.webp)

Introduction

AML compliance fintech 2026 isn't just about ticking regulatory boxes anymore. The rules have changed, the stakes have gone up, and compliance officers at fintechs are being asked to do more with faster systems, more data, and less tolerance for error.

In 2025 alone, global AML-related fines exceeded $6 billion across financial institutions. Regulators in the EU, US, and APAC have all signaled that the days of accepting best-efforts explanations from underprepared fintechs are over. If you're running a compliance program that still relies heavily on manual review queues and static rule sets, this guide is a direct challenge to rethink that approach.

In 2025 alone, global AML-related fines exceeded $6 billion across financial institutions.

We'll cover what's changed in the regulatory environment, where fintechs most commonly fail AML audits, and how modern compliance programs are being built to actually work in 2026.

- What Changed in AML Compliance for Fintechs in 2026

- The Core Components of a Fintech AML Program

- How AI Is Reshaping AML Compliance in Fintech

- Building a Risk-Based AML Framework

- What Regulators Are Watching in 2026

Onboard Customers in Seconds

What Changed in AML Compliance for Fintechs in 2026

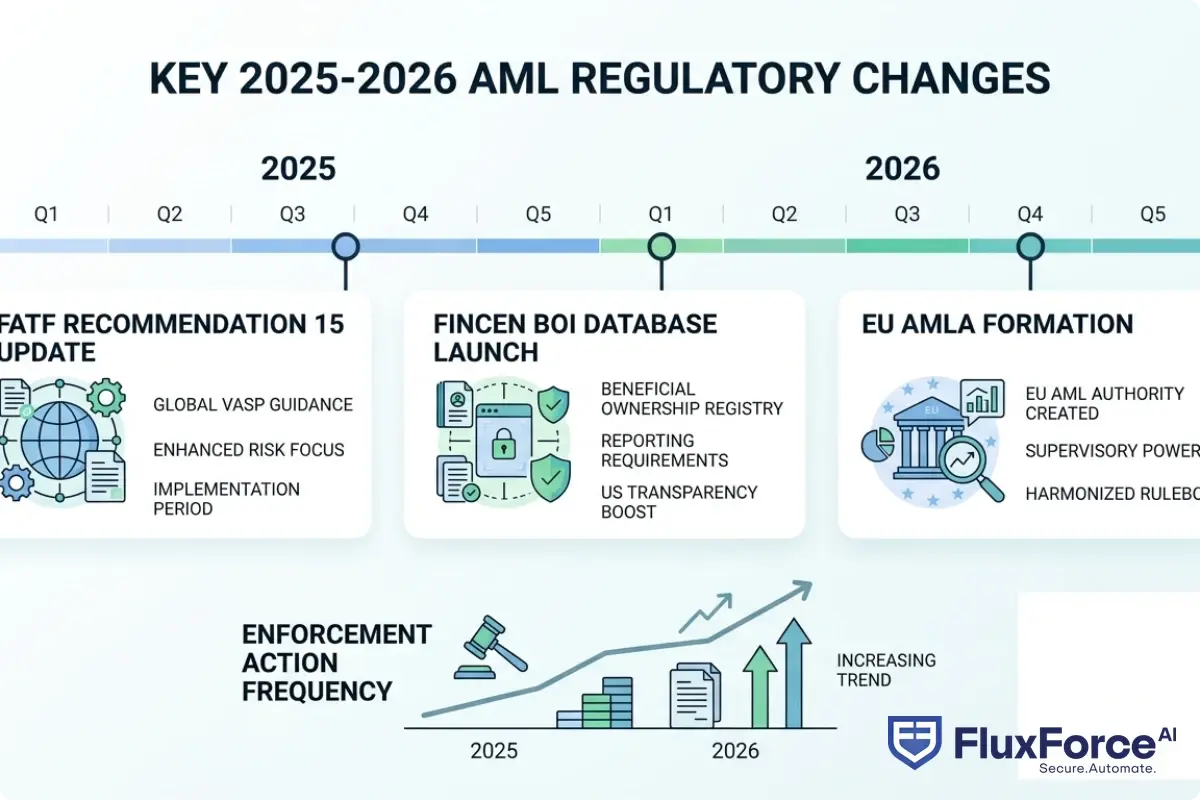

The regulatory environment that fintechs operate in today looks meaningfully different from even 18 months ago. Three areas in particular have seen the most significant shifts.

