.webp)

Introduction

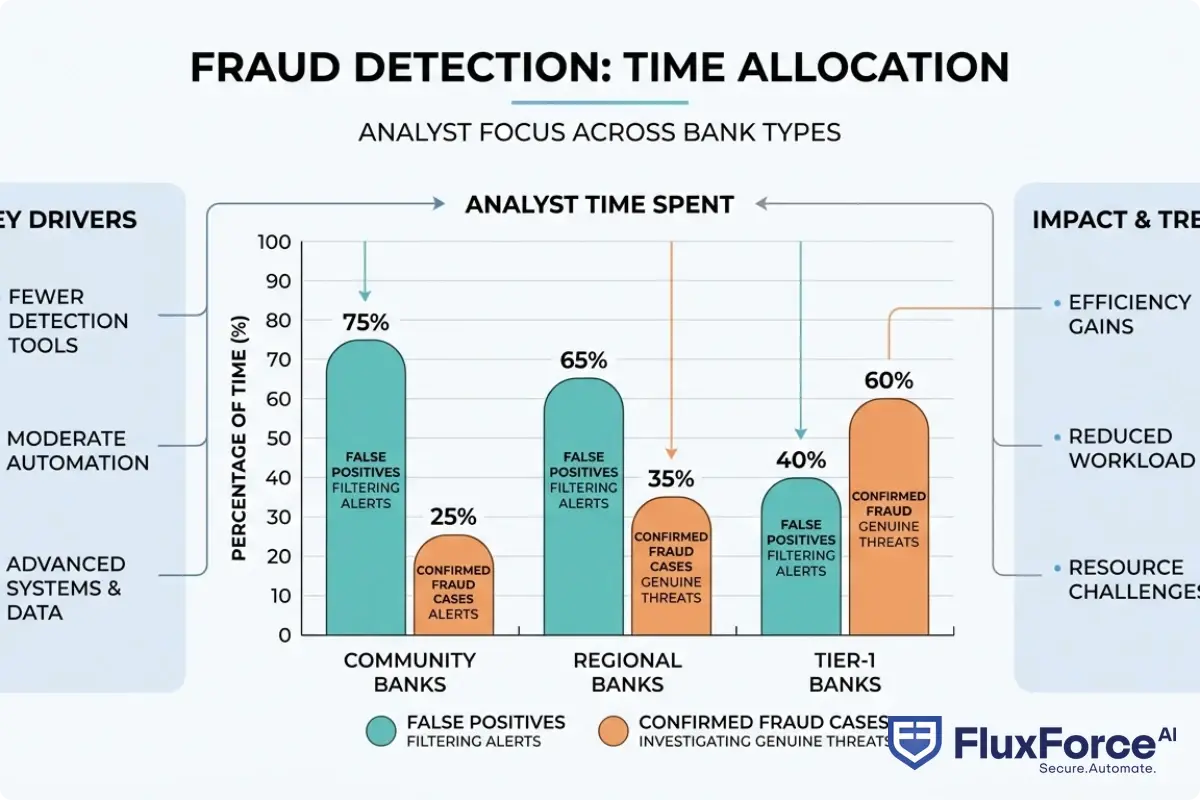

Fraud alert fatigue in financial institutions is one of the most expensive problems that rarely appears on a budget sheet. Analysts at most mid-to-large banks spend roughly 70% of their working hours reviewing alerts that turn out to be false positives: transactions flagged by rules engines, behavioral models, or siloed detection tools that ultimately show no wrongdoing. The fraud never existed. The hour is gone.

Analysts at most mid-to-large banks spend roughly 70% of their working hours reviewing alerts that turn out to be false positives: transactions flagged by rules engines, behavioral models, or siloed detection tools that ultimately show no wrongdoing.

This is not an edge case. According to research from the Association of Certified Fraud Examiners, organizations globally lose an estimated 5% of revenues to fraud annually, yet the operational cost of managing false alert volume generated by legacy systems often exceeds the losses from actual fraud events. The irony is real: the tools built to stop fraud are, in many cases, the reason fraud teams cannot do their jobs.

This post breaks down why the problem exists, what drives alert fatigue at scale, and how a unified risk platform with explainable AI cuts through the noise.

