.webp)

Introduction

Fraud detection platforms mid-market banks actually need look very different from the enterprise suites that dominate analyst reports. Tier 1 banks get purpose-built systems with dedicated implementation teams and eight-figure budgets. Mid-market banks, regional lenders, and credit unions often get a discounted version of the same overbuilt product, with the same alert volumes, the same integration complexity, and a price tag that still stings. That gap is finally closing. This guide covers 10 platforms worth evaluating in 2026, what separates them, and how to think through the tradeoffs before you commit.

- Why Mid-Market Banks Face a Different Fraud Problem

- How AI Fraud Detection Actually Works

- What to Look for Before Choosing a Platform

- Top 10 Fraud Detection Platforms for Mid-Market Banks in 2026

- Sardine vs Unit21: Which One for Mid-Market Banking

Onboard Customers in Seconds

Why Mid-Market Banks Face a Different Fraud Problem

Mid-market institutions sit in a difficult position. They're large enough to attract sophisticated fraud rings, but not large enough to absorb the $2M-$5M annual cost of a typical enterprise transaction monitoring software deployment. The result is a painful mismatch: either they overpay for tools built for JPMorgan Chase, or they under-invest and rely on rule-based systems that generate hundreds of alerts per analyst per day.

They're large enough to attract sophisticated fraud rings, but not large enough to absorb the $2M-$5M annual cost of a typical enterprise transaction monitoring software deployment.

The Real Cost of Fraud Alert Fatigue

Fraud alert fatigue is not just an analyst morale issue. When investigators review 400-600 alerts daily and 95% are false positives, two things happen. First, the true positives get missed, creating real financial losses. Second, experienced analysts burn out and leave, taking institutional knowledge with them.

According to FinCEN, financial institutions filed over 3.6 million Suspicious Activity Reports in 2023. The industry estimates the vast majority of triggered alerts never become SARs. The ratio problem is real, and automated transaction monitoring that reduces noise is one of the fastest ROI improvements mid-market banks can make.

