.webp)

Introduction

KYC automation is reshaping how banks onboard customers. What once took 5 to 7 business days now completes in under 4 hours at institutions using AI-driven identity verification and document processing. For compliance officers and CISOs navigating tighter regulatory scrutiny in 2026, that speed matters. But the bigger question is not how fast you can onboard someone. It is whether automated KYC onboarding without compliance risk is actually achievable. The short answer: yes, if you architect it correctly. This guide covers how leading banks are doing it, what regulators expect from AI-driven compliance decisions, and where the ROI actually comes from for mid-tier and community institutions.

- What Is KYC Automation and How Does It Work?

- How KYC Automation Cuts Digital Banking Onboarding Time

- AML Transaction Monitoring: Reducing False Positives with Machine Learning

- How Do Regulators Evaluate Explainable AI in Compliance Decisions?

- Biometric Identity Verification and Cross-Border Payment Security

Onboard Customers in Seconds

What Is KYC Automation and How Does It Work?

KYC automation uses AI, machine learning, and API-driven data pipelines to replace or augment the manual steps in customer identity verification. At its core, a digital KYC platform does three things: it collects identity documents and biometric data, cross-references them against authoritative sources, and flags or approves applicants based on risk scoring models, all without a human reviewing each file individually.

The FATF Digital Identity Guidance defines a risk-based approach to digital identity that most national regulators now reference directly. Your KYC automation architecture needs to align with those same risk tiers from day one, or you will face examination findings before the ink is dry on your go-live memo.

KYC vs. AML Automation: What Is the Difference?

KYC automation handles identity verification at account opening. AML transaction monitoring operates continuously after the account is live, watching for suspicious activity patterns. They are complementary, not interchangeable. Conflating the two creates compliance gaps: an institution can have excellent onboarding controls but weak ongoing monitoring, or vice versa.

KYC AML compliance automation banks implement today usually covers both layers, but the tooling differs. KYC tools focus on document processing, biometrics, and sanctions matching. AML tools focus on transaction behavior, velocity analysis, and network graph detection.

