.webp)

Introduction

KYC automation 2026 is at an inflection point. Financial institutions face more pressure than ever to cut manual review costs, meet tighter regulatory deadlines, and accomplish both with teams that haven't grown proportionally to transaction volume. The promise is real: AI-assisted identity verification, automated aml compliance workflows, and intelligent sar filing tools that flag suspicious activity without drowning analysts in false alarms. The reality is more complicated. Some parts of the KYC stack automate brilliantly. Others are deceptively hard to get right. And a few vendor claims are not ready for production in a regulated environment.

This post breaks down what actually works in KYC automation, where the failure modes are, and which trends deserve genuine skepticism from compliance officers and CISOs alike.

- What Is KYC Automation and Why 2026 Is a Turning Point

- What Actually Works in KYC Automation Right Now

- The BSA/AML Compliance Checklist: What Can and Can't Be Automated

- SAR Filing and CTR Filing: Where Automation Makes the Biggest Difference

- What Doesn't Work: The Automation Failures No One Talks About

Onboard Customers in Seconds

What Is KYC Automation and Why 2026 Is a Turning Point

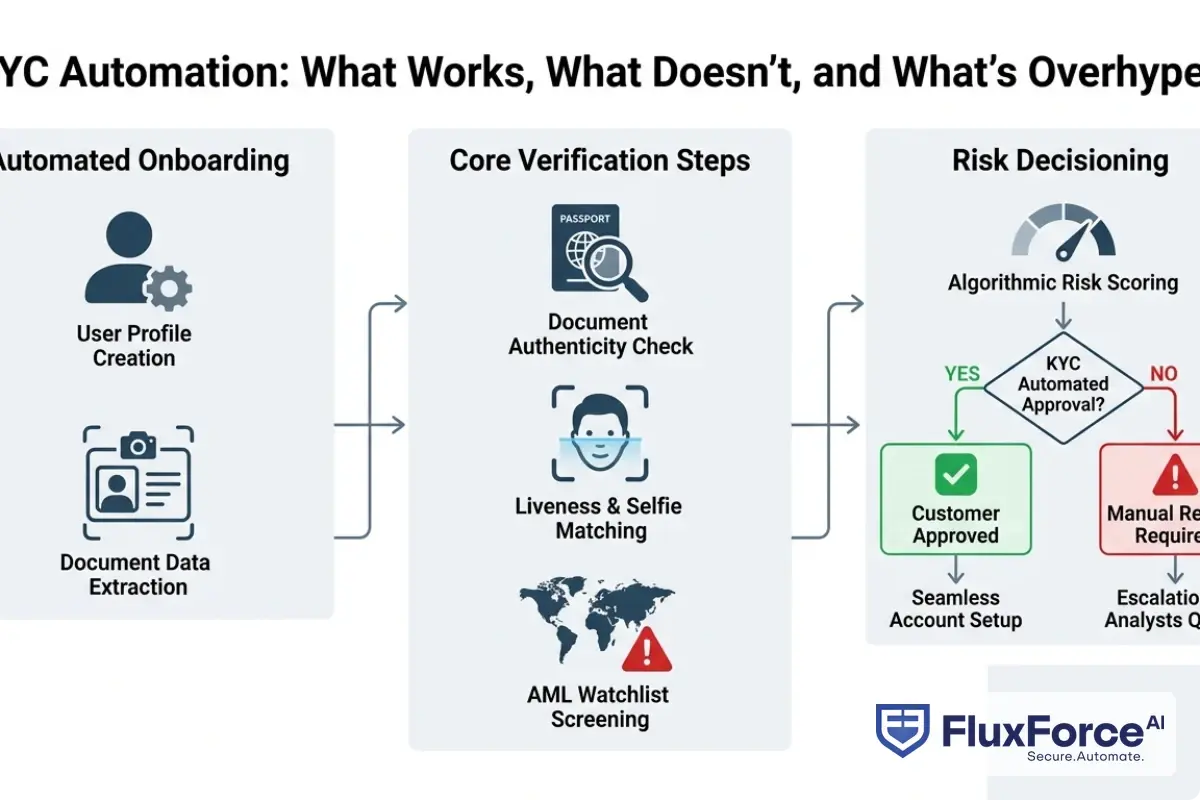

KYC automation is the use of technology, typically machine learning, rules engines, and API-connected data sources, to carry out Know Your Customer checks without manual analyst intervention. In practice, this covers identity document extraction, sanctions screening, risk scoring, and increasingly, ongoing monitoring of customer behavior for suspicious activity patterns.

