.webp)

Introduction

When AI model documentation regulators walk into an exam, they're not looking for a binder full of flowcharts. They want evidence that your institution actually understands what its AI systems do, why they make the decisions they make, and what happens when things go wrong. The gap between "we have documentation" and "we have documentation that satisfies an examiner" is wider than most compliance teams realize until it's too late.

This is especially true in 2026, as the EU AI Act's phased requirements take effect and U.S. prudential regulators have started asking pointed questions about model governance that go well beyond traditional SR 11-7 guidance. Whether you're a community bank running a single AML screening tool or a large fintech with dozens of ML models in production, the documentation bar has moved significantly. Here's what examiners are actually looking for.

- Why AI Documentation Has Become a Regulatory Priority

- What AI Model Documentation Regulators Actually Require

- Model Risk Management for AML and KYC Systems

- SAR Filing and CTR Automation: What Documentation Must Cover

- The EU AI Act and What It Means for AI Documentation in Financial Services

Onboard Customers in Seconds

Why AI Documentation Has Become a Regulatory Priority

The shift started before the EU AI Act. U.S. bank examiners from the OCC, Federal Reserve, and FDIC have been applying SR 11-7 guidance (the Federal Reserve's landmark model risk management framework) to AI systems since at least 2020. Enforcement has accelerated.

In 2024, the OCC issued examination guidance explicitly addressing machine learning models used in credit underwriting and aml compliance. The message was clear: models that make consequential decisions need documentation that an independent reviewer, not just the team that built the model, can follow.

The honest answer for why documentation matters more now is that regulators have gotten smarter about AI. Examiners are no longer satisfied with high-level architecture diagrams. They want training data provenance, validation test results, performance monitoring logs, and a clear change management trail. Institutions that assumed their existing model governance policies covered AI have been surprised by the specificity of examiner questions.

What AI Model Documentation Regulators Actually Require

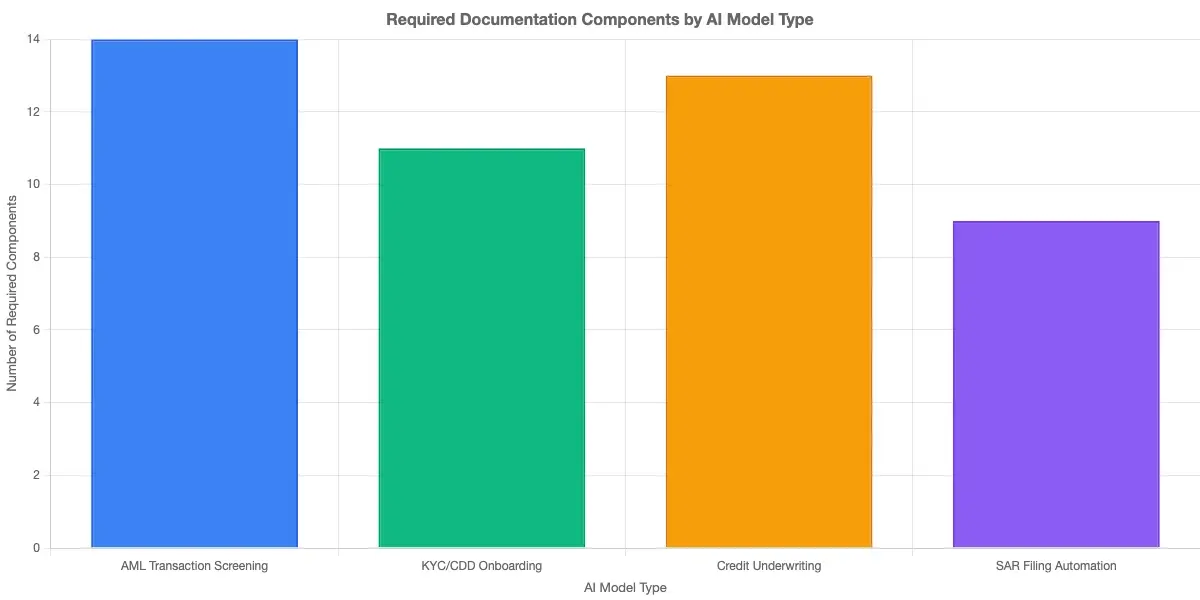

What AI model documentation regulators actually review falls into five categories that every compliance officer should have mapped before an exam:

Model Inventory and Classification: A complete registry of all AI/ML models in production, with risk classifications tied to the potential impact of errors. A model that flags suspicious activity reports gets higher scrutiny than one that recommends marketing offers.

Development Documentation: Training data sources, data quality controls, feature engineering decisions, and the rationale for algorithm selection. Regulators want to understand why you chose a gradient boosted tree over logistic regression for your AML screening model.

