.webp)

Listen To Our Podcast🎧

Introduction

Zero trust security for financial institutions has moved from a theoretical architecture debate to a board-level priority. Banks, insurers, and fintechs face pressure from regulators, threat actors, and an application perimeter that legacy access controls can't handle. The old assumption that anything inside the network is trustworthy breaks down the moment an employee clicks a phishing link, a third-party vendor is compromised, or a rogue insider escalates privileges. This guide lays out a complete zero trust framework built for the realities of regulated financial services: fragmented vendor stacks, strict audit requirements, and the constant friction between security controls and operational speed.

- What Is Zero Trust Security for Financial Institutions?

- Why Point Solutions Break Down in Financial Services

- The Core Pillars of Zero Trust Security for Financial Institutions

- How a Unified Risk Platform Transforms Zero Trust Execution

- Explainable AI: Making Zero Trust Decisions Auditable

Onboard Customers in Seconds

What Is Zero Trust Security for Financial Institutions?

Zero trust security for financial institutions is a security model that treats every access request as untrusted until verified, regardless of where it originates. No implicit trust is extended to users, devices, or workloads based on network location alone.

The principle sounds straightforward. The execution is not. A mid-sized bank might have hundreds of internal applications, dozens of third-party integrations, and thousands of employees accessing sensitive data from multiple devices and locations. Applying continuous verification across all of those touchpoints without crippling operations requires careful architecture choices, not just a vendor purchase.

The Three Core Assumptions of Zero Trust

Zero trust rests on three foundational assumptions:

- Assume breach: Design your architecture as if the perimeter has already been compromised. Segment access aggressively.

- Verify explicitly: Authenticate and authorize every request using identity, device health, location, and behavioral signals before granting access.

- Use least-privilege access: Give users and systems only the access they need for specific tasks, for the minimum time required.

Why Financial Services Needs Zero Trust Now

The NIST Special Publication 800-207 on zero trust architecture has become the de facto reference standard for regulated industries since its 2020 release. Financial regulators in the US, UK, and EU have increasingly cited zero trust principles in cybersecurity guidance for banks and payment processors. For institutions under PCI DSS, DORA, or SOX, zero trust isn't optional architecture, it's the expected direction of travel.

Why Point Solutions Break Down in Financial Services

The honest answer about point solutions vs platform financial services is that the fragmentation problem becomes expensive before it becomes a visible security failure. A typical mid-market bank might run 30 to 60 separate security tools across identity, endpoint detection, fraud monitoring, API security, and compliance reporting. Each tool has its own console, its own alert queue, and its own data format.

That isn't just a management headache. It creates detection gaps where threats fall between tools that don't share context. An anomalous login detected by the identity provider never reaches the fraud monitoring system. A suspicious API pattern flagged by the gateway doesn't correlate with the behavioral signal from the endpoint agent.

The Cost of Vendor Sprawl in Financial Security

Vendor consolidation fintech teams are pursuing aggressively in 2025 and 2026 for measurable reasons:

- Alert fatigue: Security teams at large banks routinely receive tens of thousands of alerts per day. Most are noise. When tools don't share context, analysts spend time triaging duplicates rather than investigating real threats.

- Integration overhead: Maintaining custom integrations between 40 tools consumes a disproportionate share of security engineering time, and every vendor update risks breaking a connector.

- Compliance reporting gaps: When audit evidence lives in 12 different systems, producing a coherent compliance report for a regulator is a multi-day manual exercise.

The shift toward vendor consolidation fintech organizations are undertaking isn't purely about cutting costs. It's about reducing coordination overhead that makes security teams slow.

What a Platform Approach Actually Changes

Moving from point solutions to an ai security operations platform changes the underlying data model. Instead of each tool maintaining its own siloed records, a platform approach centralizes signals from identity, fraud, compliance, and endpoint into a shared graph. Correlations that would take a human analyst hours to piece together happen in milliseconds.

The practical result is that fraud compliance identity platform capabilities become achievable that simply don't exist when fraud, compliance, and identity are managed in separate tools by separate teams operating on separate schedules.

