.webp)

Listen to our podcast 🎧

Introduction

Every year, between 2% and 5% of global GDP is laundered — and less than 2% is ever recovered. Insurance may look less risky than banking, but it has become a silent channel for financial crime. Conservative estimates suggest $80–$100 billion is laundered annually through insurance products alone.

For insurance CISOs, AML in banking has long set the compliance standard — but AML in finance now extends well beyond banks. Anti-money laundering (AML) has become a business risk, a security issue, and increasingly, a CISO responsibility.

What is Anti Money Laundering?

Many people ask, “what is anti money laundering?” At its core, it means putting systems in place to stop criminals from turning dirty money into clean money.

In banking, AML this usually covers customer checks, transaction monitoring, and reporting unusual activity.

But in insurance, the picture is different. If you ask, “what is AML in finance?” the answer goes beyond banks. Insurers deal with policy issuance, life products, and long-term contracts. Criminals use these as a slower but safer way to hide money.

Why Policy Issuance is a Risk Point ?

Unlike banks, insurers may not always have strong KYC and AML checks at the start of a relationship. This gap makes policy issuance an easy entry point for laundering.

Regulators are catching on. A few examples:

- BNP Paribas’s insurance arm Cardif was fined 2.5 million euros for weak AML risk checks.

- BGL BNP Paribas in Luxembourg faced a 3 million euro penalty for failing due diligence.

This shows that AML in finance applies as much to insurance as it does to banks.

Why CISOs Should Pay Attention ?

As Stéphane Nappo, Global CISO at Groupe SEB, once pointed out, building a reputation takes years, yet one mistake can ruin it in minutes.

In insurance, that mistake could be a weak AML check during policy issuance. One missed step in the KYC process banking workflow can lead to fines, loss of trust, and damaged brand value.

For CISOs, bringing KYC AML banking practices into the insurance space is now a must-have strategy.

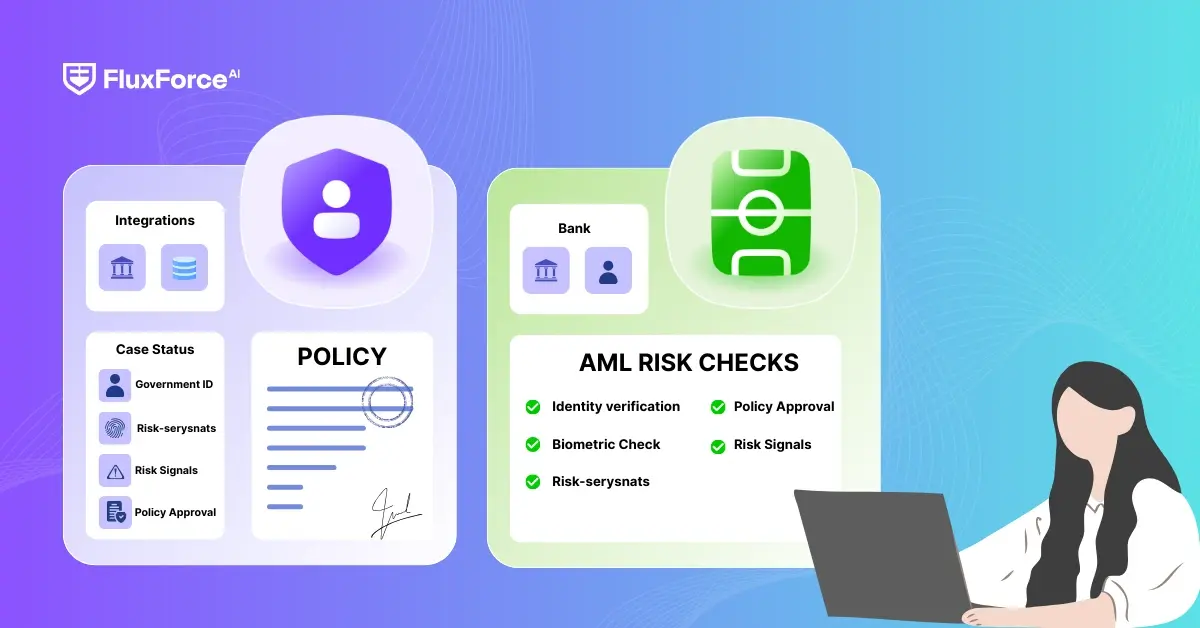

Why CISOs Must Lead AML Risk Checks in Insurance ?

