.webp)

Introduction

AI fraud detection has become the operational backbone of enterprise risk management, replacing rule-based systems that can no longer keep pace with sophisticated fraud networks, real-time payment rails, and regulatory demands spanning dozens of jurisdictions simultaneously.

Volume is one challenge. The real difficulty is complexity. A bank handling cross-border wire transfers faces OFAC screening obligations, PCI DSS encryption mandates, FFIEC model risk governance requirements, and AML reporting duties, all in the same transaction window. Legacy systems weren't built for this. AI was.

This guide covers the essential features that compliance officers, CISOs, and risk teams need to evaluate when selecting or upgrading AI fraud detection infrastructure, with practical depth on real-world deployment challenges.

- What Is AI Fraud Detection and Why Enterprise Risk Teams Need It Now

- Core Features of Enterprise-Grade AI Fraud Detection Systems

- OFAC Screening Integration and AML Compliance Automation

- KYC Verification Systems and Biometric Identity Verification

- Zero Trust Security Architecture for Open Banking APIs

Onboard Customers in Seconds

What Is AI Fraud Detection and Why Enterprise Risk Teams Need It Now

AI fraud detection is the application of machine learning, behavioral analytics, and real-time pattern recognition to identify fraudulent transactions, synthetic identities, and anomalous account behavior before financial losses or regulatory violations occur.

The shift from rule-based to AI-driven detection is a regulatory and operational necessity. FATF's guidance on digital assets and virtual asset service providers explicitly expects institutions to apply risk-based, technology-assisted monitoring rather than static rule libraries that cannot adapt to evolving fraud patterns.

Financial Risk Scoring vs. Rule-Based Detection

Traditional fraud detection assigns hard thresholds: flag any wire over $10,000, block any transaction from a high-risk country. Financial risk scoring via AI is more granular. It assigns probability scores based on hundreds of real-time variables including device fingerprint, typing cadence, geolocation drift, merchant category mismatch, and account velocity.

Traditional fraud detection assigns hard thresholds: flag any wire over $10,000, block any transaction from a high-risk country.

The honest answer about rule-based systems is that they made sense in 2005 when fraud patterns were stable. They don't work now. Fraudsters specifically engineer their behavior to stay below static thresholds, which is precisely why fixed-rule detection misses the fraud that matters most.