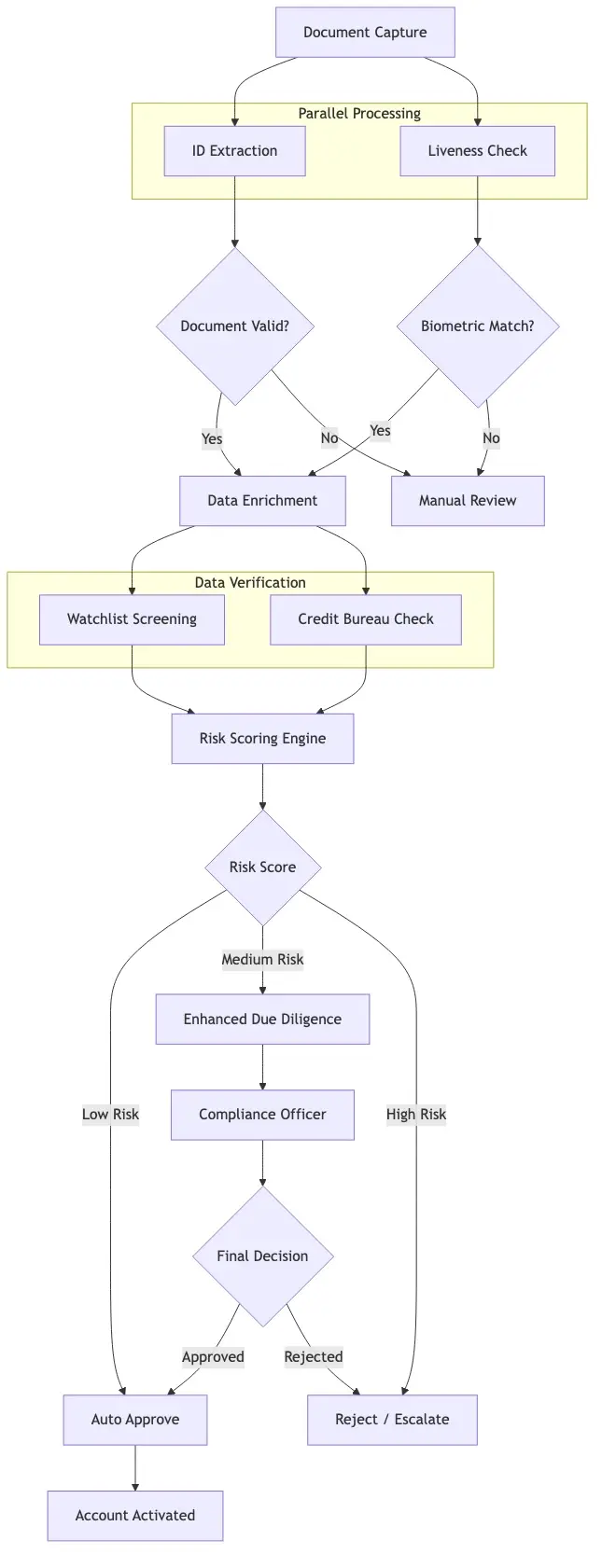

Core Components of an Automated KYC Platform

A production-ready KYC automation software stack typically includes:

- Document capture and OCR extraction: Passport, national ID, and utility bill processing with confidence scoring

- Liveness detection and facial biometric matching: Comparing a selfie or short video to the ID photo, with anti-spoofing controls

- Database and watchlist checks: PEP lists, sanctions databases (OFAC, EU, UN), and adverse media feeds

- Risk-based decisioning engine: Scoring applicants based on country risk, document quality, and behavioral signals

- Audit trail generation: Structured logs that satisfy regulatory examination requirements

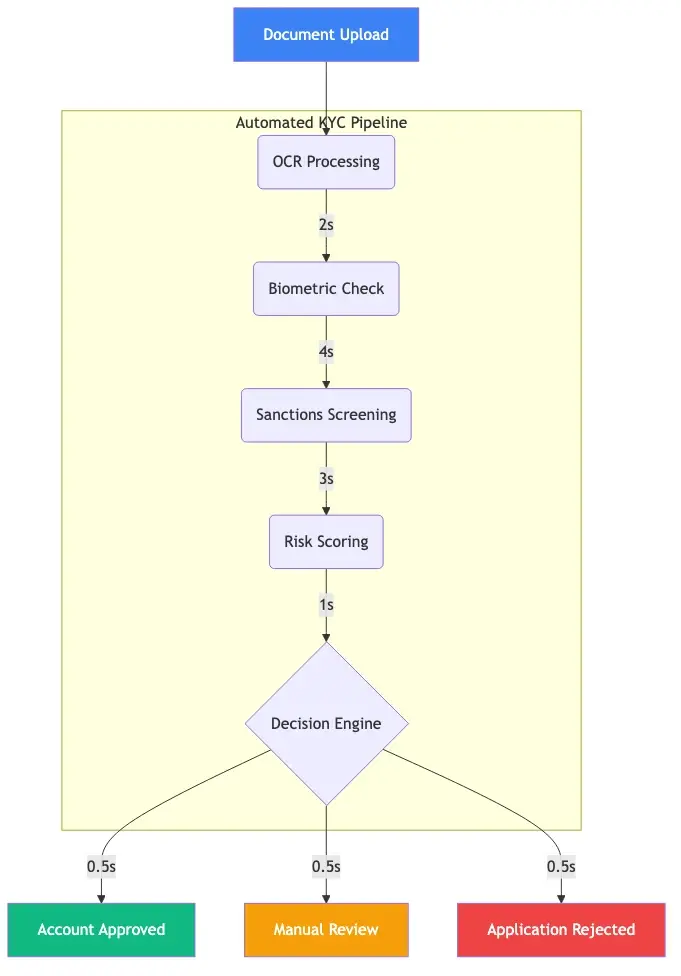

How KYC Automation Cuts Digital Banking Onboarding Time

KYC automation for digital banking onboarding typically reduces the end-to-end process from 5 to 7 days to under 4 hours. McKinsey banking operations research puts the average onboarding time reduction at 70 to 80% for institutions that fully automate document verification and risk scoring. The savings come from eliminating three specific bottlenecks: manual document review queues, analyst time spent on low-risk applicants, and back-and-forth document re-submission loops caused by unclear rejection reasons.

