.webp)

Introduction

Mid-market bank fraud 2026 is already underway, and most institutions in the $1B to $50B asset range are underprepared for what's hitting them. Fraudsters have quietly shifted focus away from the largest global banks (which now run some of the most sophisticated detection systems in the world) toward mid-sized institutions that carry significant transaction volume but operate with leaner fraud teams and older technology stacks.

Mid-market bank fraud 2026 is already underway, and most institutions in the $1B to $50B asset range are underprepared for what's hitting them.

According to the FBI's Internet Crime Complaint Center, financial fraud losses in the U.S. exceeded $12.5 billion in 2023. The trend line points sharply upward into 2026. Mid-market banks are absorbing a growing share of those losses, often without the real-time visibility to catch fraud before it clears.

This post covers why mid-market banks have become the preferred fraud target, how the most damaging patterns actually work, and what modern fraud detection genuinely requires in 2026.

- Why Mid-Market Banks Are Now the Primary Fraud Target

- The Fraud Exposure Gap Between Big Banks and Mid-Market

- How Synthetic Identity Fraud Exploits Mid-Market Vulnerabilities

- The Hidden Cost of Transaction Monitoring at Mid-Market Scale

- AI Fraud Detection: What It Is and How It Actually Works

Onboard Customers in Seconds

Why Mid-Market Banks Are Now the Primary Fraud Target

There is a clear logic to how fraud operators choose their targets. Global banks now employ hundreds of fraud analysts and run machine learning models trained on billions of transactions. They block account takeover attempts in milliseconds. The return on investment for attackers has dropped sharply at that tier.

Mid-market banks represent a different calculation. They hold real assets, process real payments, and often serve thousands of small businesses and retail clients. But their fraud operations frequently rely on rule-based transaction monitoring software configured five or more years ago, teams of fewer than 20 analysts, and alert queues that overflow daily.

The gap is not about intent. Mid-market compliance and fraud teams are often sharp and experienced. The gap is in tooling and scale. When a bank processes 500,000 transactions per day with a team built to review 300 alerts, the math stops working. Fraud operators have noticed, and mid-market bank fraud in 2026 reflects that shift clearly.

The Fraud Exposure Gap Between Big Banks and Mid-Market

The disparity in fraud budgets is significant. JPMorgan Chase reportedly spends over $600 million annually on cybersecurity and fraud prevention. The average mid-market bank spends $2 million to $8 million across all fraud and AML operations combined, a fraction of what the threat surface demands.

This creates a measurable detection gap. Large banks catch roughly 80-90% of fraud attempts in real time. Mid-market banks, depending on their technology stack, catch 50-65% in real time, with the remainder flagged in next-day batch reviews after funds have already moved.

Payment fraud prevention at the mid-market level also suffers from a staffing squeeze. When fraud analysts spend 60-70% of their day chasing false positives on legitimate transactions, actual fraud slipping through receives less attention. This is the fraud alert fatigue problem in practice, not theory.

When fraud analysts spend 60-70% of their day chasing false positives on legitimate transactions, actual fraud slipping through receives less attention.

Fraud operators test attacks against mid-market banks first. If an account takeover scheme or synthetic identity fraud pattern works at a regional bank, it scales. By the time the institution notices a pattern, the fraud ring has typically moved on.

For a detailed breakdown of card-specific fraud patterns and AI-based detection approaches, see our AI-powered fraud detection strategy for risk heads.

