.webp)

Introduction

AI in banking 2026 is at a genuine inflection point: the pilots are over, proof-of-concept budgets have been spent, and boards are asking whether the technology delivered. For most financial institutions, the honest answer is that it depends heavily on what you built, how you measured it, and whether compliance and risk teams were involved from day one. This post separates what is actually working from what remains aspirational, covering fraud prevention ROI, compliance automation, and the rise of agentic AI across banking, insurance, and supply chain finance. If you are making investment decisions for the next 18 months, this is the analysis you need.

For financial institutions looking to address these challenges, core banking modernization & security solutions offer a proven path forward.

- What AI in Banking 2026 Actually Looks Like

- AI Automation Banking: The Use Cases Delivering Real Value

- Agentic AI Banking: Beyond Rules and Workflows

- How AI in Banking 2026 Is Reshaping Fraud Prevention ROI

- Compliance Automation ROI: Where the Real Savings Come From

Onboard Customers in Seconds

What AI in Banking 2026 Actually Looks Like

AI in banking 2026 is not a single story. It is dozens of experiments at different maturity stages, producing wildly different outcomes depending on an institution's data quality, regulatory environment, and willingness to change processes rather than just add tools on top of existing ones.

Gartner's 2025 research placed the average AI project failure rate in financial services above 60% when measured against original ROI targets. That does not mean the technology fails. It means most deployments underestimated what production-ready actually requires in a regulated environment.

Gartner's 2025 research placed the average AI project failure rate in financial services above 60% when measured against original ROI targets.

The Gap Between Vendor Claims and Live Deployments

The marketing for ai automation banking solutions promises straight-line improvements: 80% reduction in false positives, 90% faster KYC, full regulatory reporting in minutes. The reality in most banks is closer to 30-40% improvement in specific, well-scoped workflows, achieved after 9-18 months of integration work and a significant rethinking of underlying data architecture.

The gap is rarely about the AI model. It is about the data pipelines feeding it, the change management required to get operations teams to trust outputs they cannot fully interpret, and the compliance review process that must sign off before anything touches a live customer workflow.

Where Banks Are Genuinely Seeing Returns

The areas where AI in banking 2026 is delivering measurable, auditable returns are narrower than the hype suggests but still material:

