.webp)

Introduction

A unified risk platform in financial services is no longer a theoretical architecture discussion. It is the operational response to a threat environment where fraud, compliance, and identity attacks land on the same transaction simultaneously, and regulators expect an audit trail tying every automated decision to a specific model version, input feature set, and human oversight checkpoint.

Most financial institutions arrived at their current technology stack incrementally: a fraud tool here, a KYC provider there, an AML screening engine added after the next regulatory examination. The result is an architecture that worked when these problems were separate but struggles when attackers exploit the seams between them. This post examines the structural case for platform consolidation, the explainability requirements that accompany AI deployment in finance, and how multi-agent systems are changing what risk operations can accomplish in real time.

- What Is a Unified Risk Platform in Financial Services?

- Point Solutions vs Unified Risk Platform: The True Operational Cost

- How Explainable AI Finance Changes the Compliance Conversation

- XAI Fraud Detection, Compliance, and Identity: Why Separation Fails

- Configurable AI Autonomy: Human in the Loop AI Banking

Onboard Customers in Seconds

What Is a Unified Risk Platform in Financial Services?

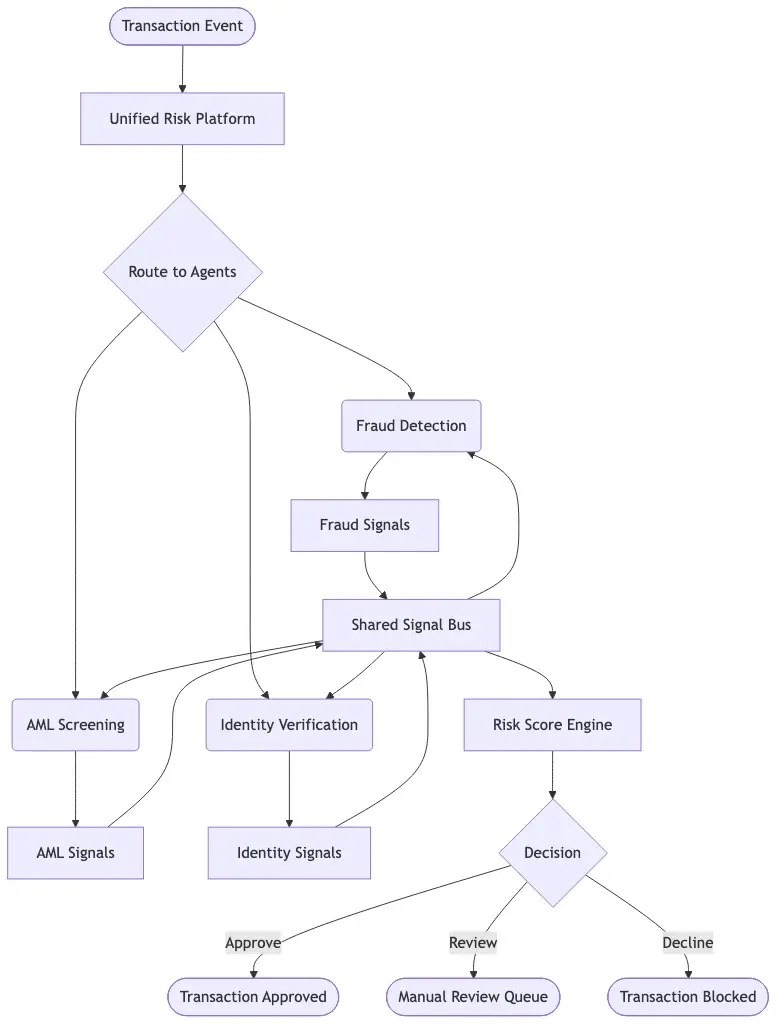

A unified risk platform is a single system that covers fraud detection, compliance monitoring, identity verification, and AI-driven security operations under one data model, one audit trail, and one governance framework. The key distinction is unified rather than integrated. Integration means connecting separate tools through APIs. A unified platform means those domains share state natively: a fraud signal updates the risk profile the AML engine reads, and identity verification results feed the behavioral baseline without a middleware hop.