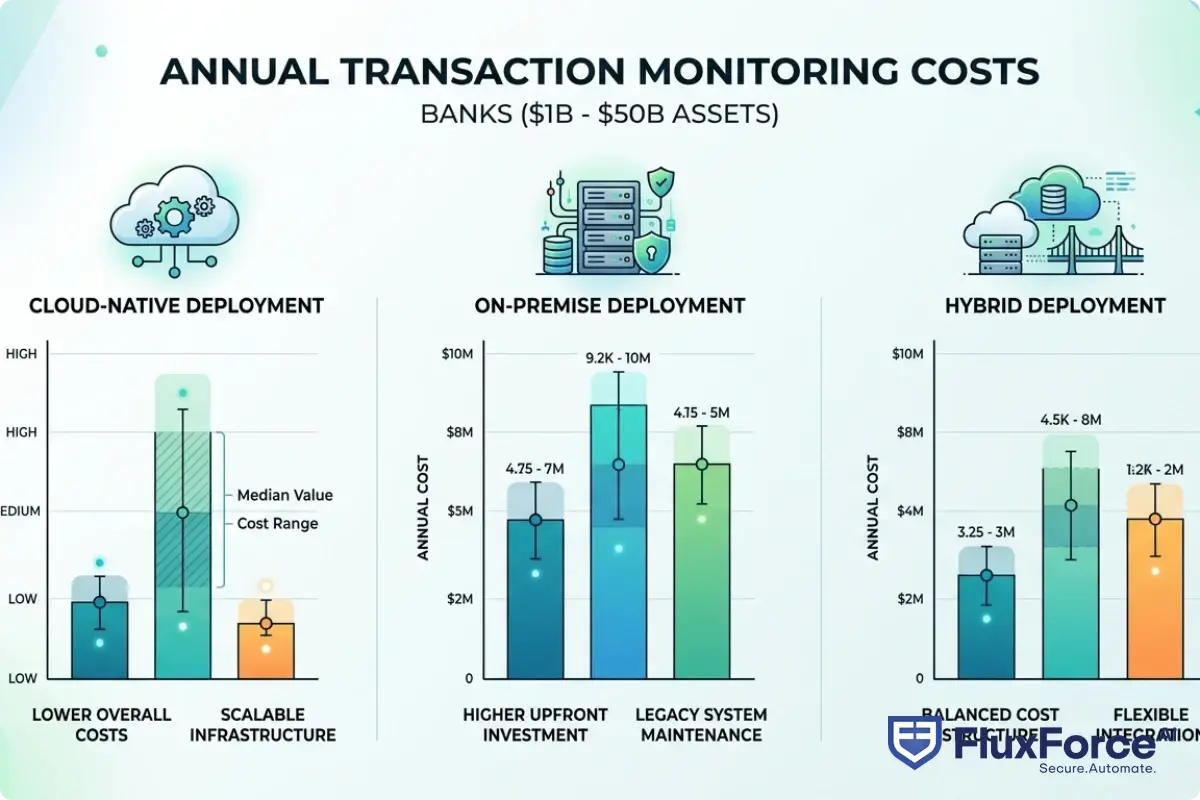

Transaction Monitoring Cost: What You Should Actually Pay

Transaction monitoring cost varies significantly based on deployment model. Cloud-native platforms with consumption-based pricing typically run $80,000-$250,000 annually for mid-market volumes. Legacy on-premise systems can reach $500,000+ when you factor in hosting, maintenance, and the developer hours required to tune rules. If your current vendor quotes more than $300,000 per year for a bank under $10B in assets, the new generation of tools deserves a serious evaluation.