Validation Reports: Independent validation is non-negotiable under SR 11-7. The validation must be performed by someone outside the model development team, and the report must address conceptual soundness, data integrity, and performance benchmarking against alternative approaches.

Ongoing Monitoring Records: Monthly or quarterly performance reports showing model stability, population drift analysis, and any threshold changes. If your SAR filing model's recall rate dropped 8% over Q3, that needs to be documented with a root cause explanation.

“Key InsightIf your SAR filing model's recall rate dropped 8% over Q3, that needs to be documented with a root cause explanation.

Change Management Logs: Every model update, even minor recalibrations, needs a documented approval chain. Regulators have cited institutions specifically for undocumented "minor" changes that turned out to have material effects on model output.

For aml compliance fintech environments specifically, FinCEN's guidance on AI-assisted monitoring added requirements around explainability: you must be able to articulate, in plain language, why a specific transaction triggered a sar filing. That explainability requirement has teeth in exam settings.

Model Risk Management for AML and KYC Systems

AML compliance software built on machine learning introduces specific documentation challenges that don't exist with rule-based systems. Rules are transparent. You can show an examiner exactly why a $15,000 cash deposit triggered a CTR filing. ML models don't work that way.

You can show an examiner exactly why a $15,000 cash deposit triggered a CTR filing.

For kyc automation systems in 2026, regulators expect documentation that addresses three specific questions:

Who validated the model's fairness? Adverse impact analysis is now standard in credit and increasingly expected in KYC. If your identity verification model has meaningfully different approval rates across demographic groups, you need documentation showing you identified that, analyzed it, and either accepted it with a reasoned justification or remediated it.

What happens during data drift? Models trained on pre-pandemic transaction patterns may behave unpredictably when transaction volumes or customer behavior shift. Your documentation should show monitoring controls that detect this and a defined revalidation trigger.

How are model decisions explained to customers? Under fair lending and ECOA rules, adverse action notices must convey the principal reasons for a decision. If your kyc automation system rejects an onboarding application, you need a documentation trail showing how that decision was translated into a customer-facing explanation.

Our team has seen institutions with sophisticated ML infrastructure get cited because their validation documentation was thorough for the initial build but had no records of the 14 subsequent model updates. Regulators treat each update as a new potential risk event.

For more context on how KYC and AML checks interact in regulated workflows, see our breakdown of AML risk checks in policy issuance and identity verification strategy.

SAR Filing and CTR Automation: What Documentation Must Cover

SAR filing efficiency has become a genuine operational challenge. The volume of suspicious activity report filings has increased substantially, and institutions are increasingly using automated systems to identify potential SAR candidates.

The documentation requirement here is strict. Per the BSA/AML examination manual from the FFIEC, institutions using automated tools for SAR decisions must document:

- The model's decision criteria and how they map to sar filing requirements

- How the system handles edge cases where the automated recommendation conflicts with analyst judgment

- Quality control procedures verifying that SAR narratives are accurate and complete

- The audit trail showing the human review step before any SAR is filed

CTR filing rules are more rule-based (the $10,000 threshold is statutory), but automated CTR filing systems still require documentation showing how the system aggregates transactions across accounts and correctly identifies structuring patterns.

CTR filing rules are more rule-based (the $10,000 threshold is statutory), but automated CTR filing systems still require documentation showing how the system aggregates transactions across accounts and correctly identifies structuring patterns.

The real trap for fintech bsa aml small teams is the assumption that because a vendor built the model, vendor documentation is sufficient. It isn't. Regulators hold the regulated institution responsible for understanding and validating any model it uses, regardless of whether it was built in-house or purchased. You need documentation showing your team reviewed the vendor's methodology and independently validated that it fits your specific customer population.

For community banks navigating bsa aml compliance, the documentation challenge is compounded by limited technical staff. A practical approach: document what you can verify independently, specifically input/output behavior and performance on your own customer data, and explicitly note where your validation ends and vendor representations begin. That boundary acknowledgment is itself a sign of a mature documentation program.

The EU AI Act and What It Means for AI Documentation in Financial Services

The EU AI Act, which came into force in August 2024 with phased compliance timelines running through 2026, classifies most financial services AI systems as "high-risk." That classification triggers documentation requirements that go significantly beyond what U.S. regulators currently mandate.

According to the EU AI Act requirements, high-risk AI systems must maintain technical documentation covering:

- A general description of the system and its intended purpose

- The design specifications and development process

- Training, validation, and testing data used, including data governance measures

- Monitoring, functioning, and control procedures

- A detailed description of the risk management system

For institutions operating across both EU and U.S. jurisdictions, the EU AI Act creates documentation requirements that are more prescriptive and more granular than SR 11-7. The practical approach most compliance teams are taking: build to the EU AI Act standard where it's stricter, and you'll meet U.S. requirements as well.