2026 marks a shift because three things converged: regulatory bodies like FinCEN published updated guidance on the use of automated tools in BSA/AML programs; the EU AI Act's provisions for high-risk AI in financial services took effect for larger institutions; and a second wave of aml compliance fintech companies matured past the demo stage into enterprise-grade deployments.

The institutions that deployed automation in 2021-2022 now have three or more years of production data. That data tells a more nuanced story than the original vendor pitches.

The Case for Automating KYC Compliance

The economics are straightforward. A bank processing 50,000 new account applications per year, with manual KYC review averaging 12 minutes per application, spends roughly 10,000 analyst-hours on onboarding alone. Automation can cut that to 2-3 minutes of exception handling per case, saving around 8,000 hours annually, roughly the equivalent of four full-time compliance analysts.

Beyond cost, the consistency argument is strong. Manual reviewers produce inconsistent results across shifts and locations. Automated systems apply the same rule set at 2 AM on a Sunday as at 10 AM on a Monday, which matters significantly during regulatory exam preparation.

Where Manual KYC Still Gets Stuck

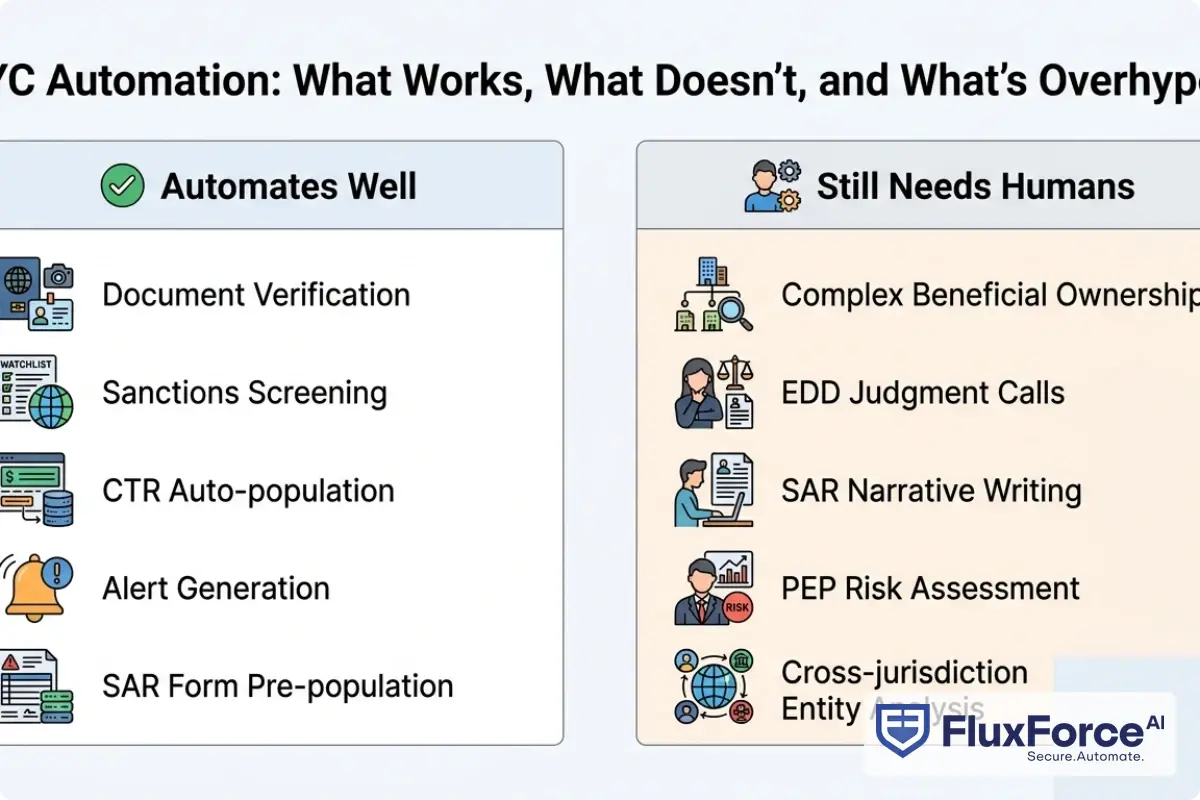

The bottlenecks automation hasn't fully solved concentrate in two areas: complex beneficial ownership structures and cases requiring contextual judgment. A sole trader with a straightforward identity document clears in seconds. A private equity fund with six layers of holding companies in three jurisdictions still requires a compliance analyst who understands corporate law, not just data matching.

That distinction matters when sizing your automation ROI. Most institutions can automate 60-75% of their KYC volume. The remaining 25-40% is where your experienced team earns its keep.

Most institutions can automate 60-75% of their KYC volume.