McKinsey banking operations research puts the average onboarding time reduction at 70 to 80% for institutions that fully automate document verification and risk scoring.

How to Reduce KYC Onboarding Time with AI

The honest answer on how to reduce KYC onboarding time with AI is to start with straight-through processing for your lowest-risk segments. If 60% of your applicants are domestic, low-risk individuals with clean document scans, those should auto-approve. Reserve analyst time for the 10 to 15% that trigger edge cases.

Specific tactics that deliver measurable results:

- Pre-fill from trusted sources: Connect to government identity APIs or credit bureau data to reduce manual data entry errors before they trigger re-submission loops

- Confidence thresholds, not binary decisions: Set OCR confidence scores so borderline documents route to human review rather than auto-reject, reducing customer abandonment

- Parallel processing: Run document validation, sanctions screening, and biometric matching simultaneously rather than sequentially

Parallel processing alone typically cuts 30 to 40 minutes from average processing time, and it requires no changes to your risk scoring logic.

Automated KYC Onboarding Without Compliance Risk

The concern most compliance officers raise is valid: moving faster creates risk exposure. Automated KYC onboarding without compliance risk requires three non-negotiable controls.

First, your risk scoring model needs calibration against your actual customer population, not a generic industry benchmark. A regional bank in Southeast Asia has a different risk distribution than a US neobank. Second, track false-negative rates (approving a bad actor) separately from false positives. Most vendors optimize to reduce false positives because operations teams complain loudest about alert volume, but regulators care about false negatives. Third, every automated decision needs an auditable reason code, which connects directly to the explainability requirement regulators now enforce.

AML Transaction Monitoring: Reducing False Positives with Machine Learning

The false positive problem in AML transaction monitoring is genuinely costly. Industry estimates from ACAMS suggest more than 90% of alerts generated by traditional rule-based systems are false positives. Analysts spend the majority of their working hours dismissing alerts that should never have fired. That is not only an efficiency problem, it causes alert fatigue, which means real suspicious activity gets buried under noise.

Industry estimates from ACAMS suggest more than 90% of alerts generated by traditional rule-based systems are false positives.

AML False Positive Reduction with Machine Learning

AML false positive reduction with machine learning works by learning behavioral baselines for each customer segment rather than applying uniform velocity thresholds across the entire portfolio. A small business owner sending 40 wire transfers per month to three known suppliers should trigger different thresholds than a newly opened personal account doing the same activity.

Best-performing models combine:

- Supervised learning on historical SAR filings: Training on confirmed suspicious activity gives the model real signal from your actual fraud cases

- Unsupervised anomaly detection: Identifies patterns that do not match any known customer archetype, catching novel schemes that rule-based systems miss

- Network graph analysis: Flags transaction rings and structuring patterns that individual account-level rules never surface

Institutions deploying machine learning for AML monitoring consistently report 40 to 60% reductions in false positive volumes. A team that previously triaged 1,000 alerts per week can handle 1,600 with the same headcount. For a deeper look at agentic approaches to this problem, see how AI fraud agents cut false positives by 80%.

Real-Time ACH and Wire Fraud Detection

Real-time ACH wire fraud detection differs from batch AML monitoring because the intervention window is measured in seconds, not hours. For ACH and wire transfers, the fraud detection model needs to score the transaction before it settles.

The architecture uses low-latency inference pipelines with pre-computed customer risk scores. Each transaction triggers a delta check against the established baseline. If it exceeds the threshold, the payment holds for a 60-second review window before routing to an analyst. This works for high-value wires without adding friction to routine payroll runs. The card fraud parallel follows similar principles, which we covered in our AI-powered fraud detection strategy for risk heads.

How Do Regulators Evaluate Explainable AI in Compliance Decisions?

Explainable AI for financial regulators has moved from optional to expected in 2026. The US OCC, the EBA in Europe, and the Monetary Authority of Singapore have each issued guidance stating that AI models used in credit or fraud decisions must produce human-readable explanations. This is the question compliance officers are asking most urgently right now, and for good reason.