Compliance Automation Benchmarks 2026

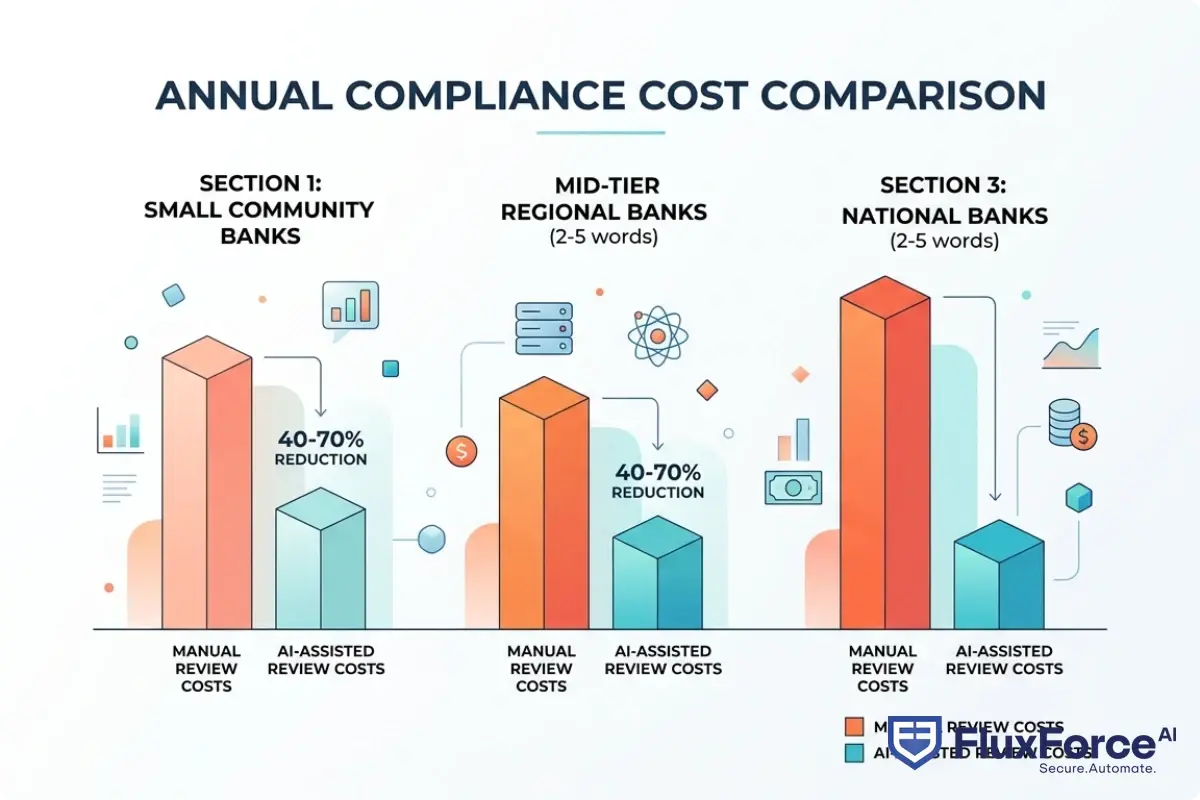

Institutions that moved to AI-assisted AML monitoring are seeing a 40-60% reduction in manual review hours and a 25-35% improvement in SAR filing accuracy, according to compliance automation benchmarks from 2026 production deployments at mid-tier banks and RegTech-enabled credit unions.

The benchmark that matters most for enterprise risk teams: mean time-to-detection for account takeover. AI systems with real-time scoring typically reduce this from 3.2 days to under 4 hours, based on international banking risk standards benchmarks from institutions that have completed full AI migration cycles.