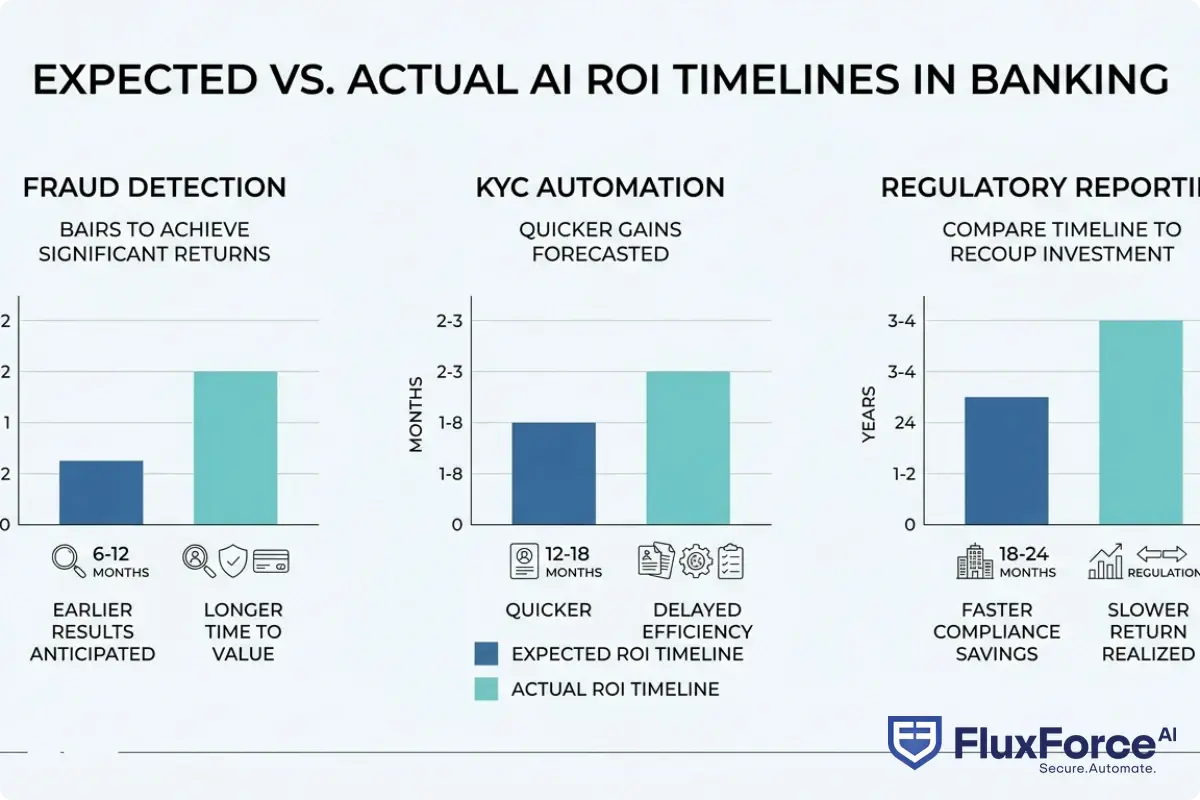

- Real-time transaction fraud detection: Banks using AI-powered models report 40-60% reductions in fraud losses on card transactions, because models process hundreds of behavioral signals in under 50 milliseconds.

- AML alert triage: Reducing low-quality alert volume so human analysts focus on genuinely suspicious activity.

- Document-heavy onboarding: Automating identity document extraction and verification, cutting average KYC onboarding time from 3-5 days to under 8 hours in well-implemented programs.

These outcomes are real. They are also the product of focused, well-resourced programs, not plug-and-play installations.

AI Automation Banking: The Use Cases Delivering Real Value

AI automation banking works best where the underlying task is high-volume, rule-consistent, and data-rich. Transaction scoring rather than credit philosophy. Document verification rather than relationship-based lending. The distinction shapes where to invest first and what realistic timelines look like.

Fraud Detection and Transaction Monitoring

Card fraud detection is the clearest current win in ai automation banking. Traditional rule-based systems flag transactions on static thresholds. AI models trained on behavioral patterns detect fraud that breaks none of those rules, because the pattern itself is anomalous.

Banks using AI-powered fraud detection as part of a layered card fraud analytics strategy typically see false positive rates drop by 30-50%. Every false positive is a blocked legitimate transaction, a customer service call, and a churn risk, so this reduction has direct revenue impact beyond just the fraud prevention line. One caveat: these systems need continuous retraining. Fraud patterns shift as adversaries study how models behave, and an 18-month-old model without updates often performs worse than a current rule-based system.

KYC and Onboarding Automation

KYC automation is the second use case delivering consistent results. Document extraction, liveness detection, sanctions screening, and adverse media checks can all be automated to a level that satisfies most regulatory standards, provided the audit trail is clean.

The tradeoff: automated KYC is faster for standard cases and struggles with edge cases, unusual document formats, and customers whose digital footprint does not match training patterns. Banks that went fully automated without human-in-the-loop escalation paths discovered this in production, often through regulatory examination findings.

How AI Reduces the Cost of Compliance Financial Services

The cost of compliance financial services has grown at roughly 5-8% annually for a decade, driven by expanding regulatory scope and increasing transaction data volumes. Manual compliance cost at a mid-size bank now runs $30-50 million annually when you account for staff, technology, and the opportunity cost of slow processes.

The cost of compliance financial services has grown at roughly 5-8% annually for a decade, driven by expanding regulatory scope and increasing transaction data volumes.

AI reduces this in three specific ways: faster alert triage, automated report generation, and real-time sanctions screening that does not require human review for clean matches. The savings rarely reach the 70-80% figures in vendor slides. A more defensible benchmark is 25-40% reduction in direct compliance operational costs, achieved over 2-3 years with proper implementation.

