.webp)

Introduction

Transaction monitoring software is the backbone of modern financial crime compliance, and the buying decision you make in 2026 will shape your team's productivity and regulatory exposure for years. The market has shifted: legacy rule-based tools that once dominated banking compliance are losing ground to AI-native platforms that process events in milliseconds. This guide covers everything a CISO, compliance officer, or operations head needs to know before signing a contract: how these systems work, what drives cost, which vendors are worth evaluating, and how to cut false positive rates without compromising detection. If you are replacing a dated system or buying for the first time, the framework mapped out here will save you months of vendor calls.

- What Is Transaction Monitoring Software?

- How Does AI Detect Fraud? A Technical Breakdown

- The False Positive Problem in Transaction Monitoring

- Real-Time Fraud Detection: What Banks Actually Need

- Transaction Monitoring Cost: What to Budget in 2026

Onboard Customers in Seconds

What Is Transaction Monitoring Software?

Transaction monitoring software is a platform that ingests financial transaction data, applies detection rules or machine learning models, and flags potentially suspicious activity for human review or automated action. At minimum, a compliant system must support Suspicious Activity Report (SAR) filing workflows, audit trails, and configurable alert thresholds.

The term covers a wide range of tools: basic rule engines that flag transactions above a dollar threshold, full-stack AML platforms with entity resolution and network analysis, and modern AI-native systems that continuously learn from analyst decisions. In regulated industries, deploying some form of transaction monitoring software is not optional. The Bank Secrecy Act and its international equivalents (EU AMLD6, FATF recommendations) require financial institutions to monitor, detect, and report suspicious transactions.

