.webp)

Introduction

KYC CDD requirements for banks in 2026 are stricter, more technology-dependent, and harder to ignore than at any point in the past decade. If you run compliance at a bank, credit union, or fintech, you're dealing with pressure from multiple directions: FinCEN's evolving Customer Due Diligence rules, rising SAR filing volumes, and the EU AI Act's fresh reach into financial services technology. This guide breaks down exactly what's required, what's changed, and where most institutions are still falling short. We'll cover BSA/AML compliance basics, enhanced due diligence triggers, KYC automation options, and what community banks specifically need to watch. No regulatory jargon where plain English works.

- What Are KYC CDD Requirements and Why Do They Matter in 2026?

- The BSA/AML Compliance Checklist Every Bank Needs

- KYC CDD Requirements for Community Banks: A Different Set of Challenges

- SAR Filing and CTR Filing Rules: What You Need to Know for 2026

- KYC Automation in 2026: What Technology Actually Delivers

Onboard Customers in Seconds

What Are KYC CDD Requirements and Why Do They Matter in 2026?

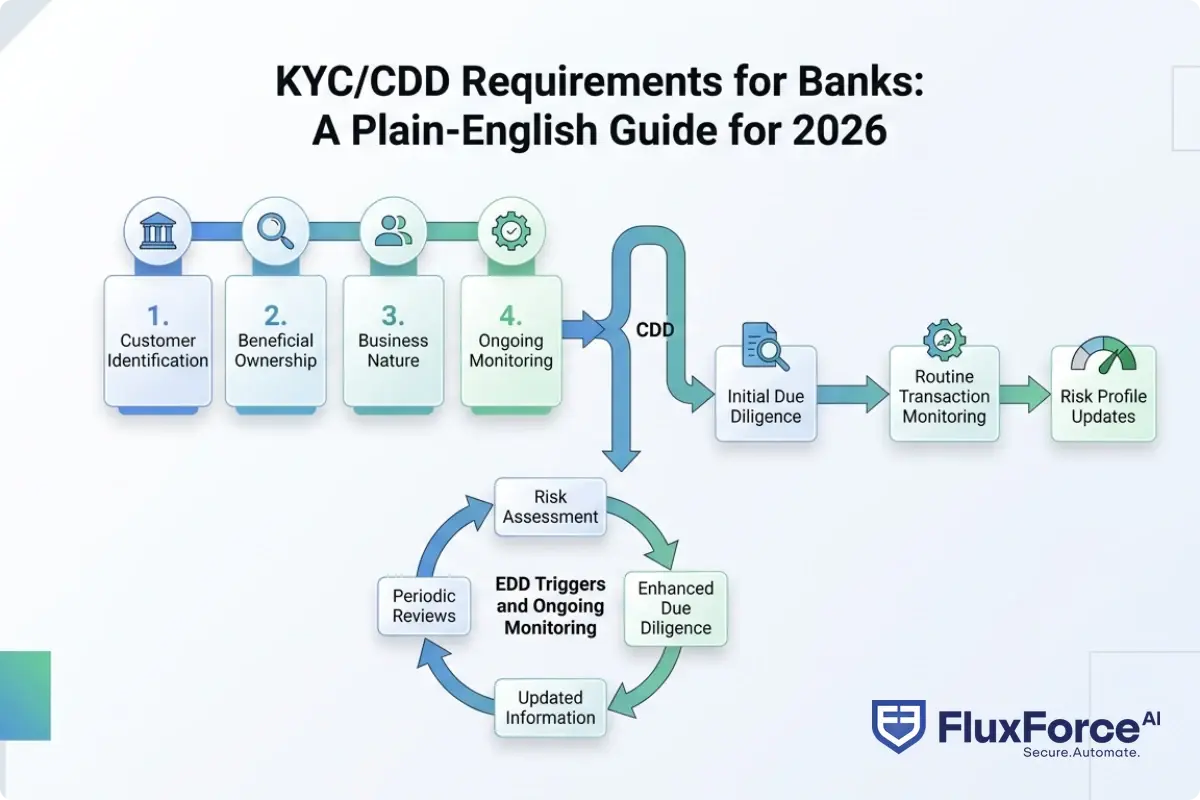

KYC (Know Your Customer) and CDD (Customer Due Diligence) requirements are the set of identity verification and ongoing monitoring obligations that banks must fulfill to detect and prevent money laundering, terrorist financing, and financial crime. In the US, these requirements primarily flow from the Bank Secrecy Act (BSA) and FinCEN's 2016 CDD Final Rule, which added a fourth pillar: beneficial ownership identification.

