.webp)

Introduction

Synthetic identity fraud has become one of the most costly threats facing financial institutions in 2026. Unlike traditional identity theft where criminals steal real person's data, synthetic fraud combines real and fabricated information to create entirely new identities that don't exist. These ghost profiles can operate undetected for months or even years before financial institutions realize they've been compromised.

For CISOs, compliance officers, and risk teams, understanding synthetic identity fraud detection patterns is no longer optional. The Federal Reserve estimates that synthetic identity fraud costs the financial industry over $6 billion annually, with losses growing 25% year over year. This guide breaks down the five critical detection patterns your team needs to implement now.

The Federal Reserve estimates that synthetic identity fraud costs the financial industry over $6 billion annually, with losses growing 25% year over year.

- What is synthetic identity fraud and how does it work?

- Pattern 1: Cross-bureau data inconsistencies

- Pattern 2: Unusual credit building velocity

- Pattern 3: Digital footprint anomalies

- Pattern 4: Behavioral biometrics and device signals

Onboard Customers in Seconds

What is synthetic identity fraud and how does it work?

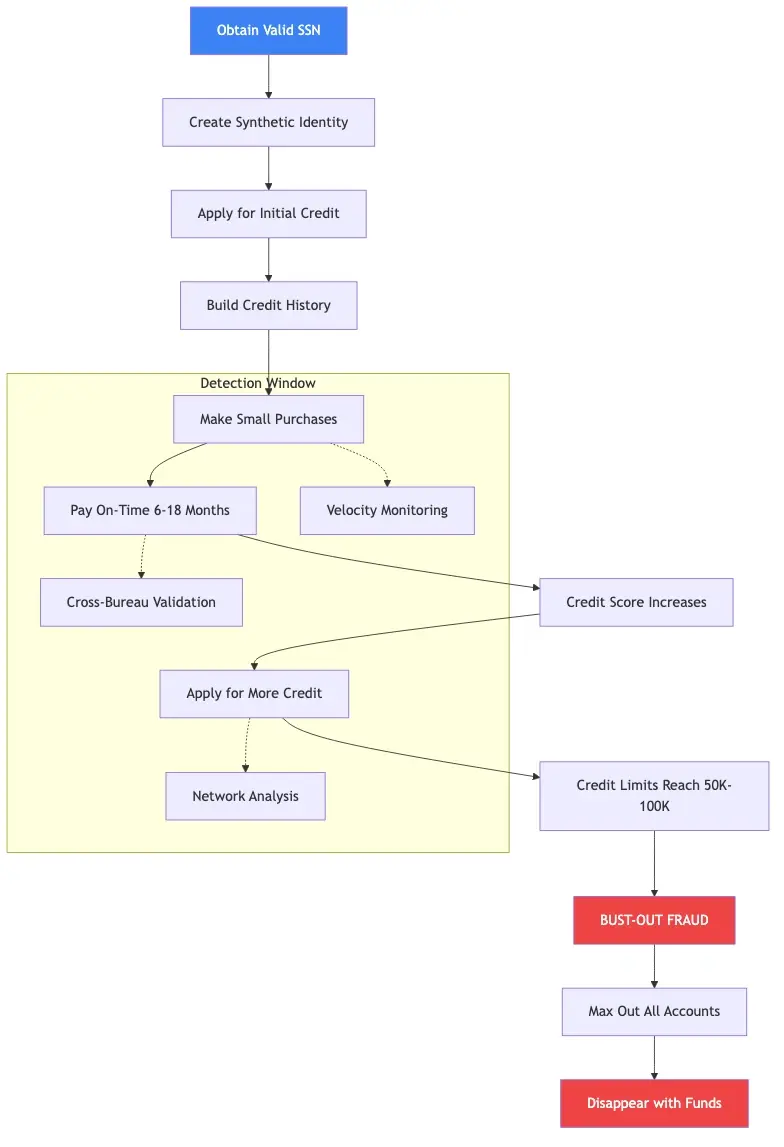

Synthetic identity fraud occurs when criminals combine real personal information (like Social Security numbers) with fabricated details to create hybrid identities that appear legitimate but don't belong to any real person.

Unlike traditional identity theft, synthetic fraud targets credit files rather than existing bank accounts. Criminals typically use real SSNs from children, elderly individuals, or others who don't actively monitor their credit. They pair these with fake names, addresses, and dates of birth to build credit profiles from scratch.