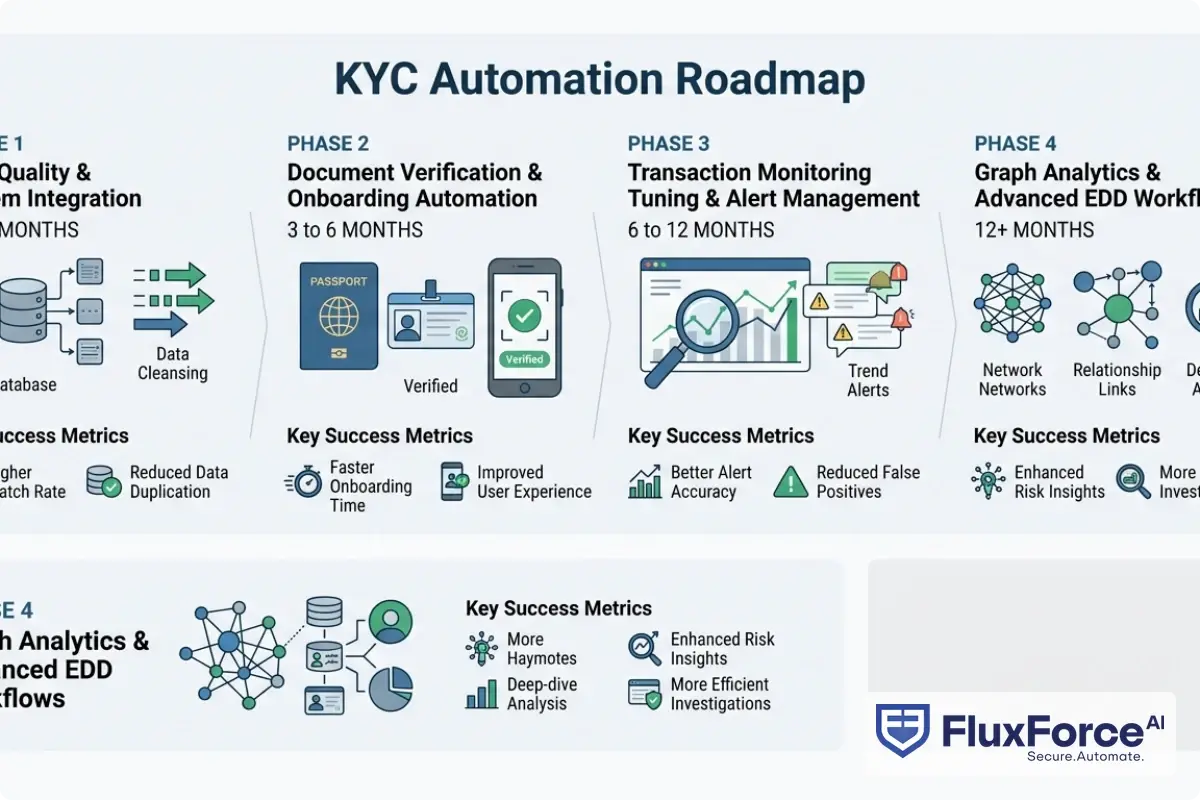

What Actually Works in KYC Automation Right Now

Document Verification and Identity Proofing

Optical character recognition paired with liveness detection is genuinely mature technology in 2026. Major providers now hit 99%+ accuracy on standard government-issued IDs in good lighting conditions. Liveness detection has gotten significantly harder to spoof since 2023, though deepfake countermeasures remain an ongoing arms race (more on that in the overhyped section).

For banks and fintechs with high-volume digital onboarding, document verification automation is the single highest-ROI change available today. A customer uploads their passport, the system extracts and validates the data in under 3 seconds, and a risk score is generated before the next screen loads.

AML Compliance Software That Delivers Real Results

The best aml compliance software in 2026 shares three traits: it integrates directly with your core banking or CRM system rather than via CSV exports, it maintains an auditable decision log that satisfies regulators, and it supports configurable rule tuning without requiring a vendor professional services engagement for every threshold change.