In 2026, the pressure has increased. The Anti-Money Laundering Act of 2020 (AMLA 2020) is now fully in effect, bringing new whistleblower protections, updated SAR reporting standards, and a requirement for FinCEN to publish national AML/CFT priorities annually. The most recent priority list includes virtual asset risks, ransomware proceeds, and trade-based money laundering, all of which affect how banks should structure their risk models.

The Four Pillars of CDD Under the BSA/AML Framework

FinCEN's CDD Final Rule established four core requirements that every covered financial institution must maintain:

- Customer identification and verification - Collect and verify name, date of birth, address, and identification number at account opening

- Beneficial ownership identification - Identify natural persons who own 25% or more of a legal entity, plus one control person

- Ongoing monitoring - Watch for unusual or suspicious activity against the customer's expected transaction profile

- Understanding the customer relationship - Develop a risk profile for each customer to make monitoring meaningful

The honest answer is that most banks handle items 1 and 2 reasonably well. Items 3 and 4 are where the gaps live, and where examiners are focusing attention in 2026.

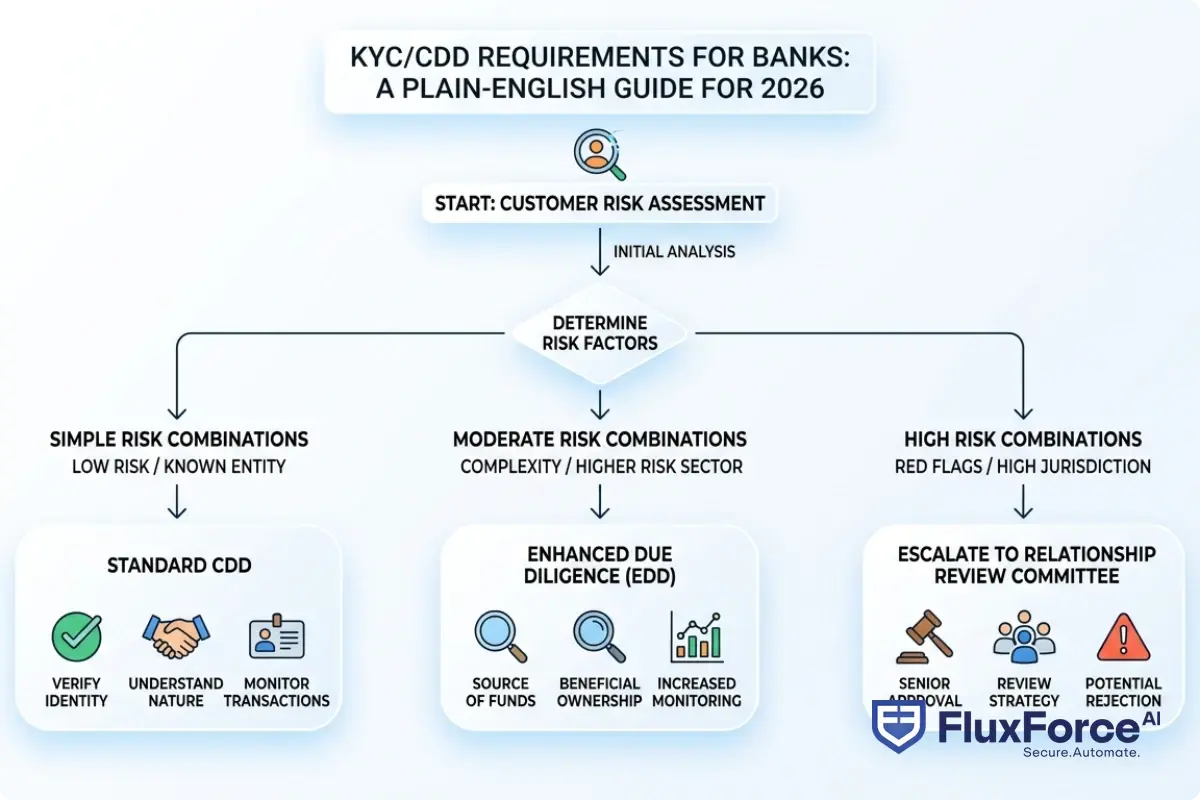

How CDD Differs From Enhanced Due Diligence

Standard CDD applies to most customers. Enhanced due diligence (EDD) kicks in when a customer or transaction presents higher risk. The difference is not just paperwork depth but ongoing monitoring frequency and the sources of information you're required to consult. We cover EDD triggers in detail later in this guide.

The BSA/AML Compliance Checklist Every Bank Needs

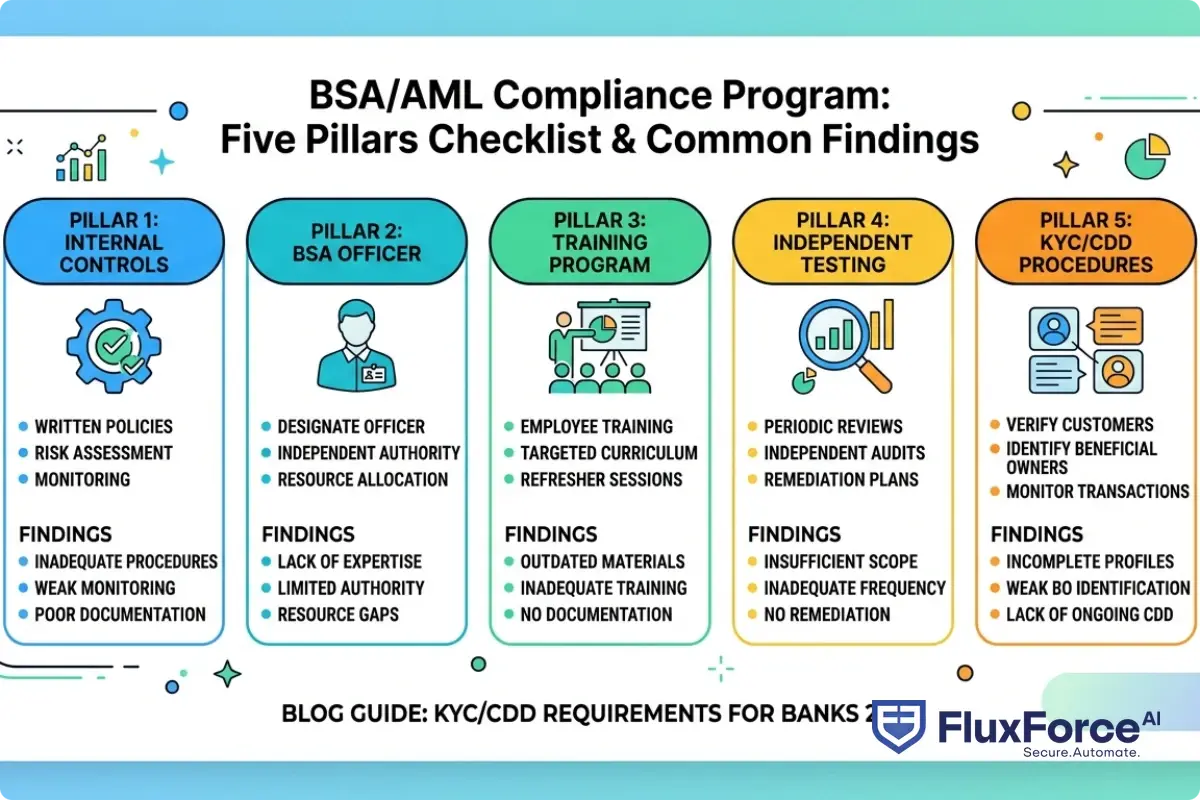

A practical bsa aml compliance checklist covers more than the four CDD pillars. It includes program documentation, training, independent testing, and a designated BSA Officer. The Bank Secrecy Act requires covered institutions to maintain a written AML program reasonably designed to prevent the institution from being used for money laundering or terrorist financing.