How synthetic identity fraud rings operate

The process follows a predictable pattern that compliance officers should recognize:

- Identity synthesis: Criminals obtain valid SSNs through data breaches, dark web markets, or social engineering

- Credit file creation: They apply for credit using the synthetic identity, building a credit history over 6-18 months

- Credit building: Small purchases are made and paid off to establish good credit scores

- Bust-out fraud: Once credit limits reach $50,000-$100,000, criminals max out all accounts and disappear

This patient approach makes synthetic fraud detection incredibly difficult. Traditional fraud detection systems flag unusual activity, but synthetic identities build legitimate-looking credit histories over time.

The difference between synthetic and traditional identity fraud

Understanding this distinction matters for fraud detection strategy. Traditional identity theft involves stealing an existing person's complete identity. The victim notices quickly when their credit card gets charged or their bank account gets drained. Synthetic identity fraud creates victims who may not know their SSN is being used for years.

Children are particularly vulnerable because their clean credit files won't be checked until they apply for student loans or their first job. By then, the synthetic identity may have accumulated thousands in debt under their SSN.

Pattern 1: Cross-bureau data inconsistencies

One of the strongest synthetic fraud detection signals comes from comparing data across the three major credit bureaus. Synthetic identities often show different information at Experian, Equifax, and TransUnion because criminals don't update all bureaus simultaneously.

Identity verification fraud red flags

Look for these specific inconsistencies:

- Name variations: Slight spelling differences across bureaus ("Jon" vs "Jonathan", "Sara" vs "Sarah")

- Address gaps: One bureau shows a current address while others show no address history

- SSN issuance date mismatches: The SSN issue date doesn't align with the stated birth date

- Employment inconsistencies: Different employers reported to different bureaus

These discrepancies seem minor individually but form a clear pattern when viewed together. Manual review teams often miss these signals because they're checking one bureau at a time.

How to detect synthetic identity fraud in banking

Banks should implement automated cross-bureau validation that runs on every new account application. The system should flag applications where:

- SSN was issued less than 5 years ago to someone claiming to be over 25

- No credit file exists despite the applicant claiming extensive credit history

- Address on application doesn't match any bureau records

- Phone number has been associated with 5+ different SSNs in the past year

According to the Federal Trade Commission, cross-referencing multiple data sources reduces synthetic fraud losses by up to 40%.

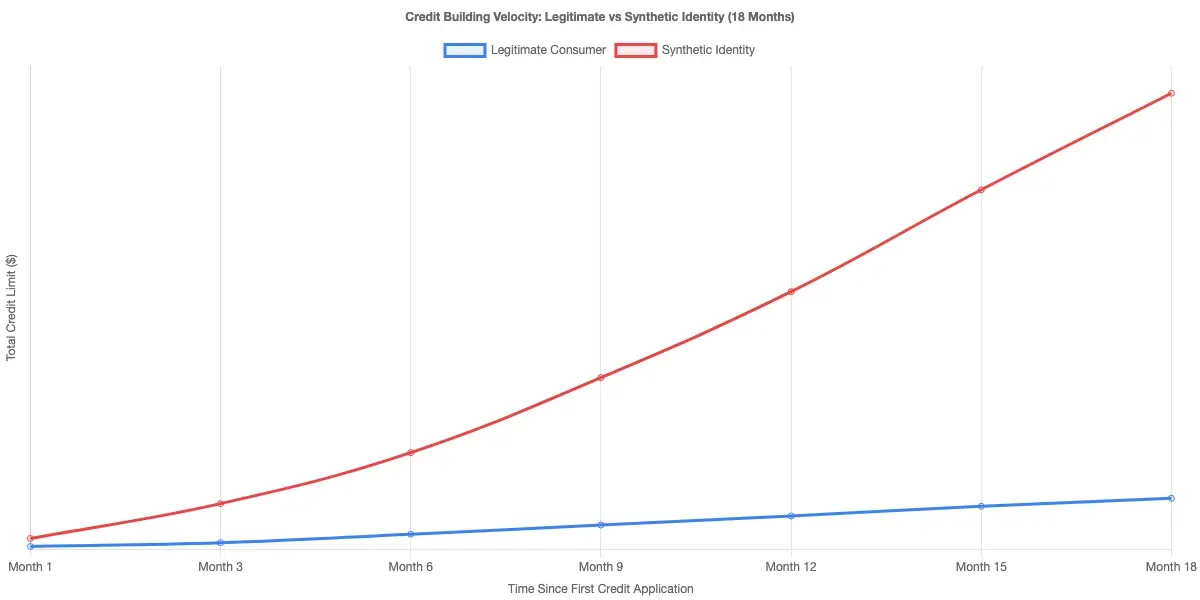

Pattern 2: Unusual credit building velocity

Synthetic identities build credit faster than legitimate consumers, creating detectable velocity patterns. Real people typically have gradual credit growth with occasional inquiries. Synthetic identities show aggressive, linear credit building.

