.webp)

Introduction

The BSA AML compliance checklist for community banks has never been more scrutinized than it is in 2026. FinCEN enforcement actions hit a five-year high recently, with community banks accounting for nearly 40% of cited deficiencies despite holding a fraction of total U.S. banking assets. The pressure is real: underfunded compliance teams, aging core systems, and rapidly evolving typologies around digital payments and crypto transactions are colliding at exactly the moment examiners are demanding more. This post breaks down what a current, practical BSA/AML program actually looks like for a community bank, covering KYC requirements, SAR filing, CTR filing rules, software selection, and where most programs fall short. If you have a compliance exam coming up or are rebuilding your AML program from scratch, use this as your working guide.

FinCEN enforcement actions hit a five-year high recently, with community banks accounting for nearly 40% of cited deficiencies despite holding a fraction of total U.S.

- What BSA/AML Compliance Requires in 2026

- Your BSA AML Compliance Checklist: The Five Pillars

- KYC and CDD: Core Community Bank Compliance Requirements

- SAR Filing and CTR Filing: Getting the Details Right

- Choosing AML Compliance Software for Community Banks

Onboard Customers in Seconds

What BSA/AML Compliance Requires in 2026

The Bank Secrecy Act, first enacted in 1970, has accumulated decades of amendments, FinCEN guidance, and FFIEC examination expectations. In 2026, the core requirements remain anchored in five program pillars established by FinCEN, but the implementation bar has moved considerably higher.

The FFIEC BSA/AML Examination Manual, the de facto standard for examination expectations, was updated in 2021 and continues to shape how examiners evaluate programs. Examiners now expect documented risk assessments, transaction monitoring calibrated to your specific customer base, and evidence that your SAR and CTR decisions are defensible.

For community banks specifically, the challenge is not awareness of these requirements. It is resourcing. A bank with $800 million in assets might have two full-time compliance staff responsible for the same scope of activity that a $10 billion bank handles with a team of 30. That gap shows up in examinations.

Your BSA AML Compliance Checklist: The Five Pillars

Here is the working BSA AML compliance checklist organized by the five FinCEN program pillars. Each item represents something an examiner will look for.

Pillar 1: Internal Controls

- Written BSA/AML policy approved by the board within the last 12 months

- Risk-based transaction monitoring thresholds documented and reviewed annually

- Alert disposition process defined with expected completion timelines

- Currency Transaction Report (CTR) and Suspicious Activity Report (SAR) procedures documented

- OFAC screening processes integrated into onboarding and ongoing monitoring

Pillar 2: Independent Testing

- Annual independent audit of BSA/AML program (internal audit or third-party)

- Audit scope covers transaction monitoring, SAR/CTR filing, KYC, and training

- Prior audit findings tracked with remediation deadlines and current status

Pillar 3: Designated BSA Officer

- BSA Officer has sufficient seniority, authority, and resources

- BSA Officer reports directly to the board at least annually

- Backup coverage defined for BSA Officer absence

Pillar 4: Training

- Annual AML compliance training for all customer-facing staff

- Role-specific training for high-risk areas (wire transfers, cash-intensive business accounts)

- Training records retained for at least five years

Pillar 5: Customer Due Diligence (CDD)

- CDD procedures apply to all new customers and existing customers upon trigger events

- Beneficial ownership collected for all legal entity customers at the 25% threshold

- Enhanced Due Diligence (EDD) procedures in place for high-risk customers

This checklist is the minimum. Examiners increasingly expect banks to demonstrate that these controls work in practice, not just that the documents exist.

KYC and CDD: Core Community Bank Compliance Requirements

KYC automation is changing how community banks handle onboarding. Historically, collecting ID documents and running basic screening was a manual, paper-based process. In 2026, regulators expect a more dynamic approach.

The FinCEN Customer Due Diligence Rule requires banks to collect and verify four core elements: legal name and address, date of birth or formation date, identification number (SSN, EIN, or passport), and beneficial owners for legal entities at the 25% ownership threshold.