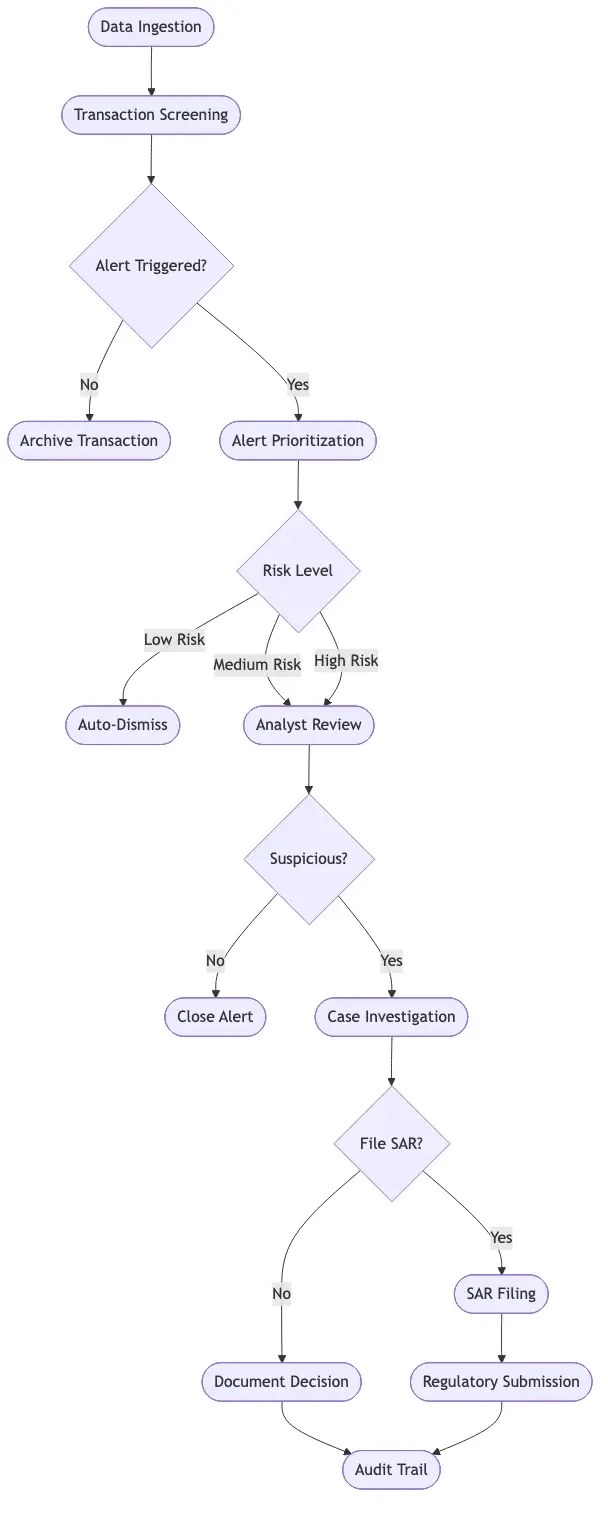

The Core Monitoring Workflow

A typical transaction monitoring cycle follows these steps:

- Data ingestion: Transactions stream in from core banking, card networks, or payment rails

- Enrichment: Customer profile data, device signals, and behavioral history are appended

- Detection: Rules and/or ML models score each transaction for risk

- Alert generation: Transactions above a risk threshold become alerts in an analyst queue

- Investigation: Analysts review, document, and disposition each alert

- Reporting: Confirmed suspicious activity triggers a SAR filing

Rule-Based vs. AI-Native Platforms

Rule-based systems rely on static thresholds and scenarios defined by compliance teams. They are transparent and auditable, but they do not adapt. If criminals shift tactics, the rules do not update until a human rewrites them.

AI-native platforms continuously recalibrate based on new transaction patterns. The tradeoff is explainability: some ML models require additional tooling to produce the documentation regulators expect. Most production deployments in 2026 use automated transaction monitoring with a hybrid approach, rule-based detection for well-understood typologies and AI-based detection for emerging patterns.

How Does AI Detect Fraud? A Technical Breakdown

AI fraud detection works by training statistical models on historical transaction data to identify patterns associated with confirmed fraud. This is fundamentally different from rule-based detection because the system learns from outcomes rather than relying solely on human-authored logic.

AI Fraud Detection Explained

AI fraud detection explained simply: most commercial platforms combine several techniques rather than relying on a single model type.

- Supervised learning: Models trained on labeled fraud and legitimate transaction pairs learn decision boundaries. These work well when you have enough labeled examples.

- Unsupervised anomaly detection: Useful for catching novel fraud types where labels do not yet exist. The model flags transactions that deviate significantly from a customer's established behavior.

- Graph analytics: Detects money laundering networks by mapping relationships between accounts, devices, and IP addresses. Particularly effective for catching synthetic identity fraud rings.

- Sequence models (LSTM, Transformer): Analyze the sequence of a customer's transactions to detect behavioral drift over time.

