.webp)

.webp)

Introduction

Fraud detection gaps are costing financial institutions more than they realize, and the evidence shows up most painfully in quarterly loss reports. According to the Federal Trade Commission's Consumer Sentinel Network Data Book, U.S. consumers reported $10 billion in fraud losses in 2023 alone. Yet most organizations catch only a fraction of actual fraud before it converts to realized loss. The problem is not solely that fraud has become more sophisticated (though it has). The real issue is that the detection systems built to stop fraud were designed for a different era of attacks. This post breaks down seven specific patterns that slip through the cracks of traditional transaction monitoring software and rule-based detection engines, and explains what it actually takes to close them.

consumers reported $10 billion in fraud losses in 2023 alone.

- Why Traditional Systems Create Fraud Detection Gaps

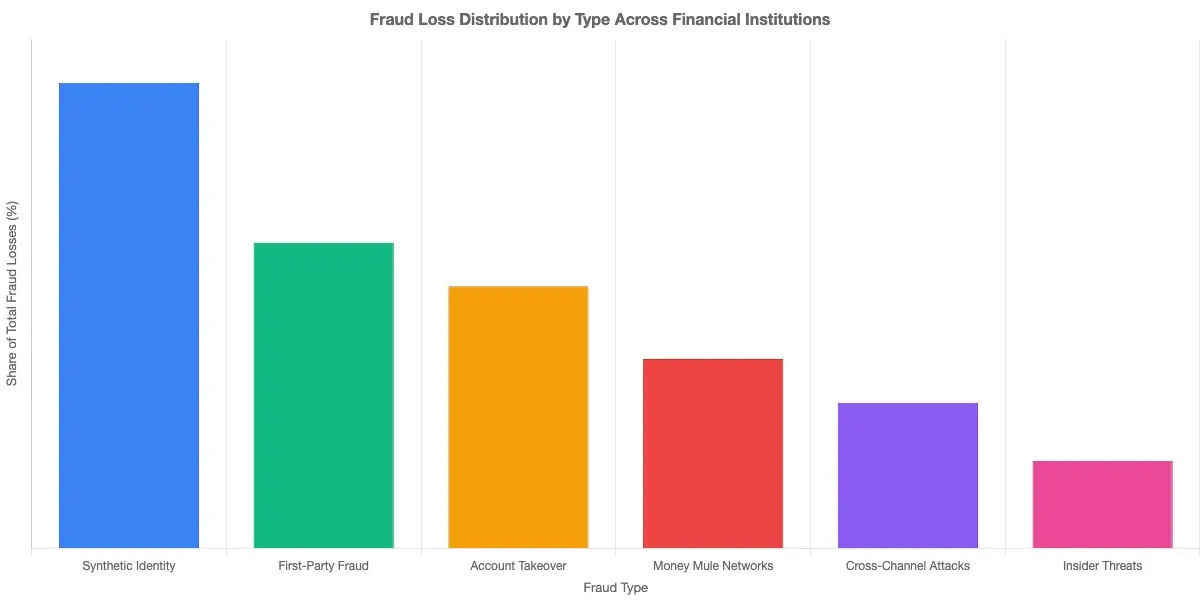

- Pattern 1: Synthetic Identity Fraud

- Pattern 2: First-Party Fraud and Friendly Fraud

- Pattern 3: Real-Time Payment Fraud

- Pattern 4: Multi-Layered Money Mule Networks

Onboard Customers in Seconds

Why Traditional Systems Create Fraud Detection Gaps

Most legacy fraud systems run on a simple premise: flag transactions that break predefined rules. Set a threshold, write a rule, trigger an alert. For the fraud patterns of 2005, this was sufficient.

The problem is that rule-based systems are static. Every rule is readable by attackers who probe and test boundaries. Once a fraudster maps your $9,999 threshold trigger, they run $9,800 transactions indefinitely. And because adding more rules generates more alerts, compliance teams quickly drown in false positives. The average analyst reviews hundreds of flagged transactions per day, most of them legitimate customer activity.

The ACFE's Report to the Nations found that organizations lose approximately 5% of annual revenue to fraud each year, and the median fraud case goes undetected for 12 months. That is not purely a detection speed problem. It is a pattern recognition failure.

The ACFE's Report to the Nations found that organizations lose approximately 5% of annual revenue to fraud each year, and the median fraud case goes undetected for 12 months.

