.webp)

Listen To Our Podcast🎧

Introduction

AML compliance for fintechs in 2026 is no longer optional, secondary, or something you can "figure out later." Regulators have made it clear: if you move money, you must comply with anti-money laundering fintech requirements. No exceptions for being a startup. No exceptions for being "just a platform."

In 2025 alone, FinCEN levied $2.3 billion in penalties against financial services companies — and fintechs received a disproportionate share of enforcement actions. The message is unmistakable: the regulatory honeymoon for fintechs is over.

This guide breaks down everything you need to build a defensible, scalable fintech AML program — even if your compliance team is small and resource-constrained.

In this guide, you'll learn:

- The exact BSA/AML requirements that apply to fintechs

- How to build a risk-based AML program from scratch

- The 5 pillars of a defensible compliance program

- How to handle SAR filing, CDD, and transaction monitoring efficiently

- Technology strategies for small compliance teams

Does Your Fintech Need AML Compliance?

The short answer is almost certainly yes. If your fintech touches money in any way — payments, lending, deposits, transfers, crypto, or even stored value — you have AML obligations under federal and potentially state law.

Which Fintech Models Fall Under AML Requirements?

According to FinCEN, the following fintech business models are considered Money Services Businesses (MSBs) and must register and comply with BSA compliance for fintechs and broader AML regulations for fintechs in 2026:

Covered Business Models

- Payment processors and facilitators — processing payments on behalf of merchants or consumers

- Money transmitters — transferring funds from one person to another (including digital wallets)

- Neobanks — typically operating under a bank charter or bank partnership (the sponsor bank's BSA program applies, but you share responsibility)

- Lending platforms — originating loans directly or through partnerships

- Crypto/digital asset platforms — classified as money transmitters by FinCEN since 2013

- Stored value/prepaid card issuers — issuing or selling prepaid access

BaaS and Shared Compliance Responsibility

Key insight: Even if you're operating under a sponsor bank's charter, you are not exempt from AML obligations. FinCEN’s 2024 guidance made it explicit that fintechs in banking-as-a-service (BaaS) partnerships share compliance responsibility with their sponsor banks. The OCC has issued multiple enforcement actions against sponsor banks for inadequate oversight of their fintech partners.

"Partnering with a bank does not outsource your compliance obligations. It creates shared obligations." — FinCEN Advisory, 2024

AML Compliance for Fintechs in 2026: The Regulatory Framework

The Bank Secrecy Act (BSA) and its implementing regulations form the foundation of anti-money laundering fintech requirements in the United States. If you are building or operating a fintech in 2026, these are the specific requirements you need to meet:

Federal AML Requirements for Fintechs

|

Requirement |

What It Means |

Deadline |

|

FinCEN MSB Registration |

Register as a Money Services Business if you meet the definition |

Before commencing business |

|

BSA/AML Program |

Written, board-approved fintech AML program with the 5 pillars |

Before commencing business |

|

SAR Filing |

File Suspicious Activity Reports within 30 days of detection |

Ongoing |

|

CTR Filing |

File Currency Transaction Reports for cash transactions >$10,000 |

Same business day |

|

CDD/KYC |

Verify customer identity and apply customer due diligence at onboarding |

At account opening |

|

Beneficial Ownership |

Identify and verify beneficial owners (25%+ ownership) |

At account opening |

|

Recordkeeping |

Maintain records for 5 years minimum |

Ongoing |

|

Corporate Transparency Act |

Report beneficial ownership to FinCEN (if applicable) |

As of 2025 |

State-Level Licensing Requirements

Beyond federal requirements, 47 states plus DC, Puerto Rico, and the US Virgin Islands require money transmitter licenses. Each state has its own application process, bonding requirements, and examination schedule.

According to the Conference of State Bank Supervisors (CSBS), the average fintech spends $500K–$2M and 12–18 months obtaining multi-state money transmitter licenses. The Nationwide Multistate Licensing System (NMLS) has streamlined the process, but it remains one of the most expensive and time-consuming compliance burdens for fintechs.