The FinCEN Customer Due Diligence Rule requires banks to collect and verify four core elements: legal name and address, date of birth or formation date, identification number (SSN, EIN, or passport), and beneficial owners for legal entities at the 25% ownership threshold.

Beyond collection, KYC automation in 2026 means continuous monitoring. Static onboarding profiles are not sufficient when a customer's behavior changes, they appear on a new sanctions list, or adverse media surfaces. Banks that rely solely on onboarding checks and annual reviews are leaving themselves exposed.

Enhanced due diligence applies to higher-risk customers: politically exposed persons (PEPs), foreign nationals, high-cash businesses, and accounts with complex beneficial ownership structures. EDD means understanding the source of funds, the expected transaction patterns, and the business purpose with specificity. A description of "small business" is not sufficient documentation.

For community banks managing AML compliance with small teams, analysis of AML screening workflows in digital lending shows that automated risk scoring at onboarding can cut manual review time by roughly 60%, which matters considerably when your compliance team is two people.

SAR Filing and CTR Filing: Getting the Details Right

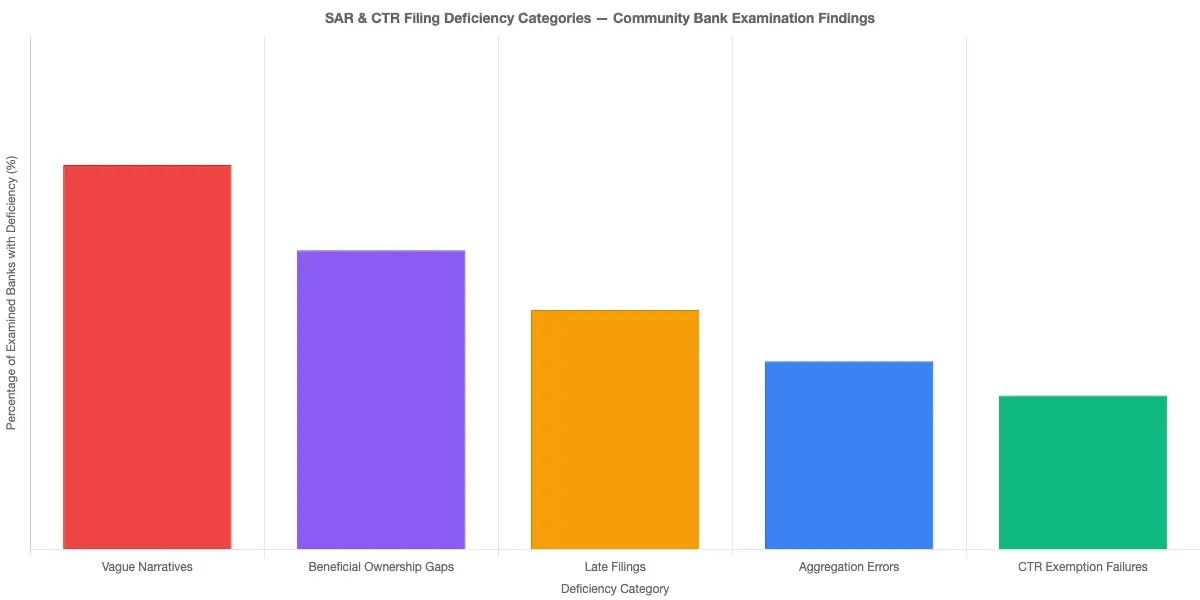

SAR filing is one of the most error-prone areas in community bank AML programs. Examiners cite two common failure modes: filing SARs that are too vague to be useful to law enforcement, and failing to file SARs on activity that clearly warrants reporting.