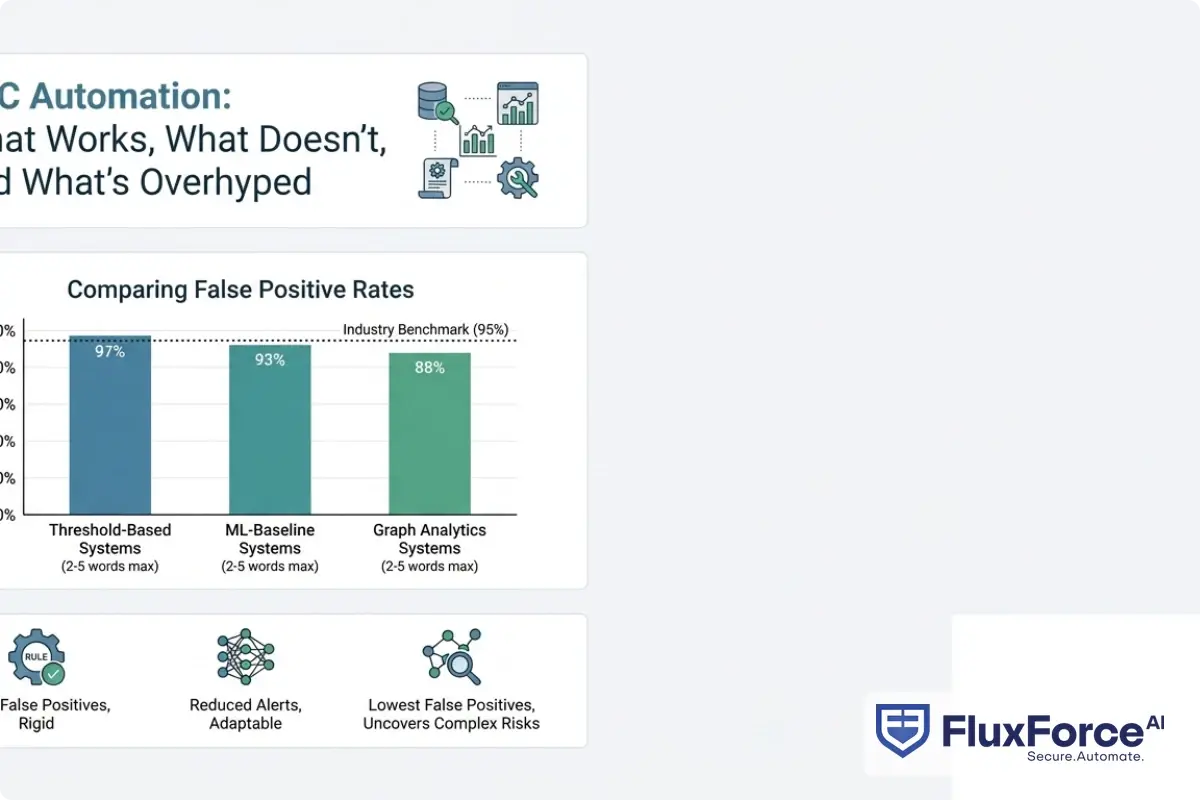

Transaction monitoring tools that use behavioral baselines rather than static thresholds have materially reduced false positive rates in production deployments. One regional bank documented a 43% reduction in false positive alerts after switching from a threshold-based system to a machine learning baseline model.

One regional bank documented a 43% reduction in false positive alerts after switching from a threshold-based system to a machine learning baseline model.

As analyzed in our post on how agentic AI fraud agents cut false positives by 80%, the difference between rule-based and adaptive systems compounds over time as the model learns your specific customer base.

How Anti Money Laundering Technology 2026 Has Matured

Anti money laundering technology in 2026 is increasingly centered on graph analytics: mapping relationships between accounts, beneficial owners, and transaction counterparties to detect network-level patterns that no single-account rule would catch. Shell company structures that exploit the weakness of account-level monitoring become far more visible when you map the full transaction graph.

The practical caveat is that graph analytics requires quality data. If your customer master data has duplicates, stale addresses, and inconsistent entity names, graph-based anti money laundering technology will produce as many false positives as it prevents. The technology is sound; the data quality dependency is where implementation projects frequently stall.

The BSA/AML Compliance Checklist: What Can and Can't Be Automated

For U.S.-regulated institutions, the bsa aml compliance checklist has five core pillars: internal controls, independent testing, a designated BSA officer, ongoing training, and customer due diligence. Of these, internal controls and CDD are the most automatable.

The FinCEN Customer Due Diligence Rule requires collecting and verifying the identity of beneficial owners who hold 25% or more of a legal entity. Automation handles the collection and initial verification well. The verification step gets messier when a beneficial owner has a common name, an address in a high-risk jurisdiction, or a thin credit file.

