.webp)

Introduction

The enhanced due diligence EDD guide most compliance teams need is not the one their BSA officer wrote five years ago. In 2026, regulators expect financial institutions to do more than run a name through a sanctions database and call it done. Standard KYC catches the obvious risks. EDD is what you do when the obvious isn't enough and the stakes are too high to guess.

This post breaks down when EDD is required, how to build a defensible process, and what aml compliance software and anti money laundering technology actually help versus what is just expensive noise. Whether you are at a large bank, a fintech, or a community institution with a lean compliance function, the framework here applies.

- What Is Enhanced Due Diligence and Why Standard KYC Falls Short

- The AML Compliance Framework: Where EDD Fits In

- How to Build an EDD Process That Survives Regulatory Scrutiny

- AML Risk Assessment Guide: Scoring Customers for Enhanced Review

- SAR Filing Best Practices When EDD Uncovers Red Flags

Onboard Customers in Seconds

What Is Enhanced Due Diligence and Why Standard KYC Falls Short

Enhanced due diligence (EDD) is a deeper level of customer verification applied to individuals or entities that carry elevated money laundering, fraud, or sanctions risk. Where standard customer due diligence (CDD) collects identity documents and screens against watchlists, EDD investigates the source of funds, beneficial ownership structures, geographic risk, and transaction patterns before and after onboarding.

The gap between KYC and EDD is not just procedural. It is the difference between checking who someone is and understanding where their money comes from.

Standard KYC vs. Enhanced Due Diligence: Key Differences

Standard KYC satisfies the identity verification requirement under the Bank Secrecy Act and FinCEN's Customer Due Diligence Rule. It answers: Is this person who they say they are? EDD answers the harder question: Is this person's money legitimate, and does their intended activity make sense given their stated profile?

The practical difference shows up in what you collect. Standard KYC: government ID, address, date of birth, SSN. EDD: source of wealth documentation, business ownership structures, expected transaction volumes, third-party references, and enhanced screening against adverse media.

KYC CDD Requirements for Banks: The Baseline Before EDD

Under the kyc cdd requirements for banks, all customers must go through standard CDD at account opening. This means verifying identity, understanding the nature and purpose of the relationship, and implementing ongoing monitoring for suspicious activity. EDD is triggered on top of that baseline for customers who fall into high-risk categories defined in your written program.

The common mistake is treating EDD as a one-time event. A customer who passed EDD three years ago but whose transaction volume has tripled without explanation is a problem. Regulators want to see refresh cycles, updated risk scores, and clear escalation paths when something changes.