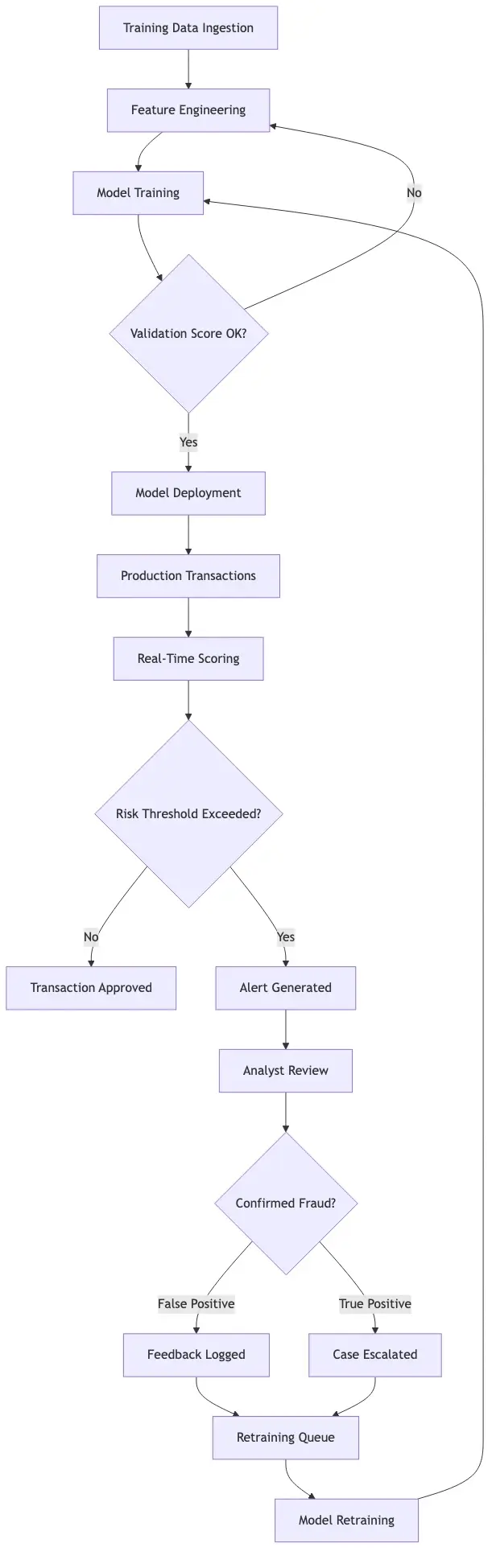

How AI Fraud Detection Works in Banking

AI fraud detection in banking involves a production challenge that is easy to underestimate: models trained on historical data drift as fraud tactics evolve. A well-run machine learning fraud detection program includes continuous retraining pipelines, champion/challenger model testing, and performance dashboards that alert the team when detection rates fall.

Banks getting the most value from AI are not just plugging in a vendor's model. They are building feedback loops where analyst decisions on alerts flow back into training datasets. That feedback loop is what separates a system that improves over time from one that stagnates within 18 months of deployment. Payment fraud prevention at scale requires this kind of continuous improvement, not a static deployment.

Detecting Synthetic Identity Fraud

Detecting synthetic identity fraud in real-time is one of the hardest problems in financial crime. Fraudsters construct fictitious identities using real Social Security numbers combined with fabricated names and addresses, often building credit profiles over 12-18 months before a bust-out event. Rule-based systems almost never catch these because individual transactions look legitimate. Graph-based AI models that analyze relationships between shared data elements, such as the same SSN appearing across multiple new account applications, are far more effective at catching these patterns before losses accumulate.

