.webp)

Introduction

FFIEC exam AI systems are now one of the top examiner priorities entering 2026, and the scrutiny has moved well past basic functionality checks. If your institution deployed machine learning for transaction monitoring, KYC automation, or SAR filing in the past two years, examiners will arrive expecting model governance documentation, explainability artifacts, bias testing records, and evidence that your AML compliance program actively controls the AI rather than simply relying on its outputs. The stakes are real: exam findings tied to model risk management can trigger mandatory remediation timelines, and in 2025 several institutions received Matters Requiring Attention specifically for inadequate AI oversight in their AML compliance software. This post covers what examiners actually look for, section by section, so your team can prepare before the exam cycle starts.

- Why FFIEC Exam AI Systems Face Stricter Review in 2026

- How Examiners Evaluate AML Compliance in AI-Driven Workflows

- BSA/AML Compliance Checklist for AI Systems

- KYC Automation Requirements Examiners Expect

- SAR Filing Efficiency: What Gets Tested in the Exam

Onboard Customers in Seconds

Why FFIEC Exam AI Systems Face Stricter Review in 2026

Three things converged to put AI squarely in the examiner's crosshairs this cycle. First, the FFIEC updated its model risk management expectations, making clear that SR 11-7 principles apply to machine learning models used in BSA/AML compliance regardless of vendor origin. Second, the pace of AI adoption in transaction monitoring outran governance frameworks at many institutions: models were tuned, retrained, or swapped mid-year with no formal change control or back-testing records. Third, the eu ai act financial services provisions, which classified AML and credit-scoring models as high-risk AI, sent a clear signal that regulatory scrutiny will only increase globally.

The result is that examiners arrive with a specific checklist. They are not evaluating whether your AI produces good outputs on average. They want to know how you would know if it stopped producing good outputs, and what you did the last three times you needed to find out.

The SR 11-7 Gap in Modern AI Deployments

The Federal Reserve's SR 11-7 model risk guidance predates modern deep learning by a decade, and applying it to neural network-based transaction monitoring is not straightforward. Examiners in 2026 are specifically checking for:

- A written definition of what counts as a "model" at your institution (many institutions still exempt vendor-provided rule engines)

- Model inventory completeness, including third-party and embedded models

- Independent validation performed by staff or vendors with no stake in the model's performance

- Challenge processes: documented evidence that someone with authority actually questioned the model's outputs

The gap most institutions fall into is treating the vendor's model validation report as sufficient. Examiners do not agree. They expect your institution to have conducted or commissioned its own validation, even if you license the model from a vendor.

EU AI Act Financial Services Spillover

Even if your institution operates solely in the United States, the eu ai act financial services implications matter. Several global correspondent banks have begun requiring their US partners to document AI governance practices aligned with the Act's high-risk AI framework. Some regional examiners are informally factoring that posture into their risk assessments for internationally active institutions, so tracking EU developments is worthwhile regardless of where your customers are.

How Examiners Evaluate AML Compliance in AI-Driven Workflows

AML compliance in 2026 is not evaluated in isolation from the technology delivering it. When examiners review your aml compliance software, they assess it as part of the broader BSA/AML program, not as a separate IT audit. This means the same people doing transaction monitoring reviews are also checking your model's configuration history, alert threshold documentation, and tuning rationale.

The AML Risk Assessment Guide Examiners Use

The FFIEC BSA/AML Examination Manual is the definitive aml risk assessment guide examiners apply. In 2026, the manual is supplemented by interagency AI statements. When your examiner pulls up the risk assessment section, they look for three things:

- Customer risk stratification methodology: Does your AI's risk scoring align with your documented customer risk segmentation? Can you trace a sample of decisions back to the model's logic?

- Product and channel risk weighting: Does the model account for higher-risk products like digital assets, prepaid cards, or correspondent banking with appropriate sensitivity settings?

- Geographic risk factors: Is the model updated when OFAC or FinCEN advisory geographies change, and how quickly does that update propagate?

Most findings at this stage are not about the AI being wrong. They are about the institution being unable to demonstrate control over a system it depends on for regulatory decisions.