What Explainability Actually Means for Examiners

Explainability does not mean your data science team understands the model internals. It means an examiner can ask "why was this customer flagged?" and get a specific, documented answer. SHAP (SHapley Additive exPlanations) values and LIME (Local Interpretable Model-agnostic Explanations) are the most common technical methods. The output needs to translate into plain language for audit purposes: "This applicant was flagged because their address history showed three changes in six months and their stated income was 40% above the norm for the listed employer type."

The output needs to translate into plain language for audit purposes: "This applicant was flagged because their address history showed three changes in six months and their stated income was 40% above the norm for the listed employer type."

Explainable AI compliance also matters for fair lending. If a machine learning model systematically declines applicants from certain demographic groups or geographic areas, you need to detect and correct that before regulators do. AI-powered KYC platforms without this layer are increasingly failing examination.

A Practical Framework for Explainable AI Compliance

| Layer | What It Covers | Primary Audience |

|---|---|---|

| Technical explanation | Feature importance scores, model confidence, raw input values | Data science, internal audit |

| Decision rationale | Plain-language reason codes per decision | Compliance officer, customer |

| Population-level reporting | Disparate impact testing, model drift tracking | Regulator, board risk committee |

Building all three into your regulatory compliance automation stack from the start is significantly easier than retrofitting them onto a deployed model. The fraud detection AI systems that pass examinations in 2026 are the ones where this architecture was designed in, not bolted on afterward.

Biometric Identity Verification and Cross-Border Payment Security

Biometric KYC for cross-border payments addresses a specific friction point: international payment rails require identity confirmation at both the sending and receiving ends, but document standards vary dramatically by jurisdiction. A passport from one country may not be recognized by another system's verification library, and third-party identity brokers add latency that degrades the payment initiation experience for customers.

Modern identity verification KYC systems for cross-border use combine selfie liveness checks, NFC chip reading from e-passports, and cross-border identity network APIs that support international document libraries across 190 or more countries. The biometric matching itself runs in under 5 seconds. The bottleneck is usually the back-end sanctions and PEP check against multiple jurisdictional lists.

Sanctions Screening Automation and OFAC Compliance

Sanctions screening automation OFAC compliance is a mandatory control that many institutions still handle with outdated batch processes running once or twice daily. FinCEN's AML compliance guidance specifies that sanctions screening should operate near-real-time for both new accounts and transactions.

Automated sanctions screening works by maintaining a continuously synchronized local copy of OFAC SDN, EU Consolidated, UN Security Council, and HMT (UK) lists, then running fuzzy-match algorithms against applicant and beneficiary names. The fuzzy match is where tools diverge: phonetic matching algorithms handle transliterated names from Arabic or Cyrillic scripts that straight string matching misses entirely.

For trade finance payments, sanctions screening also covers vessel names, port codes, and corporate ownership chains. Our sanctions screening automation strategy for CISOs covers the full control architecture in detail.