In most insurance firms, compliance teams have always owned the AML and KYC checks. But today, with fraud getting smarter and digital policy issuance becoming the norm, this is no longer enough. CISOs are stepping in to bring a fresh approach.

The New Role of CISOs in AML

So why should CISOs be in the front seat? Because AML in banking and finance is no longer just about paperwork. It’s about data, systems, and security.

- KYC applications are digital now, which means they can be hacked or bypassed.

- KYC tools for banks and insurers need strong cybersecurity controls to prevent fake documents from slipping through.

- KYC fraud detection depends heavily on AI, machine learning, and cross-platform monitoring and in all these areas the CISO strategy matters.

KYC fraud detection depends heavily on AI, machine learning, and cross-platform monitoring and in all these areas the CISO strategy matters.

CISOs as Business Protectors

When people ask, “what are KYC requirements?” they often think of IDs, addresses, and signatures. But CISOs see more. They see:

- Identity theft risks that can fool onboarding systems.

- Synthetic fraud where fake identities are built from stolen data.

- Policy misuse where criminals overfund or cancel policies to move illegal money.

This is why CISO best practices in AML go beyond compliance. They align with broader risk checks for insurance policy issuance and identity verification solutions for fraud prevention.

The Technology Gap

One of the biggest challenges is that compliance tools alone are not enough. For example:

- Legacy AML systems often miss patterns across multiple policies.

- Manual KYC reviews are too slow to catch fast-moving fraud.

- Some insurers still lack automated KYC verification tools for insurers, which creates blind spots.

Here, CISOs can close the gap by connecting AML in finance with stronger digital defenses.

Why this Matters ?

A report by PwC in 2023 showed that 46% of financial services firms faced fraud in the last two years, with insurance being a growing target. Criminals now see insurers as “low-hanging fruit” compared to banks.

That makes the CISO strategy clear. AML risk checks can’t be treated as an isolated compliance process. They must be part of the core security framework of the organization.