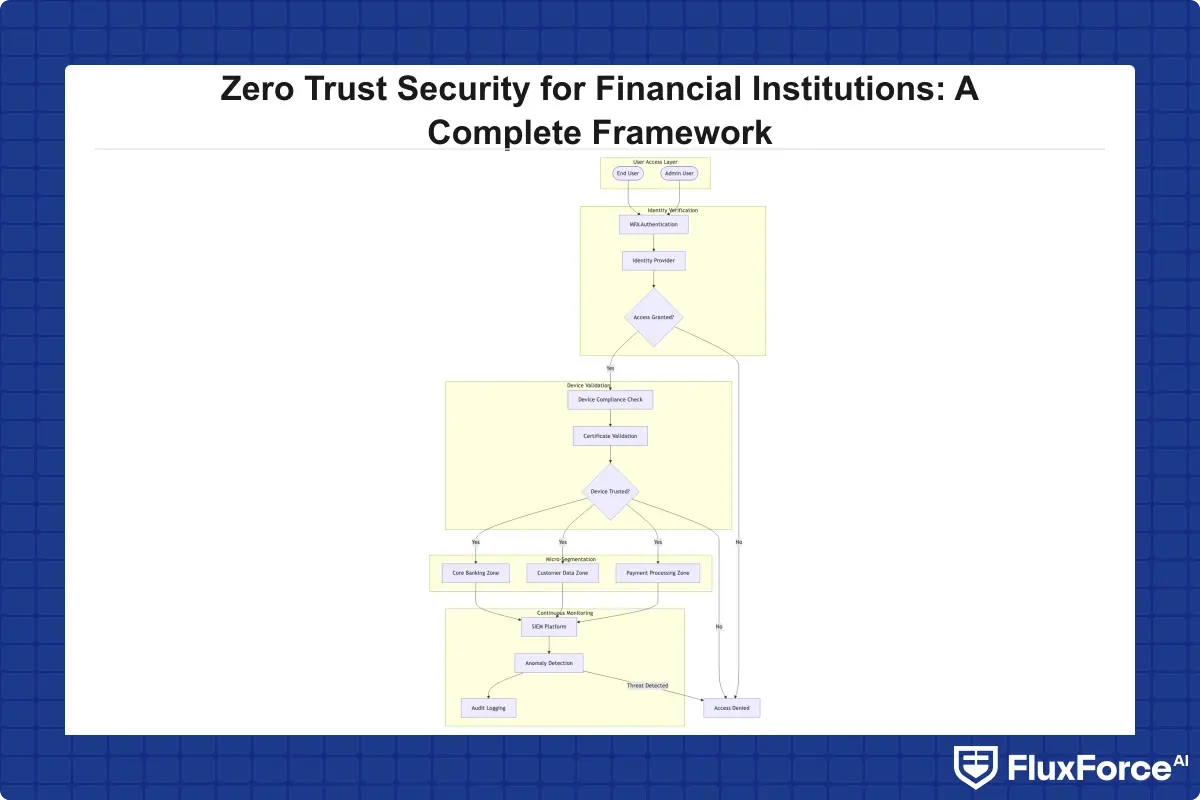

The Core Pillars of Zero Trust Security for Financial Institutions

Zero trust security for financial institutions isn't a single product. It's an architecture built on interconnected controls. Five pillars form the foundation of any implementation that will hold up to regulatory scrutiny.

Identity and Access Management

Identity is the new perimeter. Every human user, service account, and API call needs a verified identity before any access is granted. In financial services, this means multi-factor authentication at minimum, with adaptive authentication that adjusts requirements based on risk signals: unusual location, new device, off-hours access. Privileged access management for admin accounts on core banking systems is especially critical, with time-limited just-in-time access and full session recording as the baseline regulators now expect.

Device Trust and Endpoint Verification

A valid identity on an unmanaged or compromised device is still a risk. Zero trust requires that device health be checked as part of every access decision. For institutions with distributed workforces or bring-your-own-device policies, this is one of the more complex pillars to implement. Expect friction during rollout, employees don't enjoy being blocked because their laptop OS is two versions behind.

Network Micro-Segmentation

Instead of flat networks where a compromised workstation can reach the core banking database, micro-segmentation divides the network into small zones with strict traffic rules between them. Lateral movement, the technique attackers use to spread from an initial foothold to high-value targets, becomes significantly harder when each zone requires its own authorization.