- The Scale of Fraud Alert Fatigue in Financial Institutions

- Why Point Solutions Create More Noise Than Signal

- How a Unified Risk Platform Reduces Fraud Alert Fatigue

- What Is Explainable AI and Why Compliance Teams Care

- How AI Agents Reduce False Positive Alerts in Fraud Detection

Onboard Customers in Seconds

The Scale of Fraud Alert Fatigue in Financial Institutions

Fraud alert fatigue in financial institutions does not look the same at every organization, but the direction of travel is consistent. As digital transaction volumes increase, rule-based fraud engines generate proportionally more alerts. Most of those alerts are noise.

The Hidden Cost of False Positives

The visible cost of false positives is analyst time. The less visible cost is the fraud that slips through while your team is buried in low-signal work.

When analysts review 300-400 alerts per shift, they develop coping patterns: faster review cycles, pattern-matching shortcuts, and lower documentation quality. This is rational behavior under load. But it means genuinely suspicious transactions can receive the same shallow treatment as obvious false positives, and real fraud gets dismissed alongside the noise.

A McKinsey analysis of financial crime compliance operations found that teams at large banks spend 60-80% of their time on low-value alert review tasks. The cost per investigated alert, including analyst salary, case management overhead, and regulatory documentation, typically runs between $15 and $50 at scale.

A McKinsey analysis of financial crime compliance operations found that teams at large banks spend 60-80% of their time on low-value alert review tasks.

How Alert Fatigue Compounds Over Time

The compounding effect is the part most banks underestimate. An analyst who spends six months reviewing 200+ false alerts daily starts to lose calibration on what suspicious activity actually looks like. Alert fatigue creates a gradual desensitization that makes it harder to catch novel fraud patterns, especially synthetic identity fraud, which looks legitimate at every checkpoint until it does not.

This is why detecting synthetic identity fraud in real-time requires more than adding detection rules. It requires a fundamentally different approach to signal processing and triage.