The operational difference is latency and context completeness. When a transaction arrives, a unified platform evaluates fraud risk, compliance status, and identity confidence in a single orchestrated pass. Separate tools evaluate each dimension independently but cannot let one domain's output change how another domain scores the same event.

How a Unified Platform Differs from a SIEM

A SIEM collects logs and generates alerts. A unified risk platform acts on those signals. The difference matters operationally: a platform can autonomously decline a transaction, flag an account for review, or escalate to a human investigator within milliseconds, while a SIEM produces a dashboard entry requiring human action. For financial institutions processing thousands of transactions per minute, that latency gap is the difference between catching fraud and logging it after the fact.

What Belongs on a Unified Platform

The scope of a mature unified risk platform typically covers:

- Fraud detection: real-time transaction scoring, behavioral biometrics, device intelligence

- AML/KYC compliance: sanctions screening, beneficial ownership verification, ongoing monitoring

- Identity verification: document authentication, liveness detection, synthetic identity detection

- Explainable AI outputs: feature attribution reports, decision audit logs, regulator-ready documentation

Point Solutions vs Unified Risk Platform: The True Operational Cost

The point solutions vs platform financial services decision is not primarily a licensing cost question. It is an engineering capacity question and a regulatory exposure question. The average mid-size bank today runs 8 to 12 separate vendor contracts covering fraud, AML, KYC, device risk, behavioral analytics, and case management. Each vendor has its own API schema, its own alert thresholds, and its own data format. When a synthetic identity slips through because the fraud tool and the KYC tool are not sharing signals in real time, no single vendor is accountable.

That gap between tools is not a configuration problem. It is an architectural one. The gaps between point solutions become attack surfaces because attackers understand that coordinated fraud exploits exactly the domain boundaries that siloed systems cannot see.

The Integration Tax

Every point solution integration carries a hidden operational cost. Engineering teams at financial institutions spend 20 to 30 percent of their capacity on integration maintenance: schema changes from vendor API updates, version compatibility work, token management, and recovery from vendor outages. That is capacity not spent on detection logic, model improvement, or handling regulatory change requests.

Engineering teams at financial institutions spend 20 to 30 percent of their capacity on integration maintenance: schema changes from vendor API updates, version compatibility work, token management, and recovery from vendor outages.

Vendor consolidation in fintech is not primarily about reducing contract spend, though that matters. It is about eliminating the integration tax and redirecting engineering effort toward actual risk intelligence rather than plumbing.

Alert Fatigue and the False Positive Problem

When fraud, compliance, and identity tools each generate independent alerts with no shared context, analysts routinely see the same transaction flagged three times across three dashboards, each with a different severity rating and no clear way to reconcile them. Agentic AI platforms designed to reduce false positives demonstrate how cross-domain signal sharing can cut alert noise by 60 to 80 percent compared to isolated point solution stacks, giving analysts higher-quality queues rather than higher volumes.

Agentic AI platforms designed to reduce false positives demonstrate how cross-domain signal sharing can cut alert noise by 60 to 80 percent compared to isolated point solution stacks, giving analysts higher-quality queues rather than higher volumes.

How Explainable AI Finance Changes the Compliance Conversation

Regulators in the EU, UK, and US have moved beyond asking whether an AI system works. They now ask whether a human can understand and override it. That is the explainable AI finance requirement in practice, and it is where most point solution stacks fall apart most visibly.

When a fraud model flags a transaction and the compliance team needs to explain that decision during a regulatory examination, they need a coherent audit trail: what data the model used, what weight it assigned to each feature, and what the alternative outcome would have been if one input changed. If the fraud model is from Vendor A, the compliance data is from Vendor B, and the identity check is from Vendor C, assembling that narrative takes days of work across three support teams, three documentation formats, and three legal review cycles.

