.webp)

Introduction

Anti-money laundering technology 2026 is at a genuine inflection point. Three forces are colliding at once: regulators are tightening scrutiny after years of headline-grabbing enforcement actions, AI capabilities have matured enough for real-time behavioral analysis to be production-ready, and smaller institutions face the same compliance obligations as major banks with a fraction of the headcount. Whether you manage AML compliance at a community bank, a fintech startup, or an insurance carrier, the tools available to your team look fundamentally different today than they did 24 months ago.

This guide covers the seven biggest shifts in AML compliance technology this year, from AI-driven transaction monitoring and KYC automation to SAR filing automation and the EU AI Act's impact on algorithmic decision-making in financial services. The goal is practical: understand what is changing, where the real compliance risk sits, and which upgrades are worth prioritizing before your next examination.

- What Is Anti-Money Laundering Technology and Why It's Changing in 2026

- KYC Automation 2026: Continuous Verification Replaces One-Time Onboarding

- SAR Filing Best Practices and the Push for Automation

- CTR Filing Rules and the Compliance Burden on Small Teams

- How the EU AI Act Is Reshaping AML Compliance Fintech

Onboard Customers in Seconds

What Is Anti-Money Laundering Technology and Why It's Changing in 2026

Anti-money laundering technology refers to the software systems, data infrastructure, and analytical tools that financial institutions use to detect, investigate, and report suspected money laundering activity. In practice, this includes transaction monitoring platforms, sanctions screening engines, KYC/CDD tools, case management systems, and SAR filing software.

What is changing is the underlying architecture. A decade ago, most AML compliance software ran on rule-based engines: if a customer sends more than $9,500 in a single transaction, flag it. These rules were explicit, auditable, and easy to explain to examiners. They were also easy to evade, expensive to tune, and generated false positive rates above 95% at many institutions.

A decade ago, most AML compliance software ran on rule-based engines: if a customer sends more than $9,500 in a single transaction, flag it.

Today's systems are moving toward machine learning models that build behavioral baselines per customer, flag deviations rather than threshold breaches, and automatically prioritize alerts by risk score. The result: fewer false alarms, faster investigations, and better detection of the structuring and layering patterns that rule-based engines miss entirely.

How AI Models Are Replacing Static Rules in Transaction Monitoring

The core difference between rule-based and AI-driven transaction monitoring comes down to context. A rule engine looks at each transaction in isolation. An AI model looks at the transaction in the context of who the customer is, what their historical behavior looks like, what their peer group does, and what the counterparty's risk profile is.

In practice, a $4,000 cash deposit might be flagged for a customer who has never made a cash deposit before, while a $12,000 deposit from a restaurant owner with consistent weekly deposits clears without an alert. That's not a loophole. That's correct detection behavior.

In practice, a $4,000 cash deposit might be flagged for a customer who has never made a cash deposit before, while a $12,000 deposit from a restaurant owner with consistent weekly deposits clears without an alert.

For compliance teams trying to reduce false positives without increasing detection risk, the shift from rule-based systems to AI-driven AML solutions is the highest-impact change available right now. Some institutions report cutting alert volumes by 40-60% after deploying behavioral analytics, which translates directly into fewer investigators needed per thousand monitored accounts.

Some institutions report cutting alert volumes by 40-60% after deploying behavioral analytics, which translates directly into fewer investigators needed per thousand monitored accounts.

The Honest Trade-Off in AI-Powered AML

AI models are harder to explain to examiners than rule-based systems. When a regulator asks why a specific transaction was flagged, 'the model assigned a high risk score based on 47 behavioral features' is technically accurate but unsatisfying. Explainability is an active engineering challenge in AML compliance software right now, and the solutions are still maturing.

The practical answer most institutions are adopting is a hybrid approach: AI handles initial scoring and prioritization, while rule-based logic handles the final disposition criteria that need to be documented clearly in examination files.