The False Positive Problem in Transaction Monitoring

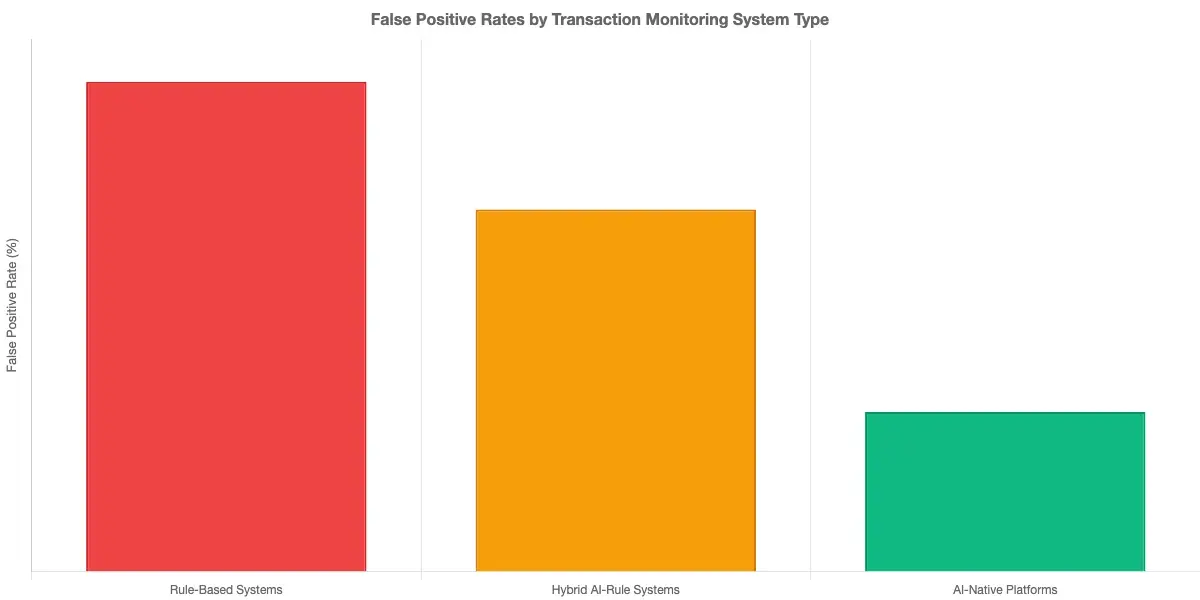

False positives are the largest operational cost most compliance teams do not fully quantify. The false positive rate in fraud detection refers to the proportion of alerts that turn out to be legitimate transactions incorrectly flagged as suspicious.

Industry benchmarks are sobering. Some rule-heavy implementations see false positive rates above 95%, meaning 19 out of every 20 alerts an analyst reviews turns out to be nothing. The false positive cost in fraud programs compounds quickly when you account for analyst time, customer friction from delayed payments, and the reputational cost of wrongly blocking legitimate transactions.

Some rule-heavy implementations see false positive rates above 95%, meaning 19 out of every 20 alerts an analyst reviews turns out to be nothing.

Why Fraud Alert Fatigue Kills Compliance Programs

Fraud alert fatigue happens when analysts are buried under so many low-quality alerts that they begin rubber-stamping investigations rather than conducting real reviews. The irony is that organizations trying to reduce compliance risk by casting a wide net often end up with worse outcomes: analysts miss genuine suspicious activity because they are numbed by volume.

Research from McKinsey shows compliance teams using AI-assisted triage spent 30-50% less time on alert review compared to purely manual workflows. The improvement is not just efficiency. It is accuracy.

Research from McKinsey shows compliance teams using AI-assisted triage spent 30-50% less time on alert review compared to purely manual workflows.

How to Reduce False Positives in AML

How to reduce false positives in AML is a practical question with several answers that teams can act on today:

- Tune existing rules annually: Most rule-based systems have thresholds set at implementation and never revisited. Annual rule reviews can meaningfully cut alert volume without changing platforms.

- Add behavioral context: Alerts on transactions that match a customer's 24-month transaction history are far less likely to represent genuine suspicious activity.

- Implement risk scoring: Replace binary alert/no-alert logic with a tiered risk score. Analysts focus on high-score items; low-score alerts get auto-closed with documentation.

- Layer ML-based triage on existing engines: Even without replacing your core detection platform, a triage model can reduce false positives in transaction monitoring by 40-60% within 90 days of deployment.

- Close the feedback loop: Feed analyst dispositions back into models. If analysts consistently close a specific alert pattern as false positive, the system should learn and stop generating it.

For a detailed look at how agentic AI approaches false positives in fraud detection, How Agentic AI Fraud Agents Cut False Positives by 80% lays out the mechanics and production results from live deployments.

For a detailed look at how agentic AI approaches false positives in fraud detection, How Agentic AI Fraud Agents Cut False Positives by 80% lays out the mechanics and production results from live deployments.

Real-Time Fraud Detection: What Banks Actually Need

Real-time fraud detection refers to systems that evaluate a transaction before it settles, typically within 50-200 milliseconds for card payments and within a few seconds for ACH or wire transfers. Not every financial crime use case requires real-time intervention, but payment fraud and account takeover do.

Real-Time Fraud Detection for Banks at Scale

Real-time fraud detection for banks operating at millions of transactions per day requires infrastructure decisions that go well beyond the detection model itself. Latency, throughput, and uptime SLAs matter as much as detection accuracy when you sit in the card authorization path.