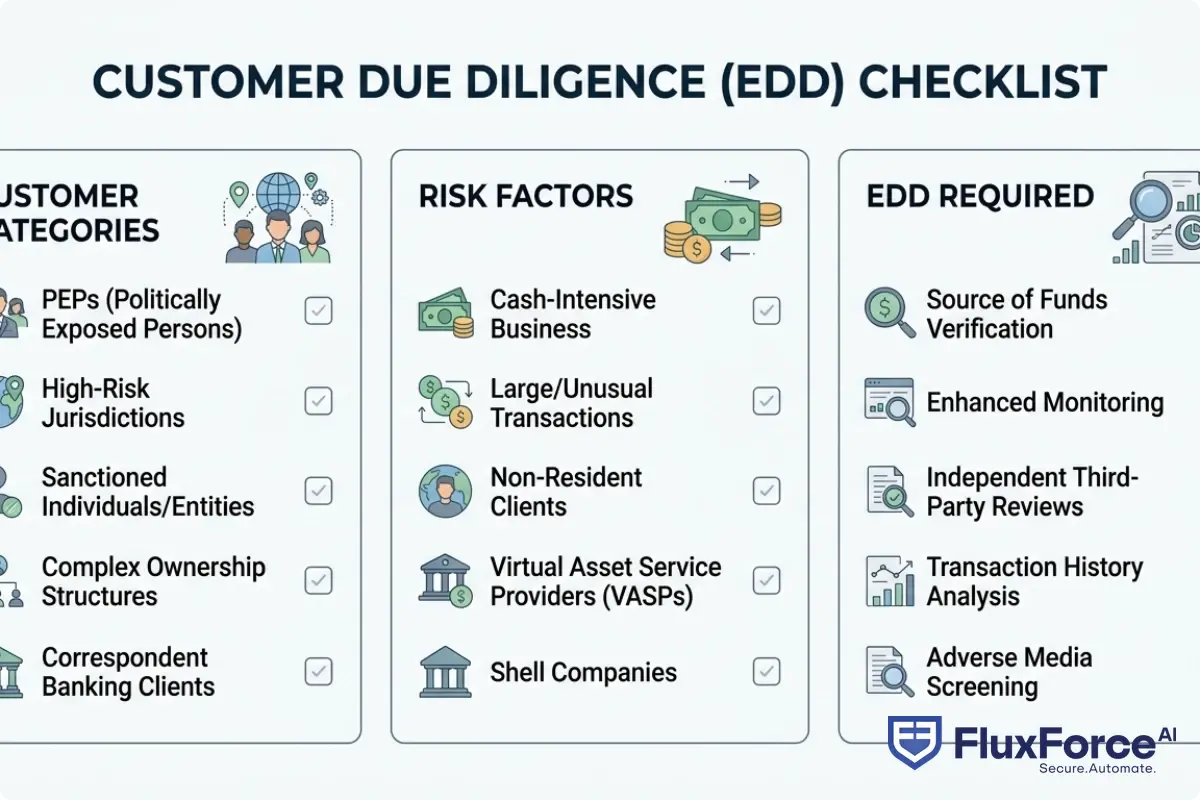

Who Triggers Enhanced Due Diligence?

Not every customer needs EDD, and over-applying it burns compliance resources. EDD is typically required for:

- Politically exposed persons (PEPs) and their close associates

- Customers from high-risk jurisdictions on the FATF grey or black list

- Non-bank financial institutions, money services businesses, and correspondent banks

- Customers with complex or opaque beneficial ownership structures

- High-net-worth individuals with no clear documented source of wealth

- Cash-intensive businesses like car dealerships, restaurants, or cannabis-adjacent services

The AML Compliance Framework: Where EDD Fits In

AML compliance is not a single control. It is a system of overlapping requirements under the Bank Secrecy Act, FinCEN regulations, OFAC sanctions rules, and the EU's AML directives. EDD is one component, tied specifically to the risk-based approach required by all of these frameworks.

The risk-based approach means your institution does not apply the same scrutiny to every customer. You identify where the real risk sits and concentrate resources there. EDD is how you operationalize that concentration for your highest-risk accounts.

BSA AML Compliance Checklist: The Five Pillars

A complete bsa aml compliance checklist covers five program pillars required by FinCEN:

- Internal policies, procedures, and controls

- A designated BSA/AML compliance officer

- Ongoing employee training

- Independent testing and internal audit

- Customer due diligence, including beneficial ownership and EDD for high-risk customers

EDD does not exist in isolation. A gap in any of the other four pillars undermines even a thorough EDD process. If your training does not teach relationship managers to recognize EDD triggers, the documentation never gets collected.

AML Compliance Fintech: Regulatory Expectations vs. Reality

AML compliance in fintech carries a specific tension. Fintechs often serve customer segments that traditional banks have underserved, which means higher proportions of customers with thin credit files, non-traditional income sources, or international transaction patterns. Standard risk models trained on traditional banking data generate high false positive rates in these populations.

FinCEN's guidance on compliance innovation explicitly acknowledges that BSA obligations should not inhibit experimentation with new compliance technologies. The expectation is documented, risk-based reasoning that an examiner can follow. AML screening in digital lending shows how continuous monitoring catches what point-in-time checks miss, which matters for both EDD refresh decisions and SAR filing timelines.