The FinCEN Customer Due Diligence Rule requires collecting and verifying the identity of beneficial owners who hold 25% or more of a legal entity.

BSA AML Compliance for Community Banks

BSA AML compliance for community banks hits differently than for large institutions. Community banks typically run with fewer than 10 compliance staff, limited IT budgets, and a customer base that includes local businesses with genuinely unusual but legitimate transaction patterns: seasonal agricultural payments or lumpy real estate transactions, for example.

Off-the-shelf aml compliance software often over-alerts on these patterns because it's trained on national transaction distributions. The better approach for community banks is to deploy a core monitoring tool, then invest significant time tuning alert parameters against your specific customer mix. That tuning phase takes 3-6 months to do properly, but it's what separates a system that works from one that generates 300 alerts a week that analysts learn to ignore.

For related guidance on building cost-effective compliance monitoring programs, see our analysis of AML screening strategy for payments risk officers.

Fintech BSA AML on a Small Team

Fintech BSA AML with a small team is genuinely hard. A fintech with three compliance staff, high transaction velocity, and a customer base that skews younger with irregular income patterns will not extract the same ROI from enterprise AML software as a large bank compliance department.

The honest recommendation: start with a managed service provider for transaction monitoring rather than a self-hosted platform. The operational burden of maintaining model thresholds, handling alert queues, and producing regulatory reports is substantial. A managed service puts first-line alert triage on a specialist team while your small staff handles escalations and filings. As you scale, you can bring more of that function in-house.

SAR Filing and CTR Filing: Where Automation Makes the Biggest Difference

Suspicious Activity Reports and Currency Transaction Reports are where sar filing efficiency directly translates to regulatory risk reduction. Missed SAR deadlines and incomplete CTR filings rank among the most common BSA examination findings, and they're also two of the most automatable compliance obligations.