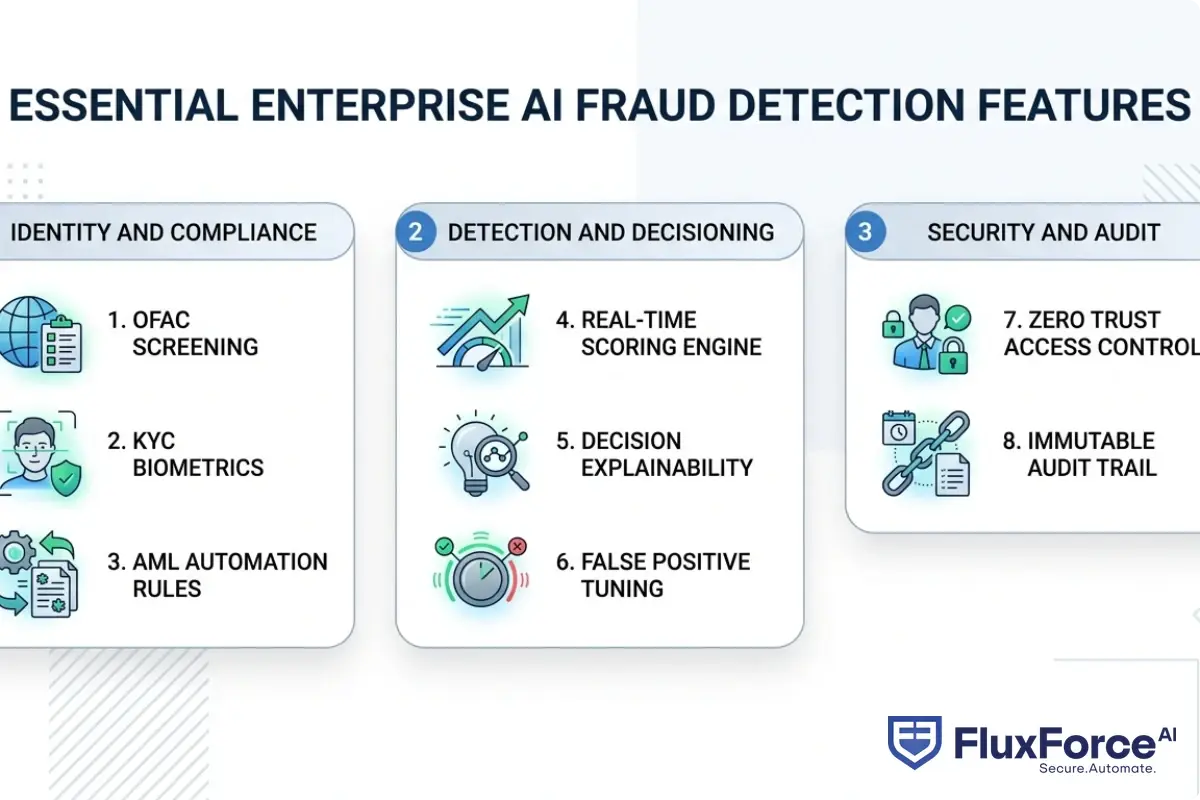

Core Features of Enterprise-Grade AI Fraud Detection Systems

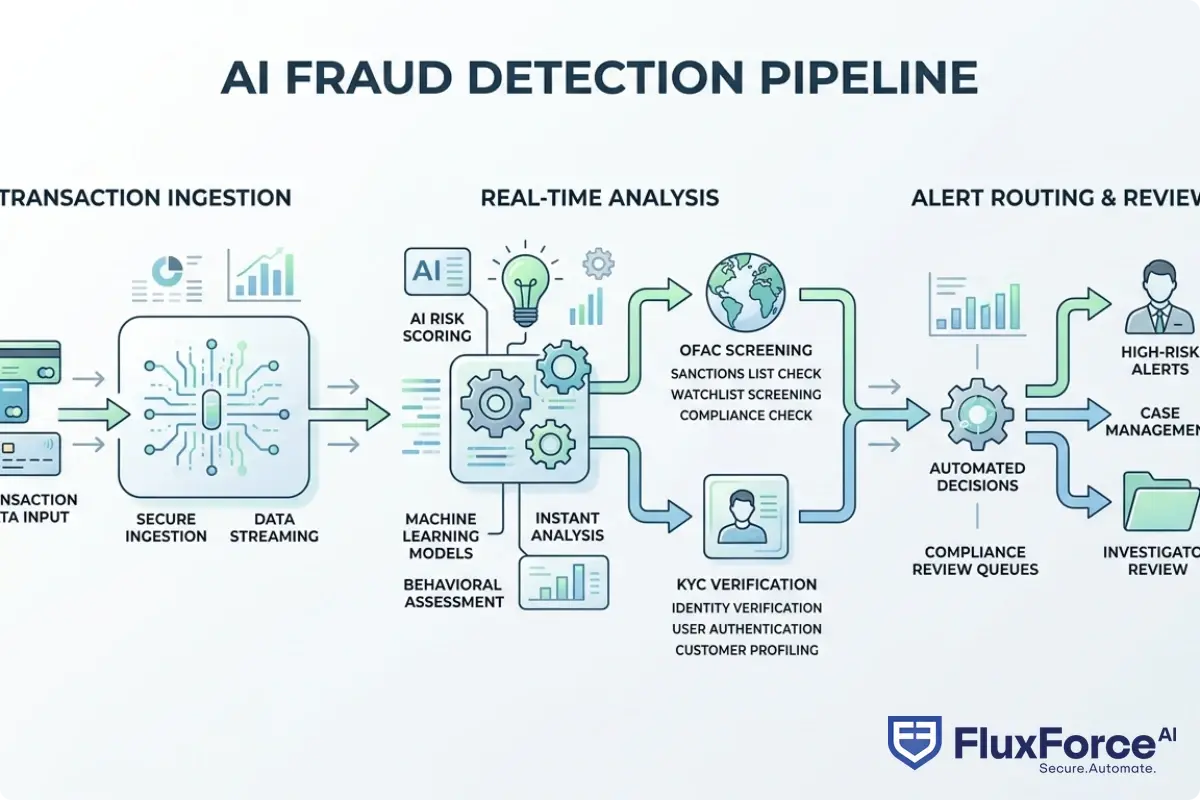

An enterprise-grade AI fraud detection platform needs more than a machine learning model. It needs a full stack of interconnected capabilities that work across transaction types, channels, and regulatory regimes.