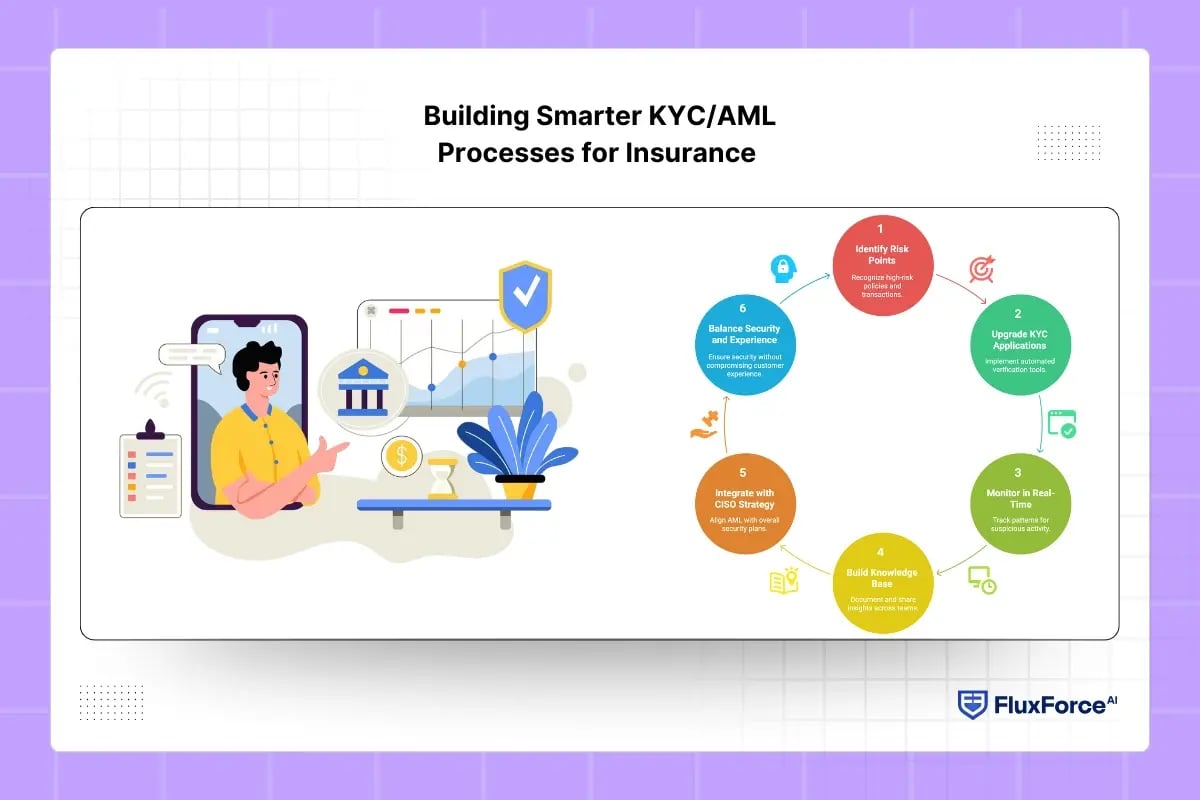

Building Smarter KYC/AML Processes for Insurance

Understanding Risk Points in Policy Issuance

One of the biggest challenges insurance leaders face is making AML risk checks strong without slowing down policy issuance. The starting point is understanding where the real risks are. Life insurance policies, annuities, and single-premium products carry higher money-laundering risks than short-term or low-value policies. CISOs who understand these differences can focus on the areas that matter most, instead of spreading resources too thin.

Upgrading KYC Applications for Accuracy

Manual ID checks and static databases are no longer enough. Fraudsters are smarter, and compliance officers cannot catch every forged document by hand. Automated KYC verification tools for insurers, which pull from multiple sources including government IDs, sanctions lists, and even device fingerprints, bring both speed and accuracy. CISOs must also ensure that these tools evolve constantly as fraud methods change.

Real-Time AML Monitoring Beyond Onboarding

Even with strong KYC, some fraudsters can slip through and exploit the system later. Unlike banks, insurers handle fewer transactions but they are higher in value, such as policy surrenders or large premium payments. A sudden large withdrawal may seem normal at first, but when looked at alongside a customer’s past behavior, it can reveal attempts at money laundering. Smart AML systems track patterns across policies and customers, helping detect unusual activity before it becomes a bigger problem.

Building an Internal Knowledge Base

AML teams often work in isolation, and insights from suspicious cases can get lost. Successful insurers treat each case as a learning opportunity. They document, analyze, and share insights across teams. Over time, this creates an internal AML playbook, helping the company respond faster to new fraud tactics while improving both compliance and security.

Integrating AML with CISO Strategy

AML work is more than just compliance. A strong CISO strategy ensures KYC and AML checks are part of the company’s overall security plan. When leaders see AML as protection against both regulatory fines and financial fraud, it becomes easier to get organizational support. This also ensures the company protects itself and its customers in a practical, efficient way.

Balancing Security with Customer Experience

Smarter KYC and AML checks are not related to slowing down customers. But here's the goal is to create a path where criminals are filtered out early, suspicious activity is detected promptly, and genuine clients feel secure. This balance builds trust and strengthens the insurer’s reputation over the long term.