SAR Filing Requirements and Narrative Standards

SAR filing requirements in 2026:

- File within 30 days of initial detection of suspicious activity (60 days if no suspect is identified at detection)

- The narrative must explain the who, what, when, where, why, and how of the suspicious activity in plain language

- Do not tip off the customer that a SAR has been filed

- Retain SAR records for five years from the filing date

- Review continuing suspicious activity every 90 days to determine whether to file a continuing SAR

The quality of SAR narratives gets direct examiner attention. A SAR that says "customer made unusual cash withdrawals" will not survive scrutiny. A SAR that explains specific amounts, dates, patterns of structuring, and why the activity deviates from established customer behavior is defensible and actionable for law enforcement.

CTR Filing Rules and Common Mistakes

Currency Transaction Reports apply to cash transactions exceeding $10,000 in a single business day, whether a single transaction or multiple transactions that are aggregated. The most common CTR mistakes:

Currency Transaction Reports apply to cash transactions exceeding $10,000 in a single business day, whether a single transaction or multiple transactions that are aggregated.

- Failing to aggregate multiple transactions by the same customer on the same day

- Incorrectly exempting customers who no longer qualify for CTR exemptions

- Missing CTR obligations on transactions conducted on behalf of another person

CTR exemptions are available for certain customers (Phase I and Phase II exemptions), but they require annual review and documentation. Banks that granted exemptions years ago and never revisited them face penalties when those customers no longer qualify.

Improving SAR filing efficiency also depends on having clean data flows. Sanctions screening automation intersects directly with SAR workflows when transactions trigger hits against OFAC lists or other watchlists, and automated screening dramatically reduces the time between detection and filing.

Choosing AML Compliance Software for Community Banks

The right AML compliance software does not look the same for every institution. A $500 million community bank has different needs than a $5 billion regional bank. Here is what actually matters when evaluating platforms.

Transaction monitoring calibration. Most off-the-shelf transaction monitoring systems ship with generic rules calibrated for large banks. A community bank with heavy agricultural lending has fundamentally different transaction patterns than an urban bank focused on consumer deposits. Look for systems that allow you to adjust thresholds per customer segment and that include calibration documentation you can show examiners.

Workflow integration. AML software that sits outside your core banking system creates manual reconciliation work. The best integrations pull transaction data automatically, reduce duplicate data entry, and route alerts to the right analyst with supporting customer context already attached.

Audit trail. Every alert disposition, SAR decision, and CTR filing needs a complete, timestamped audit trail. Examiners will ask to see not just what decisions were made, but who made them and why.

Cost reality. Community banks are not going to budget $500,000 for enterprise-grade AML platforms. Credible platforms in the $40,000 to $120,000 annual range provide adequate transaction monitoring, SAR workflow management, and CTR tracking without the overhead of implementations designed for much larger institutions.

The honest tradeoff: cheaper platforms typically require more manual configuration and ongoing tuning. You will need someone on staff who understands the system well enough to adjust rules as your customer base and risk profile evolve.

Anti-Money Laundering Technology Trends for 2026

Anti-money laundering technology in 2026 is moving in three directions that community banks should understand, even if they are not ready to deploy them immediately.

AI and Network Analysis

AI-based transaction monitoring. Rule-based systems generate false positive rates of 90 to 95% of all alerts, according to industry benchmarks. AI and machine learning models learn from confirmed SAR activity and calibrate alert thresholds dynamically. For small compliance teams, reducing false positives by even 40 to 50% represents meaningful capacity savings. How agentic AI fraud agents cut false positives by 80% explores this approach in practical detail.

Network analysis. Individual transaction monitoring misses money laundering schemes that operate across multiple accounts and entities. Graph-based analytics map relationships between accounts, beneficial owners, and counterparties, surfacing typologies that rule-based systems will never catch. This is particularly relevant for community banks serving closely networked local business communities where circular fund flows can indicate layering activity.

RegTech for Reporting and EU AI Act

Regulatory technology for reporting. Automated SAR narrative generation, CTR filing verification, and regulatory report submission are moving from large-bank capabilities to mid-market tools. Some platforms now draft SAR narratives from structured alert data, which the compliance officer reviews and edits. The time savings are real and measurable.

