.webp)

Introduction

Fintech BSA AML compliance on a small team is genuinely achievable, and the best-run challenger banks and payment apps prove it every quarter. The assumption that you need a large compliance department to satisfy Bank Secrecy Act requirements mostly comes from watching legacy banks work. Their processes were built in the 1990s, staffed for paper workflows, and never redesigned when digital transactions arrived. Fintechs don't carry that legacy weight. What they do have is regulatory pressure: FinCEN expects the same program quality regardless of headcount. This post walks through how compliance teams of five to ten people are meeting that standard today, which tools are doing the heavy lifting, and where the real time savings come from in 2026.

- What BSA/AML Compliance Actually Requires From Fintechs

- Why the Traditional Bank Compliance Model Doesn't Translate

- How Fintech BSA/AML Small Teams Win With Automation

- KYC Automation: The Foundation of a Lean Compliance Stack

- SAR Filing and CTR Filing: Recovering Lost Hours

Onboard Customers in Seconds

What BSA/AML Compliance Actually Requires From Fintechs

AML compliance is the set of policies, controls, and procedures a financial institution uses to detect and report money laundering. Under the Bank Secrecy Act, every covered institution must maintain a written AML program built on four core elements: internal controls, independent testing, a designated compliance officer, and ongoing staff training.

That's the baseline. In practice, regulators also expect:

- Customer identification and verification (CIP/KYC)

- Ongoing customer due diligence (CDD) and enhanced due diligence (EDD) for higher-risk accounts

- Transaction monitoring for suspicious patterns

- Suspicious Activity Report (SAR) filing when defined thresholds are met

- Currency Transaction Report (CTR) filing for cash transactions above $10,000

- Sanctions screening against OFAC and other watchlists

- A documented risk assessment reviewed and updated at least annually

None of that requires twenty people. What it requires is consistency and documentation. A five-person team with the right processes and software can produce cleaner exam results than a thirty-person department running on spreadsheets and manual queues.

The BSA/AML compliance checklist for community banks and fintechs looks nearly identical at the element level. The difference is in execution capacity. Fintechs process higher transaction volumes with leaner teams, which means automation isn't optional. It's the only way the math works.

Why the Traditional Bank Compliance Model Doesn't Translate

Large bank compliance programs grew around manual review queues. An analyst would pull a flagged transaction, read account history, write a narrative, and decide whether to file a SAR. At volume, that takes people. Many regional and community banks still run this way.

The model has three problems for fintechs:

- Transaction volumes don't scale linearly with staff. A payment fintech processing 50,000 transactions per day can't hire proportionally. The math breaks fast.

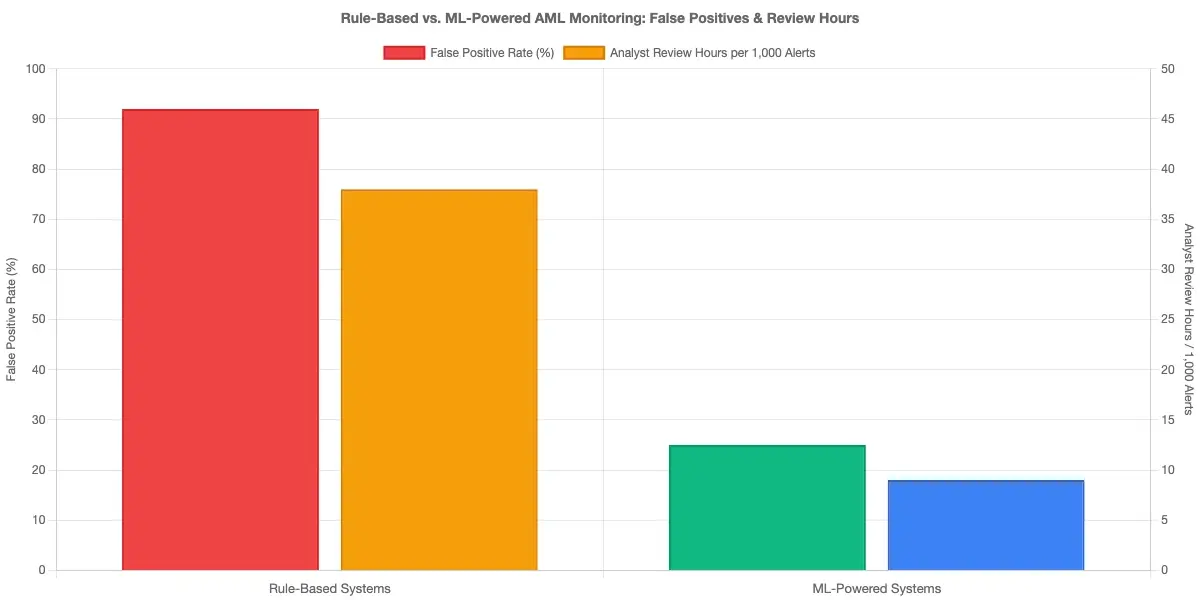

- Alert quality from legacy rule-based systems is poor. False positive rates of 90-95% are common in traditional AML monitoring setups, meaning most analyst time goes to clearing noise rather than finding actual risk.