Fraudulent account creation patterns

Watch for these velocity red flags:

- Account opening velocity: 3+ new credit accounts within 90 days

- Credit limit utilization: Consistently using 80-95% of available credit, then paying down to 0%

- Inquiry clustering: Multiple hard inquiries within a 2-week window across different lenders

- Payment perfection: 100% on-time payments with no missed minimums

Legitimate consumers miss payments occasionally. They don't max out cards then pay in full every month. This "too perfect" behavior signals synthetic fraud detection teams should investigate.

Machine learning models for synthetic fraud detection

Modern AI fraud detection systems analyze velocity patterns across thousands of data points. Machine learning models can identify synthetic identities with 85-92% accuracy compared to 60-70% for rule-based systems. The key advantage is recognizing subtle patterns humans miss.

For example, an ML model might flag an identity that:

- Opens accounts only on Tuesdays (automation pattern)

- Always pays at 2:47 PM (scheduled payment pattern)

- Uses the same device fingerprint across multiple applications

- Has credit inquiries from geographically distant lenders on the same day

These micro-patterns combine to create a fraud score that triggers manual review before the bust-out occurs.

Pattern 3: Digital footprint anomalies

Synthetic identities lack the digital breadcrumbs that real people leave behind. In 2026, legitimate consumers have extensive online presence across social media, utility accounts, and e-commerce platforms. Synthetic identities often exist only in credit bureau databases.

Fake identity prevention through digital validation

Implement these digital footprint checks:

- Social media verification: No LinkedIn, Facebook, or Instagram presence for someone claiming to be 30+ years old

- Email age: Email address created less than 6 months ago despite applicant claiming long credit history

- Phone number validation: Mobile number is prepaid/VoIP rather than postpaid contract

- Utility records: No utility bills, insurance policies, or subscription services in the name

Experian's 2025 fraud report found that 78% of synthetic identities had no verifiable digital footprint beyond credit bureau records.

Experian's 2025 fraud report found that 78% of synthetic identities had no verifiable digital footprint beyond credit bureau records.

Deepfake and synthetic media detection in identity verification workflows

The rise of AI-generated documents adds complexity to synthetic fraud detection. Criminals now use generative AI to create fake utility bills, pay stubs, and bank statements that pass visual inspection. Your verification workflow must include:

- Document authentication: Check for AI generation artifacts in uploaded documents

- Reverse image search: Verify profile photos aren't AI-generated or stock images

- Metadata analysis: Examine document metadata for creation dates and editing software

- Third-party verification: Contact utility companies or employers directly rather than relying on uploaded documents

For more on implementing deepfake detection in customer onboarding, see our guide on Detecting Synthetic Identity Fraud in Real-Time.

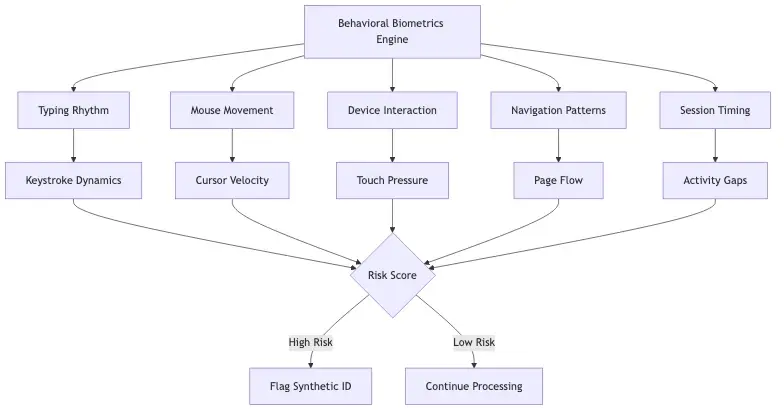

Pattern 4: Behavioral biometrics and device signals

Behavioral biometrics provides continuous authentication signals that synthetic identities can't easily fake. How someone types, moves their mouse, and interacts with your application reveals whether they're a real person or automated fraud script.