Explainable AI compliance is not a product feature. It is a regulatory requirement with enforcement teeth. The European Commission's AI regulatory framework classifies credit scoring and fraud detection as high-risk AI applications requiring detailed model logic documentation, ongoing human oversight mechanisms, and audit logs retained for defined periods.

Black Box AI Compliance Risk

Black box AI compliance risk is a formal enforcement concern under current and upcoming regulations. An institution running undocumented black box models in fraud detection or credit decisions faces not just reputational risk but direct regulatory action. The EU AI Act requires financial institutions to maintain technical documentation explaining how high-risk AI systems reach decisions, including the logic, data inputs, and accuracy metrics over time. Most point solution vendors treat model internals as proprietary, which creates a structural conflict with this documentation requirement.

A unified risk platform resolves this because the platform operator controls the model documentation, not a third-party vendor. Every model version, every retraining event, and every threshold change is captured in the platform's audit log under the institution's own governance framework.

SHAP Values Explained for Regulators

SHAP values explained for regulators means converting model mathematics into a readable decision summary that a non-technical examiner can evaluate. SHAP (SHapley Additive exPlanations) attributes each prediction to specific input features. In a fraud context, a SHAP summary might show that an unusual merchant category contributed 38 percent, the transaction time contributed 24 percent, and first use of a new device contributed 19 percent to the decline decision.

In a fraud context, a SHAP summary might show that an unusual merchant category contributed 38 percent, the transaction time contributed 24 percent, and first use of a new device contributed 19 percent to the decline decision.

Regulators need to verify that feature weighting reflects defensible business logic rather than a protected characteristic. A unified risk platform generates this narrative automatically as part of every high-risk decision. Building equivalent documentation on top of a point solution typically requires custom engineering that the vendor does not support.

AI Model Explainability for Regulators: A Practical Checklist

AI model explainability for regulators in financial services requires at minimum:

- Every AI decision traceable to specific, named input features

- Feature weights documented and version-controlled by model iteration

- Override authority assigned to a named human role with access logging

- Model drift detection with triggered re-review rather than silent adaptation

- Audit logs exportable in a regulator-readable format without vendor involvement

For institutions managing multiple compliance frameworks simultaneously, regulatory compliance automation reduces the manual burden of maintaining this documentation across jurisdictions.

XAI Fraud Detection, Compliance, and Identity: Why Separation Fails

The fraud compliance identity platform model exists because fraud, compliance, and identity are not separate risk domains. They are three views of the same transaction event, and separating them in software creates the blind spots that sophisticated attackers target.