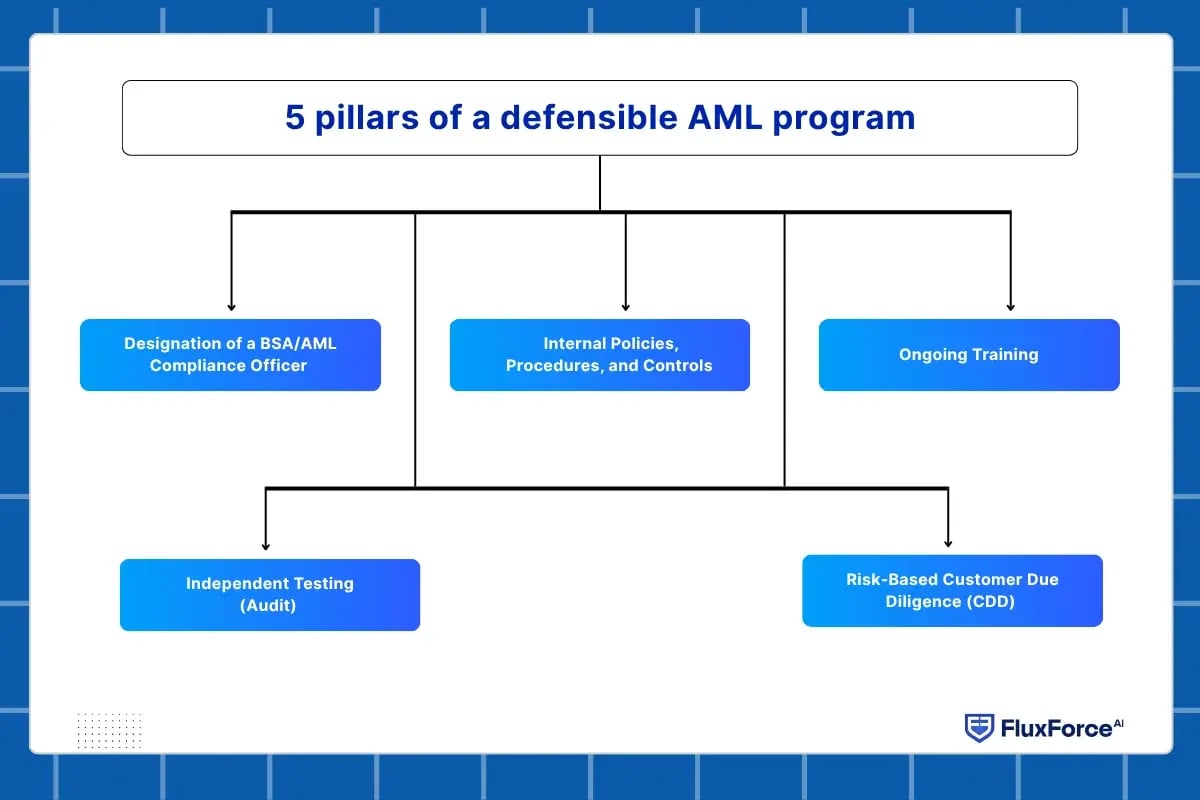

The 5 Pillars of a Defensible AML Program

A defensible AML compliance program, as required by the BSA and FFIEC guidance, must include these five pillars. If any of these are missing from your program, you have a gap that regulators will identify during your next examination.

Pillar 1 — Designation of a BSA/AML Compliance Officer

Every fintech must designate a qualified compliance officer responsible for BSA/AML compliance. This person must have:

- Sufficient authority to implement the program

- Direct access to the board of directors

- Relevant experience and training

- Independence from business-line pressure

Practical tip for startups: If you can't afford a full-time CCO, hire a fractional compliance officer or engage a compliance consulting firm. FinCEN and state regulators will accept this — what they won't accept is a lack of clear ownership.

Pillar 2 — Internal Policies, Procedures, and Controls

Your fintech AML program must include documented policies covering:

- Customer identification program (CIP)

- Customer due diligence (CDD) and enhanced due diligence (EDD)

- Transaction monitoring methodology

- SAR and CTR filing procedures

- Sanctions screening (OFAC)

- Record retention policies

- Escalation procedures

Pillar 3 — Ongoing Training

All relevant employees must receive BSA/AML training:

- At hiring and annually thereafter

- Role-specific training (front-line vs compliance vs leadership)

- Documented attendance and comprehension testing

- Updated for regulatory changes

Pillar 4 — Independent Testing (Audit)

An independent party must review your AML program:

- At least every 12–18 months

- Scope covers all BSA/AML program components

- Must be truly independent (not the compliance team auditing itself)