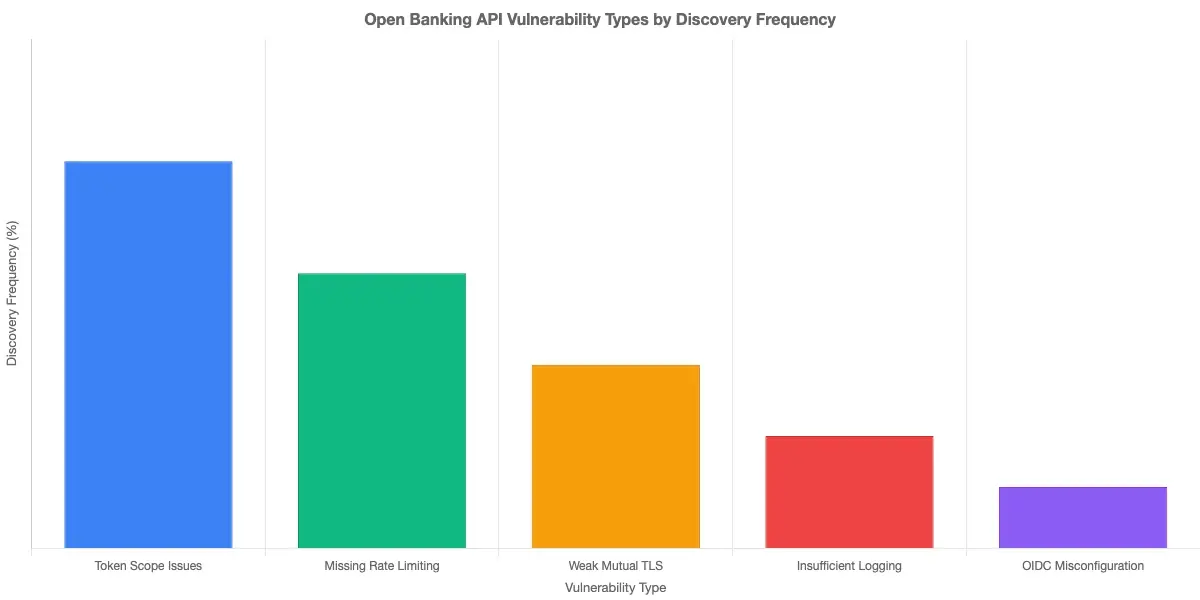

API Security for Open Banking: PSD2 Risks Banks Cannot Ignore

API security for PSD2 open banking is a growing attack surface that most banks underestimated when first deploying open banking endpoints. PSD2 and equivalent regulations require banks to expose customer account data and payment initiation APIs to licensed third parties. That is legally required. The security controls around those APIs, however, are frequently insufficient.

Common API Vulnerabilities in Open Banking Deployments

The three vulnerabilities appearing most frequently in open banking security assessments:

- Inadequate token scoping: OAuth 2.0 tokens not properly scoped allow a third party to access more data than authorized, creating data exposure risk that triggers GDPR and PSD2 liability simultaneously

- Missing rate limiting and burst protection: Malicious third-party payment initiators probing APIs during off-hours to enumerate accounts or extract transaction data

- Insufficient mutual TLS enforcement: One-way TLS does not verify the TPP's certificate, enabling impersonation of legitimate third parties

Our API security strategies for CISOs in banking covers the specific technical controls in detail. The NIST Cybersecurity Framework provides the risk management structure most regulators expect to see documented for open banking API security programs.

Trade Finance Invoice Fraud Detection with AI

Trade finance invoice fraud detection AI addresses a high-value problem that most existing compliance tools handle poorly. Invoice fraud in trade finance involves presenting the same invoice to multiple lenders, inflating valuations, or fabricating shipment documents entirely. Traditional controls rely on manual document review, which is slow and inconsistent.

AI document fraud detection for trade finance uses computer vision and NLP to detect metadata inconsistencies in PDFs, cross-reference invoice line items against commodity price databases to flag unrealistic valuations, and match bill of lading data against vessel tracking APIs to confirm the shipment actually exists. These checks run in seconds against what previously required a trade analyst spending 45 minutes per document. We cover the broader supply chain fraud picture in our AI trade document verification guide for CISOs.