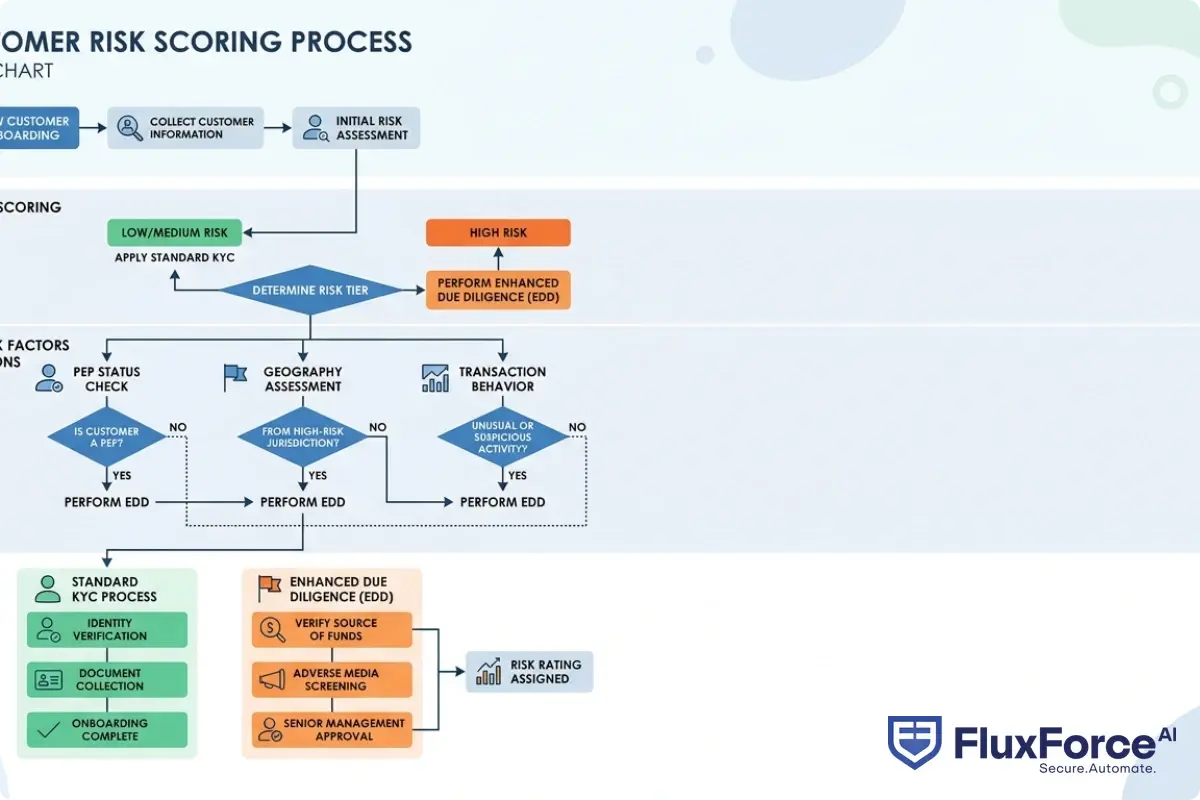

How to Build an EDD Process That Survives Regulatory Scrutiny

A defensible EDD process has three phases: identification, collection, and ongoing review. Missing any one of them is what draws examination findings. The institutions that survive exams cleanly are not the ones with the most sophisticated technology. They are the ones who can show a clear paper trail from risk identification through documentation through review decision.

Step 1: Define Your High-Risk Customer Categories in Writing

Before you can apply EDD, you need a written definition of who requires it. In practice, many institutions have informal trigger lists that live in one person's head or in a policy document last updated in 2021.

Your aml risk assessment guide approach should map customer types, products, geographies, and channels to risk tiers, with clear criteria for what moves a customer from standard CDD to EDD. The mapping should be reviewable by examiners, updated annually, and approved at board or senior management level. If you cannot point to the policy that required EDD for a specific customer, that EDD documentation is less defensible.