- Findings must be reported to the board

Pillar 5 — Risk-Based Customer Due Diligence (CDD)

Your customer due diligence procedures must follow a risk-based approach:

- Standard CDD at onboarding for all customers

- Enhanced due diligence (EDD) for high-risk customers

- Ongoing monitoring for changes in risk profile

- Beneficial ownership identification and verification

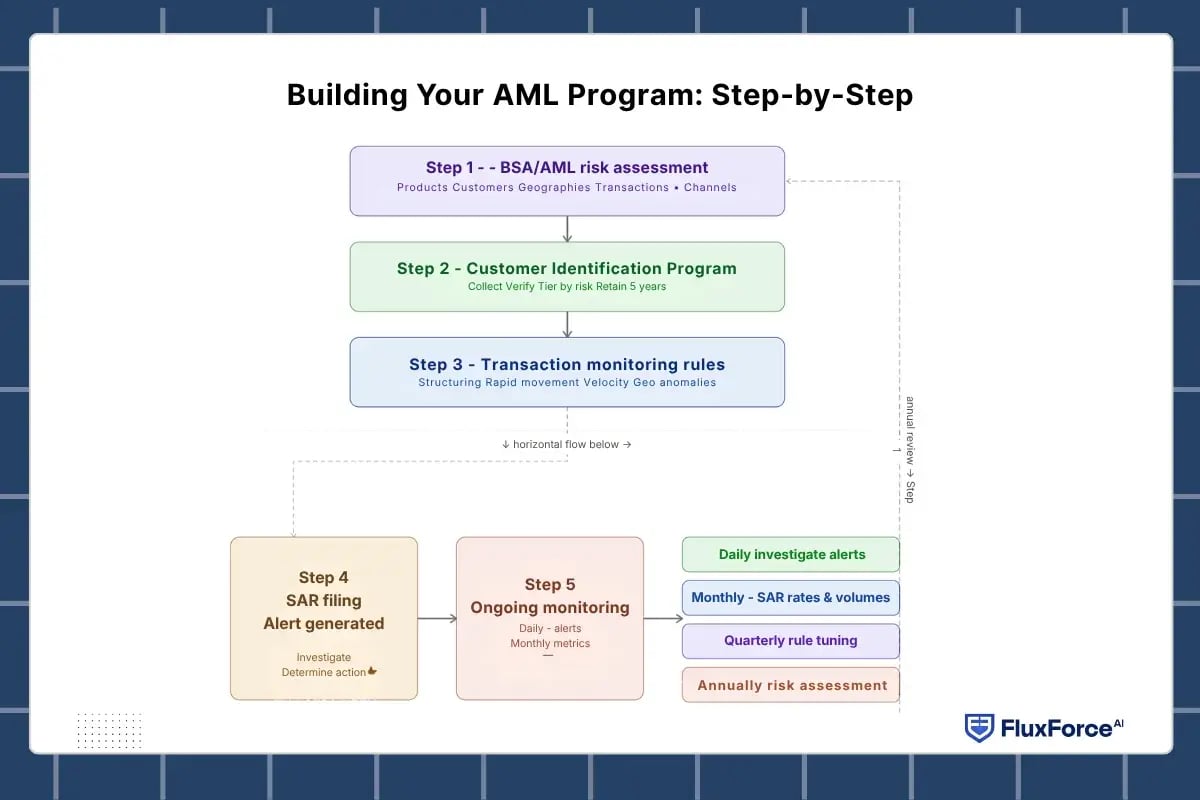

Building Your AML Program: Step-by-Step

Step 1 — Conduct a BSA/AML Risk Assessment

Before building anything, assess your specific risks. Your risk assessment should evaluate:

- Products and services — What do you offer? Which products are higher risk?

- Customer types — Who are your customers? What industries? What geographies?

- Geographic risk — Do you operate in or serve customers in high-risk jurisdictions?

- Transaction types — What payment channels do you support? Real-time? Cross-border?

- Delivery channels — How do customers access your services? Online-only? In-person?

The risk assessment drives everything. Your customer due diligence, transaction monitoring rules, training program, and staffing levels should all align with your assessed risk level.