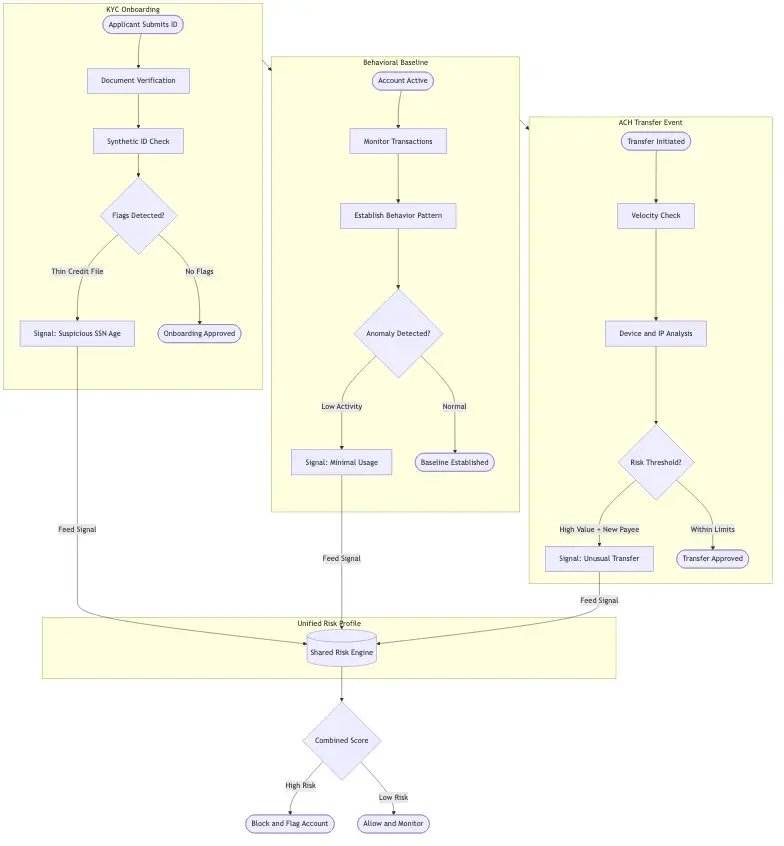

Consider a common synthetic identity attack: the attacker passes KYC onboarding because the documents are valid and the selfie matches a constructed identity. The same account builds a transaction history over 60 to 90 days to establish a behavioral baseline, then initiates a large ACH transfer to a mule network. At which point did this become a fraud problem, an identity problem, or an AML problem? All three simultaneously. A point solution stack detects it late or not at all because each tool sees only its assigned domain.

XAI fraud detection addresses this by providing both the detection capability and the explanation of why detection fired, which allows the compliance team to act on the finding and document it for regulatory purposes.

AI Agent Fraud Detection in Practice

AI agent fraud detection means deploying autonomous decision agents that query multiple data sources, apply multiple rule sets, and execute multi-step investigation workflows without requiring human input at every step. A fraud agent working within a unified risk platform might check device fingerprint, transaction velocity, behavioral biometrics, sanctions list status, and peer network comparison in a single orchestrated workflow completing in under 200 milliseconds.

This goes substantially beyond what rule-based systems can do. As AI-powered card fraud analytics demonstrates, the agent does not just score a transaction: it investigates it, gathering corroborating signals across domains before making a decision, which is how it reduces both false positives and missed fraud simultaneously.

The Identity Layer in Fraud Operations

Identity verification and fraud detection are now operationally inseparable. Synthetic identity fraud, where attackers construct plausible but fictitious identities from fragments of real data, accounts for a growing share of financial losses across banking, lending, and insurance. Detecting synthetic identity fraud in real time requires cross-referencing identity signals against behavioral patterns, device data, and network graph relationships. That cross-referencing is only practical when identity and fraud share a common data model, which is the core architectural argument for a unified risk platform in financial services.

Configurable AI Autonomy: Human in the Loop AI Banking

Not every risk decision should be fully automated, and institutions that have tried to automate everything have learned this when edge case model errors cascade into regulatory findings. The question is not whether to use AI autonomy but where to apply it and at what decision threshold.

Configurable AI autonomy means the system applies the right level of automation at each decision tier based on risk level, confidence score, and regulatory requirement. Human in the loop AI banking means the system knows when to decide autonomously and when to pause and require a human review step before proceeding.

Defining Autonomy Tiers

A practical autonomy framework for a unified risk platform in financial services looks like this:

| Decision Tier | Autonomy Level | Example Scenario |

|---|---|---|

| Low risk, high confidence | Full automation | Routine card purchase, consistent device and location |

| Medium risk, moderate confidence | Auto-flag, analyst review within 2 hours | Unusual merchant category, within historical transaction range |

| High risk, any confidence level | Human approval required before execution | Large wire to new beneficiary country |

| Sanctions match, any amount | Human review and legal sign-off required | Any OFAC or UN watchlist hit |

The platform enforces these tiers programmatically. Analysts work within the structure rather than overriding it case by case, giving compliance teams a defensible record that human judgment was applied at appropriate decision points.