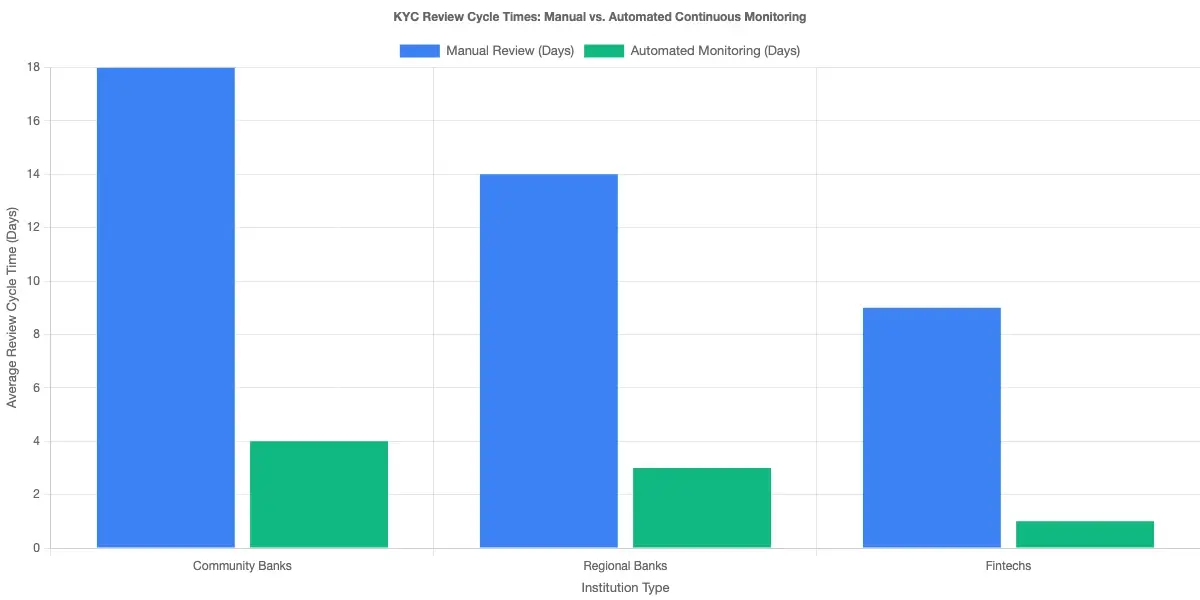

KYC Automation 2026: Continuous Verification Replaces One-Time Onboarding

KYC automation 2026 looks very different from the digital KYC that banks deployed in 2021. The earlier wave was mostly about digitizing paper-based processes: replacing physical ID verification with document scanning, moving CDD questionnaires online, and connecting to sanctions databases via API. That reduced onboarding time from days to hours.

The current wave is about continuous monitoring. Static KYC snapshots go stale within months for high-risk customers. A customer who was low-risk at onboarding may have appeared in adverse media, changed their business structure, or started transacting with newly sanctioned counterparties. Manual periodic reviews catch this eventually, but often too late to prevent examination findings.

KYC CDD Requirements Banks Must Meet in 2026

The minimum KYC CDD requirements for US banks under FinCEN's Customer Due Diligence Rule remain: identify and verify customers, understand the nature and purpose of customer relationships, monitor for suspicious activity, and identify beneficial owners for legal entity customers.

What has changed is examiner expectations around implementation. Examiners now ask whether institutions have documented risk tiers, whether periodic review schedules are calibrated to risk rather than a flat 12-month calendar, and whether adverse media screening is automated or still handled manually by analysts.

For institutions that haven't revisited their KYC program in the past two years, a practical starting point is an internal gap analysis against the FinCEN CDD rule. The AML risk checks and KYC verification strategy framework covers tiered risk assessment methodology that applies across banking, insurance, and fintech contexts.

Enhanced Due Diligence Guide for High-Risk Customer Segments

Enhanced due diligence (EDD) applies to higher-risk relationships: politically exposed persons (PEPs), customers in high-risk geographies, correspondent banking relationships, and private banking clients with significant wealth of unclear origin.