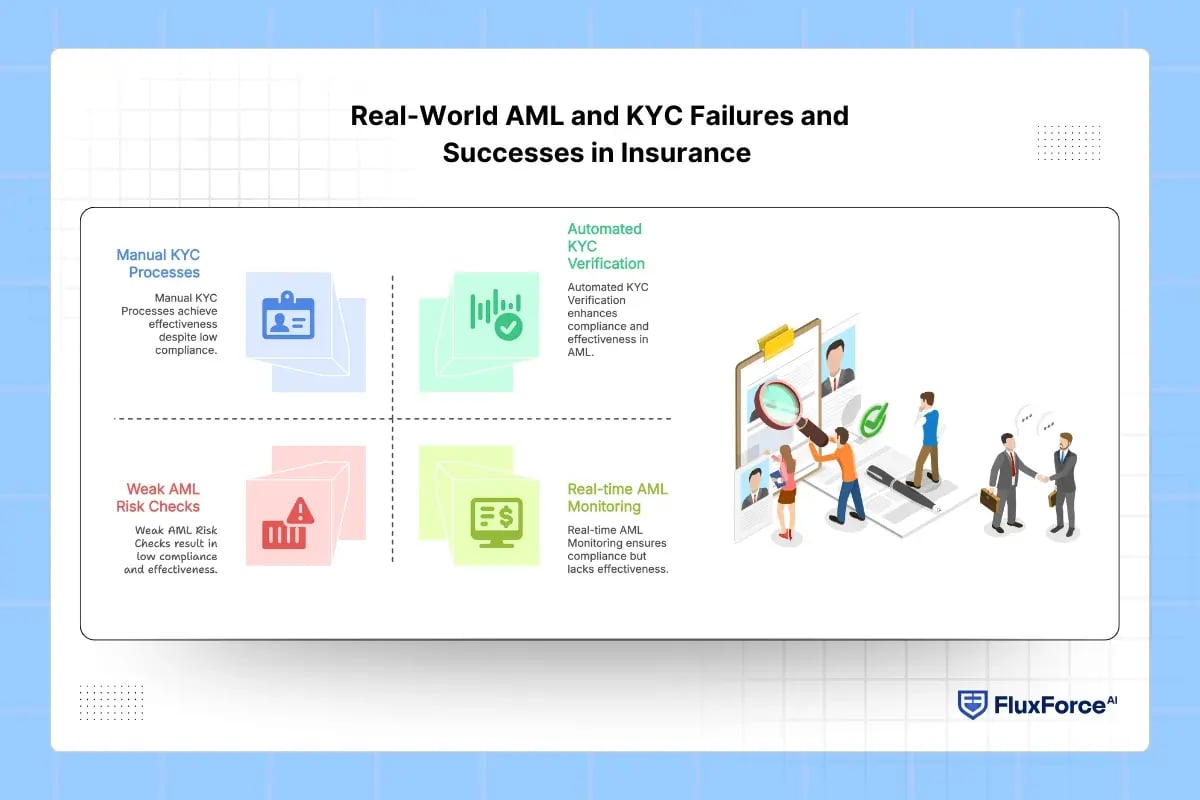

Real-World AML and KYC Failures and Successes in Insurance

High Profile AML Compliance Failures

Insurance companies are often considered lower-risk targets, but real cases prove otherwise. Crawford & Company in the UK faced penalties for failing KYC and AML checks. These examples show that all insurers must take anti-money laundering frameworks for insurance providers seriously.

How Criminals Exploit Insurance

Certain insurance products can be misused to launder money. Single-premium policies, annuities, and life insurance with surrender clauses allow criminals to turn illicit funds into legitimate payouts. Even cooling-off periods and policy loans are exploited. Brokers sometimes facilitate these schemes, making it critical to use identity verification solutions for insurance fraud prevention.

Success Stories: Compliance as Strength

Some insurers have turned KYC/AML identity verification strategies for insurance CISOs into a strong advantage. Companies using automated KYC verification tools for insurers and real-time AML monitoring detect suspicious activity faster, reduce fraud, and streamline policy issuance. This shows that compliance and efficiency can work together.

Practical Takeaways for CISOs

CISOs should focus on high-risk products, leverage automation, and share insights from suspicious cases across teams. Collaboration between IT, risk, and compliance ensures AML in finance is not just about rules but also about protecting the business and customers.

Using Data to Strengthen Compliance

PwC reports nearly two-thirds of insurers have faced fraud or financial crime recently. AI-driven KYC applications and AML banking term monitoring help detect unusual activity early, minimize human error, and improve regulatory compliance. Technology is becoming the key to strong KYC and AML in banking and insurance.