Agentic AI Banking: Beyond Rules and Workflows

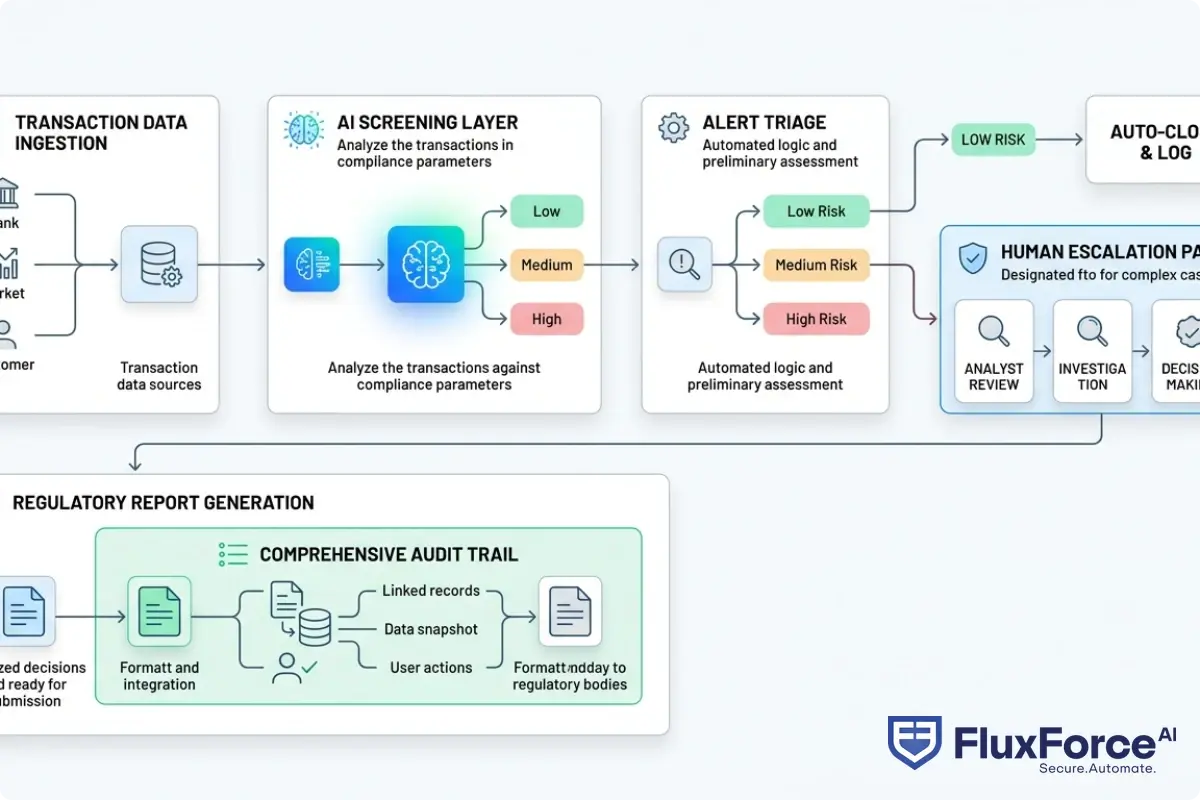

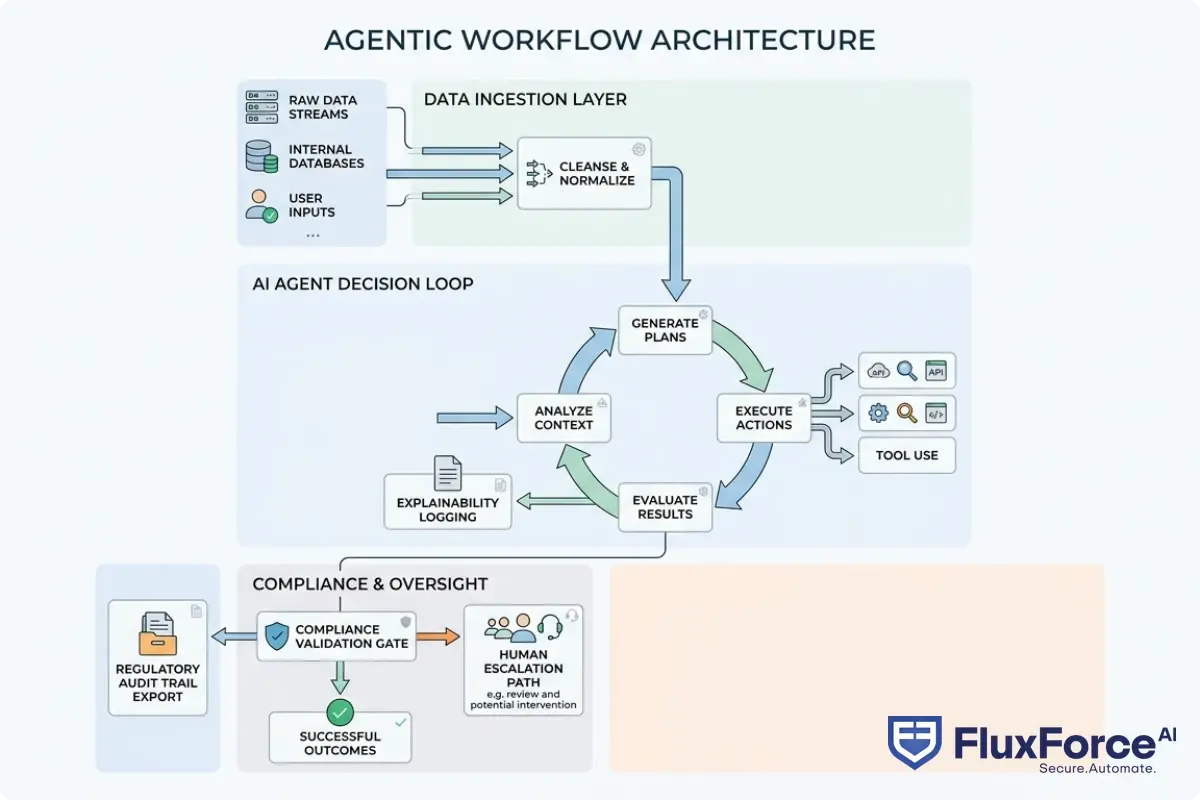

Agentic AI banking marks a shift from AI as a decision-support tool to AI as an active participant in operational processes. Instead of a model flagging an alert for human review, an agentic system investigates the alert, pulls supporting data from multiple systems, and drafts a case disposition recommendation autonomously.

This is qualitatively different from automation as it existed two years ago. It is also where the hype-to-reality gap is widest, because most production deployments of agentic AI in financial services remain narrow, supervised, and carefully sandboxed.

How Agentic AI Financial Services Differs from Traditional Automation

Traditional automation executes fixed step sequences. Agentic AI financial services systems adapt their approach based on what they discover mid-task. If an AML investigation agent finds a flagged transaction involves a correspondent banking relationship requiring additional due diligence, it autonomously retrieves relevant files, cross-references against sanctions lists, and escalates with a structured summary rather than a raw alert.

The false positive reductions achieved by agentic AI fraud agents are frequently cited, but the deeper value is in case file quality. Human investigators spend less time gathering data and more time on judgment calls.

Agentic AI Deployments in 2026: What Is Live vs. What Is Planned

Most financial institutions in 2026 have one or two agentic workflows in production, typically in fraud investigation or regulatory report drafting. Fully autonomous compliance operations without human oversight remain a future-state goal. Most regulators would not sign off on them even if the technology were ready.

The path to deploying regulatory compliance agents within 90 days exists but requires careful scoping: pick a workflow that is well-defined, data-rich, and auditable. Starting with complex regulatory judgment calls is a reliable path to failure.

How AI in Banking 2026 Is Reshaping Fraud Prevention ROI

Fraud prevention ROI gets the most attention and the most creative accounting. Vendors cite gross fraud losses prevented while omitting platform cost, integration labor, ongoing retraining, and false positive operational costs embedded in blocked legitimate transactions.