The EDD process that most institutions still run manually, pulling adverse media, verifying source of wealth, reviewing transaction patterns, and creating narrative summaries, takes 3-8 hours per case depending on complexity. Automated EDD platforms reduce this to 30-45 minutes by pre-fetching data from adverse media APIs, PEP registries, and corporate registry sources and presenting them in a pre-structured case file. This enhanced due diligence guide approach works well for institutions with 50 or more EDD reviews per month, where the time savings compound meaningfully across the year.

The honest limitation: automated data aggregation is only as good as the underlying data sources, and coverage gaps in certain jurisdictions remain a real problem for global institutions.

SAR Filing Best Practices and the Push for Automation

SAR filing efficiency is one of the most underrated compliance problems in financial services. The average time to file a Suspicious Activity Report, from initial alert through investigation, narrative writing, and submission, runs 30-45 days at institutions relying on manual processes. That timeline creates two problems: regulatory risk if the filing runs late, and investigation backlogs that leave genuinely suspicious activity unreviewed for weeks.

As a practical suspicious activity report guide for compliance teams: the process involves identifying suspicious activity, investigating the facts, drafting the narrative, completing FinCEN Form SAR, and submitting via the BSA E-Filing System. Each step has manual touchpoints where queues build under volume pressure. SAR filing best practices address each of these touchpoints explicitly.

SAR Filing Requirements 2026 and What Examiners Are Checking

The core SAR filing requirements haven't changed. Financial institutions must file within 30 days of detecting suspicious activity, or 60 days if no suspect can be identified. But examiners are increasingly scrutinizing narrative quality, not just whether the form was filed on time.

A SAR narrative that says 'customer conducted suspicious transactions inconsistent with known business' is technically compliant but practically useless for law enforcement. FinCEN guidance pushes for narratives that include specific dates, amounts, counterparties, the pattern of activity, and the reason it deviates from expected customer behavior.

AML compliance software that includes narrative generation tools can materially improve SAR quality. Systems that auto-populate case details from alert data and offer analyst-reviewable draft narratives are reducing narrative writing time by 50-70% at early adopters, which is the kind of efficiency gain that also improves examiner impressions of program maturity.

How SAR Filing Efficiency Affects Examination Risk

The relationship between SAR filing efficiency and examination risk is direct: slow processes create backlogs, backlogs create late filings, and late filings become examination findings. Beyond timeliness, regulators look at SAR filing rates relative to transaction volume as a calibration check. An institution filing significantly fewer SARs than peer banks raises questions about whether its monitoring program is actually detecting anything.

Improving SAR filing efficiency isn't just about speed. It's about having clean audit trails documenting the investigation steps taken before each filing decision. For teams at digital lending platforms, AML screening in digital lending offers a framework for connecting transaction monitoring alerts to SAR disposition workflows without introducing manual handoffs.

CTR Filing Rules and the Compliance Burden on Small Teams

CTR filing rules are straightforward in theory: file a Currency Transaction Report for any cash transaction exceeding $10,000 in a single business day, with aggregation across multiple transactions from the same customer on the same day. In practice, managing CTR obligations across multiple branches, handling exemptions for businesses with consistent cash activity, and maintaining aggregation logic creates significant administrative overhead.

For institutions processing high volumes of cash, CTR filing is where rule-based automation still makes the most sense. The threshold is explicit, the aggregation logic is well-defined, and the filing format is standardized. Most core banking systems and AML compliance software platforms handle CTR generation automatically once data feeds are configured correctly.

Fintech BSA AML Small Team Challenges

The fintech BSA AML small team problem is real and frequently underestimated. Many fintechs launch with one or two compliance staff, a basic transaction monitoring tool, and a manual SAR filing process. That setup works at low transaction volumes. It breaks badly once customer counts reach the thousands and transaction complexity increases.

The specific pain points for small fintech compliance teams:

- Alert volume that exceeds investigator capacity during transaction spikes

- No dedicated case management system, with investigations tracked in spreadsheets

- Manual SAR filing without narrative assistance

- Periodic KYC reviews falling behind schedule as the customer base grows

- Limited access to peer benchmarking data for calibrating detection thresholds

Cloud-native AML compliance software platforms priced for smaller institutions have emerged to address this gap directly. They bundle transaction monitoring, KYC automation, case management, and SAR filing in a single platform at per-account pricing rather than large upfront license fees, making them viable for teams of two or three compliance staff.