Pattern 1: Synthetic Identity Fraud

Synthetic identity fraud is the fastest-growing financial crime in the United States. The Federal Reserve estimates it costs lenders over $6 billion annually. Unlike traditional identity theft where a fraudster steals a real person's details, synthetic identity fraud involves building a fake identity from scratch, typically using a real Social Security number from a child or someone with a thin credit file, combined with fabricated name, address, and employment data.

Here is why your current system misses this: synthetic identities look exactly like legitimate thin-file applicants. They pass KYC checks, match no known fraud database, and spend months or years building a pristine credit profile before executing a bust-out scheme. Traditional transaction monitoring software sees nothing unusual because nothing unusual has happened yet.

Real-time behavioral AI catches what static rules cannot: the slow burn of a synthetic identity accumulating credit across multiple institutions simultaneously. For a detailed breakdown of detection methods in practice, see our piece on detecting synthetic identity fraud in real-time.

Pattern 2: First-Party Fraud and Friendly Fraud

First-party fraud is the category that makes compliance officers uncomfortable because the customer is the fraudster. They take out a loan with no intent to repay. They dispute a legitimate charge as unauthorized. They open a credit card, max it out, and claim the charges were made by someone else.

Traditional systems were not built to catch this pattern because the person matches all their own identity signals. They are using their real device, their real location, their real credentials. Transaction history looks perfectly normal right up until it does not.

What makes first-party fraud particularly difficult to catch is the absence of velocity signals in the early stages. Dispute management systems flag individual transactions, not behavioral trajectories that develop over 60 to 90 days. By the time the pattern is visible, the loss is already locked in. Effective payment fraud prevention for first-party cases requires a model that tracks repayment behavior and dispute patterns across time, not just the transaction at hand.

Pattern 3: Real-Time Payment Fraud

Real-time payment systems like FedNow and RTP have one defining characteristic: transactions are irreversible. Once funds move, recovery is nearly impossible. Industry data on instant payment fraud consistently shows bank recovery rates under 10%, and that figure aligns with what compliance teams report internally.

Industry data on instant payment fraud consistently shows bank recovery rates under 10%, and that figure aligns with what compliance teams report internally.

The fraud detection gap here is a speed mismatch. Traditional transaction monitoring software was built for batch processing, reviewing transactions in hourly or daily windows. Real-time payments require sub-second decisions. A system that takes three seconds to run a transaction through its rule engine is already too slow for this environment.

The only solution that works is a scoring model that evaluates risk inline, before the transaction settles. This is technically achievable but operationally difficult for institutions running 10 to 15-year-old monitoring platforms. See our analysis of AI-powered fraud detection strategy for risk heads for a look at what real-time detection architectures actually require in practice.

Pattern 4: Multi-Layered Money Mule Networks

Money muling has evolved significantly. The old model (a foreign actor recruits domestic individuals to receive and forward funds) has been replaced by layered networks using cryptocurrency hop points, shell companies, and legitimate business accounts as intermediaries.

A single fraud ring might move funds through 12 layers before they exit the financial system. Your transaction monitoring software sees individual legs of that journey but cannot connect them across accounts, institutions, or time periods. Each hop, on its own, looks like a legitimate business payment.

Network graph analysis is the detection method that actually works here. By mapping relationships between accounts, devices, IP addresses, and transaction counterparties, AI models identify mule network structures even when individual transactions appear clean. This is something rule-based systems structurally cannot do because the pattern exists only at the graph level, not at the individual transaction level.

Pattern 5: Cross-Channel Fraud Orchestration

Modern fraud attacks rarely target a single channel. A typical orchestrated attack uses your mobile app to inventory available products, your call center to socially engineer a password reset, and your web interface to initiate the transaction. Each channel generates its own alert, handled by a different team, with different tooling and different context.

Cross-channel fraud persists because most institutions treat channel risk in silos. The mobile team runs one tool, the card team runs another, the call center operates separately. None of these systems share signals in real time.

The attack that succeeds is the one that triggers no single alert across three channels while following a recognizable attack sequence. A fraudster who stays under each individual channel threshold wins every time. Unified session intelligence across channels closes this gap, but it requires infrastructure changes that go well beyond swapping out a single vendor.

Pattern 6: Alert Fatigue, the Silent Fraud Detection Gap

This pattern is not a fraud attack. It is a system failure that makes every other fraud detection gap worse. The average fraud analyst at a mid-sized bank reviews 300 to 400 alerts per day. Industry estimates consistently show that 85 to 95% of those alerts are false positives.