AI Audit Trail Automation

AI audit trail automation is the operational backbone of a compliant AI deployment. Every autonomous decision, every escalation, every human override, and every model version change must be logged with timestamp, agent identifier, model version, input data hash, and outcome. On a fragmented point solution stack, assembling this trail for a regulatory inquiry takes hours or days across multiple vendor support teams.

On a unified risk platform, the complete audit trail is a single query. That is not just an efficiency argument. It is the difference between being able to demonstrate compliance and being unable to. The NIST AI Risk Management Framework provides the governance structure for logging, monitoring, and reviewing AI system decisions in high-stakes environments, and a unified platform architecture makes implementation materially simpler.

Building an AI Security Operations Platform for Financial Institutions

An AI security operations platform in a financial services context coordinates response across fraud, compliance, identity, and access control using a multi-agent AI system where each agent handles a specific domain while sharing context through a common orchestration layer.

The multi-agent architecture solves a real specialization problem: no single model can be simultaneously optimal for real-time transaction fraud, batch AML screening, document authentication, and API abuse detection. These domains require different algorithms, different latency tolerances, and different data sources. A multi-agent AI system lets each agent specialize while the orchestration layer ensures they inform each other rather than operating in parallel isolation.

Multi-Agent AI System Architecture

A typical multi-agent AI system for a financial services risk platform includes:

- Transaction fraud agent: real-time scoring, sub-100ms decision latency, behavioral pattern matching

- AML and sanctions agent: batch and event-triggered screening against regulatory rule sets and watchlists

- Identity verification agent: document authentication, biometric liveness detection, network graph relationship checks

- API security agent: rate limit enforcement, credential abuse detection, coordinated attack pattern recognition

- Orchestration layer: routes events to relevant agents, aggregates signals, manages escalation tiers, and generates the unified audit log

The orchestration layer is where the platform model proves its value over a collection of point solutions. A coordinated account takeover might involve an API credential probe, a device change, and a transaction from a new location, each falling below individual detection thresholds. The orchestration layer sees the combination and escalates. No individual point solution can see that pattern because each tool has visibility into only its own data stream.

API security strategies for CISOs in banking covers how the orchestration layer detects coordinated API abuse that individual rate limiters miss.

AI Agents in Financial Services: Deployment Considerations

AI agents in financial services need operational guardrails that do not apply in less regulated sectors. Financial regulations require human accountability for specific decision categories regardless of AI accuracy. Agents must operate within defined authority limits documented in the institution's model governance framework, log every action in an immutable audit record, and support real-time audit access by compliance teams without requiring vendor involvement.

This is also where vendor consolidation fintech becomes a governance argument rather than just an efficiency one. When AI agents run on a platform the institution controls, the institution owns the governance documentation. When agents run as third-party black boxes, the institution depends on vendor cooperation for every regulatory inquiry.

When Vendor Consolidation Fintech Makes Sense (and When It Does Not)

Vendor consolidation in fintech is not a universal prescription. Smaller institutions with a narrow product line, a well-integrated existing stack, and stable regulatory scope may not see enough benefit to justify platform migration disruption. The case for consolidation gets stronger as operational complexity grows.

The tipping points that typically prompt the evaluation:

- More than five vendor contracts covering overlapping risk domains with no shared data model

- More than 20 percent of engineering capacity spent on integration maintenance and vendor coordination

- Regulatory examination findings citing data inconsistency or inadequate audit trails across systems

- A fraud loss event where the attacker exploited a detection gap at the boundary between two point solutions

Research from the Bank for International Settlements documents how operational complexity in financial institution technology stacks correlates with systemic risk exposure and regulatory compliance burden, reinforcing the architectural case for consolidation once these thresholds are crossed.