SAR Filing Best Practices with Automated Workflows

SAR filing best practices in an automated environment start with the alert-to-case workflow. When a transaction monitoring system flags an alert, the case management system should automatically pre-populate SAR form fields it can determine: account numbers, transaction dates, amounts, and known counterparty data. The analyst's role shifts from data entry to narrative writing and judgment calls on borderline cases.

A well-configured case management system also tracks the 30-day SAR filing deadline from the date of detection and escalates automatically if a case ages without resolution. This alone eliminates the most common SAR compliance failure: cases that fall through the cracks during staff absences or high-volume periods.

SAR Filing Requirements 2026: What Changed

SAR filing requirements in 2026 include updated FinCEN guidance on reporting cyber-enabled financial crime, covering ransomware payments and business email compromise schemes. Filing deadlines remain unchanged at 30 days from detection, or 60 days for cases requiring additional investigation, but the narrative requirements for technology-facilitated fraud are now more specific than prior guidance.

The suspicious activity report guide from FinCEN specifies that cyber-related SARs must include the type of cyber event, any known IP addresses or malware indicators, and the affected systems. Automation can help populate known indicators from threat intelligence feeds, but the narrative context still requires human judgment to be complete and defensible under examination.

CTR Filing Rules and Auto-Population Accuracy

CTR filing rules require banks to file for cash transactions exceeding $10,000. The compliance failure mode isn't usually missing a transaction outright. It's structuring detection and accurate aggregation across multiple same-day transactions by the same customer. Modern kyc compliance software aggregates transactions in real time, flagging when a customer approaches or exceeds the threshold through multiple smaller transactions across a single business day.

The accuracy of auto-population in CTR workflows is high for transactions that clear within the same branch or system. It degrades when a customer conducts transactions across multiple branches or channels that don't share a real-time data feed. That's an IT integration problem, not an AI problem, and it's worth diagnosing before attributing failures to your monitoring vendor.

What Doesn't Work: The Automation Failures No One Talks About

False Positive Overload in AML Risk Assessment

The aml risk assessment guide reality: transaction monitoring systems generate too many alerts, and most compliance teams don't have the bandwidth to work them all rigorously. When alert queues back up, analysts make faster and less thorough decisions, which defeats the purpose of automated detection.

The industry benchmark for transaction monitoring false positive rates sits at roughly 95-99%, meaning only 1-5% of alerts result in a SAR filing. Some well-tuned systems reach 90%. In poorly configured deployments, the ratio gets worse: 99.5% false positives means an analyst reviews 200 alerts to find one that warrants a filing. Staff burnout from alert fatigue is a documented contributing factor in missed genuine suspicious activity.

KYC CDD Requirements Banks Still Struggle to Automate

KYC CDD requirements for banks include ongoing monitoring, which means the compliance obligation doesn't end at onboarding. Institutions need to refresh customer data periodically, especially for high-risk customers, and to flag when customer behavior changes materially from their onboarding profile.

Ongoing monitoring automation is where most KYC programs have significant gaps. Onboarding is well-automated. Periodic review largely is not. A bank that onboarded a customer in 2021 with a standard transaction profile should detect by now if that customer's risk profile has shifted. Many don't, because the periodic review workflow is still largely manual and dependent on relationship manager discretion.

For a fuller picture of how identity verification connects to ongoing compliance lifecycle management, our post on KYC/AML identity verification strategy for claims directors addresses similar challenges in the insurance context.

Enhanced Due Diligence Guide: Where AI Falls Short

The enhanced due diligence guide principle is that high-risk customers require deeper investigation: source of wealth documentation, source of funds verification, adverse media screening, and more frequent monitoring reviews. AI handles data collection and initial screening reasonably well. The judgment call (whether a politically exposed person's wealth is consistent with their role or something is materially off) still requires experienced human review.