FATF's Updated Guidance on Virtual Assets

The Financial Action Task Force updated its Recommendation 15 guidance in late 2025, extending its virtual asset service provider (VASP) definitions to include a broader range of DeFi protocols, non-custodial wallet providers, and embedded finance products. For fintechs that previously assumed they fell outside VASP definitions, the new guidance closes several of those loopholes.

The practical effect: more fintechs now need to register as VASPs in their jurisdictions, implement the Travel Rule for crypto transfers above applicable thresholds, and maintain records of counterparty VASPs. The compliance cost for this alone is significant, especially for teams that built their tech stack before these requirements existed.

Stricter Beneficial Ownership Requirements

Across the US and EU, beneficial ownership disclosure rules tightened substantially in 2025-2026. The FinCEN Beneficial Ownership Information (BOI) database went fully operational, and fintechs that onboard business customers are now expected to verify and regularly refresh beneficial ownership data, not just collect it at onboarding.

This is a real operational burden. A business customer that looked straightforward at onboarding may have had ownership changes, sanctions exposure, or shell company complications develop since. Compliance programs need a refresh mechanism, not just a one-time check.

The European Banking Authority has published parallel guidance for EU-based fintechs, specifically around sixth Anti-Money Laundering Directive (AMLD6) requirements for ongoing customer monitoring and cross-border information sharing between national supervisors.

The Rise of Regulatory Penalties

It's worth being direct about what's happening with enforcement. Regulators globally have raised both the frequency and size of AML penalties. The UK's Financial Conduct Authority, FinCEN in the US, and the European Banking Authority have all signaled increased scrutiny on fintechs specifically, not just traditional banks.

The pattern in recent enforcement actions is telling: penalties most commonly follow not from single catastrophic failures, but from systematic gaps. Inadequate transaction monitoring coverage, SAR filing delays, weak KYC at onboarding, and poor documentation of risk decisions are the most common culprits. These are fixable problems. Most fintechs getting fined aren't operating criminal enterprises; they're operating compliance programs that were built for a lower-scrutiny era.

The Core Components of a Fintech AML Program

A functional AML program in 2026 isn't optional architecture. It's the baseline requirement for any fintech that processes payments, extends credit, or holds customer funds. Here's what actually needs to be in place.