- The documentation burden is manual. Filling out SAR forms, tracking case histories, and maintaining audit trails by hand takes hours that small teams simply don't have.

Fintechs that try to replicate the bank model at smaller scale end up behind and exhausted. The ones succeeding have rethought the workflow from scratch, starting with the question: what actually needs a human decision, and what doesn't?

The answer changes everything. A process that requires human judgment at every step is a headcount problem. A process that requires human judgment only at ambiguous decision points is a technology problem. Technology problems are much cheaper to solve.

How Fintech BSA/AML Small Teams Win With Automation

The shift that makes a small team effective is moving from reactive review to automated triage. Rather than every alert going to a human first, automation handles classification, prioritization, and documentation. Humans review only what the system flags as genuinely ambiguous or high-risk.

Three areas where this is working in 2026:

Transaction monitoring with machine learning. Modern AML compliance software trains on actual transaction patterns rather than fixed rules. False positive rates drop from 90%+ to around 20-30% in production deployments. That changes the analyst workload entirely. Instead of reviewing 50 alerts to find one real case, an analyst reviews 10 to find three or four.

False positive rates drop from 90%+ to around 20-30% in production deployments.

Automated case management. When a transaction is flagged, the system automatically pulls account history, related transactions, prior SARs, and public record data into a single case file. The analyst arrives at a pre-built narrative rather than a blank screen. SAR filing time drops from two to three hours per case to 30-45 minutes.

Straight-through processing for routine reports. CTR filing for cash transactions above $10,000 doesn't require analyst judgment. It requires accuracy and timeliness. Automation handles the filing, the regulatory formatting, and the submission, freeing the team for investigation work.

CTR filing for cash transactions above $10,000 doesn't require analyst judgment.

For teams that want a structured view of what AI automation actually changes in compliance workflows, Manual Compliance vs. AI Automation: Pros, Cons, and Best Practices covers the tradeoffs honestly, including where automation still falls short.

The practical result is that a fintech BSA AML small team of five or six people can monitor a customer base in the hundreds of thousands, as long as the technology stack is handling the triage work.

KYC Automation: The Foundation of a Lean Compliance Stack

KYC automation in 2026 does significantly more than identity document verification. That piece is table stakes. What modern KYC platforms add is:

- Real-time adverse media screening during onboarding and at account anniversary dates

- Automated PEP and sanctions checks against OFAC, UN, EU, and HMT watchlists simultaneously

- Behavioral risk scoring that adjusts a customer's risk tier based on actual transaction behavior over time, not just static information provided at signup

- Continuous CDD updates that trigger re-verification when risk indicators change, without requiring manual review of every account

The practical effect is that a two-person KYC team can maintain ongoing due diligence across a customer base of 200,000 accounts. Five years ago, that would have required ten or more people.

The honest limitation worth acknowledging: automated KYC misses edge cases that a trained analyst catches. A customer who provided accurate documents but structured early transactions to avoid detection may not trigger automated flags until the pattern becomes obvious. Human review of high-risk segments remains important even with automation in place.

For fintechs dealing with more complex KYC scenarios, particularly in lending contexts, AML Screening in Digital Lending covers how the process works across different product types.

KYC automation also matters for regulatory reasons beyond efficiency. The EU AI Act, which began applying to financial services in 2025, requires explainability for automated decisions affecting customers. Modern KYC platforms built for kyc automation 2026 compliance generate audit trails that show exactly why a risk score was assigned, which matters both for internal review and regulator examination.

SAR Filing and CTR Filing: Recovering Lost Hours

SAR filing is where compliance teams lose the most time, and where good software makes the biggest measurable difference. The average SAR takes two to four hours to complete manually. A team filing 15-20 SARs per month spends 30-80 hours per month on documentation alone.

The FFIEC BSA/AML Examination Manual sets the standard for what a SAR must include: the subject's identifying information, the nature of the suspicious activity, the amount involved, and a supporting narrative. None of that requires a human to locate and assemble from scratch. Good software does it automatically.

What SAR filing efficiency looks like in practice:

- Transaction monitoring system identifies suspicious pattern

- System auto-populates case with subject data, transaction history, and prior activity

- System drafts narrative based on activity type (structuring, layering, rapid movement, etc.)