The Act also introduces a concept that doesn't appear in current U.S. guidance: a "fundamental rights impact assessment" for high-risk AI. This requires institutions to document how their AI systems may affect protected rights including non-discrimination and data protection. That's a genuinely new obligation for most U.S. compliance teams operating in European markets.

For a broader look at regulatory compliance automation and how DORA requirements interact with AI governance, see our guide on regulatory compliance automation for compliance officers.

Documentation Gaps That Examiners Find Most Often

Based on examination findings published by the OCC and Federal Reserve from 2023 through 2025, these are the documentation gaps that show up repeatedly:

Missing or stale validation reports. Validation is often done once at launch and never updated. Model performance changes over time, and a two-year-old validation report covering a model that has been retrained three times is functionally useless as a risk control.

No documentation of rejected challenger models. SR 11-7 expects institutions to document not just the model they chose but the alternatives they considered and why they were rejected. Examiners use this to assess whether model selection was driven by business pressure rather than sound methodology.

Weak performance benchmarks. Saying "the model achieves 87% accuracy" means nothing without context. Accuracy on what dataset? Compared to what baseline? Regulators want to see performance benchmarked against simpler models and against the institution's historical outcomes.

No defined model retirement process. Models don't just get deployed; they eventually get replaced. Documentation should cover how decommissioned models are handled, how long their records are retained, and how the transition to a replacement model is managed.

Vendor documentation treated as institutional documentation. This is a significant and common error, particularly for aml compliance software purchased from third-party providers.

The OCC model risk management handbook provides the clearest published framework for what constitutes acceptable documentation. If your documentation can't be mapped to the MRM handbook's requirements, that's a gap worth addressing before your next exam.

See also our comparison of manual compliance versus AI automation approaches for context on where automated systems introduce additional documentation obligations.

Building AI Documentation That Survives a Regulatory Exam

Getting AI model documentation to a state where regulators are satisfied requires treating documentation as a continuous process, not a pre-exam scramble. Here's a practical framework that works for both large banks and fintech bsa aml small teams:

Start with the model inventory. You can't document what you haven't catalogued. Many institutions discover models they'd forgotten about when they build a proper inventory. A working model inventory includes: model name and version, purpose and decision domain, risk classification, owner, last validation date, and next scheduled review.

Separate development from validation records. These need to be kept distinct. Commingling developer notes with validation findings is a red flag for examiners. Validation must be demonstrably independent.

Write for the non-technical reader. Examiners are not data scientists. Your documentation should include an executive summary for each model that a lawyer or banker can understand. Technical appendices are fine, but the conceptual soundness section should be readable by someone without an ML background.

Build monitoring into your documentation structure. Monthly performance reports should be generated automatically where possible and stored with a consistent naming convention. This makes it easy to produce a complete monitoring history during an exam rather than reconstructing it from emails and spreadsheets.

Document your anti money laundering technology decisions, not just your outcomes. Why did you set your AML risk assessment threshold where you did? What analysis supported that choice? Regulators want to see reasoned decision-making, not just results.

For teams working with anti money laundering technology 2026 updates, the documentation workload has grown alongside the regulatory requirements. AML compliance software that generates audit-ready documentation automatically can reduce the manual burden significantly. Our guide on AML screening in digital lending for payments risk officers covers what that documentation must demonstrate in practice.

- The shift started before the EU AI Act.

- What AI model documentation regulators actually review falls into five categories that every compliance officer should have mapped before an exam:

- AML compliance software built on machine learning introduces specific documentation challenges that don't exist with rule-based systems.

- SAR filing efficiency has become a genuine operational challenge.

- The EU AI Act, which came into force in August 2024 with phased compliance timelines running through 2026, classifies most financial services AI systems as "high-risk." That classification triggers documentation requirements that go significantly beyond what U.S.

Onboard Customers in Seconds

Conclusion

AI model documentation regulators are not going to reduce their expectations. The trend across both U.S. prudential regulation and the EU AI Act is toward more granular requirements, not fewer. Institutions that treat this as a box-checking exercise will find themselves in remediation cycles that are expensive and reputation-damaging. Institutions that build genuine documentation programs will have a defensible position when examiners ask hard questions.

The core of what regulators want is actually straightforward: they want to know that you understand your AI systems, that someone independent of the development team has verified that understanding, and that you have controls in place to detect when those systems start behaving differently than expected. The documentation is the evidence of that understanding.

Start with your model inventory, close your validation gaps, and make sure your aml compliance and kyc automation systems have the explainability documentation that 2026 exam guidance requires. If you're rebuilding your compliance documentation stack from the ground up, our guide on rolling out regulatory compliance agents in 90 days covers a structured approach to getting there faster.

Share this article