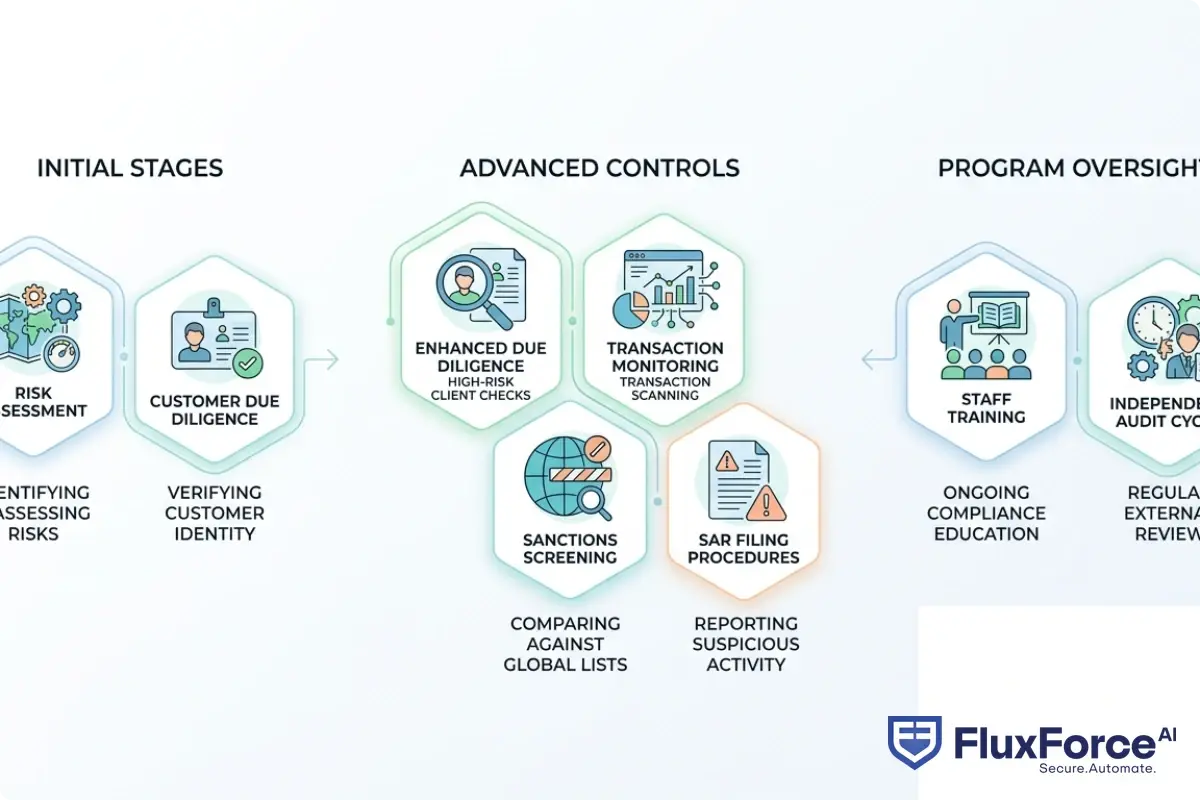

Customer Due Diligence and Enhanced KYC

Customer Due Diligence (CDD) is the foundation. It covers identity verification at onboarding, ongoing monitoring of customer behavior, and Enhanced Due Diligence (EDD) for higher-risk customers. The distinction between standard and enhanced diligence is a judgment call your program needs to make systematically, not case by case.

For fintechs onboarding retail customers, this typically means identity document verification with liveness checks, sanctions and PEP screening at onboarding and on an ongoing basis, source of funds documentation for higher-risk profiles, and periodic KYC refresh cycles based on risk tier.

For business customers, the requirements are heavier. Beneficial ownership verification, business registration documents, UBO screening, and ongoing transaction pattern reviews are all standard expectations now. Our post on AML risk checks and KYC identity verification strategy for claims directors covers how the same CDD logic applies across regulated product types beyond payments.