How AI Fraud Detection Actually Works

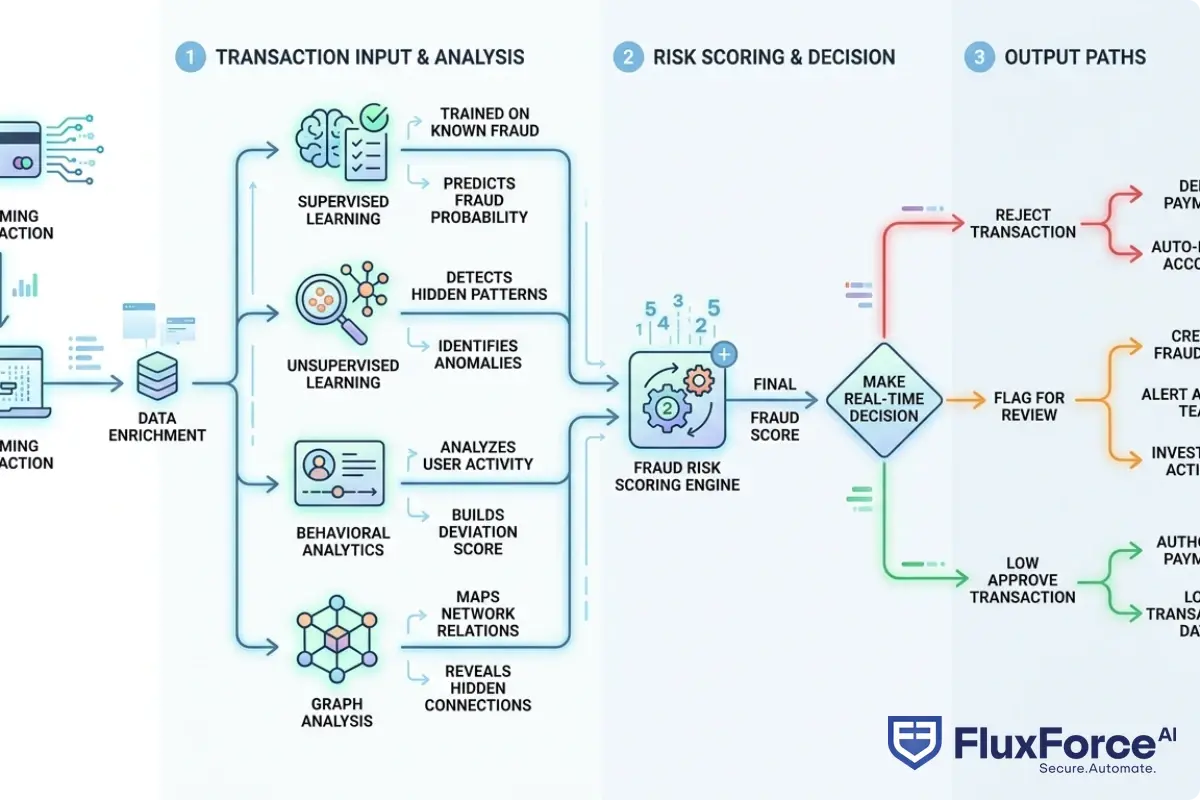

AI fraud detection is the use of machine learning models to identify suspicious patterns in financial transactions without relying exclusively on static, hand-written rules. Where traditional systems flag any wire over $10,000 to a new beneficiary, machine learning fraud detection flags a specific transaction because it deviates from a customer's behavioral baseline, matches patterns from confirmed fraud cases, and involves a counterparty with an elevated risk profile. This is ai fraud detection explained at its core: context-aware, adaptive, and probability-based rather than threshold-based.

How Does AI Detect Fraud at the Transaction Level

Most commercial ai fraud detection software uses several techniques in combination:

- Behavioral analytics: Building a baseline per customer and scoring deviations from it

- Graph analysis: Mapping relationships between accounts, devices, IP addresses, and merchants to identify fraud rings

- Supervised classification: Training models on labeled fraud data to predict the probability a transaction is fraudulent

- Unsupervised anomaly detection: Catching novel fraud patterns that have no historical precedent

Real time fraud detection requires all of this to run in under 300 milliseconds, which is why latency is one of the harder engineering challenges in this space. For a deeper technical breakdown of how these strategies apply to card fraud, AI-powered fraud detection strategy for risk heads covers the implementation details well.

Machine Learning Fraud Detection: Supervised vs. Unsupervised

Most fraud teams start with supervised models because they're easier to explain to regulators and auditors. You train the model on historical fraud labels, and it learns which features predict fraud. The problem: supervised models are inherently backward-looking. They catch fraud that looks like past fraud.

Unsupervised models identify statistical outliers without needing labeled examples. They're better at catching first-instance fraud, novel account takeover patterns, and synthetic identity fraud schemes that haven't been seen before. The strongest platforms combine both approaches with continuous retraining as new fraud patterns emerge.