Here's a working checklist for compliance teams:

Program Foundations:

- Written AML policy approved by senior management or the board

- Designated BSA Compliance Officer with appropriate authority

- Risk-based customer due diligence procedures

- Employee training at onboarding and annually thereafter

- Independent testing (internal audit or third party) at least annually

Customer Onboarding:

- Customer Identification Program (CIP) procedures documented

- Beneficial ownership certification for legal entity customers

- Risk scoring assigned at account opening

- Screening against OFAC and other sanctions lists

Ongoing Monitoring:

- Transaction monitoring system with tuned rules or ML models

- Procedures for reviewing alerts and escalating to SAR review

- Periodic customer risk re-assessment schedule

- Process for handling high-risk customer relationships

Reporting:

- CTR filing for transactions over $10,000 in cash

- SAR filing within 30 days of identifying suspicious activity (60 days if no suspect is identified)

- Recordkeeping for five years on most BSA-related documents

Missing any of these doesn't just create exam findings. FinCEN civil money penalties for BSA violations have reached over $3 billion in aggregate in recent years, with individual institution fines exceeding $100 million for systemic failures.

FinCEN civil money penalties for BSA violations have reached over $3 billion in aggregate in recent years, with individual institution fines exceeding $100 million for systemic failures.

What Examiners Are Actually Looking For in 2026

The OCC, FDIC, and Federal Reserve have all published updated examination procedures aligned with AMLA 2020. Examiners are specifically focused on whether banks have updated their risk assessments to reflect FinCEN's national AML/CFT priorities, whether transaction monitoring systems are being properly validated, and whether SAR quality (not just quantity) has improved.

KYC CDD Requirements for Community Banks: A Different Set of Challenges

BSA/AML compliance for community banks presents specific constraints that the regulatory guidance doesn't always account for. A $500 million community bank has the same core compliance obligations as a $500 billion institution, but with a compliance team that might be two or three people rather than two or three hundred.

A $500 million community bank has the same core compliance obligations as a $500 billion institution, but with a compliance team that might be two or three people rather than two or three hundred.

The bsa aml compliance community banks conversation often comes down to resource allocation. Where should a small team spend its time? The answer, from both an exam perspective and a risk management perspective, is: proportionate to your actual risk.

Risk-Based Approach for Smaller Institutions

Community banks typically have lower-risk customer bases. Most customers are local businesses and individuals with straightforward transaction patterns. This means the risk assessment process, done correctly, should result in a leaner monitoring program, not the same scope as a correspondent banking operation.

Practical steps for community banks:

- Document your risk assessment thoroughly. If examiners understand why your monitoring thresholds are set where they are, findings drop significantly.

- Review your customer risk segmentation annually. A customer rated low risk at onboarding may have changed their activity profile.

- Use your core banking system's built-in transaction monitoring before investing in separate AML software. Many community banks already run systems that flag CTR-eligible transactions and include basic suspicious activity detection.

- Partner with your state bankers association. Many offer shared BSA training resources and model policies that smaller institutions can adapt.