Transaction Monitoring Systems

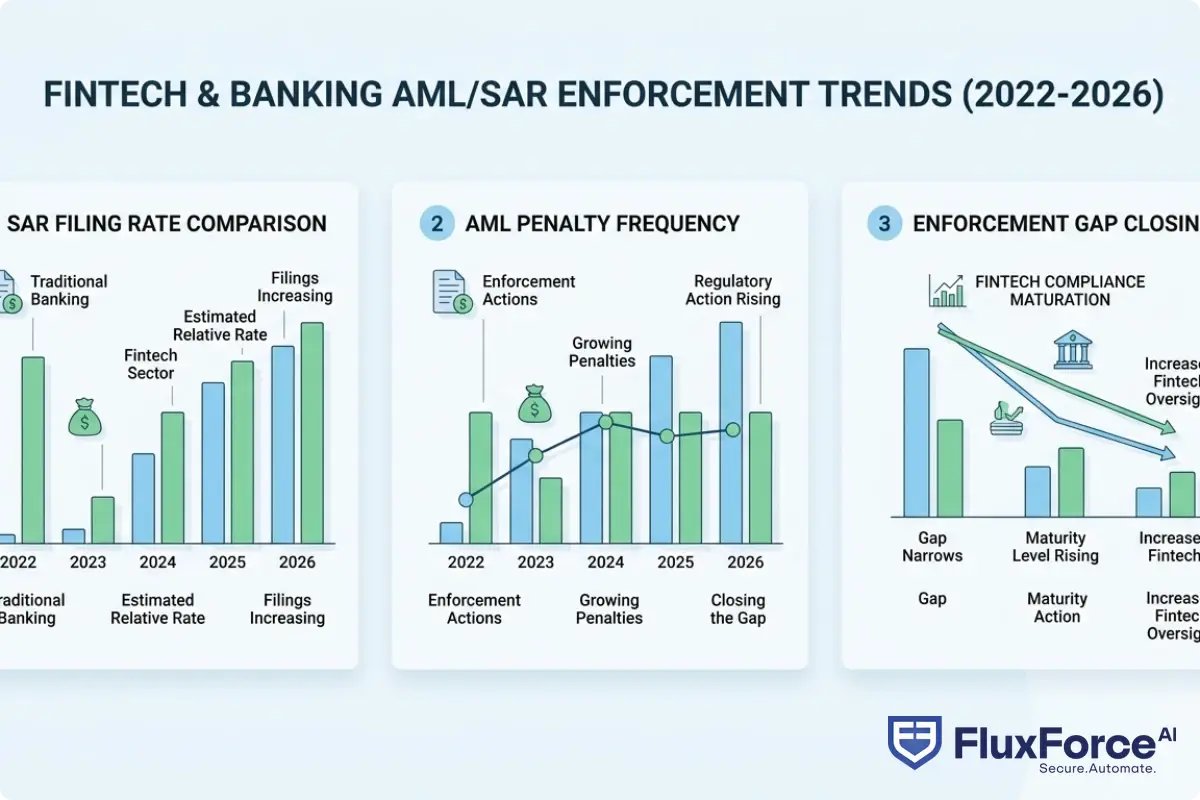

Transaction monitoring is where most fintechs have their most significant gaps. Static rule-based systems built around fixed thresholds catch some suspicious activity but generate enormous false positive rates. In practice, 95-99% of alerts produced by rule-based systems turn out to be legitimate transactions. That's not a compliance program; that's a noise machine.

In practice, 95-99% of alerts produced by rule-based systems turn out to be legitimate transactions.

The shift toward behavioral analytics and ML-driven monitoring is well underway. AML screening in digital lending illustrates how this plays out specifically in credit products. The key shift is from flagging any transaction above $10,000 to flagging transactions that deviate from a customer's expected behavioral pattern. The latter requires more upfront work to build customer behavioral baselines, but it produces alerts that analysts can actually act on.

The key shift is from flagging any transaction above $10,000 to flagging transactions that deviate from a customer's expected behavioral pattern.

Suspicious Activity Reporting Obligations

SAR filing requirements exist in every major jurisdiction. In the US, fintechs registered as money services businesses (MSBs) must file SARs with FinCEN within 30 days of detecting suspicious activity. In the EU, reports go to national financial intelligence units (FIUs). The regulatory expectation is not that you file perfectly; it's that your program has documented procedures for evaluating and making SAR decisions consistently.

The failure mode here is usually documentation, not intent. Fintechs often make reasonable judgments about suspicious activity but don't document the decision-making process. When examiners come in, the absence of documented reasoning looks like a broken program even when the underlying decisions were sound.

How AI Is Reshaping AML Compliance in Fintech

This is where compliance programs are seeing the biggest structural change. AI-driven tools aren't just faster; they do things that rule-based systems structurally can't.