EU AI Act implications. For community banks with cross-border customer relationships or fintech partnerships, the EU AI Act classifies AML and credit risk AI as high-risk systems subject to transparency, documentation, and human oversight requirements. If your AML software vendor uses AI models and you operate internationally or partner with EU-regulated entities, this governance framework applies to your technology stack.

Where Community Bank AML Programs Fall Short

Based on examination findings and industry analysis, these are the areas where community bank AML programs most commonly fail.

Outdated risk assessments. The BSA/AML risk assessment should be a living document, updated when the bank adds new products, enters new markets, or onboards high-risk customer segments. Banks that last updated their risk assessment three years ago and have since launched mobile banking and ACH origination are operating with a significant blind spot.

Transaction monitoring that was never tuned. Banks implement transaction monitoring software, set the initial thresholds during implementation, and never revisit them. When examiner-led look-back reviews find suspicious activity that the system did not alert on, the bank has a problem with no easy defense.

Weak SAR narratives. This comes up in almost every examination. The narrative is the bank's opportunity to explain suspicious activity in a way that is useful to law enforcement. Vague narratives waste everyone's time and signal to examiners that the compliance program is understaffed or under-managed.

Beneficial ownership gaps. The Corporate Transparency Act, fully effective since January 2024, requires most U.S. companies to file beneficial ownership information with FinCEN. Banks must collect and verify this data at account opening and update it when changes occur. Many community banks are still collecting beneficial ownership inconsistently.

Training gaps for specific roles. Annual AML training for all staff is standard. Training calibrated to the specific risks of wire transfer operators, commercial relationship managers, or tellers handling high-cash businesses is far less common and considerably more important when examiners pull transaction records.

Manual compliance versus AI automation explores how institutions of all sizes are rethinking these workflows. The honest assessment is that manual processes alone are becoming insufficient for the volume and complexity of current AML typologies.

KYC Automation and the Road Ahead

KYC automation in 2026 is not a luxury for community banks. It is becoming a practical necessity. The volume of ongoing monitoring obligations, triggered reviews, and EDD updates that a modern BSA/AML program requires is not manageable at scale with purely manual processes.

The good news: KYC automation tools built for smaller institutions have improved considerably. Identity verification APIs that plug into onboarding workflows, automated beneficial ownership collection with built-in verification, and continuous adverse media monitoring are available at price points that community banks can justify.

Governance matters as much as technology. Automated tools still need human review for edge cases, and examiners want to see that your compliance team understands what the system is doing and can exercise judgment when the system flags something unusual. A detailed look at KYC/AML verification strategy and oversight controls covers the framework for building accountability into automated AML workflows.

The risk of under-investing in KYC automation is concrete: slower onboarding, higher compliance costs per account, and greater exposure to examination findings in an environment where regulatory expectations continue to climb.

- The Bank Secrecy Act, first enacted in 1970, has accumulated decades of amendments, FinCEN guidance, and FFIEC examination expectations.

- Here is the working BSA AML compliance checklist organized by the five FinCEN program pillars.

- KYC automation is changing how community banks handle onboarding.

- SAR filing is one of the most error-prone areas in community bank AML programs.

- The right AML compliance software does not look the same for every institution.

Onboard Customers in Seconds

Conclusion

The BSA AML compliance checklist for community banks in 2026 covers ground that has not changed much in principle but has shifted considerably in practice. The five program pillars are not new. What is new is the expectation that your controls work at the level of sophistication that today's typologies, examiner expectations, and available technology demand.

Start with your risk assessment. If it is more than 18 months old, update it before your next examination. Work through the checklist above by pillar, and be honest about gaps in transaction monitoring calibration, SAR narrative quality, and beneficial ownership documentation. These are exactly where examiners spend their time.

AML compliance is not a documentation exercise. It is an operational discipline that requires ongoing investment in people, process, and technology. Community banks that treat it that way will be in a far better position than those still running programs designed for a very different regulatory environment.

Share this article