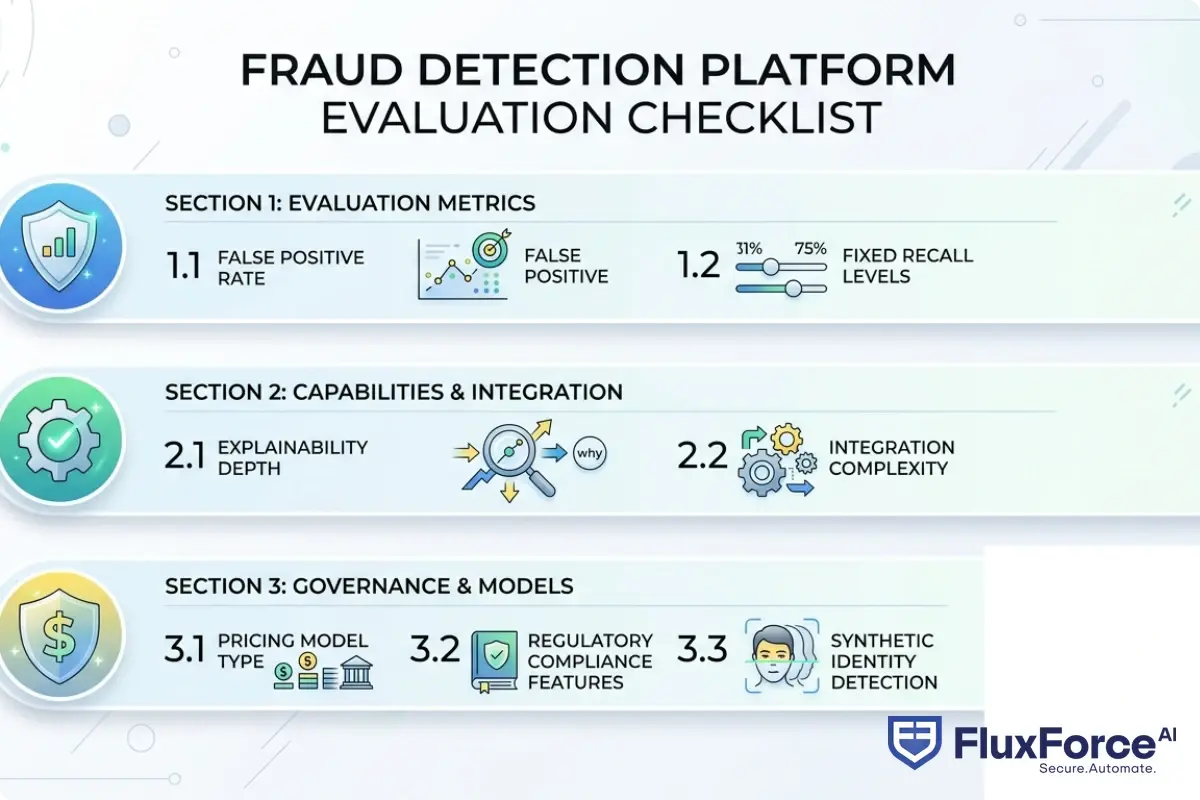

What to Look for Before Choosing a Platform

Before comparing individual vendors, get clear on your requirements. These platforms differ significantly on integration approach, explainability, pricing model, and which fraud types they're strongest on. Understanding the differences between AI and traditional fraud detection is a useful starting point before entering vendor conversations.

Reduce False Positives in Transaction Monitoring: The Key Metrics

False positives fraud detection is, in most mid-market banks, the single biggest operational cost. A false positive rate of 98% means that for every 100 alerts generated, only 2 are real fraud. If each alert costs $25-$50 in analyst time and you're generating 50,000 alerts monthly, you're spending over $1M annually to investigate noise.

The question to ask vendors: "What is your false positive rate at 95% fraud detection recall?" The false positive rate fraud detection metric at a fixed recall threshold is the honest measure of a system's precision. If they can't answer with actual customer data, that's a red flag worth acting on.

The question to ask vendors: "What is your false positive rate at 95% fraud detection recall?" The false positive rate fraud detection metric at a fixed recall threshold is the honest measure of a system's precision.

AI Fraud Detection in Banking: Explainability Requirements

Regulators increasingly expect banks to explain why an account was flagged or a transaction blocked. Under FATF Recommendation 10, transaction monitoring must be risk-based and documented. Black-box models that produce a score with no explanation create compliance exposure. Look for platforms that surface feature-level explanations alongside each alert, not just a numerical risk score.