Why Point Solutions Create More Noise Than Signal

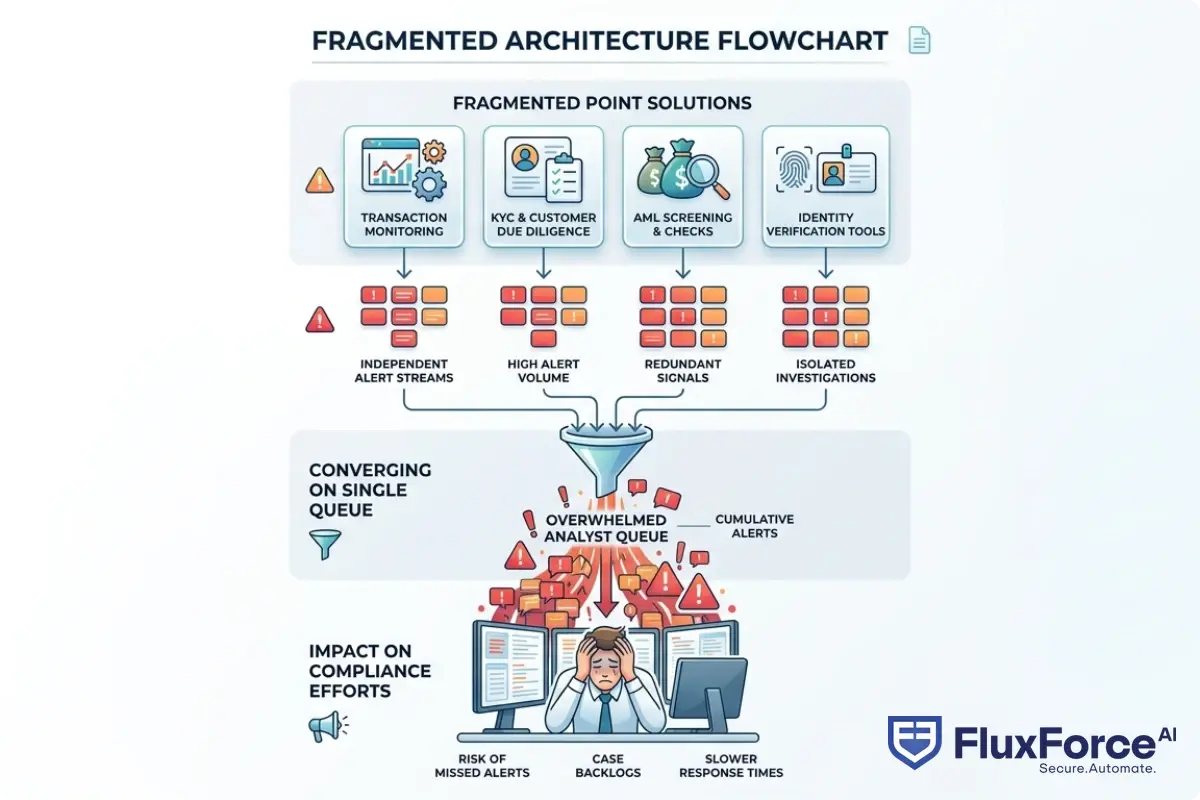

The architecture problem is straightforward once you see it. Most financial institutions have assembled a portfolio of point solutions over the past decade: one vendor for transaction monitoring, another for KYC, a third for AML screening, a fourth for identity verification. Each was evaluated separately, optimized for its own use case, and tuned against its own historical data.

Point Solutions vs Platform Financial Services: What Actually Breaks

Point solutions vs platform financial services is more than a vendor pitch comparison. It is a genuine architectural choice with measurable operational consequences.

When each system generates its own alert stream, analysts receive four separate queues with no shared context. A transaction that looks borderline in the AML system might look completely clean in the identity system, because the identity system does not have access to the AML signals. The analyst manually cross-references systems to build a picture that the platform should have assembled automatically.

The integration tax is real. Banks running five or more fraud and compliance point solutions typically spend 15-25% of their fraud operations budget on integration maintenance, data reconciliation, and keeping disparate systems communicating. That budget produces no fraud prevention value.

The Vendor Consolidation Case for Fintech

Vendor consolidation in fintech is accelerating for two reasons: regulators are pushing for consolidated audit trails, and the operational math on fragmented architectures no longer adds up.

A unified platform does not just reduce vendor relationships. It eliminates the context gaps between systems. When transaction monitoring, identity verification, and AML screening share a single data layer, the signal-to-noise ratio improves because each alert has access to the full risk picture, not just a slice of it. We have covered how this plays out in AML screening for digital lending, where consolidated data cuts false alert rates by a measurable margin.

How a Unified Risk Platform Reduces Fraud Alert Fatigue

A unified risk platform is an integrated environment where transaction monitoring, identity verification, fraud detection, and AML compliance operate from a shared data model. The platform correlates signals across all domains before surfacing anything to an analyst. Analysts see pre-triaged, context-rich cases, not raw alert queues.

AI Security Operations Platform Capabilities

An AI security operations platform built for financial services adds model-driven triage on top of the unified data layer. Instead of an analyst receiving 300 raw alerts, the platform pre-ranks them by confirmed risk confidence, clusters related alerts from the same entity or network, and suppresses alerts that match known-safe patterns.

The practical outcome is significant. A team that previously reviewed 300 alerts per shift might review 60-80 after implementing this approach. The suppressed alerts are not ignored: they are queued for batch review or handled autonomously based on risk thresholds the compliance team has approved in advance.

Fraud Compliance Identity Platform in Practice

A fraud compliance identity platform merges what traditionally required three separate vendor relationships: identity verification at account opening, ongoing behavioral monitoring, and compliance screening against sanctions and watchlists.

When these functions share data, the system detects patterns that siloed tools cannot. A customer whose identity verification passed cleanly at onboarding but who is now transacting with a counterparty flagged in sanctions screening gets a combined risk score that reflects both signals. Neither system alone would catch this pattern. Together, they do. This is also the foundation for stronger KYC and AML verification strategies for CISOs, where the biggest gains come from connecting existing data, not adding new detection layers on top of fragmented infrastructure.

What Is Explainable AI and Why Compliance Teams Care

Explainable AI in finance is the ability of an AI model to produce human-readable reasoning for each decision it makes. For fraud detection, this means the system does not just score a transaction as high-risk. It tells the analyst which features drove the score, in language an auditor or regulator can read and act on.