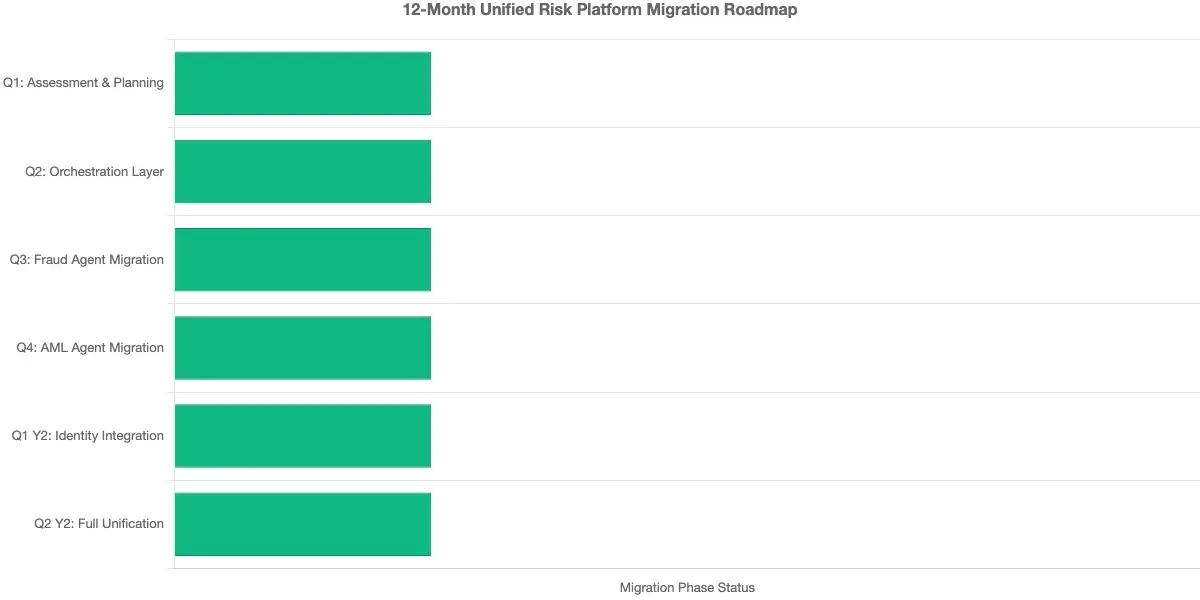

For institutions that reach these tipping points, migration sequencing matters as much as the destination. A phased approach, replacing one domain at a time while keeping others running, reduces disruption risk. The orchestration layer typically deploys first, giving the institution a coordination backbone. Then domain agents migrate one by one, with existing point solutions continuing to feed the orchestration layer during the transition.

- A unified risk platform is a single system that covers fraud detection, compliance monitoring, identity verification, and AI-driven security operations under one data model, one audit trail, and one governance framework.

- The point solutions vs platform financial services decision is not primarily a licensing cost question.

- Regulators in the EU, UK, and US have moved beyond asking whether an AI system works.

- The fraud compliance identity platform model exists because fraud, compliance, and identity are not separate risk domains.

- Not every risk decision should be fully automated, and institutions that have tried to automate everything have learned this when edge case model errors cascade into regulatory findings.

Onboard Customers in Seconds

Conclusion

The case for a unified risk platform in financial services comes down to an operational reality: fraud, compliance, and identity are not separate problems, and treating them as separate technology domains creates gaps that attackers exploit and regulators penalize. Point solutions made sense when these functions were genuinely separate. They are not anymore.

The platform model offers four things that a fragmented stack structurally cannot provide. Shared context across risk domains so that one signal can change another domain's decision. Explainable AI compliance outputs satisfying regulatory requirements without custom engineering on top of vendor black boxes. Configurable autonomy tiers keeping humans accountable at the right decision points. And a single audit trail covering every automated and human action in a format compliance teams can use during an examination.

For CISOs and compliance officers managing fraud exposure, AML obligations, identity risk, and operational resilience requirements at the same time, the question is not whether to consolidate. It is how to sequence the migration to minimize disruption while building toward a unified risk platform that can keep pace with the threat and regulatory environment financial services operates in today.

Share this article