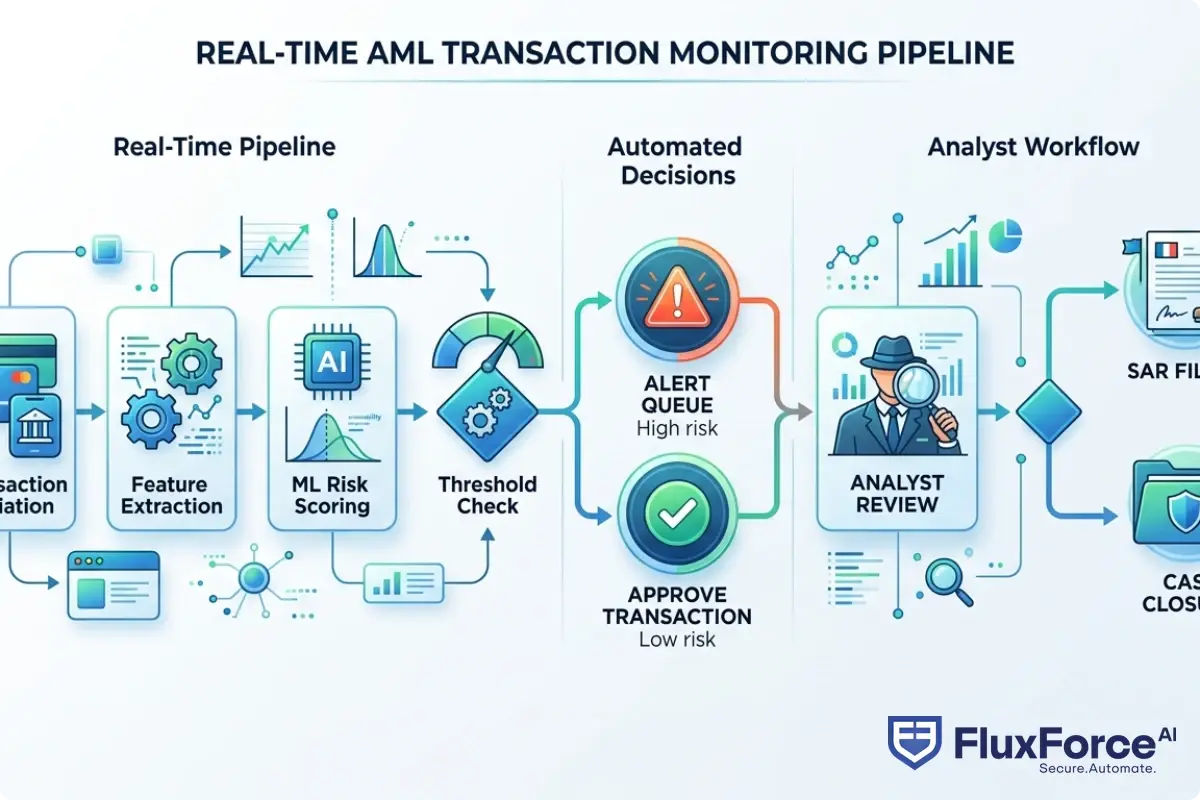

Machine Learning for Transaction Monitoring

Machine learning models can evaluate hundreds of features per transaction simultaneously: the amount, the timing, the counterparty, the geographic pattern, the merchant category, how this customer has behaved over the past 90 days, and how that compares to similar customers. No static rule set can replicate that analysis.

The practical benefit shows up in alert quality. Well-tuned ML models in production typically reduce false positive rates by 60-80% compared to rule-based baselines. That matters operationally: if your compliance team is reviewing 500 alerts per week and 490 of them are false positives, analysts are spending most of their time confirming that legitimate transactions are legitimate. Reducing that ratio means more investigative capacity applied to real cases.

How agentic AI fraud agents cut false positives by 80% explores the mechanics of this in detail. Models trained on labeled historical data learn the difference between unusual-but-legitimate and genuinely suspicious in ways that rule thresholds simply can't encode.

Reducing False Positives with AI

The false positive problem is an underappreciated compliance risk. When analysts are buried in low-quality alerts, they start taking shortcuts: approving cases faster than the situation warrants, missing patterns across multiple low-value transactions, or building informal shortlists that bypass proper review. These shortcuts are exactly what regulators find during examinations.

AI-driven alert triage, where models score and prioritize alerts by likely risk level before they reach human analysts, directly addresses this. Analysts work from the top of the risk queue down. The result is more investigative capacity applied to the cases most likely to warrant it, rather than spread thinly across hundreds of false alarms.