Black Box AI Compliance Risk

Black box AI compliance risk is a documented concern for banking regulators across multiple jurisdictions. The Financial Stability Board has published guidance noting that AI models that cannot be interrogated create systemic risk because banks cannot demonstrate to regulators how decisions were made.

In practice, a fraud decision made by a black-box model cannot easily be defended in an enforcement action, appealed by a customer, or audited by internal compliance. The liability exposure is not theoretical.

SHAP Values Explained for Regulators

SHAP values (SHapley Additive exPlanations) are one of the primary methods for making AI decisions interpretable. In a fraud context, SHAP values show the contribution of each input feature to the final risk score: transaction amount, time of day, device fingerprint, and geographic anomaly.

SHAP values explained for regulators means the compliance team can produce a plain-language audit trail for any decision. A transaction scored 0.87 for high risk came with a clear explanation: the amount was 4x the customer's 90-day average, the destination account was created 48 hours prior, and the device fingerprint matched nothing in the customer's transaction history. That explanation is defensible. A bare risk score is not.

AI Model Explainability for Regulators

AI model explainability for regulators has moved from best practice to near-regulatory expectation in several markets. The EU AI Act, DORA, and EBA guidelines on internal models all contain provisions requiring financial institutions to document how algorithmic decisions are made.

For explainable AI compliance, this is not just about satisfying auditors. It is about being able to retrain models, explain model drift, and demonstrate consistent behavior over time. XAI fraud detection systems that produce per-decision explanations make this documentation largely automatic, which is a material operational advantage for compliance teams.