When analysts review 400 alerts and 390 are wrong, attention degrades. That is not a character issue. It is a predictable cognitive response to sustained noise. The fraud events that do appear get treated with the same level of scrutiny as the 390 false alarms that preceded them.

This is also where transaction monitoring cost becomes a real strategic problem. Each false positive alert costs between $10 and $40 to process when you account for analyst time, escalation overhead, and documentation requirements. At 350 false positives per analyst per day across a team of 20, that exceeds $100,000 per day in wasted review work before you count a single real fraud case.

AI fraud detection reduces this burden by building individual behavioral baselines rather than applying uniform population-level thresholds. We have covered how agentic AI fraud agents can cut false positives by 80% and why the underlying mechanism matters for any team evaluating new tooling. For a deeper comparison, our piece on rule-based systems vs. AI-driven solutions for reducing false positives walks through the tradeoffs in concrete operational terms.

Pattern 7: Behavioral Drift in Long-Standing Customers

Long-term customers represent a fraud detection gap that almost no transaction monitoring system handles well. Account takeover is not always a sudden, obvious event. Sometimes it develops gradually.

A fraudster who gains partial access sits quietly for weeks, then slowly modifies behavior: adding a new payee, adjusting notification preferences, testing transaction limits before the large transfer. All of this happens within what rule-based systems classify as normal for that account, because the account's historical behavior is what makes these small changes appear unremarkable.

Detecting behavioral drift requires an individual behavioral model for each customer, not population-level averages. When a customer who has never initiated a wire transfer suddenly sends funds to a new overseas account, that deviation is significant even if the amount stays under reporting thresholds. Rules set the same thresholds for every account. AI fraud detection builds individual fingerprints and flags deviations from the specific customer's established pattern, not the average customer.

How AI Closes These Fraud Detection Gaps

The common thread across all seven patterns is that rule-based systems fail when fraud exploits context, timing, or cross-account relationships that no single rule can capture. AI fraud detection works differently: models learn from historical signals, adapt as patterns shift, and score risk across dozens of features simultaneously.

Machine learning fraud detection in practice involves several distinct capabilities:

- Supervised models trained on labeled fraud cases identify known patterns at scale across millions of transactions

- Unsupervised anomaly detection flags patterns that don't match any previously seen fraud type

- Graph neural networks map structural relationships across accounts, devices, and transaction counterparties

- Real-time scoring engines process and evaluate transactions in under 50 milliseconds, before settlement occurs

One limitation worth naming directly: AI models are not plug-and-play. They require clean historical data, ongoing monitoring, and skilled tuning. An institution with inconsistent data schemas or poor data hygiene will get inconsistent model performance. Realistic deployment timelines for a well-implemented AI fraud detection system run 6 to 12 months from contract to production, not the 6 weeks some vendor presentations suggest.

For a grounded comparison of where each approach holds up under real production conditions, see our post on AI vs. traditional fraud detection, which covers the specific scenarios where each method wins and where it falls short.

- Most legacy fraud systems run on a simple premise: flag transactions that break predefined rules.

- Synthetic identity fraud is the fastest-growing financial crime in the United States.

- First-party fraud is the category that makes compliance officers uncomfortable because the customer is the fraudster.

- Real-time payment systems like FedNow and RTP have one defining characteristic: transactions are irreversible.

- Money muling has evolved significantly.

Onboard Customers in Seconds

Conclusion

Fraud detection gaps do not announce themselves. They show up in loss reports six months after the fraud occurred, or in regulatory examinations that find your transaction monitoring software missed a pattern visible only in retrospect. The seven patterns covered here, from synthetic identity fraud and first-party schemes to cross-channel orchestration and behavioral drift in existing accounts, share one characteristic: they are invisible to rule-based systems operating in channel silos with static thresholds.

Closing these fraud detection gaps requires moving from static rules to adaptive models, from isolated channel tools to unified intelligence, and from population averages to individual behavioral baselines. That is not a small operational change. But the alternative is reviewing hundreds of false positive alerts every day while real fraud moves through undetected. If your team is ready to assess what a modern approach requires, start with an honest audit of your current false positive rate and mean time to detection. Those two numbers will tell you more about your fraud detection gaps than any vendor demo ever will.

Share this article