Real-Time Transaction Monitoring at Scale

Real-time transaction monitoring is the foundation. The system must evaluate each transaction in under 200 milliseconds to avoid payment rail SLA violations, while still running against entity resolution databases, watchlists, and behavioral profiles.

This gets tricky when processing SWIFT MT103s alongside domestic ACH batches and crypto on-chain transfers simultaneously. Each payment rail has different data fields and timing constraints. Native AI platforms built for multi-rail environments perform measurably better than legacy systems with bolted-on adapters.

For deeper analysis of how AI monitoring applies to card transactions specifically, this breakdown of AI-powered card fraud detection strategy covers the real-time scoring architecture in detail.

How to Reduce False Positives in Transaction Monitoring

False positive fraud alerts cost real money. Each manually reviewed alert costs between $12 and $40 in analyst time. An institution generating 50,000 alerts per month with a 95% false positive rate burns up to $1.9 million annually on friction that produces no fraud catches.

Each manually reviewed alert costs between $12 and $40 in analyst time.

How to reduce false positives in transaction monitoring starts with layered scoring: a fast initial model screens clearly legitimate transactions, a secondary model handles ambiguous cases, and a tertiary model processes high-value or novel-pattern transactions. This tiered approach typically brings false positive rates below 10% without increasing missed fraud rates. Compliance workflow automation is where this tiered model delivers its clearest operational value.

Agentic AI systems have demonstrated 80% false positive reductions in production environments, translating directly to analyst capacity freed for genuine risk investigation.

Agentic AI systems have demonstrated 80% false positive reductions in production environments, translating directly to analyst capacity freed for genuine risk investigation.

Financial Risk Scoring and Behavioral Analytics

Financial risk scoring goes beyond transaction-level checks. Behavioral analytics builds a baseline of normal activity for each customer: typical transaction amounts, geographic patterns, login times, and device consistency. Deviations trigger elevated risk scores, not automatic blocks.

A customer traveling internationally shouldn't have every transaction blocked. But a customer whose account shows a new device, a new geolocation, and three large wire transfers in 90 minutes should score very high and trigger a human review step before processing continues.