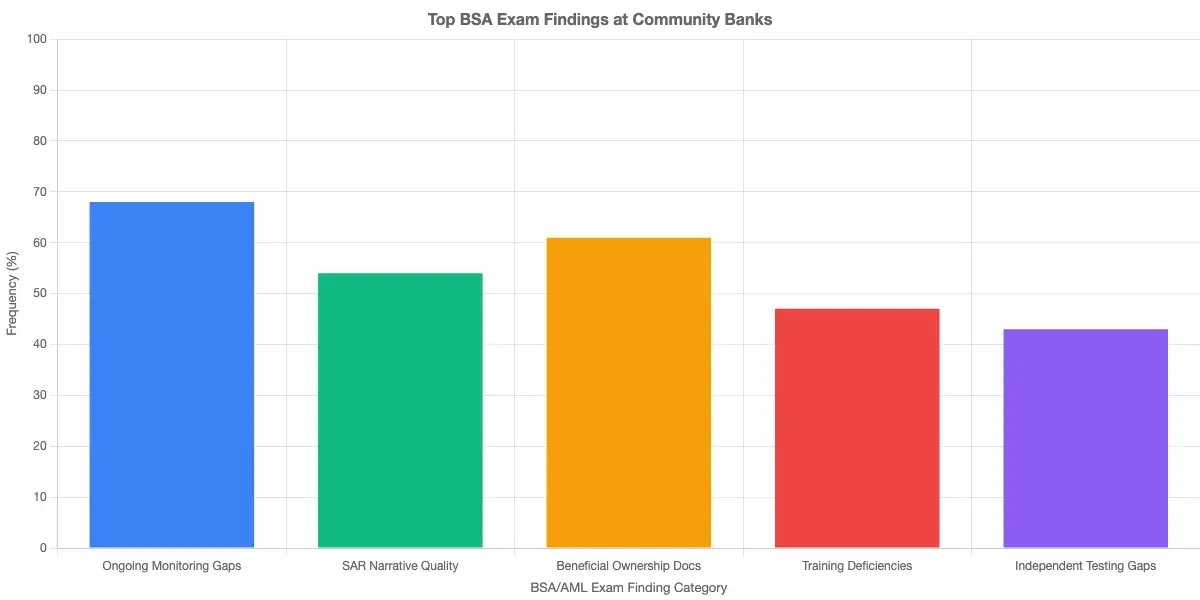

Where Community Banks Are Getting Cited

The most common exam findings for community banks right now are not in onboarding procedures. They're in ongoing monitoring: specifically, customers whose activity has changed materially but whose risk rating hasn't been updated. The second most common is SAR quality, particularly vague narratives that don't give FinCEN enough actionable detail.

If you're running compliance at a community bank with a limited budget, these two areas give you the highest return on compliance effort.

SAR Filing and CTR Filing Rules: What You Need to Know for 2026

SAR filing efficiency has become a focus area because FinCEN's feedback to the industry has been consistent: the agency receives too many low-quality SARs and not enough high-quality ones. Think of sar filing best practices as your suspicious activity report guide for examinations: the narrative section is where most banks lose examiner confidence, and where a few process changes pay off quickly.

SAR Filing Best Practices

The FinCEN SAR Activity Review consistently identifies what makes a SAR useful versus noise. Based on that guidance and examiner feedback, here's what separates strong SAR programs from weak ones:

Narrative quality:

- Identify who, what, when, where, and why in the first paragraph

- Quantify the suspicious activity: total amounts, number of transactions, date range

- Explain the expected activity based on the customer's profile and why this deviates from it

- Avoid conclusory language ("appears to be structuring") without factual support

Process controls:

- Have a SAR committee or designated reviewer for all SAR decisions, including decisions not to file

- Document your decision not to file just as carefully as decisions to file

- SAR filing requirements 2026 guidance from FinCEN discourages defensive filing without genuine suspicion

- Track your SAR metrics: alerts generated, alerts reviewed, alerts escalated, SARs filed

Filing timelines:

- The 30-day clock starts when you identify the suspicious activity, not when you finish investigating it

- Use the 60-day extension only when you genuinely have no subject identified, not as a buffer for late processing

CTR Filing Rules: Straightforward But Often Misapplied

CTR filing rules are simpler than SAR rules but still generate findings. The most common issues are structuring detection (customers breaking transactions to avoid the $10,000 threshold), failing to aggregate multiple same-day transactions by the same customer, and CTR exemptions that haven't been reviewed in years.

The most common issues are structuring detection (customers breaking transactions to avoid the $10,000 threshold), failing to aggregate multiple same-day transactions by the same customer, and CTR exemptions that haven't been reviewed in years.