Step 2: Collect Enhanced Documentation and Understand the Business

EDD documentation goes beyond identity verification. For a PEP customer, you are investigating source of wealth: where did this person accumulate their assets, and does the amount make sense given their career history? For a correspondent bank, you need due diligence on their own AML program, customer base, and jurisdictions. For a cash-intensive business, you want to understand expected deposit volumes and how the business reconciles cash intake against reported revenue.

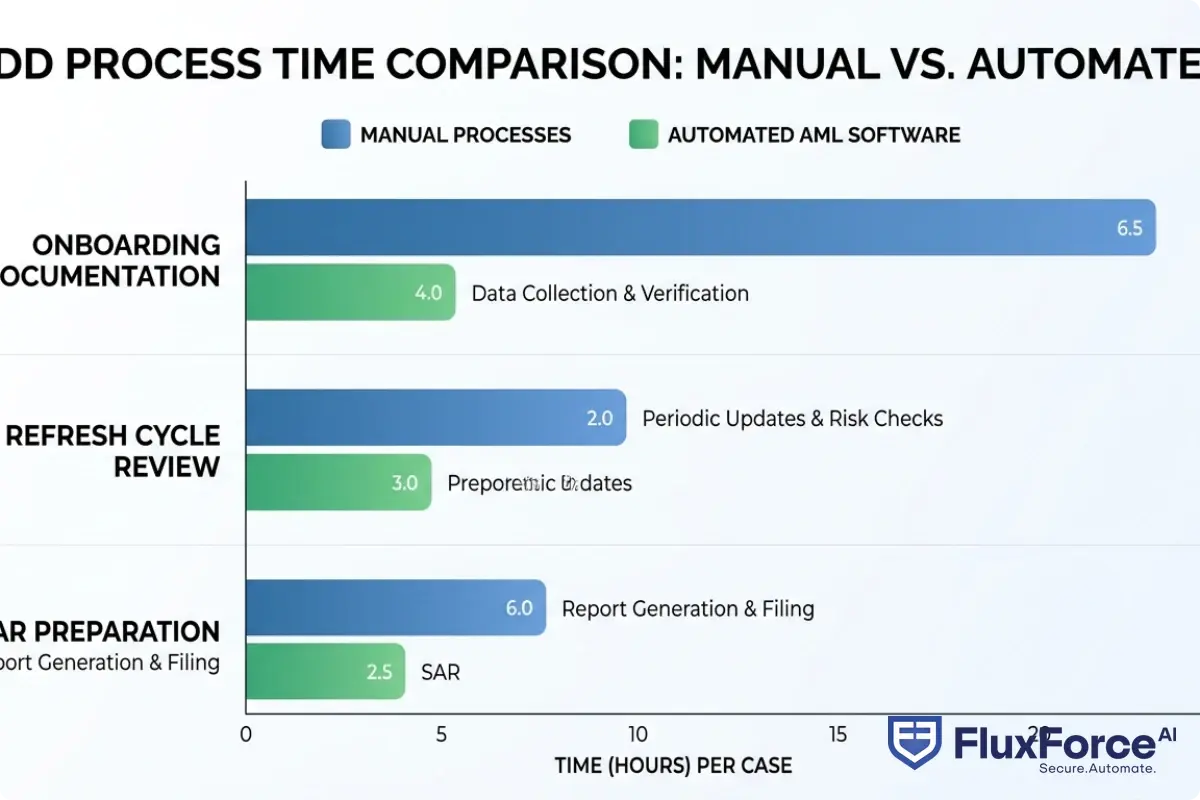

For complex customers, EDD can take two to six weeks to complete properly. Compliance teams under pressure to onboard quickly often shortcut this step. That shortcut is precisely what regulators find.

Step 3: Build Ongoing Monitoring Into the EDD Workflow

Most institutions set refresh cycles based on risk tier: high-risk customers reviewed annually, medium-risk every two to three years. But static schedules miss the point. A trigger-based refresh, such as an unusual transaction spike, adverse media hit, or change in beneficial ownership, is more effective than a calendar reminder.