Application-Level Access Controls

Every internal application should enforce its own access controls rather than trusting that the network perimeter has already validated the request. This is where zero trust intersects directly with Banking Access Controls: Zero Trust Security Architecture Strategy for Banking Ops Heads, the application layer needs to participate in the verification chain, not just sit behind it.

Continuous Monitoring and Response

Zero trust isn't a static configuration. It requires continuous visibility into what's happening across identities, devices, applications, and data. Static rule sets can't keep pace with the variety of access patterns in a large financial institution, which is why the ai security operations platform capability becomes central to the architecture rather than one component among many.

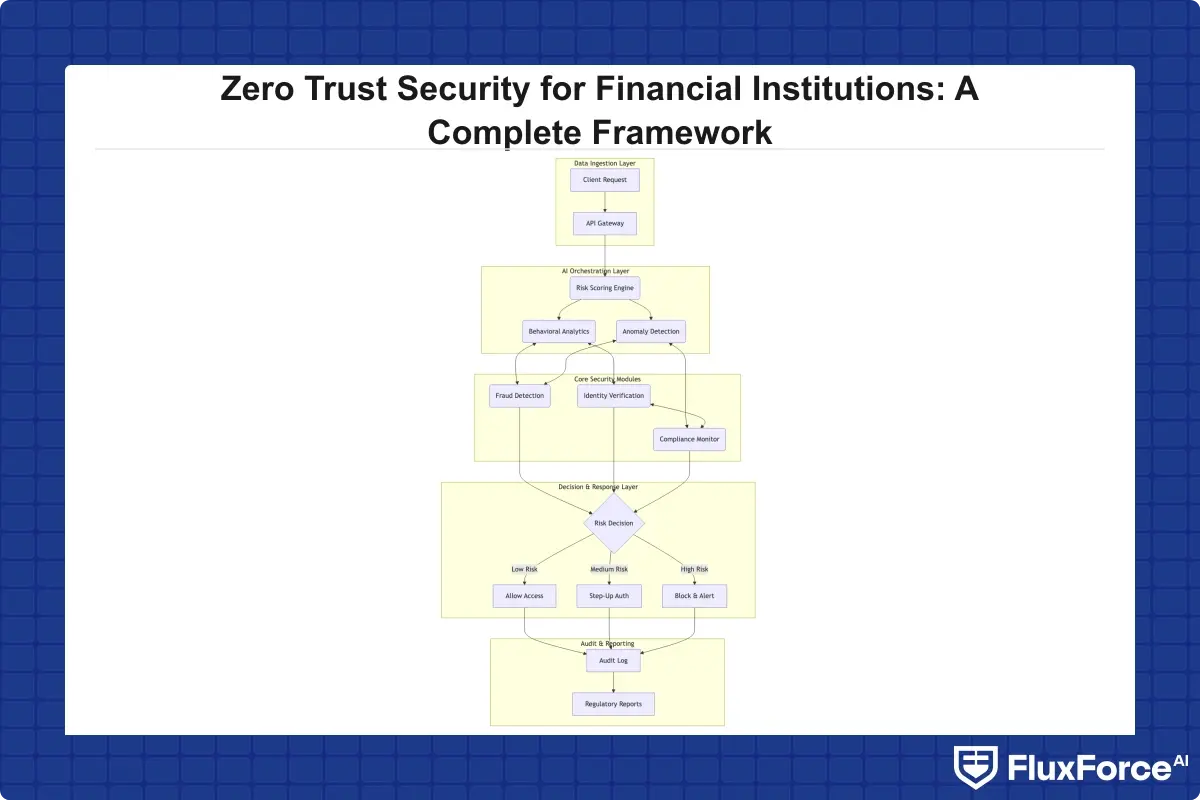

How a Unified Risk Platform Transforms Zero Trust Execution

A unified risk platform does something that point-solution stacks fundamentally cannot: it shares context across fraud, compliance, and identity in real time. When a fraud signal triggers, the platform simultaneously evaluates identity risk, checks compliance flags, and adjusts access permissions without waiting for a human to coordinate across three separate teams.

Breaking Down the Silos Between Fraud and Compliance

For institutions with high transaction volumes, coordination latency matters. Manual escalations add time to every investigation, and time in fraud detection means losses. A fraud compliance identity platform that connects these signals reduces the window between detection and response from hours to seconds. The compliance team sees the same signal as the fraud team at the same moment, with context attached.