Phase I exemptions (banks and government entities) are permanent. Phase II exemptions (businesses and payroll customers) must be reviewed annually and renewed. Many banks have exemption lists untouched for three to five years, which creates an exam finding that's easy to avoid with a simple annual review process.

For more on how automation can improve transaction monitoring and reduce false positive alert volumes, see our analysis of how agentic AI fraud agents can cut false positives by 80%.

KYC Automation in 2026: What Technology Actually Delivers

KYC automation 2026 is not a single product category. It spans identity document verification at onboarding, ongoing name screening against sanctions and PEP lists, transaction monitoring, and SAR drafting assistance. The key question for any compliance team is not "should we automate" but "which parts of our process have the highest error rate or the highest labor cost."

AML Compliance Software: Features That Matter

When evaluating aml compliance software, the features that drive real efficiency gains are:

- Case management with audit trail. Every alert, every disposition decision, every note should be logged automatically. Examiners want to see the full decision history.

- Alert tuning controls. A monitoring system you can't tune without vendor involvement will always be either too noisy or too quiet. You need to adjust thresholds based on your actual customer base.

- Integrated screening. OFAC screening, PEP screening, and adverse media checks that run at onboarding and on a scheduled basis, without manual re-upload of customer lists.

- SAR workflow tools. Features that pull transaction data directly into a SAR draft, require supervisor approval, and track the 30-day filing deadline.

Anti money laundering technology 2026 has also expanded to include machine learning-based transaction monitoring, which reduces false positives compared to static rule-based systems. The tradeoff is explainability: ML models are harder to explain to examiners when an account gets flagged. Institutions that handle this best document their model validation processes carefully and can articulate why a given transaction pattern triggered a review.

Fintech BSA/AML Compliance With a Small Team

Fintech bsa aml small team compliance is its own challenge. Many fintechs operate as money services businesses or bank partners rather than directly chartered banks, but BSA obligations follow the activity, not the charter. A fintech processing payments has transaction monitoring obligations whether or not it holds a banking license.

The practical reality: a three-person compliance team at a growing fintech can handle BSA obligations if the workflows are automated correctly. The bottleneck is usually manual alert review. If your team is reviewing 200 alerts a week and filing 15 SARs, that's sustainable. If you're reviewing 2,000 alerts and filing 15 SARs, your system needs tuning, not more headcount.

For a detailed look at how aml compliance fintech operations differ from traditional bank compliance, see our deep dive on AML screening in digital lending.

The FATF recommendations on technology in AML compliance explicitly support risk-based use of automated tools for customer due diligence, provided institutions document their validation methodology.

Enhanced Due Diligence: When Standard CDD Isn't Enough

The enhanced due diligence guide starts with a single question: what makes a customer high risk? The answer depends on your institution's risk appetite and the actual risk factors present, but regulatory guidance provides a clear framework.

Triggers That Require EDD

Certain customer types and situations require enhanced scrutiny under both US and international AML frameworks:

- Politically Exposed Persons (PEPs): Foreign government officials and their close associates. US PEPs are not required to receive EDD under federal law, though many institutions apply it as a risk management choice.

- Correspondent banking relationships: Particularly cross-border arrangements, which carry high inherent risk for layering.

- Private banking: High-net-worth individuals with complex account structures.

- Jurisdictions of concern: Customers with connections to countries on FATF's grey or black list, or countries subject to FinCEN geographic targeting orders.

- Cash-intensive businesses: Restaurants, car washes, and convenience stores, where transaction patterns are harder to verify against stated business purpose.

- Customers subject to prior SARs: A customer who generated a SAR should be re-evaluated at that point.

AML Risk Assessment Guide for High-Risk Customers

A practical aml risk assessment guide for high-risk customers requires more than checking a box:

- Source of wealth verification: Where did the customer's assets come from? This is separate from source of funds (where did this specific deposit come from).

- Business purpose verification: For commercial customers, understand what the business actually does, not just what the SIC code says.

- Senior management sign-off: EDD relationships should require approval from a compliance officer or business line senior manager, documented in the file.

