.webp)

Introduction

FinCEN 2026 priorities compliance is reshaping how banks, fintechs, and insurers design their anti-money laundering programs. The Financial Crimes Enforcement Network's updated strategic plan signals tighter expectations around SAR filing quality, beneficial ownership data accuracy, real-time transaction monitoring, and the responsible use of AI in financial crime detection. For compliance officers and CISOs already managing crowded regulatory calendars, these are not minor adjustments. They require a hard look at existing workflows, technology stacks, and examiner readiness. This post breaks down the areas where FinCEN is focusing its 2026 attention, what each means in practice, and how your team can move from reactive compliance to a position where examiners find little to flag. The frameworks here apply whether you run a $500M community bank or a fintech processing millions of transactions a day.

The frameworks here apply whether you run a $500M community bank or a fintech processing millions of transactions a day.

- What FinCEN's 2026 Priorities Mean for AML Compliance Programs

- The BSA/AML Compliance Checklist Every Institution Needs in 2026

- SAR Filing Efficiency: Updated Requirements and Best Practices

- KYC Automation 2026: From CDD to Enhanced Due Diligence

- How Anti-Money Laundering Technology Drives FinCEN Compliance in 2026

Onboard Customers in Seconds

What FinCEN's 2026 Priorities Mean for AML Compliance Programs

AML compliance is entering its most technology-intensive period to date. FinCEN's 2026 strategic priorities center on three overarching goals: improving the quality of financial intelligence submitted by financial institutions, modernizing the BSA regulatory framework, and strengthening the agency's own analytical capabilities. The practical effect for compliance teams is that check-the-box programs are no longer sufficient. Examiners are increasingly evaluating whether your program actually produces actionable intelligence, not just whether you filed the required forms.

What the FinCEN Strategic Plan Actually Covers

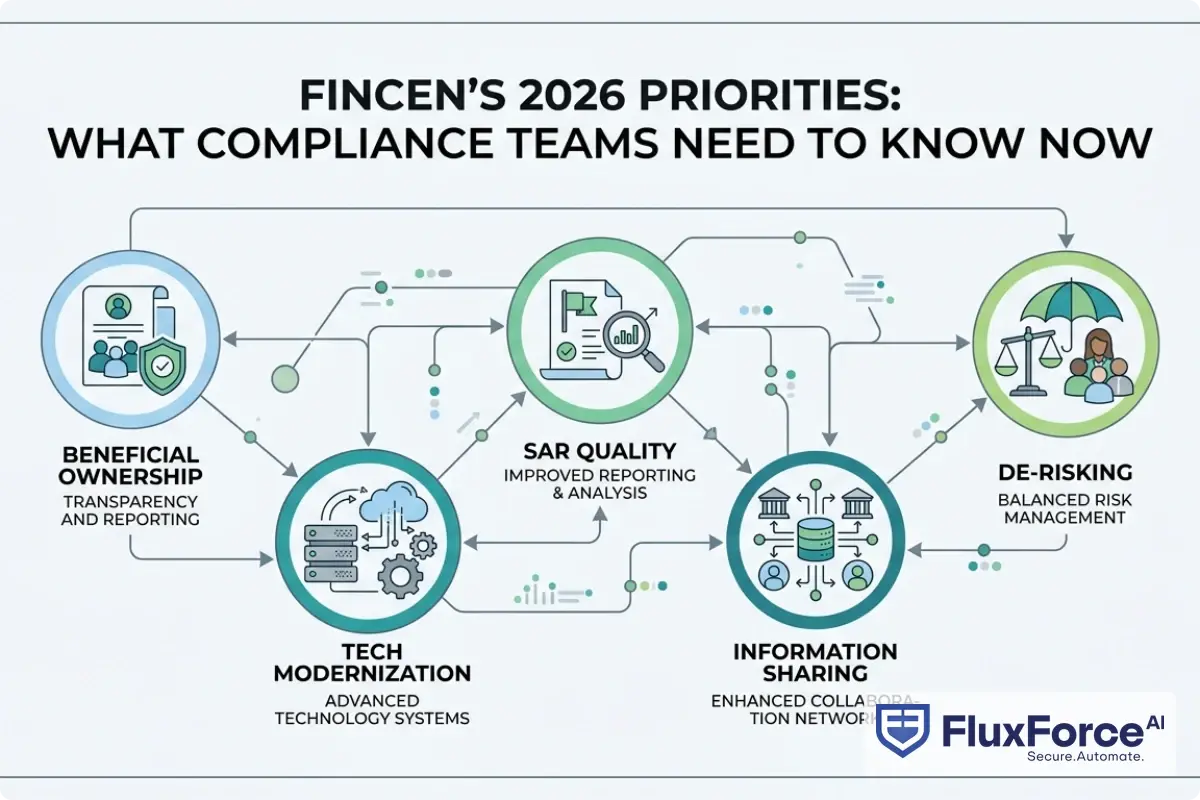

According to FinCEN's regulatory guidance and statutes, the 2026 priorities emphasize five specific areas:

- Beneficial ownership verification and the accuracy of data submitted under the Corporate Transparency Act

- SAR quality over SAR volume, with examiners scrutinizing narrative completeness

- Technological modernization, including AI adoption in transaction monitoring

- Information sharing improvements under Section 314(a) and 314(b) of the USA PATRIOT Act

- De-risking concerns, particularly around correspondent banking and politically exposed persons

The shift from quantity to quality is the headline change. Institutions that file hundreds of SARs with thin narratives are drawing more scrutiny than those filing fewer but better-documented reports.

How BSA AML Compliance Requirements Are Shifting

BSA AML compliance requirements are evolving in two parallel directions. First, the structural program elements (written policies, independent testing, designated BSA officer, training, and internal controls) remain mandatory. Second, regulators now expect those elements to be backed by data-driven evidence of effectiveness. A policy manual is not enough. You need audit trails showing the policy actually runs. Institutions caught with outdated policies or training logs that record only completion rather than comprehension are seeing findings that stick through the remediation cycle.

The BSA/AML Compliance Checklist Every Institution Needs in 2026

A practical bsa aml compliance checklist in 2026 looks different from the 2020 version. Regulators have added expectations around data governance, model risk management for AI-driven monitoring systems, and documented SAR decision rationale. The five-pillar structure persists, but each pillar now has an evidence layer beneath it that examiners want to review.

BSA AML Compliance Checklist: Core Program Elements

The five pillars of a sound BSA program now come with evidence requirements attached:

- Policies and procedures: Updated annually, version-controlled, with documented change logs and sign-off

- Internal controls: Mapped to specific transaction typologies and risk scenarios, not generic policy statements

- Independent testing: Conducted by someone with no operational stake in the results; all findings documented with management responses and remediation timelines

- Designated BSA officer: With documented authority, a defined budget, and clear escalation paths to the board

- Training: Role-specific, tracked, tested with outcome measurement rather than click-through acknowledgment

For teams using aml compliance software, each of these pillars should map directly to system controls so that audit evidence is generated automatically rather than assembled manually in the weeks before each exam.

BSA AML Compliance for Community Banks

BSA AML compliance community banks face a specific bind: they carry the same regulatory obligations as larger institutions with a fraction of the staff. The FFIEC BSA/AML Examination Manual acknowledges proportionality in implementation but makes no concession on the five pillars themselves. A $400M community bank does not need a 50-person AML department, but it does need written rationale for why its current staffing level matches its documented risk profile.

A $400M community bank does not need a 50-person AML department, but it does need written rationale for why its current staffing level matches its documented risk profile.

Practical adjustments for community banks:

- Calibrate transaction monitoring thresholds to your specific customer mix, not industry defaults

- Use the BSA E-Filing batch reporting features to cut manual SAR entry time significantly

- Write SOPs detailed enough that a replacement hire can execute them without institutional memory from the person who wrote them

AML Risk Assessment Guide: Scoring and Prioritizing Threats

An aml risk assessment guide in 2026 must address products, customers, geographies, and delivery channels in an integrated scoring model. The output should be a living document reviewed at least annually and whenever significant business changes occur, not a static PDF filed on a shared drive. Best practice is a scored matrix recalibrated quarterly, with changes triggering a review of monitoring rules. This approach maps naturally to the NIST risk management framework, which many institutions already apply to cybersecurity risk, allowing a unified methodology across both operational risk domains.