Step 2 — Design Your Customer Identification Program (CIP)

Your CIP defines how you verify customer identity at onboarding:

- Minimum information to collect: Name, date of birth, address, ID number (SSN for US persons)

- Verification methods: Documentary (government ID), non-documentary (database verification), or a combination

- Risk-based tiering: Higher-risk customers require additional verification steps

- Recordkeeping: Retain CIP records for 5 years after account closure

Step 3 — Build Transaction Monitoring Rules

Design monitoring rules based on your risk assessment:

- Structuring detection: Transactions just below reporting thresholds

- Rapid movement: Funds moving in and out within short timeframes

- Unusual patterns: Activity inconsistent with the customer profile

- Velocity checks: Unusual frequency of transactions

- Geographic anomalies: Transactions involving high-risk jurisdictions

Pro tip: Start with 15–20 core rules and refine them based on alert quality. Too many rules from day one can create unmanageable alert volumes. According to industry benchmarks, the optimal rule set generates 50–100 alerts per analyst per day — any more and quality suffers.

Step 4 — Establish SAR Filing Procedures

Your SAR filing process must be documented and include:

- Alert generated by the monitoring system

- Analyst investigation and documentation

- Determination: file SAR, no SAR, or escalate

- SAR narrative writing (the most critical element)

- Quality review before filing

- Filing via FinCEN's BSA E-Filing System

- 90-day continuing review for ongoing activity

The SAR narrative is what regulators care about most. A well-written narrative explains who, what, when, where, why, and how — and demonstrates that your institution understands the suspicious activity, not just that your system flagged it.

Step 5 — Implement Ongoing Monitoring

AML compliance is not a set-it-and-forget-it activity:

- Daily: Review and investigate generated alerts

- Monthly: Analyze alert volumes, SAR filing rates, and case disposition metrics

- Quarterly: Review and tune monitoring rules based on false positive rates

- Annually: Update risk assessment, revise policies, and conduct an independent audit

Transaction Monitoring for Fintechs: Practical Approaches

Transaction monitoring is where most fintechs struggle — and where most enforcement actions originate.

How Small Compliance Teams Can Handle Transaction Monitoring

If you have 1–3 compliance analysts (typical for an early-stage fintech), you cannot afford to generate thousands of false positive alerts. Your monitoring approach must be ruthlessly efficient.

|

Approach |

False Positive Rate |

Analyst Capacity Needed |

Cost |

|

Manual review (no automation) |

N/A — significant coverage gaps |

1 per 200 accounts |

Lowest |

|

Basic rule-based system |

95–99% |

1 per 500–1,000 accounts |

Medium |

|

Tuned rule-based system |

80–90% |

1 per 2,000–5,000 accounts |

Medium |

|

AI/ML-powered system |

20–40% |

1 per 10,000–50,000 accounts |

Higher |

Recommendation for growing fintechs: Start with a tuned rule-based approach, but plan to migrate to AI-powered monitoring as you scale beyond 10,000 customers. The efficiency gains typically offset costs within 6–12 months.

What Regulators Expect from Transaction Monitoring ?

Based on recent FinCEN and OCC enforcement actions, regulators evaluate transaction monitoring on:

- Coverage: Are all products, channels, and customer types monitored?

- Calibration: Are thresholds appropriate for your risk profile?

- Documentation: Can you clearly explain why each rule exists and how thresholds were set?

- Tuning: Do you regularly review and adjust rules based on performance?

- Timeliness: Are alerts investigated within your stated SLA (typically 24–72 hours)?