- Analyst reviews draft, adjusts narrative where needed, and approves

- System submits directly to FinCEN BSA E-Filing and logs the submission

The analyst's role becomes editorial rather than clerical. A two-hour task becomes 30 minutes, consistently.

CTR filing is simpler. For cash transactions above $10,000, the reporting obligation is mechanical. Well-configured automation identifies qualifying transactions, completes the form, and submits it with near-zero manual intervention.

For cash transactions above $10,000, the reporting obligation is mechanical.

For teams managing sanctions obligations alongside transaction monitoring, Sanctions Screening Automation for CISOs covers how automated screening handles OFAC and other watchlist requirements at scale.

Building an AML Risk Assessment Without a Dedicated Analyst

The AML risk assessment shows examiners you understand your own risk profile. Regulators want to see that you've identified high-risk products, customers, and geographies, assessed your control gaps, and documented a remediation plan.

Most small teams treat the risk assessment as an annual document-production exercise. That's the wrong approach. It should be a living document, updated when products change, customer mix shifts, or new typology guidance arrives from FinCEN.

What works for small teams:

- Use a structured template. The FFIEC provides guidance on what a risk assessment should cover. Build your template from that structure and populate it with your specific data each year.

- Pull data from your monitoring system. Good AML compliance software exports transaction patterns, alert volumes, case outcomes, and typology breakdowns. That data populates your risk assessment automatically rather than requiring manual collection.

- Set a quarterly review cadence. Rather than one annual scramble, spend two hours per quarter updating material factors. Annual updates become a compilation, not a reconstruction.

- Document your control gaps openly. Examiners respond better to a team that says "we identified this gap and here's our remediation timeline" than to one that claims no gaps exist. Honest risk assessments build credibility.

If you're deploying compliance automation for the first time, Roll Out Regulatory Compliance Agents in 90 Days provides a concrete implementation framework that works well as a foundation for structuring your compliance program around automated tools.

What Good AML Compliance Software Actually Does

Not all AML compliance software is built for small teams. Some enterprise platforms are retrofitted with a "small business" tier that still requires a dedicated implementation team and six months to configure. That's not useful for a four-person compliance department.

What actually works for lean fintech compliance teams has these characteristics:

| Feature | Why It Matters |

|---|---|

| API-first integration | Connects to your core banking or payments platform without a six-month build |

| Configurable risk rules | Lets your compliance officer adjust thresholds without filing a support ticket |

| Built-in SAR/CTR filing | Handles FinCEN submission directly, without export and re-import |

| Audit-ready reporting | Produces documentation in the format examiners expect |

| Ongoing model updates | Updates typology detection as FinCEN issues new guidance |

Anti-money laundering technology in 2026 has moved toward modular design. Rather than buying a monolithic platform and using 30% of its features, fintechs now frequently assemble a stack: a KYC vendor for onboarding, a transaction monitoring vendor for ongoing surveillance, and a case management vendor for SAR documentation. That modularity lets small teams pay for what they actually use.

The tradeoff is integration complexity. Three vendors means three APIs to maintain and three data flows to synchronize. For teams not confident managing that, a single-vendor platform with solid coverage is often the safer choice, even at higher per-seat cost.

Teams dealing with the alert triage problem specifically should look at How Agentic AI Fraud Agents Cut False Positives by 80%, which covers how machine learning reduces noise in financial crime detection.

- AML compliance is the set of policies, controls, and procedures a financial institution uses to detect and report money laundering.

- Large bank compliance programs grew around manual review queues.

- The shift that makes a small team effective is moving from reactive review to automated triage.

- KYC automation in 2026 does significantly more than identity document verification.

- SAR filing is where compliance teams lose the most time, and where good software makes the biggest measurable difference.

Conclusion: Fintech BSA/AML Compliance Is a Systems Problem, Not a Headcount Problem

Fintech BSA AML compliance on a small team works when treated as a systems design challenge rather than a staffing problem. The BSA doesn't require any specific number of employees. It requires a functioning program with documented controls, consistent execution, and clear evidence of ongoing monitoring.

What that means practically: invest in the right AML compliance software before adding headcount. A compliance team of five with automated KYC workflows, machine learning-based transaction monitoring, and system-generated SAR documentation can outperform a team of fifteen running on manual processes and spreadsheets.

The regulatory environment in 2026 rewards quality and consistency. Examiners look for evidence that your program caught and responded to real risk, not that you had a large department. If you're building or scaling a compliance function, the question isn't "how many people do we need?" It's "what should humans actually decide, and what should the system handle?"

If your answer to that second question is still "everything," it's time to revisit your compliance stack.

Onboard Customers in Seconds

Share this article