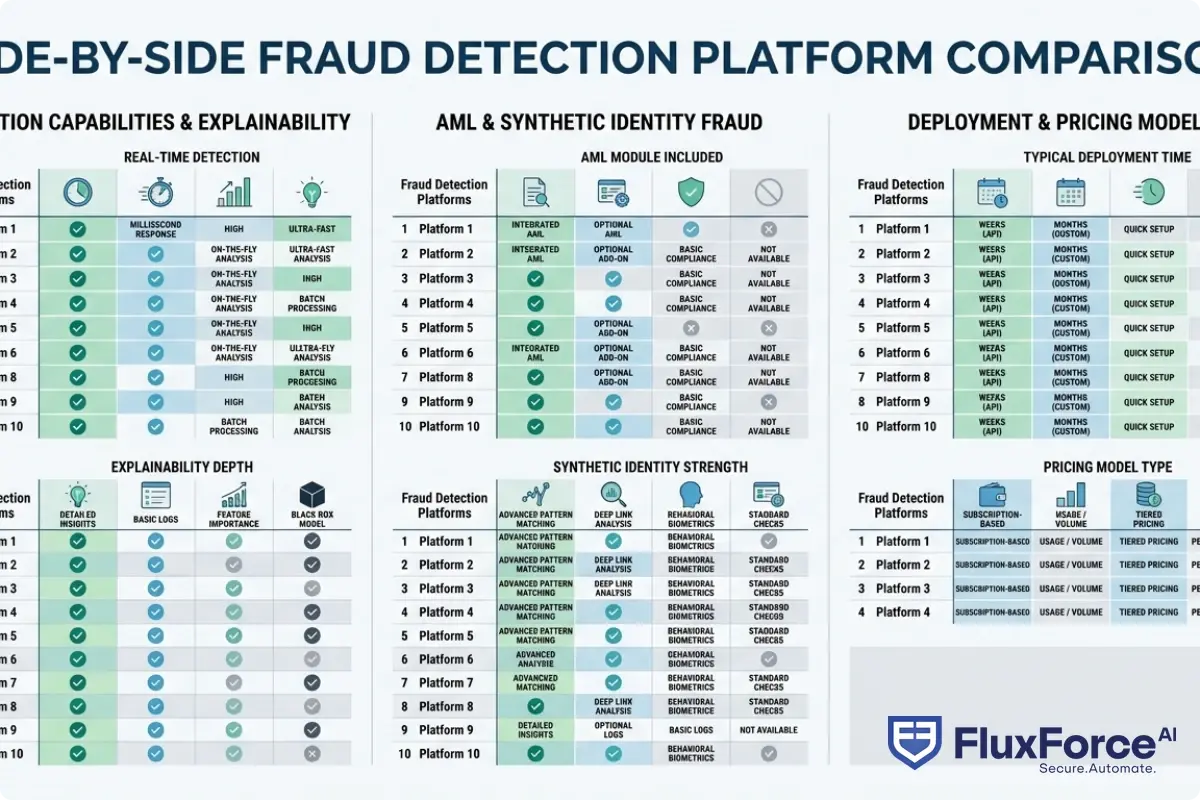

Top 10 Fraud Detection Platforms for Mid-Market Banks in 2026

These platforms are ordered by relevance to mid-market institutions specifically, not overall capability. The right choice depends on your tech stack, budget, and primary fraud vectors.

1. Unit21

Unit21 is built around the principle that risk teams should configure their own detection logic without writing code. Its no-code rule builder is one of the stronger ones on the market. Analysts can create complex detection scenarios, backtest them against historical data, and measure the projected impact on alert volume before deploying live.

Pricing is consumption-based, which works well for mid-market transaction volumes. Unit21's case management interface is also notably stronger than most competitors, which matters when analysts are the operational bottleneck. For banks dealing with high-volume ACH or wire fraud, it's a top-three option.

2. Sardine

Sardine focuses on device intelligence and behavioral biometrics, making it particularly strong on account takeover and application fraud. Its device fingerprinting captures over 3,000 signals at the browser and app level, including typing cadence, mouse movement patterns, and device configuration.

If your fraud problem concentrates in digital onboarding or mobile banking channels, Sardine deserves top-of-list consideration. In a sardine vs unit21 comparison specifically for transaction monitoring scenarios, Sardine tends to win on first-party fraud signals while Unit21 wins on transaction pattern complexity and rule configurability.

3. Featurespace

Featurespace's ARIC platform uses adaptive behavioral analytics, meaning its models update continuously as customer behavior changes. This matters for banks with seasonal transaction patterns or customer bases that shifted significantly in recent years.

The platform is strong on credit card fraud and effective at catching authorized push payment fraud, which remains one of the fastest-growing fraud categories in retail banking globally.

4. Hawk AI

Hawk AI combines rule-based transaction monitoring with machine learning explainability. Its "AI Explainable" layer surfaces the specific data points driving each alert score, which simplifies the SAR filing process and can reduce analyst review time by roughly 40% according to published customer case studies.

Hawk AI also includes a dedicated AML module, making it one of the better choices if you need consolidated fraud and AML coverage rather than separate point solutions with separate data silos.