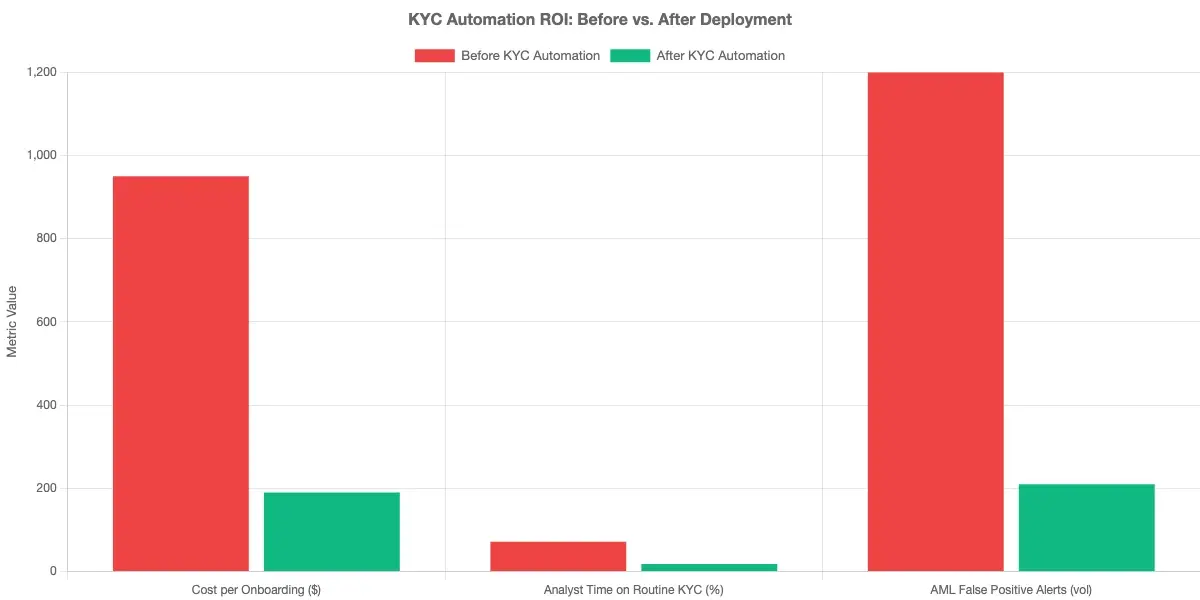

RegTech and KYC Automation ROI: What Community Banks Actually See

RegTech ROI for community banks is the question that large-bank case studies never answer. Published benchmarks come from tier-1 institutions with compliance teams of 200 people. A community bank with 8 compliance staff needs different numbers to make the business case internally.

Real Benchmark Data for Mid-Tier Institutions

Based on RegTech platform evaluation data from 2025 to 2026, community banks under $10B in assets that deploy KYC automation software typically see:

- Onboarding cost per customer: Drops from $35 to $50 (manual) to $8 to $12 (automated), a 70 to 75% reduction

- Compliance staff time on routine KYC: From 60 to 70% of working hours down to under 20%, freeing capacity for higher-risk case reviews

- Regulatory exam preparation time: Reduces 40 to 50% because audit trails are generated automatically

- AML false positive alert volume: Drops 40 to 60% within 6 months of deploying ML-based monitoring

Payback periods for a $500K to $1M RegTech platform investment typically run 14 to 22 months for community banks. The biggest driver is not headcount savings. It is avoiding regulatory fines, which at the community bank level can be existential. KYC automation compliance 2026 benchmarks consistently show that the avoided-fine calculation alone justifies the investment for most mid-tier institutions.

KYC AML Compliance Automation: Common Implementation Pitfalls

The implementation problems that most commonly delay ROI:

- Data quality issues discovered mid-project: Historical customer data in core banking systems often has inconsistent formats, missing fields, and duplicate records. Budget for a data remediation phase before go-live, or the automated system will inherit every manual process problem.

- Integration complexity with legacy core banking: Most core banking platforms were not designed for real-time API calls from a KYC layer. Plan for middleware or an event-driven integration pattern.

- Change management gaps for compliance staff: Analysts who have done manual reviews for years need structured retraining on exception-handling workflows, not just system training.

Regulatory compliance automation delivers the promised returns when those three issues are addressed proactively. Skip them and you will be 9 months into a deployment with a system your compliance team does not trust.

- KYC automation uses AI, machine learning, and API-driven data pipelines to replace or augment the manual steps in customer identity verification.

- KYC automation for digital banking onboarding typically reduces the end-to-end process from 5 to 7 days to under 4 hours.

- The false positive problem in AML transaction monitoring is genuinely costly.

- Explainable AI for financial regulators has moved from optional to expected in 2026.

- Biometric KYC for cross-border payments addresses a specific friction point: international payment rails require identity confirmation at both the sending and receiving ends, but document standards vary dramatically by jurisdiction.

Onboard Customers in Seconds

Conclusion

KYC automation is no longer a future-state initiative for banks. In 2026, it is the baseline for institutions that want to compete on customer experience while satisfying regulators who expect documented, auditable, and explainable AI-driven decisions. The banks seeing 80% reductions in onboarding time are not using exotic technology. They are combining solid document verification, machine learning-based AML transaction monitoring, and fraud detection AI frameworks that hold up under examiner scrutiny.

The ROI is real, even for community banks. The compliance risk is manageable when the architecture includes proper audit trails, calibrated risk scoring, and the explainability layer regulators now require. Start with the highest-volume, lowest-risk applicant segment, prove the model, then expand. That is the path to automated KYC onboarding without compliance risk, and it is the approach most successful implementations have followed.

Share this article