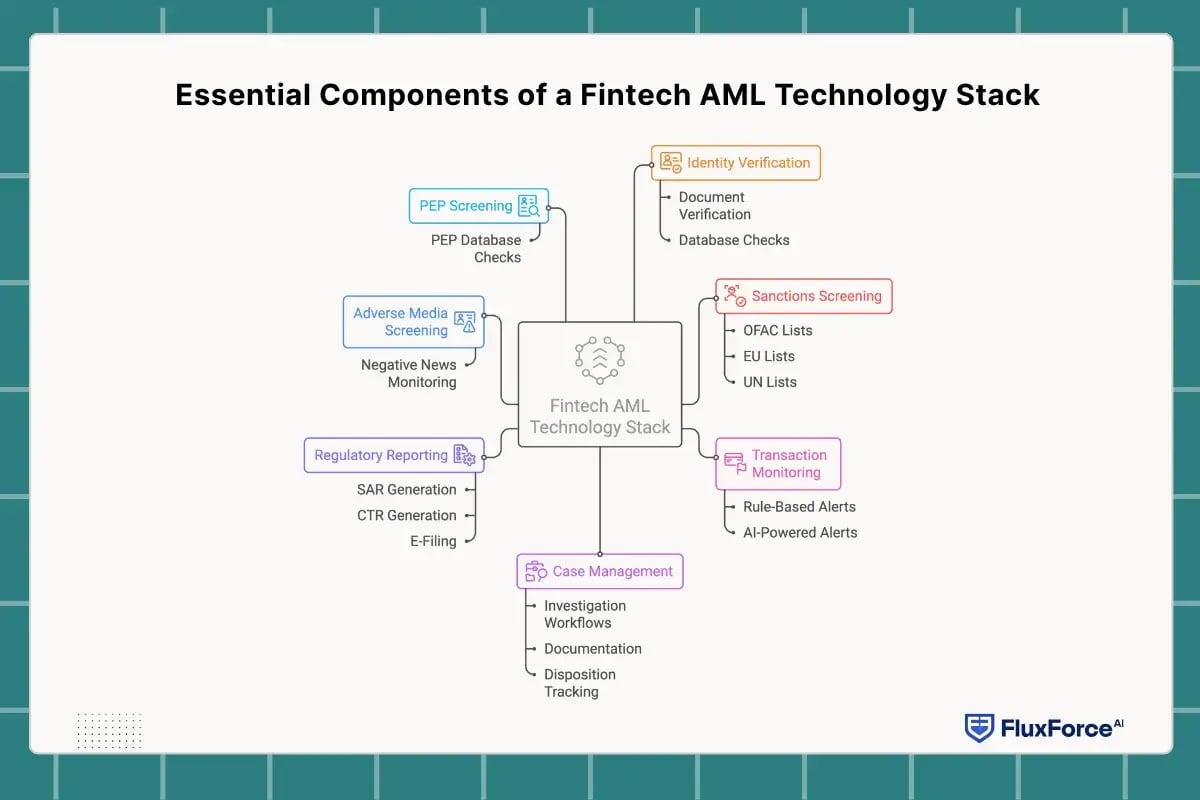

Technology Stack for Fintech AML Compliance in 2026

Essential Components of a Fintech AML Technology Stack

A modern fintech AML technology stack should include:

- Identity verification (IDV) — automated document verification and database checks

- Sanctions screening — real-time screening against OFAC, EU, and UN sanctions lists

- Transaction monitoring — rule-based or AI-powered alert generation

- Case management — investigation workflows, documentation, and disposition tracking