What AML Compliance Software Must Document

Your aml compliance software needs to produce audit trails that examiners can walk through without your team narrating every step. Institutions that require compliance staff to manually explain what the system did during a review consistently get worse outcomes than those with self-documenting logs. At minimum, your system should capture:

- Alert generation events with the rule or model version that triggered each alert

- Disposition decisions with timestamps, analyst IDs, and populated rationale fields

- Model performance metrics pulled on a scheduled basis (false positive rate, SAR conversion rate, alert aging)

- Configuration changes with approval records showing who authorized each change

BSA/AML Compliance Checklist for AI Systems

The bsa aml compliance checklist for AI-assisted programs differs from the traditional version in one key way: the examiner also wants controls on the controls. Showing that alerts are reviewed is not enough. You need to show that the system generating those alerts is itself reviewed, tested, and documented.

A complete exam-ready checklist covers four areas:

Model Governance

- Model inventory entry with risk rating

- Independent validation within the past 12-24 months

- Change management log for threshold adjustments

- Annual review sign-off by a qualified second-line reviewer

Transaction Monitoring

- Alert volume and false positive rate tracked monthly

- Alert aging policy with documented escalation thresholds

- Coverage testing confirming the model catches typology scenarios from current FinCEN advisories

Customer Due Diligence

- CDD rule compliance documentation for legal entity customers

- Beneficial ownership collection process with refresh triggers

- Enhanced due diligence escalation records for high-risk customers

Filing

- SAR filing pipeline with complete decision audit trail

- CTR exemption list with annual review evidence

- Quality control sampling for filed SARs and CTRs

Model Validation Requirements

Examiners expect validation reports that go beyond vendor attestations. The validation should test the model against your institution's own transaction data, not benchmark datasets alone. For AML compliance in digital lending and fintech contexts where transaction patterns differ significantly from traditional banking, institution-specific validation is particularly important. Third-party validation vendors are acceptable, but your institution must formally review and accept or challenge the findings in writing.

Ongoing Monitoring and Tuning Records

Every time your team adjusts alert thresholds, the examiner wants to know why. "Too many false positives" is not sufficient rationale on its own. The documentation should show the data: what was the false positive rate before the change, what was the SAR conversion rate at the prior threshold, and what did back-testing show about the impact? Institutions that answer these questions with a written report rather than a verbal explanation during the exam consistently receive better outcomes.

KYC Automation Requirements Examiners Expect

KYC automation has matured significantly, and examiner expectations have matured with it. kyc automation 2026 reviews focus less on whether you automated onboarding at all and more on whether the automation is disciplined. The most common finding in this area: institutions automated data collection but left the risk decision to a human reviewer with no structured decision framework, creating inconsistency that examiners flag as a control weakness.

The kyc cdd requirements banks face under the CDD Rule remain the baseline, but examiners now layer on questions about how your automation handles exceptions, edge cases, and refresh cycles for existing customers who were onboarded under older procedures.

Enhanced Due Diligence Guide for High-Risk Customers

Your enhanced due diligence guide should be a living document that maps specific customer risk factors to specific investigative actions. Examiners test this by pulling a sample of high-risk customers and asking your team to walk through the EDD performed on each. Common gaps that surface:

- EDD was documented but not risk-based (identical questionnaires for an MSB and a foreign PEP)

- Refresh triggers were defined in policy but the system did not actually re-score customers when trigger events occurred

- Source of wealth documentation was collected but no analyst evaluated it against the customer's declared business activity

For a detailed look at how identity verification integrates with AML risk decisions in practice, see AML Risk Checks in Policy Issuance, which covers the same examiner logic applied in insurance contexts.

CDD Rule Compliance in Automated Onboarding

The beneficial ownership collection requirement under the FinCEN Customer Due Diligence Rule is technically complex to automate correctly. Examiners check that your system identifies legal entity customers, prompts for beneficial ownership data at the right ownership percentage thresholds, and re-collects that data when material ownership changes are flagged by your monitoring system. The most common failure point: systems that collect ownership data at onboarding but have no mechanism to detect post-onboarding ownership changes and trigger a refresh.

SAR Filing Efficiency: What Gets Tested in the Exam

SAR filing efficiency is an area where examiners have become notably granular. They are not just checking that SARs get filed. They are checking how long decisions take, whether the reasoning is documented, and whether the decision not to file receives the same rigor as the decision to file.

The sar filing requirements 2026 retain the 30-day filing window as the standard, but examiner expectations around the decision audit trail have tightened considerably. Institutions using AI to prioritize or pre-populate SAR narratives are specifically asked to demonstrate that human reviewers actually review the AI output rather than accept it without independent scrutiny.