Key infrastructure requirements:

- Sub-100ms P95 latency during peak processing windows

- 99.99% uptime with no maintenance windows during business hours

- Stateful session tracking for sequence-based anomaly detection

- Integration with card management, core banking, and identity verification systems

Vendors still batch-processing transactions nightly are not viable for real-time payment fraud prevention at card speed. Confirm the streaming architecture before adding any vendor to your shortlist.

Batch Processing Still Has a Place

The honest answer is that most organizations need both real-time and batch processing. Real-time scoring handles card fraud and account takeover. Batch processing handles AML typology detection, where you often need to analyze patterns across weeks of transaction history before a trend becomes actionable.

If a vendor pitches a pure real-time or pure batch architecture, ask directly how they handle use cases outside their model. The answer reveals how well they understand your actual operating environment versus how well they understand their own sales narrative.

Transaction Monitoring Cost: What to Budget in 2026

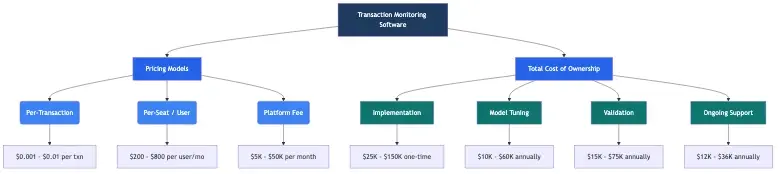

Transaction monitoring cost varies significantly depending on deployment model, transaction volume, and feature scope. Understanding the full cost picture before you sign prevents the budget surprises that typically surface 12 months post-implementation.

Pricing Models in the Market

| Model | Typical Range | Best For |

|---|---|---|

| Per-transaction | $0.0001-$0.005/transaction | High-volume fintechs and payment processors |

| Per-seat (analyst) | $500-$3,000/analyst/month | Mid-size banks with stable analyst teams |

| Platform fee + usage | $50,000-$500,000/year base | Enterprise banks with custom requirements |

| SaaS subscription | $2,000-$25,000/month | Mid-market, packaged feature sets |

Hidden Costs Most Buyers Underestimate

The license fee is rarely the largest line item. Build these into your total cost of ownership:

- Implementation and integration: Connecting automated transaction monitoring to core banking, card platforms, and identity systems typically runs 3-6 months and costs 50-150% of first-year license fees.

- Tuning period: Plan for 2-3 months of model tuning after go-live. Analyst time during this period is real cost, not covered by the vendor contract.

- Ongoing headcount: AI reduces analyst workload but does not eliminate it. Budget for investigation time based on projected post-tuning alert volume, not pre-AI volumes.

- Regulatory validation: OCC, FINRA, and ECB supervisors increasingly expect documented validation of ML models used in BSA/AML programs. Factor in the time and expertise this requires.

For compliance teams already running automated reporting workflows and evaluating the build-vs-buy question, Manual Compliance vs. AI Automation: Pros, Cons, and Best Practices provides a useful cost framework.

Comparing Transaction Monitoring Software Vendors in 2026

The vendor market has consolidated meaningfully over the past three years. A few platform players dominate the mid-market and enterprise segments, with a long tail of point solutions targeting specific verticals. Evaluating ai fraud detection software options requires matching vendor strengths to your primary use case rather than buying on feature count.

Sardine vs Unit21: An Honest Comparison

The sardine vs unit21 question comes up constantly in mid-market evaluations, and the right answer depends on where your primary bottleneck sits.

Sardine is strongest for real-time payment fraud prevention, particularly for fintechs and neobanks processing card and ACH payments. Its device intelligence and behavioral biometrics capabilities are genuinely differentiated. If account takeover and card fraud are your primary concerns, Sardine belongs on your shortlist.

Unit21 is a compliance operations platform first: its investigative workflow tools, SAR filing automation, and case management capabilities are more mature than Sardine's. It fits better when AML compliance operations are the bottleneck rather than real-time fraud scoring.

The practical split: Sardine stops fraud before it clears; Unit21 manages the compliance workflow after detection. Some organizations run both, using Sardine at the authorization layer and Unit21 for case management and SAR filing.