- Regulatory reporting — SAR/CTR generation and e-filing

- Adverse media screening — automated negative news monitoring

- PEP screening — politically exposed persons database checks

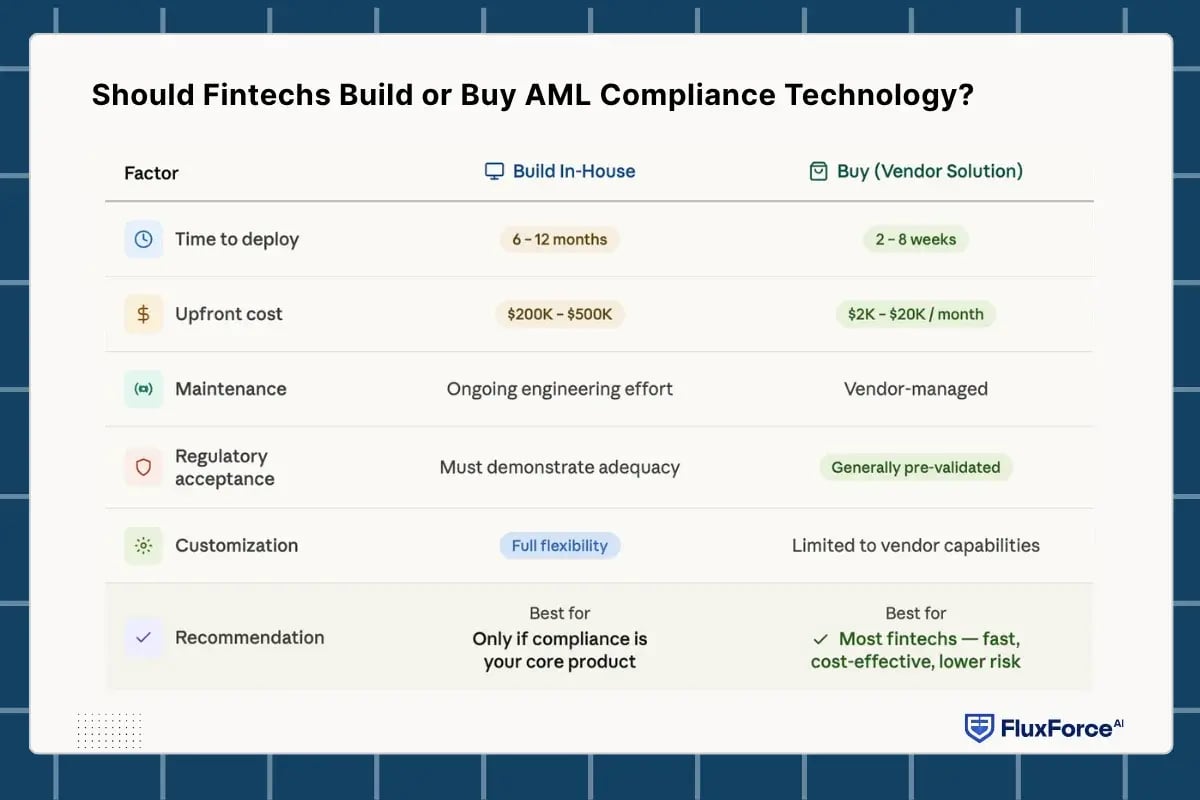

Should Fintechs Build or Buy AML Compliance Technology?

Common Mistakes That Get Fintechs in Trouble

Based on analysis of FinCEN and state enforcement actions against fintechs from 2023–2025:

Mistake 1 — "Our Sponsor Bank Handles Compliance"

Reality: You share responsibility. If your sponsor bank's AML program is inadequate, you may also face enforcement action. The OCC fined multiple sponsor banks in 2025 for failing to ensure their fintech partners maintained adequate BSA programs.

Mistake 2 — Not Filing SARs (or Filing Late)

Reality: Failure to file Suspicious Activity Reports (SARs) is the most frequently cited violation in BSA enforcement actions. If you detect suspicious activity and do not file within 30 days, you are in violation — regardless of whether the activity ultimately results in confirmed fraud

Mistake 3 — No Risk Assessment

Reality: Your AML program must be risk-based. Without a documented risk assessment, your entire program becomes difficult to defend during an examination. Regulators will almost certainly issue a finding.

Mistake 4 — Over-Relying on Technology Without Understanding It

Reality: Deploying a transaction monitoring tool without ongoing tuning is ineffective. Regulators expect you to understand your monitoring methodology — including rules, thresholds, and exceptions.

Mistake 5 — Treating Compliance as a Cost Center

Reality: The average FinCEN enforcement penalty in 2025 was $12.7 million, while the average annual cost of a well-structured AML program for a mid-stage fintech is $200K–$500K. The cost-benefit tradeoff is clear.

Key Takeaways

- AML compliance for fintechs is mandatory in 2026 — if you move money, you must comply. There are no exceptions for startups or BaaS partnerships.

- The 5 pillars are non-negotiable: BSA/AML compliance officer, written policies, training, independent testing, and risk-based customer due diligence (CDD).

- Start with a risk assessment — it drives every other compliance decision and is the first thing regulators will ask for.

- Transaction monitoring is where fintechs fail most often — invest in monitoring systems your team can effectively manage.

- SAR filing is the most common enforcement trigger — late or missing SARs result in more penalties than most other BSA violations.

- Technology should augment your team, not replace understanding — regulators expect you to clearly explain your monitoring methodology.

Conclusion

AML compliance for fintechs in 2026 is no longer optional. It plays a key role in building a secure and scalable business. A well-structured, risk-based AML program helps you stay compliant while also building trust with banks, investors, and customers.

As AML compliance fintech 2026 requirements continue to evolve, fintechs that treat compliance as a core part of their operations will be better positioned for long-term growth.

If you're also navigating data privacy alongside AML compliance, you can read our related guide on AML Risk Checks in Policy Issuance KYC AML & Identity Verification Strategy for Compliance Officers in Insurance

Share this article