AI-generated adverse media summaries in 2026 are genuinely useful. They aren't reliable enough to replace a compliance analyst who can read context, understand regional political dynamics, and make a risk-proportionate judgment without reflexively filing a defensive SAR on a legitimate customer.

What's Overhyped in KYC Compliance Software

The EU AI Act Financial Services Reality Check

The EU AI Act classifies AI systems used in AML and credit-risk assessment as high-risk applications. For financial institutions deploying AI-driven kyc compliance software in EU-regulated entities, this creates concrete obligations: documented model governance, explainability for automated decisions affecting customers, and regular bias testing against protected characteristics.

Many vendors marketing their systems as AI-powered haven't completed the compliance work to satisfy these requirements yet. Before deploying any AI-driven KYC tool in an EU-regulated entity, ask the vendor for their EU AI Act conformity documentation. If it doesn't exist, you're taking on regulatory exposure that may not surface until your next supervisory review.

Biometrics and Deepfake Detection: Promising but Overstated

The claim that current biometric liveness detection is deepfake-proof is not accurate. Sophisticated deepfakes can defeat some liveness detection systems, and the attack surface evolves faster than most vendors publicly acknowledge. Responsible vendors are transparent about known weaknesses and publish their countermeasure update cadence.

For institutions onboarding high-value customers or operating in jurisdictions with active synthetic identity fraud activity, biometric verification should be one layer in a multi-factor stack, not the sole control. For the full picture of how rapidly fraud attack methods evolve relative to detection, see our post on detecting synthetic identity fraud in real-time.

Building a Realistic KYC Automation Strategy for 2026

Institutions that extract the best results from KYC automation in 2026 share several practices. They automate the high-volume, low-judgment decisions first. They invest in data quality before layering on advanced analytics. They treat alert threshold tuning as an ongoing operational discipline rather than a one-time setup task. And they keep experienced compliance staff focused on complex cases where human judgment creates disproportionate value.

AML compliance fintech tools are materially stronger than they were three years ago. According to FATF guidance on digital identity, AI-assisted compliance tools can strengthen detection programs when implemented with appropriate governance frameworks. The question for most institutions isn't whether to automate. It's how to sequence the automation to build ROI without creating new compliance gaps in the process.

For teams evaluating platforms, the bsa aml compliance checklist is your validation framework. Does this tool support your internal controls program? Does it produce auditable outputs that hold up under examination? Does it integrate with your independent testing workflow? Any platform that can't satisfy all three isn't enterprise-ready. For more detail on how automation fits into regulatory reporting programs, see our post on banking compliance reporting for payments risk officers.

- KYC automation is the use of technology, typically machine learning, rules engines, and API-connected data sources, to carry out Know Your Customer checks without manual analyst intervention.

- Optical character recognition paired with liveness detection is genuinely mature technology in 2026.

- For U.S.-regulated institutions, the bsa aml compliance checklist has five core pillars: internal controls, independent testing, a designated BSA officer, ongoing training, and customer due diligence.

- Suspicious Activity Reports and Currency Transaction Reports are where sar filing efficiency directly translates to regulatory risk reduction.

- The aml risk assessment guide reality: transaction monitoring systems generate too many alerts, and most compliance teams don't have the bandwidth to work them all rigorously.

Onboard Customers in Seconds

Conclusion

KYC automation 2026 delivers measurable value in the right places: document verification, sanctions screening, CTR auto-population, and SAR workflow management top the list. The tradeoffs are equally real. Alert fatigue, data quality dependencies, and judgment gaps in complex enhanced due diligence scenarios mean automation is a force multiplier for compliance teams, not a substitute for them.

The institutions ahead in this space approached automation with clear expectations, invested in data quality before adding analytical sophistication, and kept their experienced aml compliance staff focused on the decisions that move the needle on regulatory outcomes. If you're building or rebuilding your KYC program for 2026, start with the highest-volume, most-automatable decisions and work systematically outward from there.

For a broader view of how agentic AI fits into compliance workflows today, explore our guide on how to roll out regulatory compliance agents in 90 days.

Share this article