How AI Agents Reduce False Positive Alerts in Fraud Detection

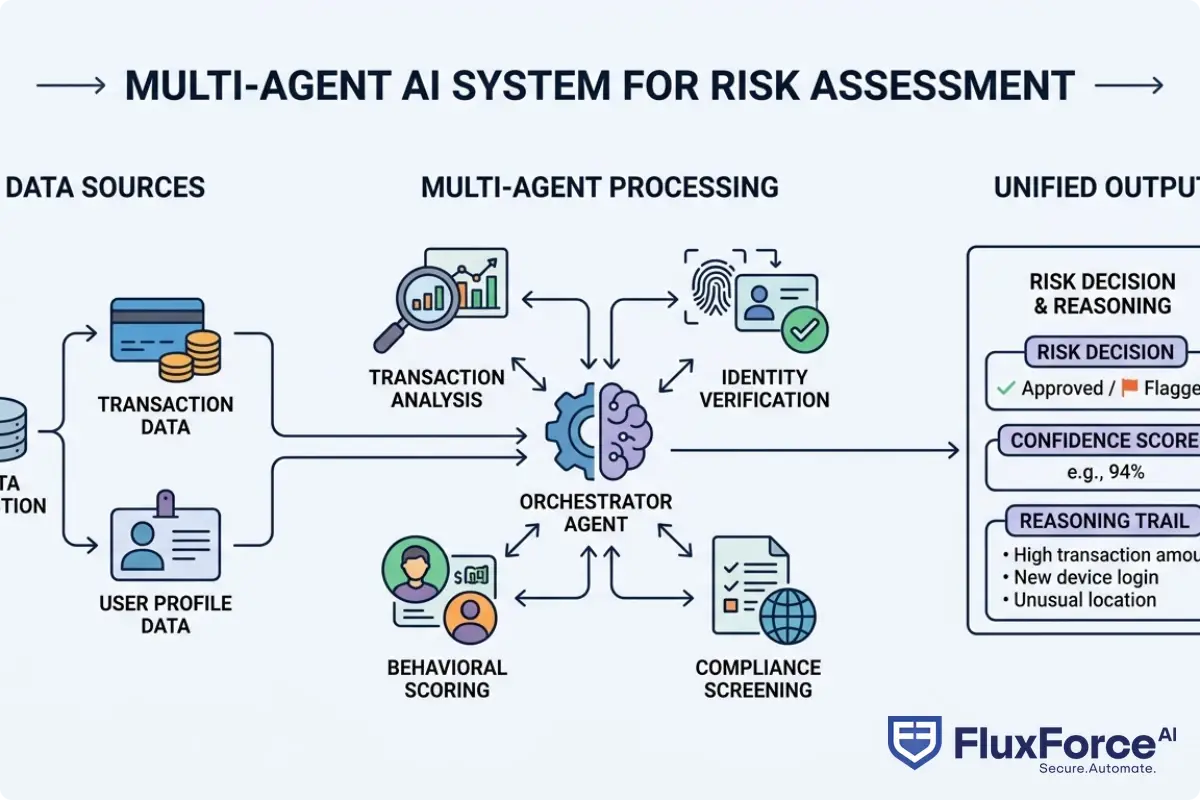

AI agents in financial services work differently from static models. Instead of a single model scoring each transaction in isolation, a multi-agent AI system deploys specialized agents that each focus on a specific domain, then collaborate to produce a joint risk assessment.

Multi-Agent AI System for Fraud Detection

In a multi-agent AI system for fraud, agent collaboration is the key differentiator. A transaction monitoring agent might flag a payment based on amount anomaly. The identity agent checks whether the account passed biometric verification recently. The behavioral agent confirms whether this payment pattern matches the customer's history. The network agent checks whether the destination has any known bad-actor associations.

When all four agents contribute to a single risk decision, the false positive rate drops because the threshold for surfacing an alert to a human analyst is now a multi-signal consensus, not a single-model flag. Each agent can effectively veto a high-risk signal if its own domain data contradicts it.

AI Agent Fraud Detection in Real-Time

AI agent fraud detection operates at the speed fraud actually happens. Card fraud and account takeover typically execute in under two minutes from initial access to fund movement. Static rule engines that batch-process transactions every 15-30 minutes are structurally unable to stop these attacks in time.

AI agents that score in real-time, within 200-500ms of transaction initiation, can block fraud before settlement. The precision of multi-signal scoring means fewer false blocks at the same sensitivity level. This is the architecture behind the false positive reduction rates discussed in our post on how agentic AI fraud agents cut false positives.

AI Audit Trail Automation

AI audit trail automation is a direct output of agentic architectures. Because each agent logs its inputs, outputs, and reasoning for every decision, the case management system automatically builds a complete decision record without analyst documentation overhead.

This reduces per-alert documentation time from several minutes to near-zero. It also produces the granular audit evidence that regulators increasingly expect under DORA and EBA model governance guidelines.