How Examiners Measure SAR Filing Efficiency

Examiners pull a sample of alerts that were closed without filing and test whether the disposition rationale is sufficient. The sar filing best practices that survive exam scrutiny share a common trait: the narrative for a non-filing decision is as specific as the narrative for a filing. "Reviewed and determined no suspicious activity" does not pass. A note explaining what was reviewed, what it showed, and why it does not meet the reporting threshold does pass.

Your suspicious activity report guide should include decision templates that prompt analysts to document specific elements for every disposition. Without those templates, most analysts default to minimal documentation that will not hold up to examiner scrutiny.

Documenting the Decision Logic Behind SAR Filings

When AI assists in drafting SAR narratives or flagging relevant transactions, examiners want the AI's contribution labeled and a human reviewer's sign-off on the substance documented separately. This is where clean alert management directly supports exam readiness. The comparison of rule-based versus AI-driven approaches to false positive reduction is relevant here: every alert that reaches the SAR decision stage should have a clean audit trail showing a human made the final call.

CTR Filing Rules and AI-Assisted Currency Reporting

CTR filing rules are more deterministic than SAR filing, which makes AI-assisted CTR processing somewhat simpler to defend in an exam. The complexity is in aggregation logic. Examiners specifically test whether your system correctly aggregates cash transactions across accounts, across branches, and across business days when a customer conducts multiple transactions on the same calendar day.

The most common CTR-related finding in AI deployments: institutions that moved to automated CTR generation discovered their aggregation logic did not match the regulatory definition of a "day" for multi-branch transactions, and had been systematically under-filing for months before the gap surfaced. A back-test comparing your AI's CTR decisions against manual review for a representative sample period is the most reliable way to find these issues before the examiner does.

CTR exemption management is a separate risk area. If your institution maintains a list of exempt customers, that list needs a documented annual review cycle with evidence that each high-volume cash customer still meets the Phase I or Phase II exemption criteria. Automated exemption lists that are never reviewed are a consistent exam finding.

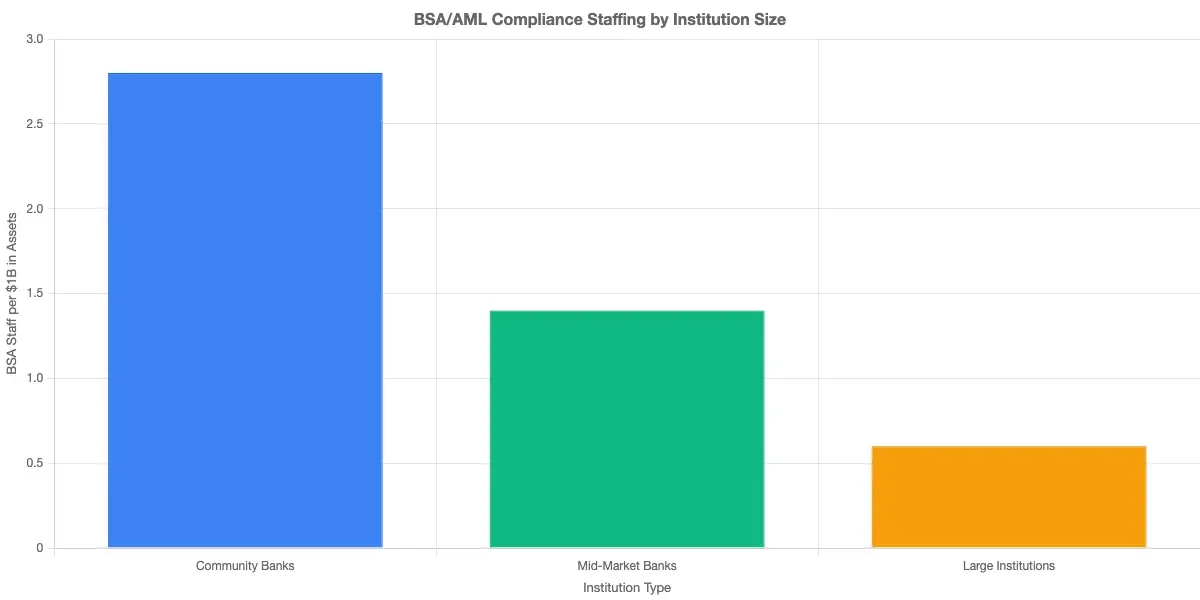

How Community Banks Handle BSA/AML Compliance Differently

bsa aml compliance community banks face the same regulatory requirements as their larger peers, but with fundamentally different resource profiles. A community bank with $500 million in assets may have a BSA officer who also handles other compliance responsibilities and a transaction monitoring team of two people. The examiner applying the same AI governance framework as they would to a $50 billion institution creates genuine pressure on those teams.