5. Effectiv

Effectiv is one of the newer entrants and worth serious attention for banks that need rapid deployment. The platform is API-first and can integrate with core banking systems in days rather than months. It uses graph machine learning to identify fraud rings, which is particularly effective at catching synthetic identity fraud networks before they cause large losses.

For banks that need to be live within 60-90 days, Effectiv is likely the fastest path to production among platforms in this tier.

6. NICE Actimize

NICE Actimize is the closest thing to enterprise-grade in this list, but the company has made real progress on mid-market packaging over the last two years. Their Xceed Cloud platform offers a SaaS model with modular pricing that works for institutions below $20B in assets.

The tradeoff is implementation complexity. NICE Actimize deployments typically take 3-6 months and require significant internal resources to configure properly. If you have the bandwidth, the detection capability is among the best available.

7. ComplyAdvantage

ComplyAdvantage's strength is its financial crime intelligence data layer. The platform continuously monitors 100+ data sources for adverse media, sanctions updates, and PEP exposure, integrating that context directly into transaction risk scores.

For banks with significant cross-border transaction volumes or high-risk customer segments, that real-time intelligence layer is a meaningful differentiator over platforms that rely on static watchlists updated weekly or monthly.

8. Feedzai

Feedzai runs a full-stack machine learning pipeline, ingests event streams in real time, and is designed for high-transaction-volume environments. The platform has strong payment fraud prevention capabilities and handles card-not-present fraud particularly well across both retail and commercial banking use cases.

The honest limitation: Feedzai is designed for banks with data science teams. Without ML engineers on staff, you'll get considerably less from it than from a more turnkey solution.

9. Verafin (Nasdaq)

Verafin focuses on collaborative fraud and AML detection. Its network intelligence approach allows participating banks to share anonymized fraud signals across its cloud, which improves detection for fraud that moves between institutions. For community banks and credit unions facing coordinated fraud rings, this network effect is a genuine competitive advantage.

Nasdaq's acquisition has expanded enterprise capabilities, but the platform still feels purpose-built for institutions below $50B in assets, which is a good fit for this list.

10. Sift

Sift is primarily a digital trust and safety platform, strongest on e-commerce and fintech fraud patterns. For traditional mid-market banks, it's most relevant if you have a significant digital banking footprint, particularly around account creation, promotion abuse, and card-not-present transactions.

Sardine vs Unit21: Which One for Mid-Market Banking

This comparison surfaces repeatedly because both platforms target similar buyers and both carry strong market momentum heading into 2026. They're optimized for different fraud problems, which actually makes the choice more straightforward than it might appear at first.

False Positive Rate Fraud Detection: Platform Comparison

Unit21 customers consistently report reducing alert volumes by 30-50% in the first six months, primarily through better rule tuning and model-assisted alert prioritization. The platform excels at complex transaction pattern monitoring and suits banks with high ACH or wire volumes well.

Sardine customers report larger reductions in false positives specifically for digital channel fraud, including new account fraud and account takeover. If your fraud losses concentrate in your mobile app or online banking portal, Sardine's behavioral signals catch issues that standard transaction pattern analysis misses entirely. The false positive rate fraud detection improvement is most pronounced for identity-based fraud vectors.

Integration and Pricing

Both platforms are API-first and integrate with standard core banking systems. Unit21's no-code interface means your risk team manages configuration without ongoing engineering support after the initial deployment. Sardine requires more developer involvement for its device SDK implementation, but that investment pays off in signal quality for digital channels.

On pricing, both use consumption-based models. For a mid-market bank processing 5 million monthly transactions, expect $150,000-$250,000 annually with either platform, depending on module selection and volume tiers.

For a mid-market bank processing 5 million monthly transactions, expect $150,000-$250,000 annually with either platform, depending on module selection and volume tiers.

How to Reduce False Positives in AML Without Replacing Your Stack

Many mid-market banks don't need a full platform replacement to improve their false positive situation. The issue is often configuration, not technology. Here's where to start before you issue an RFP.