Unit21 Alternatives Worth Evaluating

If Unit21 does not fit your requirements, the strongest unit21 alternative options in 2026 include:

- Hawk AI: Purpose-built AML with solid explainability features; particularly competitive in the European regulatory environment

- Featurespace: ARIC platform uses adaptive behavioral analytics; strong track record in banking and gaming verticals

- Feedzai: Machine learning fraud detection with depth in card issuing and acquiring contexts

- ComplyAdvantage: Better positioned for sanctions screening and adverse media than transactional fraud detection

- Spec: Newer platform with an agentic AI architecture that materially reduces analyst workload in production

For a direct architectural comparison of how these platforms differ, AI vs. Traditional Fraud Detection: Key Differences Every Risk Officer Should Know covers the practical tradeoffs in detail.

How to Evaluate Transaction Monitoring Software

Buying transaction monitoring software is a 6-18 month process when you factor in vendor evaluation, contract negotiation, implementation, and model tuning. A structured approach reduces the risk of choosing a platform that does not fit your actual environment.

Define Your Primary Use Cases First

Before talking to vendors, rank your requirements by business priority:

- Payment fraud prevention (card-present, CNP, ACH, wire)

- AML compliance (SAR filing, typology detection, regulatory reporting)

- Account takeover detection

- Synthetic identity fraud detection

- Sanctions screening and adverse media monitoring

Your top-ranked use case drives the shortlist. A platform built for AML workflow automation is not the same product as one built for real-time payment fraud scoring.

Technical Due Diligence Checklist

Request the following from every shortlisted vendor:

- False positive rate benchmarks from production deployments, not lab environments or reference customers

- P95 latency data at your expected transaction volume

- Model explainability documentation sufficient for regulatory examiner review

- Data residency and encryption standards matching your jurisdiction

- Integration documentation specific to your core banking or card management platform

For institutions with API-heavy architectures, the security evaluation criteria in API Security Strategies for CISOs in Banking apply directly when transaction monitoring integrates with third-party payment APIs.

Run a Proof of Concept on Your Own Data

Never buy based on a demo using vendor reference data. Require a POC using at least 90 days of your own historical transactions, with known fraud cases in the test set. Measure detection rate on confirmed fraud, false positive rate on confirmed legitimate transactions, total alert volume your analysts would actually face, and time from data ingestion to first actionable alert.

Validate Regulatory Compliance Before Signing

Confirm the platform supports SAR and CTR filing workflows per FinCEN requirements, audit trail retention for your jurisdiction, and model documentation adequate for examiner review. For regulated institutions working through compliance reporting automation, Regulatory Compliance in Banking: Reporting and Automation Strategy for Payments Risk Officers provides a practical framework for structuring that validation work.

- Transaction monitoring software is a platform that ingests financial transaction data, applies detection rules or machine learning models, and flags potentially suspicious activity for human review or automated action.

- AI fraud detection works by training statistical models on historical transaction data to identify patterns associated with confirmed fraud.

- False positives are the largest operational cost most compliance teams do not fully quantify.

- Real-time fraud detection refers to systems that evaluate a transaction before it settles, typically within 50-200 milliseconds for card payments and within a few seconds for ACH or wire transfers.

- Transaction monitoring cost varies significantly depending on deployment model, transaction volume, and feature scope.

Onboard Customers in Seconds

Conclusion

The right transaction monitoring software in 2026 is the one that matches your primary use case, delivers honest false positive rates in production, and fits your team's actual capacity. Whether you evaluate Sardine, Unit21, or an agentic AI alternative, push every vendor on four things: their real-world false positive rate, latency at your transaction volume, implementation timeline and full cost, and regulatory documentation. Moving from legacy rules to automated transaction monitoring that genuinely learns from your data is one of the few compliance investments with a direct and measurable return. Organizations that cut fraud alert fatigue through AI-assisted triage five years ago are spending a fraction of what their peers spend on analyst headcount today. Start with your use case, demand production benchmarks, and build in time for proper model tuning before declaring go-live.

Share this article