BSA AML Compliance Checklist for Community Banks

Community banks face a different version of the resource problem. They have established compliance programs, experienced examiners who know their business, and strong community relationships. But they also operate with limited IT budgets, legacy core banking systems with limited API connectivity, and examination teams applying the same substantive standards as for large banks.

A practical BSA AML compliance checklist for community banks in 2026:

- Documented risk assessment updated within the last 12 months

- Transaction monitoring system calibrated to the institution's specific product mix and customer base

- CTR filing with automated aggregation and exemption management

- SAR filing process with average time-to-file tracked and consistently below 30 days

- KYC/CDD program with documented risk tiers and periodic review schedule

- Beneficial ownership collection for all new legal entity accounts

- Staff training records current within the last 12 months

- Independent BSA audit completed within the last 12-18 months

How the EU AI Act Is Reshaping AML Compliance Fintech

The EU AI Act's provisions for high-risk AI systems applied to new deployments starting in August 2025, and AML systems explicitly fall under the high-risk category. For financial institutions operating in the EU, or for AML compliance fintech vendors selling into EU markets, this creates concrete new obligations around documentation, human oversight, and conformity assessment.

The main requirements affecting AML compliance software: human oversight provisions requiring that automated decisions be reviewable before adverse action, documentation requirements for training data and model performance metrics, conformity assessments before deployment, and minimum accuracy and robustness standards.

EU AI Act Financial Services Implications for AML Programs

The honest answer is that implementation-level guidance for AML AI systems remains in development. The European Banking Authority's guidance on AI in finance provides some structure, but specific technical standards for AML AI systems are still being finalized as of early 2026.

What compliance teams can do now: document the AI models used in transaction monitoring and KYC systems, ensure human review is embedded in the workflow before any adverse action based on automated outputs, and work with vendors to understand their conformity assessment timelines and documentation packages. For AML compliance fintech vendors, the EU AI Act is also a market opportunity. Institutions that haven't upgraded from legacy rule-based tools will have increasing difficulty demonstrating compliance with AI governance requirements. The GDPR compliance automation frameworks that became standard practice offer a useful analogy for how institutions can approach structured AI governance requirements systematically.

AML Risk Assessment Guide: What Regulators Expect in 2026

An AML risk assessment is the foundation of a defensible compliance program. It documents the institution's inherent risk based on products, services, customers, and geographies; the controls in place to mitigate that risk; and the resulting residual risk. Examiners use it to calibrate their examination scope and evaluate whether the monitoring program is appropriately tuned to the actual risk profile.

The FFIEC BSA/AML Examination Manual is the standard reference for what a risk assessment needs to contain. The core components are products and services risk, customer and client risk, geographic risk, and transaction activity risk. This AML risk assessment guide covers what examiners look for in each category and where community institutions most often fall short.

BSA AML Compliance Community Banks Must Prioritize in Their Risk Assessments

For community banks, the most common risk assessment gaps found in examinations fall into three categories.

Insufficient geographic risk analysis. Many community banks list their service area as low-risk without documenting why, relative to FinCEN geographic targeting orders and high-risk jurisdiction lists. That's a documentation gap even if the underlying assessment is correct.

Customer risk tiering that doesn't match monitoring thresholds. Banks that classify cash-intensive businesses as medium-risk but don't have monitoring scenarios specifically calibrated for that segment have a gap between their documented risk profile and their actual detection coverage. BSA AML compliance at community banks depends on this alignment being explicit and examinable.

Stale assessments. Risk assessments updated every three years may have been acceptable a decade ago. Examiners now expect annual updates, or updates triggered by material changes in products, customers, or geographies.

Anti Money Laundering Technology Evaluation Against Your Risk Profile

Technology selection needs to follow your risk assessment, not precede it. An institution with primarily digital channels and no cash products has different monitoring needs than a community bank serving cash-intensive businesses.