Real-Time Risk Scoring

Modern AML programs don't just process transaction batches overnight. Real-time risk scoring evaluates each transaction as it processes and can flag or hold transactions before settlement. For fintechs processing high-volume payments, this means you're not discovering that you processed 10,000 suspicious transactions last Tuesday; you're catching them as they happen.

The tradeoff is real: real-time scoring requires low-latency infrastructure and well-calibrated models. Get it wrong and you create false holds that damage customer experience. This is one reason the shift to real-time monitoring is typically a 6-18 month implementation project, not something you can switch on overnight.

Building a Risk-Based AML Framework

The risk-based approach is the regulatory expectation in every major framework. FATF, FinCEN, AMLD6, and the UK's Money Laundering Regulations all require it. But risk-based can become a vague justification for inconsistency if it isn't operationalized carefully.

Risk Assessment Methodology

A credible risk assessment identifies the specific money laundering and terrorist financing risks your business faces, evaluates the likelihood and impact of each, and maps your controls to those risks. It's not a document you file once; it should be a living assessment that updates when your product, customer base, or regulatory environment changes.

In practice, a fintech risk assessment should cover product-specific risks (what types of financial crime could your product facilitate?), customer risk categories (what segments carry higher risk and why?), channel risks (direct vs. partner-onboarded customers), and geographic exposure to higher-risk jurisdictions. If your risk assessment was written two years ago and hasn't been touched since, it's probably already out of date.

Customer Risk Tiering

Once you have a risk assessment, you need a tiering model that applies it to individual customers. The typical structure is three-tier: standard, medium, and high risk. What drives placement in each tier should be documented explicitly: sanctions matches, PEP status, high-risk jurisdiction connections, business type, transaction patterns, or any combination.

This tiering should drive real operational differences in monitoring intensity, review frequency, and EDD requirements. A tiering model that doesn't actually change how you treat customers is just paper compliance. Regulators know what that looks like, and they don't give credit for it.

What Regulators Are Watching in 2026

If you want to know where to focus your compliance resources, look at what's appearing in enforcement actions. Three areas are getting disproportionate attention right now.

FATF Travel Rule Enforcement

The Travel Rule requires fintechs and VASPs to transmit originator and beneficiary information with crypto transfers above certain thresholds. In 2026, enforcement has caught up with the policy. Firms that were technically non-compliant for years because enforcement was lax are now getting examined.

Implementation is genuinely complex, especially for fintechs that need to work with counterpart VASPs across multiple jurisdictions with different thresholds and technical standards. The interoperability problem hasn't been fully solved. But the fact that implementation is technically complicated doesn't satisfy regulators who expect you to have a roadmap and evidence of active progress.

Crypto and DeFi AML Obligations

DeFi creates real compliance challenges that don't have clean solutions. When you're dealing with protocols rather than counterparties, the standard CDD framework doesn't map cleanly. Regulators know this. What they're looking for is evidence that fintechs with DeFi exposure have assessed the risk, implemented controls appropriate to what's technically possible, and documented their reasoning.

The worst outcome is ignoring the question entirely. A fintech that can show a documented analysis of DeFi risks with honest acknowledgment of limitations is in a much better position than one that has made no effort at all.

Cross-Border Payment Scrutiny

Cross-border payment flows are under increased examination, particularly flows involving jurisdictions on FATF's grey list or jurisdictions with known trade-based money laundering exposure. If a meaningful percentage of your transaction volume involves these geographies, expect that to be a focus area in any regulatory examination.

The sanctions screening automation strategies for CISOs covered on our site are directly relevant here. Automated sanctions screening with documented override procedures is the baseline expectation now; manual screening at scale stopped being credible a long time ago.

Common AML Compliance Failures (and How to Avoid Them)

The same patterns appear in enforcement actions over and over. Here are the most relevant ones for fintechs operating in 2026.

