humans focus on judgment.

Key sar filing best practices for stronger narratives:

- Follow the "who, what, when, where, why, how" structure for every narrative

- Keep descriptions factual, not conclusory

- Reference specific transaction dates, amounts, and account numbers

- Avoid jargon that FinCEN analysts won't recognize

A SAR committee or peer review process ensures filings aren't the single judgment of one analyst. A second reviewer catches errors and strengthens the defensibility of each filing decision.

CTR Filing Rules and Common Mistakes

Currency transaction reports cover cash transactions exceeding $10,000. The rules themselves are straightforward. The errors are not.

The $10,000 Threshold and Aggregation Requirements

The most common CTR error isn't missing a single large transaction. It's failing to aggregate multiple transactions by the same customer on the same business day. Two $6,000 deposits made at different branches by the same individual on the same day require a CTR. Tellers and frontline staff need specific training on this aggregation requirement because it's genuinely counterintuitive.

CTR filing rules also cover transactions conducted on behalf of another person. If a business owner sends an employee to make a deposit, the CTR must identify both the person conducting the transaction and the business entity on whose behalf it's made. Getting both fields accurate is a recurring exam finding at smaller institutions.

Structuring, which means deliberately breaking up transactions to stay below the $10,000 threshold, is a federal crime under 31 U.S.C. § 5324. Your monitoring controls need detection scenarios specifically for structuring patterns, not just for isolated large transactions.

CTR Exemptions and the FinCEN Exemption Process

Banks can reduce CTR filing volume by designating certain customers as exempt using FinCEN Form 110. The exemption categories cover government entities, listed companies (publicly traded on major exchanges), and non-listed businesses that meet specific criteria around transaction frequency and legitimate commercial activity.

Exemptions must be reviewed annually and properly documented. An exempt customer who begins showing unusual activity patterns may need their exemption revoked. Managing the exemption list is often overlooked at smaller institutions, but it appears regularly in examination findings.

KYC Automation and CDD Requirements for Banks

KYC cdd requirements banks have grown more complex since the 2016 FinCEN CDD Rule added beneficial ownership verification for legal entity customers. In 2026, the Corporate Transparency Act has added another layer: FinCEN's Beneficial Ownership Information database began accepting reports in January 2024, creating a reference point for verifying customer-provided ownership data against independent filings.

The Four CDD Requirements

FinCEN's CDD Rule requires covered financial institutions to:

- Identify and verify customer identity (standard KYC)

- Identify and verify beneficial owners of legal entities (the 2016 addition, 25% ownership threshold)

- Understand the nature and purpose of customer relationships to develop a risk profile

- Conduct ongoing monitoring to identify and report suspicious transactions, and update customer information when it changes

The fourth requirement is where most institutions still struggle. Customer risk profiles built at onboarding often go years without updates. Kyc automation 2026 addresses this with automated triggers: when a customer's transaction patterns deviate materially from their documented purpose, the system flags the account for review rather than waiting for a scheduled refresh.

Enhanced Due Diligence Guide for High-Risk Customers

The enhanced due diligence guide centers on four high-risk customer categories: politically exposed persons (PEPs), customers in high-risk geographies, entities with complex or opaque ownership structures, and cash-intensive businesses.

EDD isn't just collecting more documents. It's conducting a deeper investigation into the source of funds, the purpose of the relationship, and the expected transaction volume, then documenting those findings thoroughly enough to satisfy an examiner. For insurance companies, this maps directly to KYC and AML verification in policy issuance, where due diligence must be sustained across a multi-year customer relationship, not just performed at application.

Kyc automation tools that integrate with external data providers (sanctions lists, PEP databases, adverse media feeds) reduce the manual research burden for EDD substantially. Without automation, thorough EDD on high-risk customers is often done inconsistently because the time cost is prohibitive for most compliance teams.

How to Choose AML Compliance Software

Anti money laundering technology 2026 has matured considerably. The gap between best-in-class platforms and legacy transaction monitoring systems is widening in ways that directly affect exam outcomes. Examiners now ask not just whether you have transaction monitoring in place, but whether your system is calibrated to your risk profile, whether you're measuring false positive rates, and whether you have a documented tuning process.