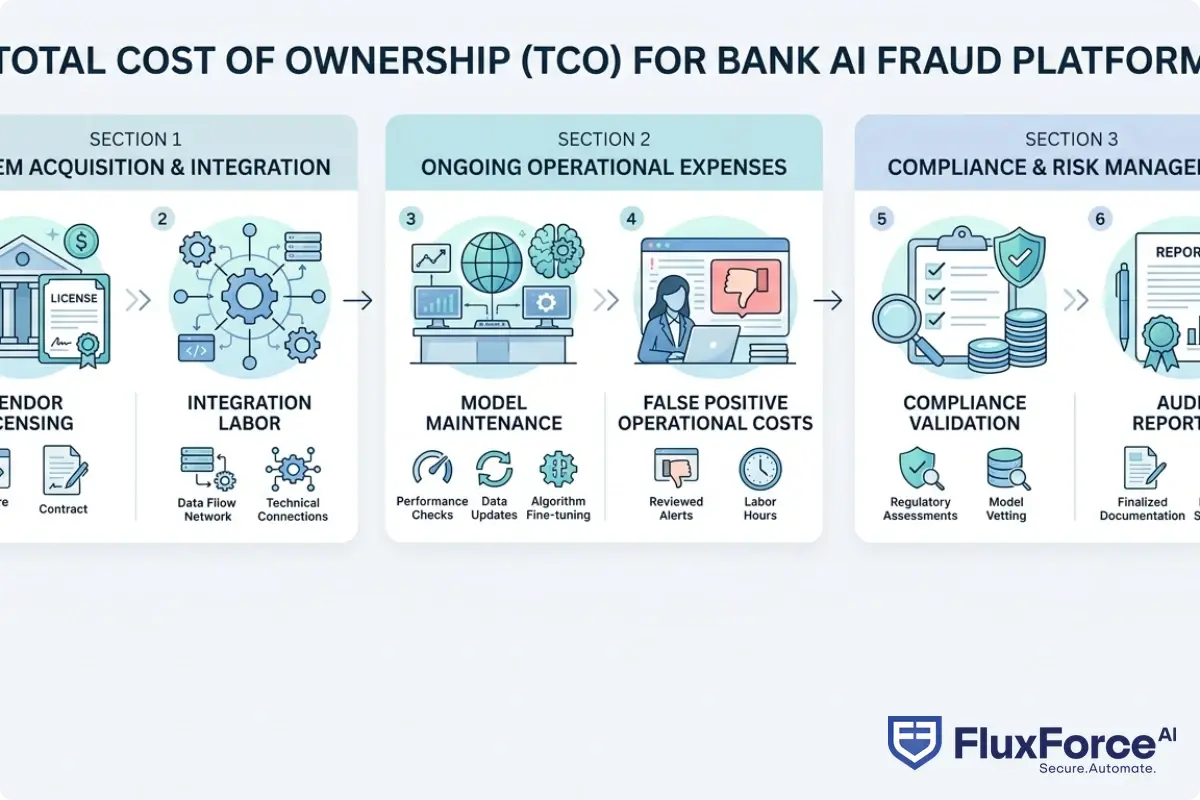

Total Cost of Ownership for a Fraud Platform

The total cost of ownership fraud platform calculation needs to include:

- License or subscription cost: Typically $500K-$3M annually for a mid-size bank depending on transaction volume

- Integration and implementation: Usually 1.5-2.5x the first year's license cost

- Ongoing model maintenance: Data science and MLOps resources to retrain and monitor

- False positive operational cost: 15-30 minutes of human review per false positive; significant at scale

- Compliance validation: Regulatory review of AI model decisions and explainability documentation

When you run the full calculation, fraud prevention ROI is still positive for most institutions. The payback period is typically 18-36 months, not the 6-month projections appearing in some vendor proposals.

McKinsey's research on AI in financial services consistently shows that institutions investing in data infrastructure before deploying AI models achieve significantly better outcomes than those treating it as a pure software purchase.

The Manual Compliance Cost That Never Shows Up in Demos

Manual compliance cost is almost always underestimated because it is distributed across departments, buried in headcount hired incrementally, and rarely labeled as compliance labor in budget models. A large bank has compliance-related work embedded in operations, IT, legal, audit, and customer service, and most of it never appears in compliance cost line items.

The comparison between manual compliance and AI automation approaches shows that labor represents 60-70% of total compliance operational cost. That is the component most amenable to automation and where compliance automation ROI is most defensible when presenting to a board.

Compliance Automation ROI: Where the Real Savings Come From

Compliance automation ROI is most defensible in bounded domains: transaction reporting, sanctions screening, and regulatory filing preparation. These are high-volume, low-ambiguity tasks where the main challenge is speed and consistency, not interpretive judgment.

Regulatory Reporting Automation

Regulatory reporting that previously required 2-3 days of analyst time per cycle can be reduced to 4-6 hours of reviewing AI-prepared drafts. The model pulls the right data, applies the correct regulatory schema, and flags edge cases for human review. The DORA compliance automation programs being deployed by digital banks illustrate this pattern clearly. The compliance automation ROI on regulatory reporting often reaches 200-300% in the first year when measured against full labor cost.

The compliance automation ROI on regulatory reporting often reaches 200-300% in the first year when measured against full labor cost.

Automated sanctions screening against consolidated watchlists, with AI-powered disambiguation for common name false matches, processes millions of records daily without human input, escalating only genuine near-matches.

From Manual Compliance Cost to Measurable ROI

Organizations that automate too quickly often recreate their manual process in software form, automating the inefficiency rather than rethinking the workflow. This produces 10-15% cost reductions instead of the 30-40% that well-scoped programs achieve.

The NIST AI Risk Management Framework provides authoritative guidance for responsible AI deployment in regulated sectors. Compliance teams increasingly use it as a validation checklist before sign-off. The compliance automation ROI calculation should always include a regulatory risk reduction line: an AI system with a clean audit trail reduces examination costs and enforcement exposure in ways that are difficult to quantify but very real.