OFAC Screening Integration and AML Compliance Automation

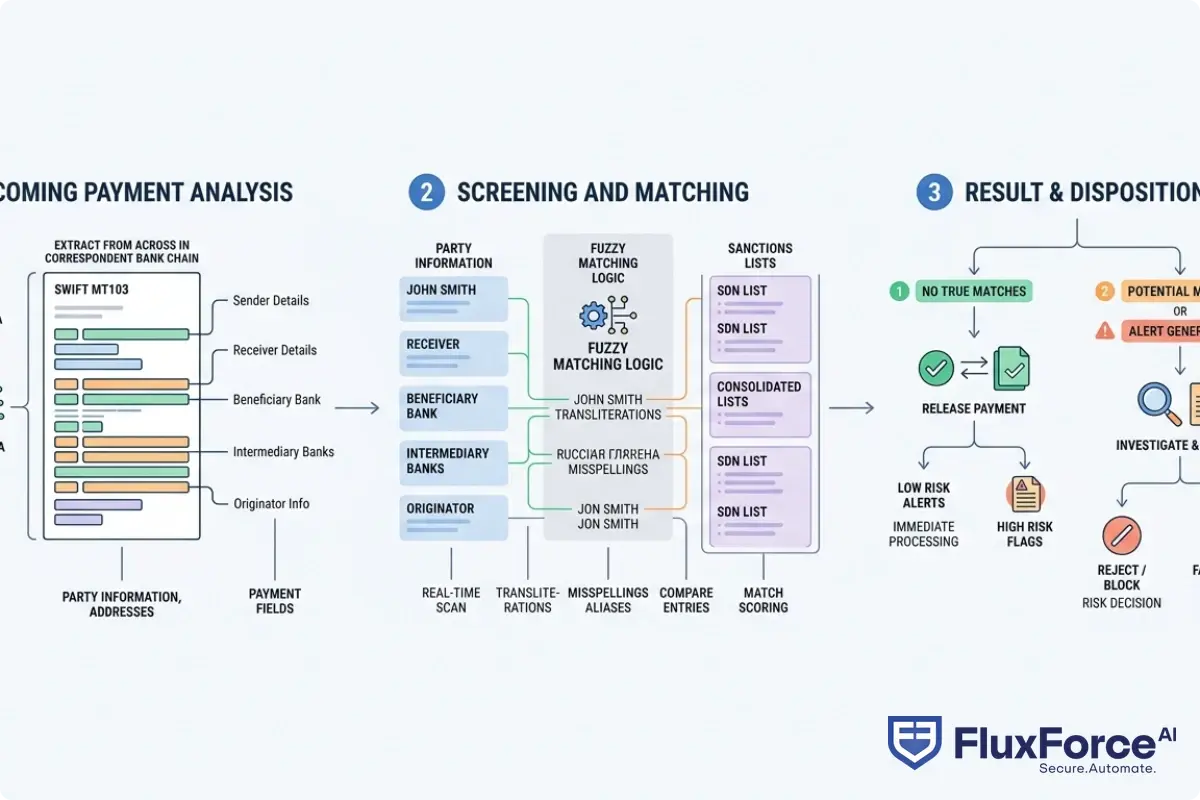

OFAC screening integration is non-negotiable for any U.S.-regulated financial institution or foreign bank with U.S. dollar correspondent relationships. The U.S. Treasury's OFAC division maintains sanctions lists that must be checked against every transaction party, including beneficial owners, intermediary banks, and end beneficiaries.

OFAC Watchlist Integration Requirements for Financial Institutions

OFAC watchlist integration requirements for financial institutions extend well beyond checking names against the SDN list. Institutions must screen across multiple lists including SDN, Consolidated Sanctions List, CAPTA, and Sectoral Sanctions Identifications, apply fuzzy matching logic to catch spelling variations and transliterations, and process the full transaction graph.

A common gap: many institutions screen named parties but miss the correspondent bank chain in SWIFT messages. An automated OFAC screening system should parse MT103 fields 52, 56, 57, and 58 for all intermediary institutions and check each against current lists in real time.

How to Integrate OFAC Screening into Crypto On-Ramp Workflows

Blockchain transactions don't carry the same structured counterparty data as traditional wire transfers. How to integrate OFAC screening into crypto on-ramp workflows requires screening wallet addresses against OFAC's published virtual currency addresses, but that alone isn't sufficient for compliance.

Best AI fraud detection tools for cryptocurrency exchanges now incorporate on-chain analytics to trace fund flows across multiple hops, identify mixing service usage, and flag transactions where funds originate from OFAC-sanctioned wallets even after several intermediate transfers. This requires integrating blockchain analytics APIs alongside traditional OFAC list checks.

Geographic OFAC Risk Mapping for High-Risk Jurisdictions

Geographic OFAC risk mapping for high-risk jurisdictions assigns tiered risk scores to countries based on OFAC program coverage, FATF grey and black list status, Financial Secrecy Index rankings, and correspondent banking withdrawal patterns.

This mapping feeds directly into AML compliance automation rules: transactions touching Tier 3 jurisdictions trigger enhanced due diligence workflows automatically, without waiting for a compliance analyst to manually notice a country code in a payment instruction.