Onboard Customers in Seconds

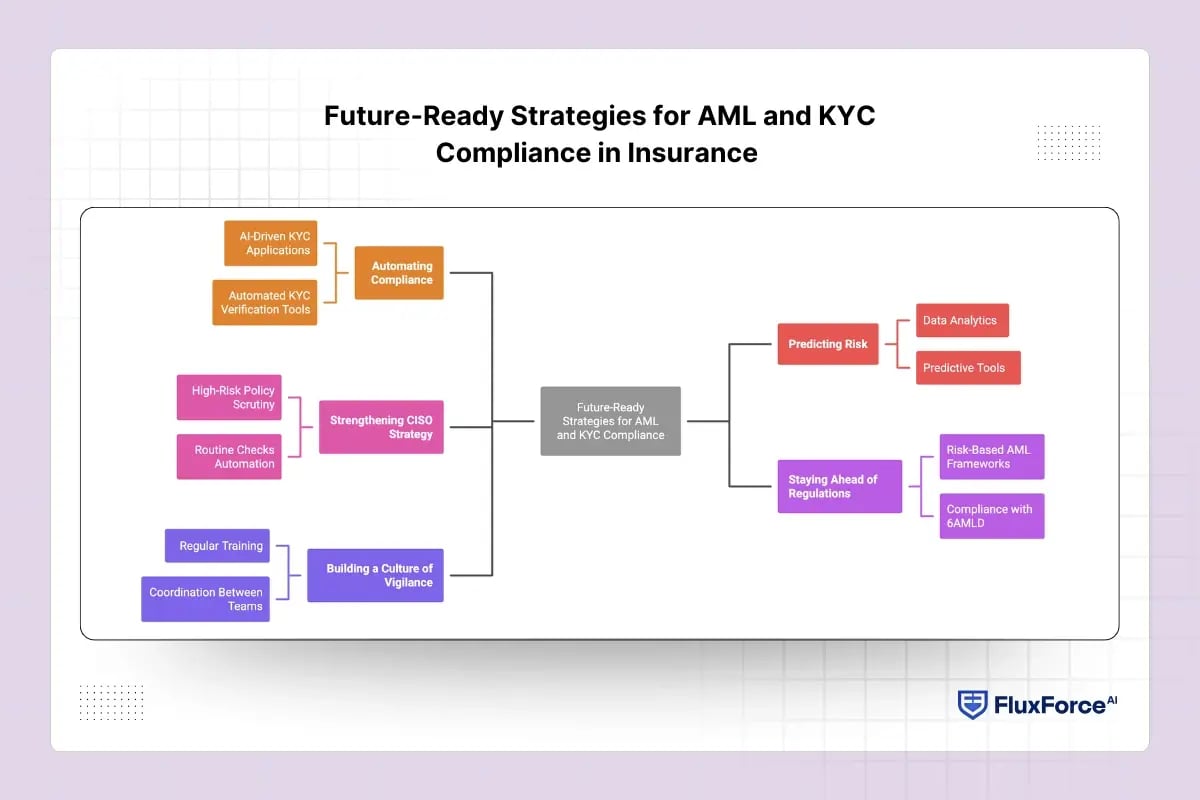

Future-Ready Strategies for AML and KYC Compliance in Insurance

Automating Compliance Without Losing Control

Manual checks are no longer enough. Insurance CISOs are increasingly adopting AI-driven KYC applications and automated KYC verification tools — the same standard now expected in AML in banking. This allows companies to monitor policies and verify identities in real time while ensuring KYC and AML checks are accurate, consistent, and faster. Automation reduces errors and frees compliance teams to focus on high-risk cases.

Predicting Risk with Smart Data

Data analytics is the new frontline. By analyzing patterns across policies, claims, and transactions, insurers can spot suspicious activity before it becomes fraud. Predictive tools strengthen identity verification solutions for insurance fraud prevention and provide CISOs with actionable insights for AML risk checks for insurance policy issuance.

Strengthening CISO Strategy

A modern CISO strategy includes compliance at every step of the insurance process. High-risk policies receive extra scrutiny, while routine checks are handled automatically. Using both technology and human expertise ensures strong oversight, follows CISO best practices, and makes operations more efficient.

Staying Ahead of Regulations

Global AML rules change quickly. Risk-based anti-money laundering frameworks allow insurance providers to adjust without slowing down operations. Using automation and data analysis helps companies stay compliant with rules like the EU’s 6AMLD while keeping business running smoothly.

Building a Culture of Vigilance

Fraud cannot be stopped by technology alone. Insurers should foster a culture in which all staff appreciate the importance of KYC/AML identity verification. Regular training and strong coordination between IT, risk, and compliance teams strengthen AML practices.

Conclusion

The battle against financial crime in insurance is real, but today’s innovations make it winnable. Automated KYC verification tools for insurers, AI-based KYC applications, and effective AML risk checks for insurance policy issuance give CISOs the power to protect their organizations. Compliance isn't mere a regulation but an asset. Insurers embracing automation, predictive analytics, and a vigilant workforce not only secure their operations but also position themselves ahead of competitors in a fast-changing market.

Share this article