How to Reduce False Positives in Transaction Monitoring

The first lever is customer segmentation. Most legacy systems apply the same detection rules to every account. Behavioral segmentation, building separate baselines for different customer types such as retail vs. commercial or domestic vs. international, typically reduces false positives by 20-35% without changing the underlying detection models at all.

The second lever is velocity calibration. Rules that trigger on absolute thresholds rather than relative deviations from customer baseline behavior generate the majority of false positives in most AML systems. Switching from "flag $10,000 cash deposits" to "flag deposits that are 3x this customer's 90-day average" dramatically improves precision without reducing fraud capture rates.

For more advanced automation approaches that go beyond rule tuning, how agentic AI reduces false positives by 80% covers the next tier of optimization strategies.

False Positive Cost Fraud: The Numbers That Matter

The industry average cost per false positive alert is $35-$50 in analyst time. For a bank generating 20,000 alerts monthly with a 97% false positive rate, that's roughly $680,000-$970,000 in annual analyst cost, for alerts that generate zero SARs.

Reducing your false positive rate from 97% to 90% on that same volume saves approximately $240,000-$350,000 per year. That's the financial case for investing in better tooling, and it doesn't require replacing your core system. The comparison of rule-based systems vs. AI-driven solutions is worth reading before starting any vendor conversations.

Real-Time Fraud Detection: What Mid-Market Banks Actually Need

Real time fraud detection in banking means catching fraud before a transaction completes, requiring sub-second decisioning. For payment fraud prevention on card transactions, most networks require authorization decisions within 100-300 milliseconds. That constraint shapes which platforms are actually viable for inline payment fraud use cases.

Real-Time Fraud Detection Banks: Latency Requirements

The latency requirement creates a real architectural constraint. Cloud-based platforms with round-trip API calls can add 50-150ms of latency per transaction. That's acceptable for most use cases but becomes problematic at high volumes (over 500 transactions per second) or for synchronous payment authorization pipelines.

Most mid-market banks don't hit these thresholds, but it's worth asking any vendor for their p95 latency numbers at your expected transaction volume. Theoretical benchmarks on clean data are not the same as production latency under load.

Synthetic Identity Fraud Detection in Real Time

Synthetic identity fraud is the fastest-growing fraud type in retail banking and particularly hard to catch in real time because fraudsters spend months building legitimate-looking credit histories before striking. According to the Federal Trade Commission, identity-based fraud continues to grow year over year, with synthetic variants being among the hardest for traditional systems to detect.

Detecting synthetic identity fraud in real time requires graph-based analysis that maps relationships between application attributes across the full customer lifecycle, not just individual transaction scores at point of authorization. Platforms with strong graph ML capabilities, particularly Effectiv and Featurespace, have a meaningful advantage here. Standard transaction monitoring software without graph analysis tends to catch synthetic identity fraud only after significant losses have already occurred.

- Mid-market institutions sit in a difficult position.

- AI fraud detection is the use of machine learning models to identify suspicious patterns in financial transactions without relying exclusively on static, hand-written rules.

- Before comparing individual vendors, get clear on your requirements.

- These platforms are ordered by relevance to mid-market institutions specifically, not overall capability.

- This comparison surfaces repeatedly because both platforms target similar buyers and both carry strong market momentum heading into 2026.

Onboard Customers in Seconds

Conclusion

The market for fraud detection platforms mid-market banks can actually deploy and afford has matured considerably. The 10 platforms covered here offer genuine detection capabilities at pricing that doesn't require a Tier 1 budget or a six-month implementation project. Unit21, Sardine, Effectiv, and Hawk AI stand out as the most mid-market-native options, with strong no-code configuration, consumption-based pricing, and deployment timelines measured in weeks.

Start with your fraud loss breakdown: which fraud types are costing the most, and which channels are being exploited. That alone narrows your shortlist from 10 to 3 or 4. Then run a proof-of-concept on your own transaction data with your actual false positive rate as the primary success metric. Vendors who demonstrate measurable alert reduction on real data are the ones worth contracting. Automated transaction monitoring that reduces analyst burden pays for itself quickly. The right platform will make that case with numbers, not marketing slides.

Share this article