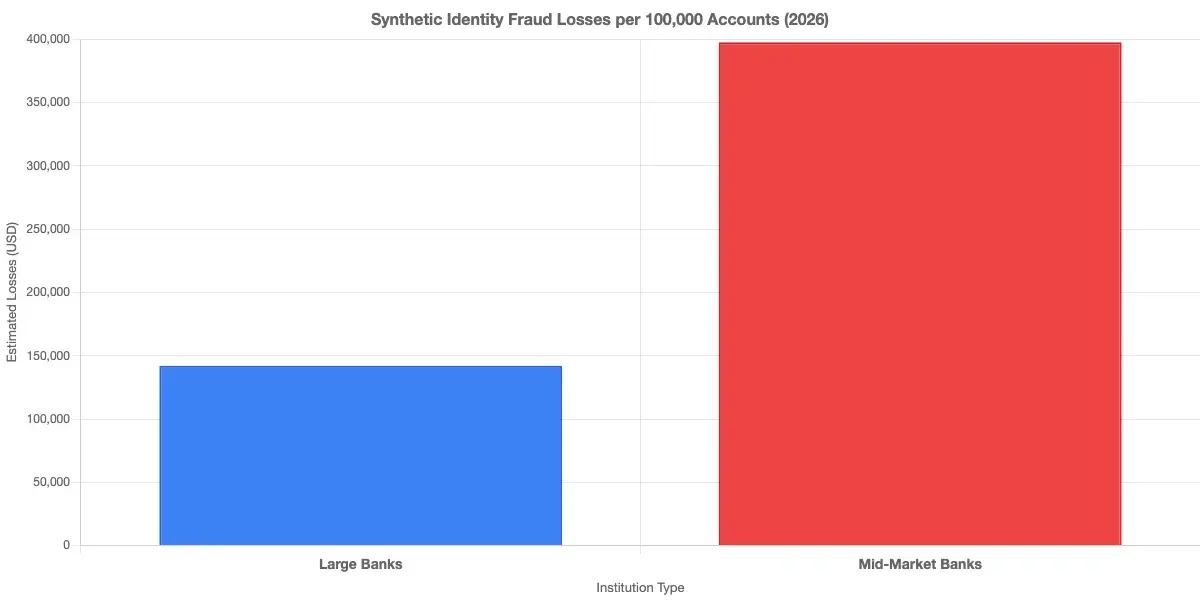

How Synthetic Identity Fraud Exploits Mid-Market Vulnerabilities

Synthetic identity fraud is the fastest-growing fraud category in U.S. banking. The Federal Financial Institutions Examination Council (FFIEC) has flagged it as a top examination concern in its recent guidance. Unlike traditional identity theft, synthetic fraud combines real Social Security numbers (often stolen from children or deceased individuals) with fabricated names and addresses to create identities that carry no fraud history.

These synthetic identities are used to open accounts, build credit history over months or even years, and then execute a bust-out event where every available credit line is maxed before the identity disappears. Mid-market banks are particularly exposed because:

- Their onboarding KYC checks are often less sophisticated than those at large banks

- Their fraud models haven't been trained on synthetic patterns at scale

- Their customer data is rarely cross-referenced in real time against industry consortium databases

The average synthetic identity fraud loss per successful bust-out runs $15,000 to $30,000. A coordinated ring targeting a mid-market bank can execute hundreds of these in a single quarter before detection occurs.

Our detailed guide on detecting synthetic identity fraud in real time covers the specific signals that AI models catch where rule-based systems fail entirely.

The Hidden Cost of Transaction Monitoring at Mid-Market Scale

Transaction monitoring cost is one of the most underestimated line items in mid-market banking. The visible cost is the software license. The invisible cost is the analyst time consumed by false positive alerts.

FinCEN and independent compliance research estimate that financial institutions spend approximately $200 to $300 billion globally on financial crime compliance each year. For a mid-market bank specifically, the cost picture looks like this:

- A typical rule-based system generates 90-98% false positive rates on flagged alerts

- At $20-$50 per analyst hour, a team processing 500 alerts per day can spend $3 million to $7 million annually on reviews that produce no suspicious activity reports

- That same budget could fund two additional fraud analysts or a meaningful AI detection upgrade

The transaction monitoring cost problem is also a regulatory risk. When analysts are buried in false positives, genuinely suspicious patterns get less scrutiny. Regulators have increasingly flagged this in exam findings, particularly at institutions running outdated rule configurations without any machine learning layer on top.

Automated transaction monitoring, properly implemented, doesn't just reduce analyst workload. It shifts the workload toward the cases that actually matter.

AI Fraud Detection: What It Is and How It Actually Works

AI fraud detection is the use of machine learning models to identify potentially fraudulent transactions or behaviors in real time, based on patterns learned from large historical datasets of fraud and non-fraud events.

Unlike rule-based systems that flag transactions meeting specific preset criteria, machine learning fraud detection identifies statistical anomalies that don't fit a customer's normal behavior. A customer who normally transfers $500 per month initiating a $12,000 wire on a Sunday night triggers a risk score, even when no static rule covers that exact pattern.

How does AI detect fraud? The core process works in four steps:

- Transaction data ingestion: Every transaction converts into a feature vector with hundreds of attributes, including amount, time, geolocation, device fingerprint, counterparty history, and account age.

- Model scoring: A trained model (gradient boosting, neural network, or graph-based) assigns a risk score in under 100 milliseconds.

- Alert triage: High-risk scores trigger alerts. Scores below threshold pass automatically. Borderline scores route to a secondary review queue.

- Feedback loop: Analyst dispositions (fraud confirmed or cleared) feed back into the model, continuously improving precision over time.

AI fraud detection in banking has moved from experimental to operational at major institutions. For mid-market banks, implementation complexity depends heavily on data infrastructure quality. Banks with clean, labeled historical fraud data can deploy effective models in 90-120 days. Banks with fragmented core systems and poor data quality take longer, but the path is well-documented at this point.

For a full comparison of what AI-based detection catches versus what rule-based systems miss, see our breakdown of AI vs. Traditional Fraud Detection.

Real-Time Fraud Detection vs. Batch Processing: Why Timing Matters

Real-time fraud detection means evaluating every transaction at the moment it is initiated, before it clears. Batch processing means reviewing transactions in groups, typically overnight or on a significant delay.

The timing difference has a direct dollar impact. Most payment fraud, particularly ACH and wire fraud, becomes nearly irretrievable once funds leave the originating bank. If detection happens six hours later in a batch review, the fraud is already complete and the recovery odds are low.

Real-time fraud detection banks are now building infrastructure that processes decisions in under 200 milliseconds at peak load. This requires fundamentally different architecture than batch systems: streaming data pipelines, low-latency model serving, and real-time enrichment with device and network signals.