SAR Filing Efficiency: Updated Requirements and Best Practices

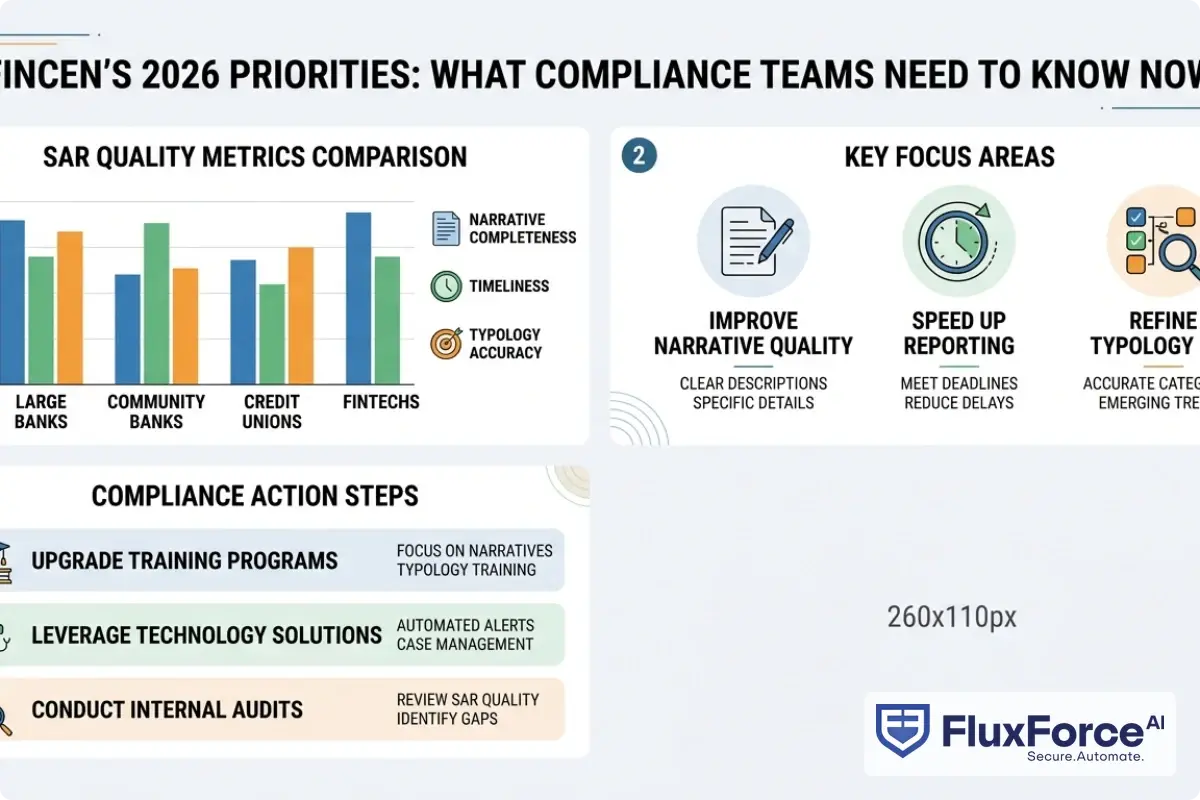

SAR filing efficiency is the compliance function that most directly determines examiner satisfaction in 2026. FinCEN has been explicit in its published guidance: they want fewer, better SARs. A suspicious activity report that describes the what without articulating the why wastes analytical resources and often triggers a follow-up request for supplemental documentation.

SAR Filing Requirements 2026: Key Changes

SAR filing requirements 2026 include several updates that compliance teams should verify they have integrated into their workflows:

- The 30-calendar-day filing window (extendable to 60 days when no suspect is identified) remains unchanged

- Narrative fields now expect specific dollar amounts, transaction dates, and a clear articulation of why the activity is suspicious rather than merely unusual

- Continuing SARs (90-day follow-up filings) must reference the original filing and demonstrate whether the suspicious pattern continued, escalated, or resolved

- Joint filing is actively encouraged when multiple institutions are involved in the same transaction chain

- FinCEN's SAR Activity Review publications identify typologies by sector; compliance teams should be reading these quarterly and updating narrative templates accordingly

Suspicious Activity Report Guide: What Triggers a SAR

A thorough suspicious activity report guide starts with typology awareness. FinCEN's Financial Trend Analysis reports identify recurring red flags by industry and account type. In 2025 and 2026, the most frequently cited triggers include:

- Structuring transactions to avoid the $10,000 CTR threshold (commonly called smurfing)

- Rapid movement of funds through multiple accounts with no clear business rationale

- Customers whose transaction patterns do not match their stated occupation or business type

- Cryptocurrency-to-fiat conversions at high frequency without corresponding commercial activity

- Trade-based money laundering indicators in commercial account activity, including over- and under-invoicing

If your monitoring system generates alerts on these typologies, confirm that the SAR narrative template for each is specific enough to be actionable rather than a recitation of the alert logic that triggered it.

SAR Filing Best Practices for High-Volume Teams

SAR filing best practices for teams processing hundreds of alerts monthly come down to triage discipline. Not every alert requires a SAR, and the decision trail matters as much as the filing itself. A defensible decision tree:

- Does the activity meet the regulatory threshold for suspicion?

- Does documented customer information explain the activity?

- Is there a law enforcement interest warranting a SAR even if the amount falls below threshold?