Behavioral biometrics implementation for continuous authentication

Deploy these behavioral signals:

- Typing dynamics: Keystroke pressure, rhythm, and error patterns

- Mouse movement: Natural curves and acceleration vs robotic straight lines

- Device interaction: Touch pressure, swipe patterns, and screen navigation

- Session behavior: Time spent reading terms, scrolling patterns, form completion speed

Synthetic fraud operations often use automated scripts or low-wage workers in fraud mills. Neither replicates natural human behavior patterns. Behavioral biometrics can flag these applications before they reach manual review.

Identity synthesis attacks through device fingerprinting

Device fingerprinting reveals connections between seemingly unrelated applications:

- Same device, multiple identities: One device submitting applications under 5+ different names

- Emulator detection: Applications coming from Android emulators rather than physical devices

- VPN/proxy usage: IP addresses from known fraud hotspots or data centers

- Browser fingerprinting: Identical browser configurations across multiple applications

When combined with behavioral signals, device fingerprinting creates a powerful synthetic fraud detection layer. Our analysis shows this combination reduces false positives by 60% while catching 35% more synthetic identities.

For banking teams implementing zero trust architectures, behavioral biometrics integrates naturally with existing security frameworks. Learn more in our Zero Trust Security for Mobile-First Banks guide.

Pattern 5: Network and relationship mapping

Synthetic identities don't exist in isolation, they connect to other fraud rings through shared data points. Network analysis reveals these connections that individual application review misses.

How synthetic identity fraud rings operate at scale

Fraud rings operate like legitimate businesses with division of labor:

- Data suppliers: Obtain SSNs and personal information through breaches or social engineering

- Document forgers: Create fake supporting documents (utility bills, pay stubs)

- Application submitters: Submit applications across multiple financial institutions

- Cash-out operators: Execute the bust-out and launder the proceeds

This specialization creates detectable patterns. The same phone number, email domain, or device might appear across dozens of applications under different names.

Synthetic identity fraud red flags for compliance officers

Network analysis should flag:

- Shared contact information: 3+ applications using the same phone number with different names

- Address clustering: Multiple applications from the same address or mail drop

- Employer patterns: Applications claiming employment at companies that don't exist

- Beneficiary connections: Multiple accounts naming each other as beneficiaries or authorized users

Graph database technology excels at this analysis. Instead of checking each application in isolation, graph databases map relationships and surface suspicious clusters automatically.

Third-party vendor risk assessment automation

Don't forget that synthetic fraud can enter through vendor partnerships. Third-party vendors with weak KYC processes can introduce synthetic identities into your ecosystem. Implement vendor risk assessments that include:

- KYC process audits: Verify vendors use the same synthetic fraud detection standards

- Data sharing agreements: Require vendors to report suspected synthetic identities within 24 hours

- Periodic re-verification: Re-audit vendor KYC processes annually

- Integration security: Ensure API connections don't bypass your fraud detection systems

For supply chain and logistics teams, vendor risk is especially critical. Read our High-Risk Supplier Validation guide for implementation details.

AI vs rule-based synthetic identity detection

The shift from rule-based to AI-powered detection represents the biggest advancement in synthetic fraud prevention. Rule-based systems catch known patterns but miss evolving tactics. AI systems learn from new data and adapt to emerging fraud techniques.

Comparison of detection accuracy

| Detection Method | Accuracy Rate | False Positive Rate | Time to Detect |

|---|---|---|---|

| Manual review | 45-55% | 15-20% | 3-5 days |

| Rule-based systems | 60-70% | 25-30% | Real-time |

| Machine learning | 85-92% | 8-12% | Real-time |

| AI + behavioral biometrics | 90-95% | 5-8% | Real-time |

The business case for AI-powered detection is clear. A mid-size bank processing 10,000 applications monthly could prevent $2-4 million in annual synthetic fraud losses by upgrading from rule-based to AI detection.

Best synthetic fraud detection software for banks

When evaluating vendors, prioritize these capabilities:

- Real-time scoring: Decisions in under 500 milliseconds to avoid application friction

- Explainable AI: Clear reasoning for declined applications to meet regulatory requirements

- Continuous learning: Models that update automatically as fraud tactics evolve

- Integration flexibility: APIs that work with your existing core banking and CRM systems

- Compliance reporting: Built-in audit trails for regulatory examinations

The cost of synthetic identity fraud to financial institutions makes this investment essential, not optional. Banks still using manual review or basic rule systems are losing 3-5x more to synthetic fraud than competitors with AI-powered detection.