The operational benefit of vendor consolidation fintech platforms deliver goes beyond fewer vendor contracts. It means fewer handoffs between teams, fewer integration failures during vendor updates, and a single audit log that regulators can review instead of requiring evidence from a dozen systems.

Configurable Autonomy for Different Risk Appetites

This is also where configurable ai autonomy becomes meaningful for risk officers. Not every institution is comfortable with fully automated fraud blocks. A platform that lets you set the autonomy level, from alert and recommend, to auto-block with human review queue, lets security teams match their risk appetite to the technical capabilities without forgoing protection. For banks at different stages of AI maturity, that flexibility makes adoption practical rather than aspirational.

Explainable AI: Making Zero Trust Decisions Auditable

The compliance challenge with AI-driven security decisions isn't accuracy. Modern machine learning models catch fraud patterns that rule-based systems miss by significant margins. The challenge is ai model explainability regulators can point to when something goes wrong or when an audit requires evidence of a fair, consistent decision process.

Black box ai compliance risk is real and increasingly a regulatory focus. The EU AI Act, DORA, and emerging SEC guidance on algorithmic decision-making all push toward explainability requirements. An institution that can't explain why a transaction was blocked, or why a user's access was revoked, is exposed to both regulatory scrutiny and customer complaints.

SHAP Values and Regulatory Communication

Explainable ai finance teams use several technical methods to make model outputs interpretable. SHAP (SHapley Additive exPlanations) values are among the most widely adopted. Shap values explained to regulators identify which features drove a specific model decision, expressed in plain-language terms: this transaction was flagged because the amount was four times the user's 90-day average and originated from a new device in a different country.

This is explainable ai compliance in practice. The model doesn't just flag a transaction, it produces a human-readable explanation that goes into the audit record. Compliance officers can review it, regulators can request it, and it can be used to defend decisions in the event of a dispute.

XAI Fraud Detection in Regulated Environments

XAI fraud detection systems integrated with zero trust architectures offer a concrete operational advantage: every access or transaction decision comes with a decision log capturing both the inputs and the reasoning. This ai audit trail automation means compliance teams aren't reconstructing decisions after the fact from sparse log data, the explanation is generated at decision time and stored automatically.

For institutions running AI-driven fraud analysis, the explainability layer is what separates a production-grade deployment from a pilot project regulators won't certify for live use. See how Card Fraud Analytics: AI-Powered Fraud Detection Strategy for Risk Heads handles this challenge at the operational level.

AI Agents and Human-in-the-Loop Banking Security

Ai agents financial services teams are deploying represent a meaningful evolution in how zero trust gets executed at scale. Rather than waiting for human analysts to correlate signals across identity, fraud, and compliance, AI agents handle routine coordination automatically and escalate only the genuinely ambiguous cases.

A multi agent ai system built for financial security might include specialized agents for transaction monitoring, identity risk scoring, API anomaly detection, and regulatory reporting. Each agent handles its own domain but shares context through a common data layer. The result is faster detection and response without a proportional increase in analyst headcount.

AI Agent Fraud Detection: What Changes

Ai agent fraud detection works differently from traditional rule engines. Instead of static thresholds, an agent continuously recalibrates based on behavioral baselines, peer group comparisons, and emerging pattern signals. This means fewer false positives on legitimate high-value transactions and faster detection of novel fraud patterns that don't match any existing rule. Institutions running How Agentic AI Fraud Agents Cut False Positives by 80% have documented the detection improvement in quantitative terms.

Institutions running How Agentic AI Fraud Agents Cut False Positives by 80% have documented the detection improvement in quantitative terms.

The tradeoff is that agents need supervision, especially in early deployment. That's where human in the loop ai banking becomes a practical necessity rather than a theoretical safety net. Agents handle the high-confidence decisions autonomously. The low-confidence or high-stakes decisions go to a human review queue. Over time, as the agent's decision quality is validated against your specific environment, the queue typically shrinks.

Configurable AI Autonomy in Practice

Configurable ai autonomy is the feature that makes AI agents acceptable to risk officers who have learned not to fully trust systems they can't inspect. The ability to set autonomy thresholds per risk tier, high-confidence, low-value decisions auto-resolved; high-stakes decisions always escalated, gives institutions a practical path to AI adoption without the career risk that comes with a fully autonomous system making a high-profile error.