Teams that document the no-SAR decision with the same rigor as the SAR filing itself face fewer follow-up questions from examiners. AI tools are now assisting with this triage. For a detailed look at how agentic AI reduces false positive alert volumes, see how AI fraud agents cut false positives by 80%.

For a detailed look at how agentic AI reduces false positive alert volumes, see how AI fraud agents cut false positives by 80%.

KYC Automation 2026: From CDD to Enhanced Due Diligence

KYC automation 2026 is not optional for institutions managing more than a few thousand customer relationships. Manual KYC processes create two problems: they slow onboarding to the point where customers abandon the process, and they introduce inconsistency that examiners flag as a control gap. Automation does not eliminate human judgment. It applies human judgment at the decision points that actually require it, rather than to every data entry task.

KYC CDD Requirements for Banks Under New Rules

KYC CDD requirements banks must satisfy include the four pillars established by FinCEN's 2016 Customer Due Diligence Rule, which remain in force under the 2026 framework:

- Identifying and verifying customer identity at account opening

- Identifying and verifying beneficial owners (25% equity threshold plus the control prong for legal entities)

- Understanding the nature and purpose of customer relationships to develop risk profiles

- Conducting ongoing monitoring to identify suspicious transactions and keep customer information current

The Corporate Transparency Act adds a cross-reference obligation: financial institutions will need to validate beneficial ownership data against FinCEN's own beneficial ownership database once access opens. Compliance teams should be planning system integrations now. Waiting for the access window creates a scramble that produces inconsistent results and leaves gaps in the audit record.

Enhanced Due Diligence Guide for High-Risk Customers

An enhanced due diligence guide must be triggered by objective criteria applied consistently, with documented rationale for each escalation decision. High-risk triggers that should automatically move a customer to EDD status include:

- Politically exposed persons, domestic and foreign, and their close associates

- Customers in FATF high-risk or monitored jurisdictions

- Cash-intensive businesses: car dealerships, jewelry retailers, money services businesses

- Customers with prior SAR filings or documented law enforcement inquiries on record

- Non-face-to-face account openings above defined size thresholds

EDD is not exclusively a banking concern. For organizations managing AML risk checks in insurance policy issuance, life insurance products with large lump-sum premiums are a recognized money laundering channel requiring the same diligence standards as high-risk bank accounts.

How Anti-Money Laundering Technology Drives FinCEN Compliance in 2026

Anti-money laundering technology is the area where 2026 diverges most sharply from prior regulatory periods. Regulators and financial institutions are now having concrete conversations about AI in AML that were purely theoretical three years ago. The question is no longer whether to adopt the technology but how to do it in a way that satisfies both detection goals and model risk management requirements.

Anti-Money Laundering Technology 2026: AI and Machine Learning Applications

Anti-money laundering technology 2026 deployments fall into four practical categories:

| Technology Type | Primary Use Case | Maturity Level |

|---|---|---|

| Rules-based monitoring | Transaction thresholds, structuring detection | Established |

| Machine learning anomaly detection | Behavioral deviation, peer group analysis | Maturing |

| Network analysis and graph AI | Relationship mapping, shell company detection | Emerging |

| Generative AI and large language models | SAR narrative drafting, alert triage support | Early stage |

The honest position on generative AI in AML is that it helps with narrative drafting and alert summarization, but it is not yet reliable enough to make autonomous filing decisions. Institutions piloting LLM-assisted SAR writing report that drafts still require human review for factual accuracy and legal defensibility. That is not a reason to avoid the technology. It is a reason to define the human-in-the-loop requirements before deployment rather than after an examiner finds an error in a filed report.

AML compliance software vendors universally claim AI capabilities in 2026. The real differentiator is explainability: can the system tell an examiner, in plain English, why it generated a specific alert and how it weighted the contributing factors? Black-box models fail model risk management reviews regardless of their detection accuracy numbers.

EU AI Act Financial Services: Cross-Border Compliance Implications

The EU AI Act financial services provisions classify high-risk AI systems to include those used in creditworthiness assessment and AML transaction monitoring. For institutions operating across the EU and US, this creates a dual compliance obligation: FinCEN's existing BSA guidance plus Article 10 data quality requirements and Article 13 transparency requirements for AI-generated outputs. The EU AI Act risk classification framework should be mapped against current monitoring tools now, before cross-border regulators begin requesting conformity documentation. For a detailed comparison of rule-based and AI-driven approaches to alert management, the analysis of rule-based systems vs. AI for false positive reduction covers implementation-level tradeoffs that apply directly to this decision.

FinCEN 2026 Priorities Compliance for Fintechs and Community Banks

FinCEN 2026 priorities compliance hits fintechs and community banks differently, but both groups share a core challenge: full regulatory obligations with constrained resources. Neither typically maintains a large dedicated AML department, which means every process inefficiency has a direct cost in either staff hours, examiner findings, or both.