Core Features to Evaluate in AML Compliance Software

When evaluating aml compliance software, these capabilities separate adequate from genuinely effective:

- Risk-based transaction monitoring with scenario libraries covering current FinCEN typologies

- Automated alert management with disposition workflows that create a complete audit trail

- SAR and CTR generation that pre-populates from alert data to improve sar filing efficiency

- KYC and CDD integration so customer risk profiles feed directly into monitoring thresholds

- Reporting dashboards that give senior management and the board real visibility into program metrics

- Model governance tools for documenting tuning decisions and demonstrating calibration to examiners

The shift toward regulatory compliance automation doesn't replace BSA officer judgment. It frees officers from manual data collection so they can focus on the cases that genuinely require human analysis.

Integration With Core Banking and Fintech Systems

Anti money laundering technology only works if it has clean, complete data. Integration with your core banking system, payment rails, and onboarding platform matters more than the sophistication of the monitoring engine itself. An AI-powered system fed incomplete or siloed data will produce worse alerts than a simpler rule-based system running on clean inputs.

For digital lenders and fintechs, this integration challenge is especially relevant. The compliance architecture for a digital-first institution looks different from a traditional bank's, particularly for AML screening in digital lending, where transaction velocity and product complexity create monitoring challenges that generic bank-oriented platforms often don't handle well.

BSA AML Compliance for Community Banks and Fintechs

BSA aml compliance community banks face a specific tension: FinCEN's expectations are substantively the same regardless of institution size, but the resources available to meet them are not. A $300M community bank is held to the same core standards as a $10B regional bank, just with a fraction of the team capacity.

Fintech BSA AML Small Team Challenges

Fintech bsa aml small team situations typically involve one to three people responsible for everything from CDD at onboarding through SAR filing to board reporting. The arithmetic doesn't work without technology. According to FinCEN's SAR filing statistics, financial institutions filed over 3.6 million SARs in 2023, a figure that reflects the scale of monitoring required across the industry.

For small compliance teams, the priorities are:

- Get the SAR and CTR filing mechanics right before adding analytical sophistication

- Use a vendor platform rather than spreadsheets for transaction monitoring from day one

- Document every decision, because your examiner will ask for the reasoning behind your filings and non-filings alike

The comparison between manual compliance processes and AI-driven automation is increasingly clear: manual processes don't scale, and the cost of a well-integrated platform is typically far lower than the cost of an enforcement action or consent order.

Community Bank BSA Compliance: Practical Exam Preparation

Community bank examiners from the FDIC, OCC, and Federal Reserve all follow the FFIEC BSA/AML Examination Manual. The manual describes not just what examiners evaluate, but how they score it, making it a practical self-assessment tool for any BSA officer preparing for examination.

Common findings at community banks: transaction monitoring not calibrated to the institution's specific risk profile, incomplete beneficial ownership files for legal entity customers, and SAR narratives too sparse to support the underlying filing. Each of these is fixable with preparation.

AML compliance fintech examination expectations have also tightened. State licensing agencies and the OCC's fintech charter unit are increasingly aligned with traditional bank examiners on BSA core requirements. Fintechs that assumed lighter-touch oversight are finding that assumption corrected at their first serious examination.