How FluxForce AI Is Addressing the Hype vs. Reality Problem

FluxForce operates on the premise that the gap between AI hype and operational reality in financial services is primarily an implementation architecture problem, not a technology capability limitation. The platform is built for regulated industries where every AI decision must be auditable, explainable, and aligned with specific compliance frameworks.

FluxForce Review: Key Capabilities for Regulated Industries

A FluxForce review from banking and insurance practitioners typically focuses on three differentiating capabilities:

Explainability by default: Every decision by a FluxForce AI agent includes a structured rationale log. In banking, a compliance officer needs to explain to a regulator why an alert was dismissed or why a customer was declined. A black-box score is not a defensible answer.

Workflow-level auditability: FluxForce AI captures the full workflow graph rather than just individual model outputs: what data was accessed, what tools were invoked, what decision branches were taken. This is the audit trail that survives regulatory scrutiny.

Pre-built compliance integrations: Rather than requiring banks to build AML, KYC, and sanctions screening connectors from scratch, FluxForce ships with pre-validated integrations for common regulatory data sources, reducing integration burden and time-to-value significantly.

Why Agentic AI in Financial Services Needs Explainability

The ai in banking hype vs reality debate frequently misses the explainability problem. A model achieving 95% fraud detection accuracy is impressive until the regulator asks why a specific customer was flagged and the answer is a black-box score. That is a compliance failure regardless of model accuracy.

Agentic AI financial services deployments that gain regulatory acceptance share one characteristic: they produce structured reasoning explanations that map to the institution's stated compliance policies. The Bank for International Settlements has highlighted in its supervisory publications on AI model governance that model interpretability is increasingly treated as a regulatory requirement, not an optional feature.

The Future of AI in Banking: Priorities for 2026 and Beyond

The future of AI in banking through 2027 is consolidation, not another wave of pilots. Institutions that ran 20 experiments over the past three years are now deciding which three to scale. Others are starting focused first programs informed by what those early adopters learned, with more realistic expectations about integration timelines and ROI.

Near-Term Bets Worth Making

The highest-confidence AI investments in banking for 2026:

- Agentic fraud investigation: AI agents handling the initial 80% of case investigation work, with humans reviewing and deciding. Labor savings are real with 12-18 month ROI timelines.

- Automated regulatory report drafting: Mature technology, well-understood regulatory posture, clear ROI. Start here if you have not already.

- Real-time behavioral fraud scoring: Session-level and user-lifecycle scoring beyond transaction-level analysis. Incremental fraud reduction from this layer is measurable and compounds over time.

Approach with more caution: fully autonomous credit decisions without explainability infrastructure, AI-generated customer communications without human review in regulated contexts, and general-purpose agentic deployments without defined task scope and escalation paths.

The Risks That Don't Get Enough Airtime

Model drift is real. A fraud model trained on 2024 data performs measurably worse by mid-2026 without continuous updates. Data quality problems compound: AI systems are only as good as the transaction history, customer data, and third-party signals they were trained on, and many banks carry significant data quality debt they have not yet addressed.

Concentration risk is underappreciated. When multiple institutions use the same AI vendor's fraud model, adversarial actors who identify that model's weaknesses can exploit all of them simultaneously. This risk deserves dedicated attention in security architecture planning as AI adoption scales across the industry.

- AI in banking 2026 is not a single story.

- AI automation banking works best where the underlying task is high-volume, rule-consistent, and data-rich.

- Agentic AI banking marks a shift from AI as a decision-support tool to AI as an active participant in operational processes.

- Fraud prevention ROI gets the most attention and the most creative accounting.

- Compliance automation ROI is most defensible in bounded domains: transaction reporting, sanctions screening, and regulatory filing preparation.

Onboard Customers in Seconds

Conclusion

AI in banking 2026 is delivering real returns in specific, well-implemented use cases: real-time fraud scoring, KYC automation, AML alert triage, and regulatory report drafting. The gap between vendor hype and production reality remains but is narrowing for institutions that invest in data infrastructure, explainability, and change management alongside the AI technology itself.

The rise of agentic AI banking is the most significant near-term operational shift, changing how human-AI collaboration works in compliance and risk workflows. FluxForce AI and similar purpose-built platforms address the implementation gap through pre-built compliance integrations and audit trails designed for regulatory scrutiny. For the next 18 months: start with workflows where data is cleanest, compliance requirements are clearest, and ROI is most measurable. Build explainability in from day one. Run the full total cost of ownership calculation before committing to any platform. The future of AI in banking belongs to institutions that treat it as an operational discipline rather than a technology purchase.

Share this article