Fintech BSA AML: Operating with a Small Team

Fintech BSA AML small team environments are the norm across payment processors, digital lenders, and neobanks. The regulatory expectation does not scale down to match team size. Practical strategies that actually work in this environment:

- Automate the transactional layer entirely: No human should manually review every monitoring alert. Set rule logic and risk thresholds, then focus human attention exclusively on escalated cases

- Buy before build: Purpose-built aml compliance fintech software vendors maintain pre-built typology libraries that a three-person compliance team cannot replicate internally at reasonable cost or with consistent quality

- Write SOPs that survive turnover: Small teams are disproportionately exposed when a key person departs. Document every decision point as if the reader is a competent replacement who has never seen your system before

For digital lenders, AML screening in digital lending covers the specific origination workflow touchpoints where laundering risk concentrates and where monitoring gaps most commonly appear in examinations.

AML Compliance Software: Selecting the Right Stack

Evaluating aml compliance software in 2026 requires pressing vendors on five dimensions before signing a contract:

- Regulatory coverage: Does the platform handle FinCEN BSA requirements, OFAC screening, and CDD rule compliance in an integrated system, or do you stitch together separate modules from different vendors?

- Integration depth: Does it pull transaction data from your core banking or lending system in near-real-time, or does it rely on nightly batch files that create a 24-hour blind spot?

- Explainability: Does the alert rationale satisfy model risk management documentation requirements without requiring your team to manually reconstruct the reasoning?

- SAR filing integration: Can it push SAR drafts directly to FinCEN's BSA E-Filing system, or does your team re-key data into a second application?

- Scalability pricing: Does the cost model remain proportionate as your customer base grows over the next 24 months, or does pricing jump sharply at volume thresholds?

For a detailed comparison of manual versus automated compliance operating models, manual compliance vs. AI automation covers total cost of ownership factors that belong in any vendor evaluation before signing a multi-year contract.

CTR Filing Rules and AML Risk Assessment in the New Regulatory Era

CTR filing rules have not changed substantively in 2026. The $10,000 threshold for Currency Transaction Reports remains, and the 15-day filing window applies to all covered financial institutions. What has shifted is examiner attention to CTR exemption management. Any institution with a high volume of CTR exemptions should be prepared to walk an examiner through each one with documented rationale, annual review evidence, and a clear connection to the institution's risk profile. Exemptions that were granted years ago without documented review are a common exam finding.

The aml risk assessment process is what connects CTR and SAR programs into a coherent whole. When the risk assessment is genuinely current, it drives monitoring thresholds, customer risk ratings, and EDD triggers across the entire program. Institutions that treat it as an annual compliance exercise rather than an operating document miss the point entirely. FinCEN examiners now look for evidence that the risk assessment outcome actually changed something: recalibrated thresholds, triggered customer reviews, updated training content. A risk assessment that produces no program changes raises questions about whether it reflects reality.

For organizations in regulated sectors beyond traditional banking, including cross-border supply chain and trade finance, AML risk considerations extend into vendor due diligence and counterparty screening. The intersection of transaction monitoring and third-party risk management is increasingly relevant to non-bank financial institutions operating in high-risk trade corridors.

- AML compliance is entering its most technology-intensive period to date.

- A practical bsa aml compliance checklist in 2026 looks different from the 2020 version.

- SAR filing efficiency is the compliance function that most directly determines examiner satisfaction in 2026.

- KYC automation 2026 is not optional for institutions managing more than a few thousand customer relationships.

- Anti-money laundering technology is the area where 2026 diverges most sharply from prior regulatory periods.

Onboard Customers in Seconds

Conclusion

FinCEN 2026 priorities compliance is a quality upgrade, not a volume mandate. The agency wants financial intelligence that is useful and actionable, not just filed on time. For compliance teams, that means SAR narratives that tell a complete story, KYC records that reflect current customer reality, risk assessments that actively drive program decisions, and monitoring systems that can explain their alerts to an examiner without generating a lengthy defense document for a single false positive.

The institutions that perform best in 2026 exams are those investing in aml compliance software with built-in explainability, training staff on typology-specific SAR writing, and keeping their BSA program documents genuinely current rather than updating them reactively before scheduled exams. Start with the checklist in this post, identify gaps against your current state, and prioritize the items your last examination flagged. Regulators are rewarding institutions that demonstrate good-faith, data-backed improvement over those that appear compliant on paper but deliver poor-quality intelligence outputs to the financial crime ecosystem.

Share this article