A community bank with $500 million in assets may have a BSA officer who also handles other compliance responsibilities and a transaction monitoring team of two people.

Resource Constraints and the Fintech BSA/AML Small Team Problem

The fintech bsa aml small team challenge is in some ways more acute than the community bank version. Fintechs processing high transaction volumes with three-person compliance teams face the same FFIEC exam AI systems scrutiny as a traditional bank, but without decades of institutional knowledge to draw on. aml compliance fintech programs are examined for the same elements: model governance, alert management, SAR filing quality, and CDD completeness.

The practical answer for small teams is aml compliance software that builds the audit trail automatically. When documentation happens as a byproduct of the workflow rather than as a separate administrative task, small teams can maintain exam-ready records without dedicating headcount to documentation alone. For a concrete example of how automated decision logging reduces both false positives and exam exposure, see how agentic AI cuts false positive rates in production environments.

Anti Money Laundering Technology 2026 for Smaller Institutions

Anti money laundering technology 2026 has made vendor solutions genuinely accessible to smaller institutions, with cloud-based platforms offering per-transaction pricing and built-in model validation reporting as standard features. Examiners expect institutions of all sizes to have evaluated whether their current anti money laundering technology is appropriate for their actual risk profile. If you are running a transaction monitoring system from 2018 with no documented evaluation of whether it still fits your current customer mix and transaction volumes, that gap will surface in the exam.

Preparing Your Institution Before the Next FFIEC Exam

The single most effective preparation step is a pre-exam self-assessment against the FFIEC BSA/AML Examination Manual's core examination procedures, applied specifically to your AI systems. Many institutions complete the general BSA/AML self-assessment but skip the model risk management layer. That is where most exam surprises occur.

Building Your Pre-Exam Documentation Package

Your pre-exam documentation package for AI systems should include:

- Model inventory: Every AI or ML model used in BSA/AML decisions, including vendor models and embedded scoring tools

- Validation reports: Independent validation for each model, dated within the examiner's standard lookback window

- Change log: Every threshold change, model update, or parameter adjustment in the past 24 months with documented business justification

- Performance metrics: Monthly alert volume, false positive rate, SAR conversion rate, and alert aging for the past 12 months

- Governance records: Model risk committee review minutes, annual sign-offs, and escalation records

- Training records: BSA/AML training completion for every staff member involved in AI-assisted review

For a detailed comparison of how documentation requirements differ between manual and AI-assisted compliance programs, Manual Compliance vs. AI Automation covers the tradeoffs your compliance team should understand before the next exam cycle.

Agentic AI and the Future of Exam-Ready AML Compliance

Institutions consistently passing FFIEC exam AI systems reviews with minimal findings share a common trait: their AI systems are designed to be auditable from day one, not retrofitted for exam readiness after the fact. Agentic AI systems that maintain their own decision logs, flag model drift in real time, and produce on-demand performance reports give compliance officers the evidence they need without a pre-exam documentation sprint. According to NIST's AI Risk Management Framework, trustworthy AI requires continuous monitoring, measurement, and transparency, which is precisely what examiners expect to see documented in your AML systems.

- Three things converged to put AI squarely in the examiner's crosshairs this cycle.

- AML compliance in 2026 is not evaluated in isolation from the technology delivering it.

- The bsa aml compliance checklist for AI-assisted programs differs from the traditional version in one key way: the examiner also wants controls on the controls.

- KYC automation has matured significantly, and examiner expectations have matured with it.

- SAR filing efficiency is an area where examiners have become notably granular.

Onboard Customers in Seconds

Conclusion

FFIEC exam AI systems scrutiny will get more specific from here, not less. The institutions that pass exams cleanly are not those with the most sophisticated AI. They are the ones who can explain their AI in writing, trace every material decision to a documented rationale, and show that humans govern the systems rather than the other way around. The bsa aml compliance checklist for AI is longer than it was three years ago, but the underlying principle has not changed: your institution owns every decision your AI makes, and you need records to prove it. Start with your model inventory, close the validation gap, and build the alert management documentation that lets your AML compliance program speak for itself when the examiner arrives.

Share this article