KYC Verification Systems and Biometric Identity Verification

KYC verification systems sit at the front of the fraud prevention chain. A customer who passes thorough identity verification at onboarding is significantly less likely to be a synthetic identity or a money mule account. AI-powered KYC resolves the friction tradeoff better than manual document review.

For a detailed treatment of how KYC and AML checks apply in complex onboarding scenarios, see this guide to KYC/AML verification strategy for claims directors, which covers identity verification patterns directly applicable to banking onboarding contexts.

Biometric Liveness Detection Threat Modeling Guide

A biometric liveness detection threat modeling guide should be standard documentation for any institution deploying face verification or document selfie matching. The threat model covers three primary attack vectors: injection attacks (feeding pre-recorded video to the verification API), adversarial deepfakes (AI-generated faces that defeat static liveness checks), and physical artifact attacks (3D-printed masks or printed photos).

Production-grade liveness detection uses active challenges (randomized movement prompts) combined with passive analysis including micro-expression detection and skin texture analysis. No single method defeats all attack vectors. Defense requires layering multiple techniques, and your threat model needs to account for the specific attack sophistication of your customer base.

Best AI Fraud Detection Tools for Cryptocurrency Exchanges

Best AI fraud detection tools for cryptocurrency exchanges need to handle transaction monitoring across multiple chains, wallet clustering, smart contract interaction analysis, and Travel Rule reporting under FinCEN guidelines. The key differentiator isn't blockchain data coverage. It's how well the tool integrates blockchain risk signals with off-chain customer profile data from your KYC verification systems.

Exchanges that run blockchain analytics in isolation from core customer risk profiles miss correlated risk indicators. A customer whose on-chain behavior looks borderline but whose KYC profile, device fingerprint, and IP history all show anomalies should score much higher than any single data source would suggest independently.

Zero Trust Security Architecture for Open Banking APIs

Zero trust security architecture for open banking APIs means no API call is trusted by default, regardless of network origin. Under open banking frameworks like PSD2 in Europe and equivalent standards in Asia-Pacific, third-party providers gain access to customer data and payment initiation through standardized APIs. Zero trust controls every access grant at every request.

For implementation depth on zero trust in banking environments, this zero trust security architecture strategy for banking CISOs covers the architectural decisions and access control design in detail.

Zero Trust Identity Architecture for Open Banking APIs

Zero trust identity architecture for open banking APIs requires continuous authentication, not session-based trust. Each API call must carry a verifiable credential proving identity, authorization scope, and request freshness. Mutual TLS (mTLS) between service endpoints prevents token replay attacks that would otherwise allow session hijacking across open banking connections.

According to NIST SP 800-207 on zero trust architecture, organizations should treat all network traffic as untrusted and enforce per-request authentication at every layer. The practical challenge is certificate rotation: in high-volume payment environments, rotation must be automated and zero-downtime. Manual rotation processes create gaps that attackers reliably exploit.

PCI DSS Encryption Requirements for International Wire Transfers

PCI DSS encryption requirements for international wire transfers extend beyond cardholder data to any payment credential crossing network boundaries. PCI DSS 4.0 mandates TLS 1.2 minimum, with TLS 1.3 strongly recommended for all data in transit, along with specific requirements for key management and certificate authority trust chains.

The migration from legacy TLS 1.0 and 1.1 implementations remains incomplete at many institutions, particularly those running mainframe-based payment processing. This is a documented examination finding in OCC and Federal Reserve reviews, and examiners are increasingly flagging it as a priority remediation item.

AI Agent Governance Human-in-the-Loop Controls for Finance

AI agent governance human-in-the-loop controls for finance is a fast-emerging requirement as institutions deploy autonomous AI agents for transaction decisions. The core principle: no AI agent should have final authority over high-consequence financial actions without a human approval checkpoint at the appropriate risk threshold.

This reflects FFIEC model risk management expectations from the 2023 guidance updates, which require institutions to document escalation paths, override capabilities, and human review requirements for automated decision systems. Institutions that build this documentation proactively spend far less time defending their AI governance posture during examinations.