For a deeper look at how agentic implementations work within banking security architecture, Zero Trust + Agentic AI: The New Normal for Banking Security covers the intersection of these approaches in detail.

How to Implement Zero Trust Security for Financial Institutions

Implementation is where most zero trust programs stall. The architecture is sound, the business case is clear, but the practical steps require careful sequencing, organizational buy-in, and tolerance for a period of increased friction during rollout. Here are six steps that reflect how successful implementations actually progress.

Step 1: Map Your Access Landscape

Before changing any configuration, document every user, device, application, and data flow in your environment. You can't segment what you haven't mapped. This step typically takes four to eight weeks for a mid-sized institution and reveals access patterns that security teams didn't know existed, including shadow IT and dormant privileged accounts.

Step 2: Start with Identity

Identity delivers the highest leverage per implementation effort. Deploy strong MFA across all users, enforce conditional access policies, and implement just-in-time access for privileged accounts. This step delivers measurable risk reduction before micro-segmentation or application-layer changes are complete.

The identity layer of zero trust also connects directly to customer-facing verification workflows. The same rigor applied to internal access extends naturally to customer onboarding, see AML Risk Checks in Policy Issuance: KYC/AML & Identity Verification Strategy for Claims Directors in Insurance for how this plays out across insurance and banking contexts.

Step 3: Segment by Risk, Not Convenience

Network segmentation decisions made purely for ease of management create zones that are too large to provide meaningful protection. Segment by data sensitivity and access need. Core banking data should sit in a different zone from marketing analytics, with strict controls on traffic between them.

Step 4: Integrate Continuous Monitoring

Zero trust without continuous monitoring is just access control. The monitoring layer is what makes the architecture adaptive. Connect identity, endpoint, application, and network monitoring into a unified view. This is the point where the ai security operations platform becomes the center of the architecture. API security belongs here too, financial institutions run hundreds of APIs, many connecting to third parties. For CISO-level API security strategy, API Rate Limiting: API Security Strategies for CISOs in Banking covers the specific controls that belong in this layer.

Step 5: Automate Response Gradually

Start with automated detection and alerting. Move to automated response only after you've validated the system's accuracy against your specific environment. Human in the loop ai banking isn't a sign of limited confidence in AI, it's the operationally sound approach during the learning period, and it's the model most regulators expect to see documented.

Step 6: Build the Audit Trail from Day One

Don't treat audit logging as something you'll configure later. Regulators expect a complete record of who accessed what, when, and why. The ai audit trail automation capabilities of your chosen platform should be configured from day one, not retrofitted after the first audit finding. Institutions that build the audit trail in from the start spend significantly less time on regulatory responses than those that try to reconstruct decision histories after the fact.

- Zero trust security for financial institutions is a security model that treats every access request as untrusted until verified, regardless of where it originates.

- The honest answer about point solutions vs platform financial services is that the fragmentation problem becomes expensive before it becomes a visible security failure.

- Zero trust security for financial institutions isn't a single product.

- A unified risk platform does something that point-solution stacks fundamentally cannot: it shares context across fraud, compliance, and identity in real time.

- The compliance challenge with AI-driven security decisions isn't accuracy.

Onboard Customers in Seconds

Conclusion

Zero trust security for financial institutions is the architecture that matches the actual threat environment. Perimeter defenses made sense when applications and users were in one building. They don't hold up when users are distributed, applications are cloud-native, and third-party integrations multiply every quarter.

The implementation path is sequential: map access, start with identity, segment by risk, integrate continuous monitoring, and automate gradually with human oversight in place. The unified risk platform model, combined with explainable AI and configurable autonomy, gives institutions the operational control and audit evidence that regulators require. Institutions that treat zero trust as a vendor purchase rather than an architectural commitment will rebuild the same fragmentation problem they started with.

If your institution is evaluating where to start, the fraud detection layer typically offers the fastest path to demonstrable ROI. Purpose-built fraud detection software that integrates identity, behavioral, and compliance signals into a single decision engine is both the most visible security win and the most direct line to building the regulatory confidence that zero trust programs ultimately require.

Share this article