Before evaluating any anti money laundering technology vendor, map your top three risk categories from your risk assessment to specific monitoring scenarios. If structuring is your primary concern, evaluate whether the transaction monitoring tool has multi-day, multi-account structuring detection. If high-risk geography transactions are the main risk, evaluate sanctions screening coverage and geographic risk scoring in detail before anything else.

How to Choose Anti-Money Laundering Technology for Your Institution

Selecting AML compliance software is a three-to-five year commitment, given implementation timelines and the real cost of switching. The market includes established enterprise vendors (NICE Actimize, Oracle Financial Services AML), cloud-native challengers (Sardine, Hawk AI, ComplyAdvantage), and point solutions for specific workflows like KYC automation or SAR filing.

Anti Money Laundering Technology Evaluation Criteria

The criteria that matter most in practice, based on what compliance teams report after going live:

- Alert quality, not just volume. Ask vendors for false positive rates at peer institutions with similar risk profiles. A system generating 10,000 alerts per month with a 97% false positive rate burns analyst capacity on noise and is worse than a smaller, better-calibrated system.

- Core banking integration. Real-time monitoring requires real-time data feeds. If the vendor's integration with your core takes six months and requires custom development, that's a material implementation risk to price in.

- SAR filing integration. Systems that connect transaction monitoring alerts through case management to SAR drafting to FinCEN submission reduce manual handoffs and audit trail gaps.

- Examiner acceptance. Ask for references from institutions that have been examined using the platform. Examiners unfamiliar with a particular anti money laundering technology tool may require additional documentation to understand the methodology.

- Explainability features. For AI-driven systems, evaluate the audit trail generated for each alert. Can you reconstruct the full decision logic during an examination?

Building an AML Compliance Fintech Stack on a Budget

For fintechs and community banks with limited IT budgets, building a complete AML compliance fintech stack from best-of-breed point solutions is technically possible, but it creates integration overhead and audit trail fragmentation. A single-platform approach covering KYC automation, transaction monitoring, case management, and SAR filing typically produces cleaner outcomes than five loosely integrated tools.

Agentic AI for false positive reduction represents one of the most practical developments for resource-constrained teams, automating the initial investigation steps that currently consume the most analyst time. When first-level triage is automated, analysts focus their hours on genuine suspicious activity rather than clearing obvious noise.

- Anti-money laundering technology refers to the software systems, data infrastructure, and analytical tools that financial institutions use to detect, investigate, and report suspected money laundering activity.

- KYC automation 2026 looks very different from the digital KYC that banks deployed in 2021.

- SAR filing efficiency is one of the most underrated compliance problems in financial services.

- CTR filing rules are straightforward in theory: file a Currency Transaction Report for any cash transaction exceeding $10,000 in a single business day, with aggregation across multiple transactions from the same customer on the same day.

- The EU AI Act's provisions for high-risk AI systems applied to new deployments starting in August 2025, and AML systems explicitly fall under the high-risk category.

Onboard Customers in Seconds

Conclusion

Anti-money laundering technology 2026 gives compliance teams real tools for problems that were difficult to address even three years ago: behavioral analytics that dramatically reduce false positives, KYC automation that keeps customer risk profiles current rather than stale, AI-assisted SAR narratives that improve filing quality and speed, and AML compliance software architectures that fit smaller institutions' budgets without compromising on examiner defensibility.

The institutions extracting real value from these tools share a pattern: they start with a clear risk assessment, match technology to their specific risk profile, and invest in training analysts to work with AI outputs rather than around them. AML compliance in 2026 is not about buying the most sophisticated platform on the market. It's about buying the right tools for your actual risk profile and implementing them rigorously enough to satisfy an examiner who has seen every version of this.

If your team is planning AML compliance software upgrades this year, start with your last examination findings, map them to specific capability gaps, and require vendors to demonstrate how their systems address those gaps with references from comparable institutions. That process is more defensible than feature-sheet comparison, and it consistently produces better outcomes than buying for capability and hoping it solves the right problems.

Share this article