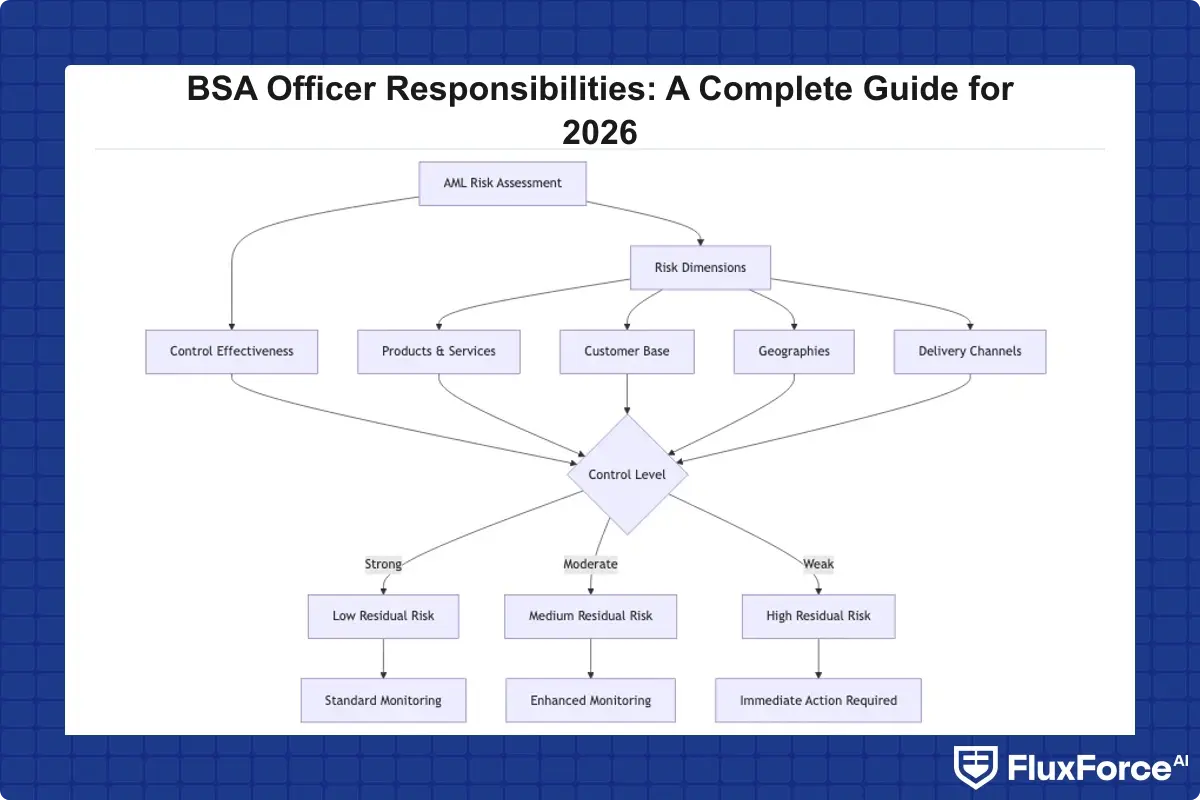

AML Risk Assessment Guide: Building Your Framework

The aml risk assessment guide is the foundation of your entire compliance program. It's where you document your institution's inherent risk, the controls that mitigate it, and the residual risk that remains. Examiners use it to assess whether your monitoring is actually calibrated to your specific risk environment, not just to generic industry benchmarks.

Risk Categories to Document and Score

A complete BSA/AML risk assessment covers four dimensions:

- Products and Services. Cash-intensive products (wire transfers, money orders, international ACH, prepaid cards) carry higher inherent risk. Document each product line with its risk characteristics and expected customer usage patterns.

- Customer Base. What percentage of your customers are businesses vs. individuals? Are any PEPs, money services businesses, or operating in high-risk industries like cannabis or cryptocurrency?

- Geographies. Do you serve customers in or transact with jurisdictions on the FATF grey list, OFAC sanctions lists, or FinCEN high-risk geography advisories?

- Delivery Channels. Digital-only onboarding and remote access channels carry different risks than in-person relationships. Non-face-to-face account opening is specifically flagged in the FFIEC examination manual as a risk factor requiring explicit control documentation.

The risk assessment must be updated whenever any of these factors change materially. A new product launch, entering a new market, or acquiring a customer portfolio all trigger a review, not just the annual calendar date.

EU AI Act Implications for AML Compliance Technology

The eu ai act financial services provisions, which took effect in stages through 2025 and 2026, create documentation and testing obligations for AI-based compliance tools used by institutions with EU exposure. If your aml compliance software uses machine learning for alert scoring or customer risk rating, determine whether those provisions apply to your operations.

This intersects directly with concerns around sanctions screening automation for financial institutions, where AI-driven decisions require audit trails satisfying both U.S. FinCEN expectations and EU AI governance requirements. The practical implication: if you're procuring a new AML platform in 2026, ask vendors specifically about their EU AI Act compliance documentation and model governance practices before you sign.

Onboard Customers in Seconds

Conclusion

This BSA officer responsibilities guide covers the core of what the role requires in 2026: a risk-based AML compliance program built from an honest assessment, SAR and CTR filings executed with documented judgment, KYC processes that continue past onboarding, and technology that actually integrates with your systems.

AML compliance has moved past the era of spreadsheets and purely manual reviews. Whether you're at a community bank working through your bsa aml compliance checklist or a fintech scaling your program under resource constraints, the institutions passing exams today have invested in the right combination of technology, documented process, and human judgment that reflects genuine understanding of the risk, not just box-checking.

Start with your risk assessment. Build your controls from it. Test them independently. Revisit everything at least annually. A risk-based program, documented thoroughly and reviewed regularly, is the kind that holds up when examiners ask why.

Share this article