The tooling has matured significantly. Modern automated transaction monitoring platforms, whether you are evaluating options in the sardine vs unit21 space or working with established enterprise vendors, now offer real-time scoring at price points accessible to institutions below $50B in assets. The deployment complexity has dropped considerably from where it stood three years ago.

Modern automated transaction monitoring platforms, whether you are evaluating options in the sardine vs unit21 space or working with established enterprise vendors, now offer real-time scoring at price points accessible to institutions below $50B in assets.

The honest tradeoff: real-time detection requires more upfront integration work, especially connecting to core banking systems, card processors, and wire origination platforms. Banks that have completed a core banking modernization project are in a much stronger position to move quickly.

Fraud Alert Fatigue and the False Positive Crisis

Fraud alert fatigue is the state where fraud analysts become desensitized to alerts because the volume of false positives is so high that genuine alarms don't receive adequate attention. This is not a morale problem. It is a systematic failure of detection configuration.

High false positive rates in fraud detection create three compounding problems:

Analyst burnout and turnover: Fraud analysts who spend their days clearing legitimate transactions don't build the investigative intuition that catches real fraud. The role becomes data entry, not investigation. Turnover in fraud operations at mid-market banks runs 25-35% annually, and alert fatigue is consistently cited as a primary driver.

Slower response to real fraud: When an analyst has 200 alerts to clear before noon, the genuine fraud case buried in that queue receives the same 90-second review as the false positive. Pattern recognition degrades across the entire team over time.

Model decay: If false positives aren't properly labeled and fed back into the model, the system never improves. Rule-based systems are particularly prone to this because adding new rules to reduce one false positive category often creates new ones elsewhere.

The true false positive cost in fraud operations, including customer friction from declined legitimate transactions, relationship damage, and operational overhead, runs $5 to $15 per alert. At hundreds of thousands of alerts annually, the false positive cost fraud teams absorb is substantial and largely invisible to leadership.

Reducing false positives in AML and fraud monitoring runs through better model tuning, behavioral baselines, and contextual enrichment. Our post on how agentic AI fraud agents cut false positives by 80% covers the specific mechanisms that make that reduction achievable in production environments.

How Mid-Market Banks Can Fight Back Against Fraud in 2026

Mid-market bank fraud 2026 is a solvable problem, not an inevitable loss. The institutions that are closing the detection gap are doing four things differently from those still absorbing compounding losses:

Moving from rules to behavioral models: Static rule-based transaction monitoring catches the fraud that happened last year. Behavioral models catch what is happening now. The transition doesn't have to be all-or-nothing. Many banks run hybrid architectures where AI scores supplement existing rules, with rules acting as hard stops for high-risk patterns and AI handling probabilistic scoring across the broader transaction population.

Investing in real-time over batch: The ROI case for real-time fraud detection is straightforward. Each percentage point improvement in real-time catch rates prevents losses that are virtually unrecoverable. Banks with real-time systems consistently report 30-45% reductions in fraud losses within 12 months of full deployment.

Targeting false positive reduction first: Reducing the false positive rate from 95% to 80% frees up analyst capacity equivalent to two or three additional FTEs. That capacity redirects toward investigation quality, not alert volume. This is precisely where legacy fraud detection systems without agentic AI show their limits most clearly, and where the ROI case for modernization is easiest to build.

Joining industry data consortia: Synthetic identity fraud is much harder to detect in isolation. Banks that contribute to and consume industry-wide fraud signal databases, including shared blacklists, known synthetic identity patterns, and mule account networks, catch fraud that no individual bank's model would identify alone. Mid-market banks have historically underinvested in this area, even though the entry cost has dropped significantly.

Payment fraud prevention at scale also benefits from zero trust principles applied to internal access controls. When fraud originates internally or through compromised credentials, robust access architecture matters as much as external transaction monitoring.

- There is a clear logic to how fraud operators choose their targets.

- The disparity in fraud budgets is significant.

- Synthetic identity fraud is the fastest-growing fraud category in U.S.

- Transaction monitoring cost is one of the most underestimated line items in mid-market banking.

- AI fraud detection is the use of machine learning models to identify potentially fraudulent transactions or behaviors in real time, based on patterns learned from large historical datasets of fraud and non-fraud events.

Onboard Customers in Seconds

Conclusion

Mid-market bank fraud 2026 represents the most concentrated fraud threat this sector has faced in a decade. Attackers have done the math: mid-market banks hold real assets, process real volume, and often run detection systems that haven't kept pace with how fraud tactics have evolved.

The answer isn't to spend like a global bank. It's to spend smarter. AI fraud detection in banking has matured to the point where mid-market institutions can deploy behavioral models, reduce false positives substantially, and shift from batch to real-time detection within realistic budget and timeline constraints.

The banks that treat fraud modernization as an operational priority in 2026, rather than a future roadmap item, will close the detection gap. Those that wait will keep absorbing losses that compound quarter over quarter. The tools exist. The only question is when your institution decides to use them.

Share this article