Configurable AI Autonomy and Human-in-the-Loop Banking

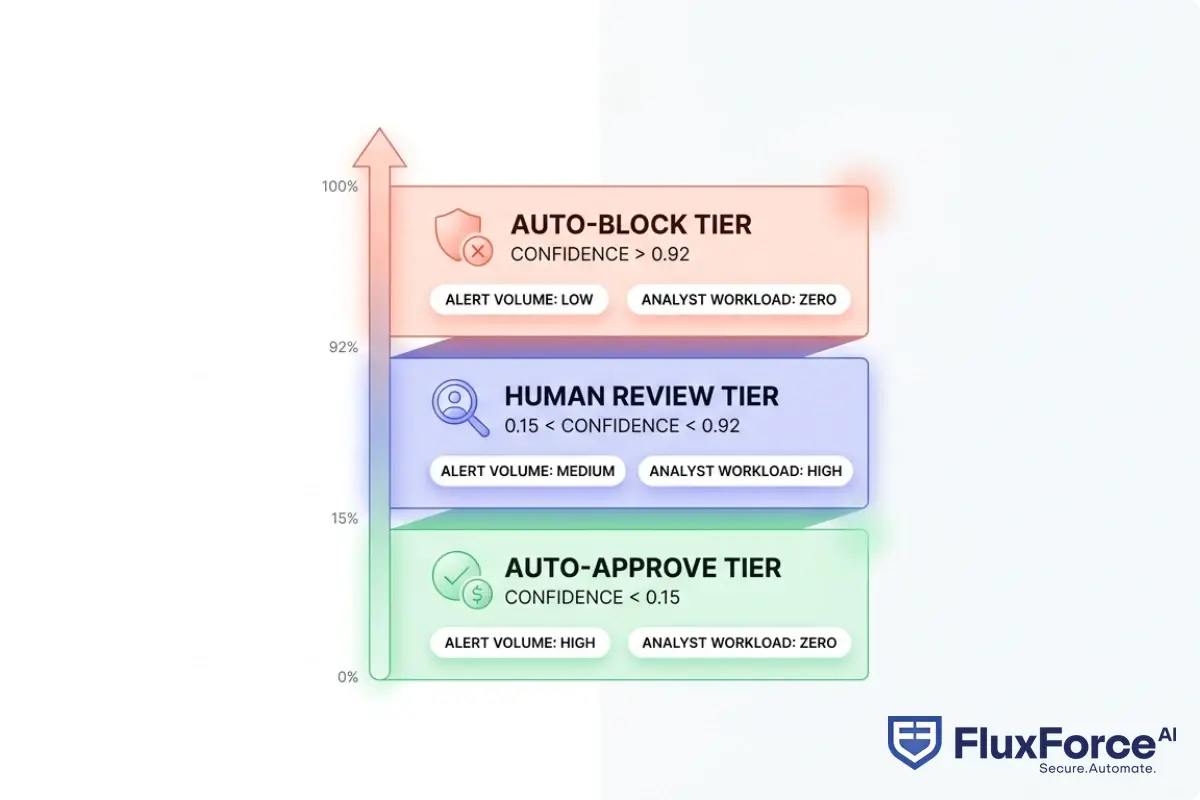

Not every fraud decision should be made by an AI model alone. The most practical deployment model for human-in-the-loop AI banking is a tiered autonomy framework where AI handles decisions at both ends of the confidence spectrum, and humans handle the uncertain middle.

Human-in-the-Loop AI Banking Workflows

A human-in-the-loop AI banking workflow looks like this in practice:

- Transactions with a model confidence score above 0.92 are automatically blocked and queued for batch analyst review

- Transactions with a confidence score below 0.15 are automatically approved and logged

- Transactions in the 0.15-0.92 band are routed to analyst queues with pre-built case summaries drawn from all contributing agent signals

Analysts only touch genuinely ambiguous cases. Volume drops by 60-80% compared to reviewing every flagged transaction, and the quality of review improves because analysts spend time on cases where human judgment adds value that the model cannot provide.

Volume drops by 60-80% compared to reviewing every flagged transaction, and the quality of review improves because analysts spend time on cases where human judgment adds value that the model cannot provide.

Configurable AI Autonomy Settings

Configurable AI autonomy means the compliance team, not the vendor, sets the thresholds. A bank under heightened regulatory scrutiny might tighten the human review band to 0.10-0.95 to increase oversight. A fintech with a different risk appetite might widen the auto-approve range based on its customer friction tolerance.

This configurability matters in regulatory conversations too. When examiners ask how your fraud system makes decisions, being able to show a compliance-team-approved threshold policy governing AI autonomy is a much cleaner answer than saying the model decides on its own. For more on building compliant AI frameworks in banking, see our analysis of zero trust and agentic AI for banking security.

- Fraud alert fatigue in financial institutions does not look the same at every organization, but the direction of travel is consistent.

- The architecture problem is straightforward once you see it.

- A unified risk platform is an integrated environment where transaction monitoring, identity verification, fraud detection, and AML compliance operate from a shared data model.

- Explainable AI in finance is the ability of an AI model to produce human-readable reasoning for each decision it makes.

- AI agents in financial services work differently from static models.

Onboard Customers in Seconds

Conclusion

Fraud alert fatigue in financial institutions is not a staffing problem. Hiring more analysts to review more false positives does not fix the underlying architecture. It scales the inefficiency.

The path forward connects three changes: consolidate point solutions into a unified risk platform that shares data across fraud, identity, and AML compliance; deploy AI agents that triage and correlate signals before they reach human analysts; and build explainable AI compliance into the architecture from the start so every decision is auditable.

The 70% of analyst time currently spent on false alerts is recoverable capacity. A team spending 30% on false positives and 70% on confirmed fraud cases is a fundamentally different operation. That shift starts with the platform decision.

If your fraud team is under water on alert volume, the comparison of AI vs. traditional fraud detection methods is a useful starting point for understanding what the architecture gap looks like in practice.

Share this article