This is where kyc automation starts to pay off. Manual refresh tracking across thousands of EDD customers is error-prone. Automated alerts tied to transaction monitoring thresholds let you catch material changes when they happen, not 18 months later at the next scheduled review.

AML Risk Assessment Guide: Scoring Customers for Enhanced Review

An aml risk assessment guide for EDD purposes needs to be more specific than high, medium, or low. Examiners want to see which factors drive the risk score and how those factors are weighted. Generic risk tiering without documented methodology is a finding waiting to happen.

Building a Risk Scoring Matrix for EDD

A practical risk matrix covers four dimensions: customer type (individual vs. entity, PEP status, beneficial ownership complexity), geography (country of residence, transaction origin, FATF standing), product and channel (wire transfers carry more risk than savings accounts; digital-only onboarding with no face-to-face verification carries more risk than branch transactions), and transaction behavior (volume, frequency, cash intensity, cross-border activity relative to stated purpose).

Each dimension gets a score, and aggregate scores above a threshold trigger EDD. The threshold should be calibrated against your institution's risk appetite, documented in your BSA/AML program, and revisited annually. Detecting synthetic identity fraud in real-time shows how real-time data feeds change the detection equation. The same applies to EDD risk scoring: you want signals flowing continuously, not just at the annual review.

Fintech BSA AML Small Team: Making EDD Work With Limited Resources

A fintech BSA AML small team often has two or three compliance staff covering everything from onboarding to SAR filing to exam prep. A risk scoring matrix requiring manual quarterly review of 10,000 customers is not feasible.

The answer is not to lower the bar. It is to automate signal collection and escalation logic so human reviewers only look at accounts that genuinely need judgment. A well-configured aml compliance software platform can reduce manual review workload by 60 to 70 percent without reducing coverage. Remaining analyst time goes to complex ownership structures, PEP relationships, and SAR-filing decisions.

A well-configured aml compliance software platform can reduce manual review workload by 60 to 70 percent without reducing coverage.

SAR Filing Best Practices When EDD Uncovers Red Flags

EDD is often how you get to a SAR. The documentation and monitoring you have collected reveals transaction patterns that cannot be explained by the customer's stated purpose. At that point, sar filing best practices determine how defensible the filing is when examined.

SAR Filing Requirements 2026: What Has Changed

SAR filing requirements in 2026 reflect FinCEN's push for higher-quality narratives and clearer typology analysis. The 30-day filing window (60 days when no suspect is identified) has not changed. What has changed is examiner expectations around narrative quality. A SAR that says the customer made multiple cash deposits without explaining why that is suspicious, what pattern was observed, and what investigation preceded the filing is increasingly flagged.

FinCEN's SAR activity review and guidance materials make clear that SARs should function as self-contained investigative documents. An examiner reading the SAR should understand what happened, why it was suspicious, and what your institution did before filing.

SAR Filing Efficiency: Reducing the Time from Detection to Filing

SAR filing efficiency matters because the clock starts when the institution detects suspicious activity. Delays in case assignment, investigation, and narrative drafting eat into the 30-day window. Institutions that routinely file at day 28 or 29 are either very disciplined or very stressed.

Case management systems that pre-populate subject information, transaction data, and typology flags from the monitoring system cut 30 to 40 percent of narrative drafting time. A suspicious activity report guide built into your workflow templates standardizes narrative structure across analysts and improves consistency when examiners review SAR quality.

Anti Money Laundering Technology 2026: Tools That Make EDD Scalable

Anti money laundering technology in 2026 has moved well past rules-based transaction monitoring. Machine learning models, network analysis, and natural language processing for adverse media screening are now standard at mid-size and large institutions. The question is not whether to use these tools but how to configure them for your risk profile and document their use in a way that satisfies examiners.

AML Compliance Software: What to Look for in 2026

Good aml compliance software in 2026 ingests real-time transaction data rather than running overnight batch jobs, performs entity resolution across multiple data sources to surface hidden account relationships, and automates the administrative parts of EDD workflows so analysts focus on judgment rather than administration.