How AI Fraud Detection Supports FFIEC Examination Readiness

AI fraud detection systems that aren't examination-ready create regulatory risk even when they perform well operationally. Examiners don't just care whether fraud is caught. They care whether the institution can explain how the system works, demonstrate independent validation, and show that human oversight operates exactly as documented.

FFIEC Examination Preparation Documentation Framework

A FFIEC examination preparation documentation framework for AI systems should include model inventory documentation, validation reports showing in-sample and out-of-sample performance metrics, alert disposition logs, model drift monitoring reports, and human override records. This is the minimum expected under SR 11-7 model risk management guidance, as maintained by the Federal Financial Institutions Examination Council.

Institutions that build these documentation layers into their AI fraud detection platforms from the start spend significantly less time preparing for examinations. Those that treat documentation as an afterthought face reconstruction projects that consume months of compliance team bandwidth right before exam windows open.

Real-Time Fraud Pattern Monitoring for AI Models

Real-time fraud pattern monitoring for AI models differs from real-time transaction monitoring. It means monitoring the model itself: tracking whether input data distribution is drifting, whether alert rates are shifting without corresponding changes in confirmed fraud, and whether specific customer segments are being scored differently than during model training.

AML compliance automation for Series A RegTech startups often skips this monitoring layer due to resource constraints. That's a mistake with measurable consequences. A model accurate during validation can degrade significantly if fraud patterns shift and the model isn't retrained or monitored for drift between examination cycles.

Measuring the ROI of Compliance Workflow Automation

Compliance workflow automation delivers measurable financial returns, but the numbers only appear when you measure the right inputs. Most institutions track automation cost accurately but undercount the full operational cost of manual processes they're replacing.

Regulatory Compliance ROI Calculator for Banks

A regulatory compliance ROI calculator for banks should account for analyst hours recaptured from manual review, SAR filing error rates and amendment costs, examination preparation time, and avoided regulatory penalties. When you include examination prep time (typically 3-6 months of analyst bandwidth annually at mid-sized institutions), the ROI on automation typically exceeds 300% within 18 months.

The variable that changes the calculation most is false positive rate. Every 10-percentage-point reduction in false positive fraud alerts at a mid-tier bank handling 100,000 monthly flagged transactions saves roughly $120,000 to $400,000 per year in analyst time alone. Multiply that by improved examination outcomes and reduced penalty exposure, and the financial case becomes straightforward.

For a direct comparison of manual compliance versus AI automation across cost, accuracy, and scalability dimensions, this analysis of manual compliance vs. AI automation breaks down the tradeoffs with operational data from regulated institutions.

- AI fraud detection is the application of machine learning, behavioral analytics, and real-time pattern recognition to identify fraudulent transactions, synthetic identities, and anomalous account behavior before financial losses or regulatory violations occur.

- An enterprise-grade AI fraud detection platform needs more than a machine learning model.

- OFAC screening integration is non-negotiable for any U.S.-regulated financial institution or foreign bank with U.S.

- KYC verification systems sit at the front of the fraud prevention chain.

- Zero trust security architecture for open banking APIs means no API call is trusted by default, regardless of network origin.

Onboard Customers in Seconds

Conclusion

AI fraud detection isn't a single product you deploy and forget. It's a stack of capabilities that need to work together: real-time transaction monitoring, OFAC screening integration, KYC verification systems, zero trust security architecture, and documentation frameworks that satisfy FFIEC examination standards.

The institutions getting the most from AI fraud detection treat it as compliance infrastructure investment, not just a fraud reduction tool. They build for explainability from day one, instrument their models for drift monitoring, and establish human-in-the-loop controls before regulators require them.

If your team is evaluating AI fraud detection vendors right now, start with four questions: Can the system explain every decision in terms an auditor can read? Does it integrate OFAC screening natively? What is the documented false positive rate at your transaction volume? How does it handle model drift between validation cycles? The answers will narrow the field quickly and reveal which vendors actually understand AML compliance automation versus which ones just claim to.

Share this article