- More frequent review: High-risk customers should be re-reviewed at least annually, with transaction monitoring thresholds set lower than standard.

- Relationship exit criteria: Know in advance what activity would cause you to close the relationship. Having that threshold documented makes the exit decision easier when the time comes.

The eu ai act financial services provisions, which came into effect in 2025, add a layer for institutions using AI-assisted risk scoring. If your EDD decisions are informed by an AI model, you now have documentation and bias-testing obligations under EU law. Institutions serving EU customers should review their AI model governance frameworks against these requirements.

For institutions managing both AML and identity verification challenges across sectors, the approach in our AML risk checks and KYC strategy for compliance officers in insurance offers transferable frameworks.

Building a Compliant KYC Program: The Practical Steps

Moving from understanding KYC CDD requirements banks 2026 mandate to actually building a program that passes examination requires sequencing the work correctly. The most common mistake is buying technology before the underlying processes are documented.

The Right Sequence for Program Development

Start with your risk assessment. Everything else flows from it: which customers get EDD, what transaction monitoring thresholds make sense, how often you need to re-screen your customer base. The risk assessment isn't a one-time document; it should be updated when your product mix changes, when FinCEN publishes new priorities, and when you enter new markets.

Then document your procedures. A risk assessment without procedures is an exam finding. The procedures don't need to be 200 pages; they need to cover every step in the process from onboarding through account closure, with enough specificity that a new BSA analyst could execute them without calling the BSA Officer every five minutes.

Technology comes after process. The best aml compliance software can't fix a broken process; it just breaks faster. Once your procedures are documented and tested manually, you can identify which steps are candidates for automation and which need human judgment.

What a Healthy Program Looks Like

A well-functioning KYC and AML program in 2026 shares a few observable characteristics:

- Alert rates are declining or stable, not rising year over year (rising alert rates indicate a tuning problem)

- SAR-to-alert ratios are tracked and within expected ranges for the institution's risk profile

- The BSA Officer has a direct reporting line to the board or a board committee

- Independent testing findings are addressed within defined remediation timelines

- Staff turnover in the compliance function is tracked, because high turnover correlates with program gaps

For institutions looking to apply similar discipline to API-layer security alongside their AML programs, our guide on API security strategies for CISOs in banking covers complementary controls. And if you're evaluating broader automation tradeoffs, our manual compliance vs. AI automation comparison offers a balanced view of where technology helps and where it creates new risks.

The OCC's BSA/AML examination procedures are publicly available and worth bookmarking. Reading what examiners are actually looking for clarifies compliance priorities faster than any conference presentation.

- KYC (Know Your Customer) and CDD (Customer Due Diligence) requirements are the set of identity verification and ongoing monitoring obligations that banks must fulfill to detect and prevent money laundering, terrorist financing, and financial crime.

- A practical bsa aml compliance checklist covers more than the four CDD pillars.

- BSA/AML compliance for community banks presents specific constraints that the regulatory guidance doesn't always account for.

- SAR filing efficiency has become a focus area because FinCEN's feedback to the industry has been consistent: the agency receives too many low-quality SARs and not enough high-quality ones.

- KYC automation 2026 is not a single product category.

Onboard Customers in Seconds

Conclusion

KYC CDD requirements for banks in 2026 are not fundamentally new, but the execution bar has risen. FinCEN wants better SAR quality. Examiners want documented risk assessments tied to actual monitoring program design. Regulators on both sides of the Atlantic are paying closer attention to how AI tools factor into compliance decisions.

The institutions that do this well aren't necessarily the ones with the biggest budgets. They're the ones with documented processes, honest risk assessments, and monitoring programs calibrated to their actual customer base rather than generic industry templates. If your program has those three things, you're in better shape than most.

If you're working through a specific gap, whether that's beneficial ownership documentation, SAR workflow efficiency, or transaction monitoring tuning, the starting point is always the same: document what you're doing now, identify where the gaps are, and fix the highest-risk gaps first. That's sound aml compliance practice regardless of what the regulatory calendar looks like.

Share this article