The eu ai act financial services provisions classify most AML risk scoring systems as high-risk AI under Article 6, requiring documentation, human oversight mechanisms, and bias testing before deployment. For institutions serving EU markets, this directly affects how AI-assisted EDD systems are configured and audited. Sanctions screening automation implementations show how to structure the audit trail regulators now expect from AI-driven compliance decisions.

KYC Automation 2026: From Manual Review to AI-Assisted Decisions

KYC automation in 2026 means AI-assisted document verification, automated beneficial ownership extraction from corporate registries, and risk scoring that updates as transaction data flows in. Institutions that have implemented this properly report 40 to 50 percent reductions in onboarding time for standard CDD, freeing analyst capacity for EDD cases that need human judgment.

Institutions that have implemented this properly report 40 to 50 percent reductions in onboarding time for standard CDD, freeing analyst capacity for EDD cases that need human judgment.

The risk of over-automating is real. How agentic AI fraud agents cut false positives by 80% shows where human review remains essential: any case that could generate a SAR still needs analyst sign-off, and any EDD decision affecting a customer relationship needs documented human reasoning, not just an algorithm output.

EDD for Fintechs and Community Banks: Different Scale, Same Stakes

The regulatory obligations for EDD are the same whether you are a $100M community bank or a fintech processing $2B in annual payment volume. The implementation looks completely different, and neither environment is easier than the other.

The regulatory obligations for EDD are the same whether you are a $100M community bank or a fintech processing $2B in annual payment volume.

BSA AML Compliance Community Banks: Unique Challenges

BSA AML compliance at community banks faces a specific problem: examiner expectations calibrated for large institutions do not always translate sensibly to a bank with one BSA officer and no dedicated technology budget. The FFIEC BSA/AML Examination Manual acknowledges risk-based scaling, but in practice, community banks face documentation requirements that assume more staff and technology than most have.

The practical answer is to be exceptionally clear in your written program about what your institution can and cannot do with current resources, and what compensating controls are in place. Examiners can work with documented limitations. They struggle with undocumented gaps.

CTR Filing Rules: Automation That Prevents Missed Filings

CTR filing rules require Currency Transaction Reports for cash transactions above $10,000 within a business day, with aggregation required across multiple transactions by the same customer. For lean compliance teams, manual CTR tracking creates gaps, especially in branch environments where transactions are spread across tellers or across morning and afternoon sessions.

Automated CTR generation tied to the core banking system eliminates this risk, but only if the aggregation logic is correctly configured and tested. An automated system that does not aggregate properly is worse than a manual process because it creates a false sense of compliance. AML risk checks in policy issuance shows how automated AML workflows reduce manual workload in adjacent regulated contexts, with architecture decisions directly applicable to EDD and CTR automation in banking.

- Enhanced due diligence (EDD) is a deeper level of customer verification applied to individuals or entities that carry elevated money laundering, fraud, or sanctions risk.

- AML compliance is not a single control.

- A defensible EDD process has three phases: identification, collection, and ongoing review.

- An aml risk assessment guide for EDD purposes needs to be more specific than high, medium, or low.

- EDD is often how you get to a SAR.

Onboard Customers in Seconds

Conclusion

The enhanced due diligence EDD guide your institution actually needs is one built around your real risk profile, not a template copied from a larger bank's program. EDD is not a checkbox exercise. It is the operational expression of your risk-based aml compliance program, and regulators can tell the difference between documentation that exists on paper and documentation that reflects actual institutional understanding.

The practical priorities are clear: define high-risk customer categories in writing, document your risk scoring methodology in a form examiners can follow, build refresh cycles that respond to triggers rather than just calendars, and invest in aml compliance software that reduces the administrative burden without creating new regulatory gaps. The institutions that stay ahead treat EDD as a risk management tool, not a regulatory tax.

If you are assessing where your current EDD program has gaps, Manual Compliance vs. AI Automation is a useful starting point for identifying where technology can replace manual processes without creating new examination exposure.

Share this article