Gaps in Transaction Monitoring Coverage

Not monitoring certain transaction types or customer segments because they were deemed low-risk at program design is a recurring problem. Product expansions, new customer types, and new payment rails frequently get added without updating monitoring coverage. A fintech that launched with P2P payments and added crypto buy/sell two years later may be monitoring the P2P flows adequately but not the crypto activity.

The fix is a monitoring coverage audit: map every product, transaction type, and customer segment against your monitoring controls and document explicitly what's covered, how, and at what thresholds. Gaps should trigger either control additions or documented risk acceptance decisions, not silence.

Inadequate SAR Filing Practices

Common SAR failures include late filing (missing the 30-day window after detection), insufficient narrative detail in the descriptions, and inconsistent filing decisions across similar cases. Some of these problems come from under-resourced teams handling alert volumes they weren't staffed for.

Adding automation to the triage and documentation layer can free analyst capacity for the judgment-intensive parts that require human review. The honest reality is that a compliance team stretched thin across too many low-quality alerts will eventually cut corners, and those corners are exactly what examiners look for.

How to Operationalize Your AML Compliance Program

Knowing what a good program looks like is one thing. Actually building it inside a fintech that's also trying to grow, ship product, and manage costs is another challenge entirely.

Staffing and Training Requirements

The minimum viable AML team for a regulated fintech typically includes a dedicated BSA/AML Officer (a regulatory requirement in the US for MSBs), at least one or two compliance analysts handling ongoing monitoring and SAR review, and a compliance technology owner who understands both the regulatory requirements and the underlying tech stack.

Training is non-negotiable. Annual AML training for all employees plus role-specific training for anyone with compliance-relevant responsibilities is the baseline expectation. Document attendance carefully. Regulators ask for training records, and a missing log looks as bad as no training at all.

Technology Stack Considerations

The technology decisions matter more than most fintechs acknowledge early on. A compliance program built on spreadsheets and basic rule engines may work at low transaction volumes, but it won't scale, and the technical debt it creates makes the eventual upgrade far harder.

Core components of a modern AML tech stack include a KYC and identity verification layer, a sanctions and PEP screening service, a transaction monitoring system with ML capabilities, a case management tool for investigation workflow, and a SAR filing interface. These can be separate vendors or a consolidated platform depending on your scale. The important thing is that each component has clear ownership, documented configuration, and a defined process for updates as new money laundering typologies emerge.

Vendor Due Diligence for AML Tools

Relying on a third-party compliance vendor doesn't transfer regulatory responsibility. If your transaction monitoring vendor misses something, you're still accountable. You need to understand how your vendor's models work, what their false positive and false negative rates look like on your specific customer population, and what their process is for updating models when regulators publish new typologies.

The API security strategies for CISOs in banking covers related considerations for evaluating API-based compliance integrations from a security and resilience perspective. The same vendor due diligence logic applies directly to AML tooling decisions.

- The regulatory environment that fintechs operate in today looks meaningfully different from even 18 months ago.

- A functional AML program in 2026 isn't optional architecture.

- This is where compliance programs are seeing the biggest structural change.

- The risk-based approach is the regulatory expectation in every major framework.

- If you want to know where to focus your compliance resources, look at what's appearing in enforcement actions.

Onboard Customers in Seconds

Conclusion

AML compliance fintech 2026 is not the same program you could have run two years ago. The regulatory floor has risen, enforcement is more active, and the volume and complexity of transactions that regulated fintechs process has grown faster than most compliance programs have adapted to.

The fintechs getting it right aren't necessarily the largest or best-funded. They're the ones that did the unglamorous work: documenting risk assessments honestly, building transaction monitoring coverage that actually covers all their products, staffing their compliance function proportionally to their risk profile, and investing in automation where it reduces noise rather than just replacing human judgment wholesale.

If your current program has gaps, the right move is to identify and document them now rather than wait for an examiner to find them. A documented remediation plan is a far better starting point than an undocumented problem. Regulators don't expect perfection; they expect a credible, good-faith effort to manage real risks with real controls. That's the standard worth building toward in 2026.

Share this article