Synthetic identity fraud prevention best practices

Effective synthetic fraud prevention requires a layered defense strategy. No single detection method catches all synthetic identities. The best programs combine multiple signals with clear escalation procedures.

Implementation roadmap for compliance teams

Month 1-2: Foundation

- Audit current detection methods and identify gaps

- Implement cross-bureau data validation

- Deploy device fingerprinting on all digital channels

Month 3-4: Enhancement

- Add behavioral biometrics to application flows

- Integrate network analysis for relationship mapping

- Train manual review teams on synthetic fraud patterns

Month 5-6: Optimization

- Deploy machine learning models for real-time scoring

- Implement continuous monitoring for existing accounts

- Establish feedback loops to improve model accuracy

AI model governance and documentation for regulatory audits

Regulatory scrutiny of AI fraud detection continues to increase. Your AI model governance framework must include:

- Model documentation: Clear records of training data, features, and decision logic

- Bias testing: Regular audits to ensure models don't discriminate against protected classes

- Performance monitoring: Track accuracy, false positives, and drift over time

- Human override: Manual review process for borderline cases and customer appeals

For detailed guidance on AI model governance, see our AI Model Governance Framework for Financial Services Audits.

The cost of inaction: synthetic identity fraud loss statistics 2026

Synthetic identity fraud isn't a future threat, it's happening now with devastating financial impact. The numbers tell a clear story about the urgency of implementing robust detection systems.

Key statistics for risk committees

- $6.2 billion: Annual losses to US financial institutions from synthetic identity fraud

- 25%: Year-over-year growth rate in synthetic fraud attempts

- 18 months: Average time before synthetic identities are detected

- 80%: Of synthetic fraud losses occur in the bust-out phase (preventable with early detection)

- $30,000: Average loss per synthetic identity bust-out

These numbers represent more than financial losses. Synthetic fraud damages customer trust, increases compliance scrutiny, and diverts resources from legitimate business growth.

Machine learning fraud detection ROI for banks

The ROI calculation for AI-powered detection is straightforward:

Annual savings = (Current fraud losses × Detection improvement %) − Implementation cost

For a regional bank losing $5 million annually to synthetic fraud:

For a regional bank losing $5 million annually to synthetic fraud:

- Current detection rate: 50% (manual review)

- AI detection rate: 90%

- Fraud prevented: $2 million annually

- Implementation cost: $400,000

- First-year ROI: 400%

Beyond direct fraud prevention, AI systems reduce manual review workload by 60-70%, freeing analysts to focus on complex cases that require human judgment.

- Synthetic identity fraud occurs when criminals combine real personal information (like Social Security numbers) with fabricated details to create hybrid identities that appear legitimate but don't belong to any real person.

- One of the strongest synthetic fraud detection signals comes from comparing data across the three major credit bureaus.

- Synthetic identities build credit faster than legitimate consumers, creating detectable velocity patterns.

- Synthetic identities lack the digital breadcrumbs that real people leave behind.

- Behavioral biometrics provides continuous authentication signals that synthetic identities can't easily fake.

Onboard Customers in Seconds

Conclusion

Synthetic identity fraud represents one of the most sophisticated threats facing financial institutions in 2026. The five detection patterns we've covered, cross-bureau inconsistencies, credit velocity anomalies, digital footprint gaps, behavioral biometrics signals, and network relationships, provide a comprehensive framework for identifying synthetic identities before bust-out occurs.

The technology exists to detect 90%+ of synthetic fraud attempts in real-time. Banks and fintechs still relying on manual review or basic rule-based systems are leaving money on the table and exposing themselves to unnecessary risk. The question isn't whether you can afford to implement AI-powered synthetic fraud detection. It's whether you can afford not to.

For teams ready to move forward, start with a gap analysis of your current detection capabilities. Map your existing controls against the five patterns outlined here. Identify which signals you're missing and prioritize implementation based on your specific risk profile and customer segments.

The synthetic fraud threat will only grow more sophisticated. Your detection capabilities must evolve faster than criminal tactics. With the right combination of AI, behavioral biometrics, and network analysis, financial institutions can stay ahead of synthetic identity rings and protect both their bottom line and their customers.

Share this article