.webp)

Listen To Our Podcast🎧

Introduction

Ultimate beneficial owner verification sits at the center of every serious anti-money laundering program, yet the gap between what regulators expect and what most institutions actually do remains uncomfortably wide. The 2016 FinCEN Customer Due Diligence (CDD) Rule made it mandatory for covered financial institutions to identify and verify beneficial owners of legal entity customers, and the Corporate Transparency Act (CTA) extended those requirements further starting in 2024. Deficient UBO identification appeared as a contributing factor in a notable share of enforcement actions between 2022 and 2024. This post untangles what UBO verification actually requires, where the complexity hides, and how modern aml compliance software and kyc automation are making the process faster and more defensible across banks, fintechs, insurers, and regulated institutions of every size.

- What Is Ultimate Beneficial Ownership and Why It Matters for AML Compliance

- The Regulatory Framework Behind Ultimate Beneficial Owner Verification Requirements

- How Ultimate Beneficial Owner Verification Works in Practice

- AML Compliance for Fintechs: UBO on Small Teams

- BSA/AML Compliance Checklist: What Banks Must Verify for Each Account

Onboard Customers in Seconds

What Is Ultimate Beneficial Ownership and Why It Matters for AML Compliance

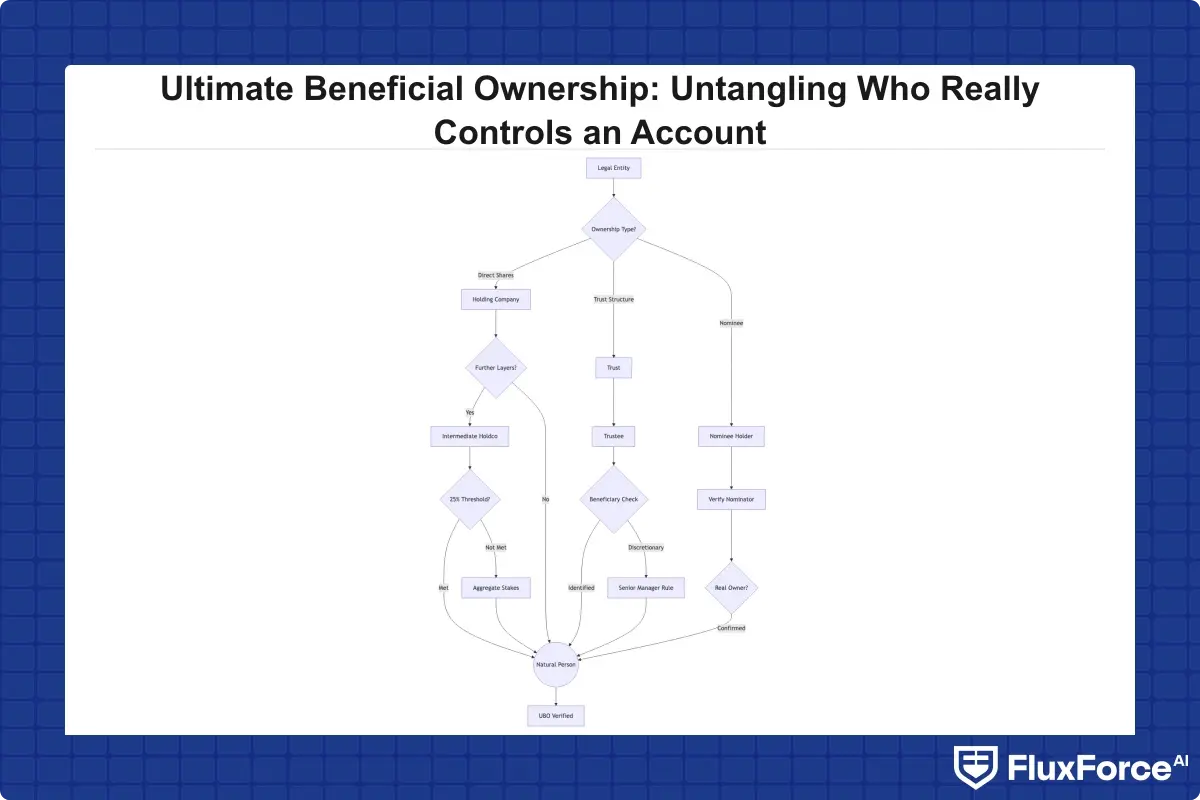

Ultimate beneficial ownership refers to the natural persons who, directly or indirectly, own or control a legal entity. That sounds simple. In practice, it's rarely simple, because modern corporate structures are often designed, sometimes legitimately, to layer ownership across multiple jurisdictions, holding companies, trusts, and nominee arrangements. For aml compliance purposes, identifying the human being who ultimately benefits from or controls an account is the only way to close the gap that shell companies exploit.

The Financial Action Task Force (FATF), the global standard-setter for anti-money laundering, treats beneficial ownership transparency as a foundational requirement for an effective AML regime. Countries that fail FATF mutual evaluations on UBO face correspondent banking pressure and grey-listing risk.

Why Shell Companies Make UBO Disclosure Complicated

A single operating company might sit beneath two holding companies, one registered in the Cayman Islands and one in Delaware, with the ultimate owner being a trust whose settlor is a politically exposed person in Eastern Europe. Each layer is technically legitimate. Together, they create a structure that can obscure the true controller from any institution that doesn't look hard enough.

The money laundering risk is straightforward: funds entering the financial system through such structures can cycle through multiple jurisdictions before reaching their destination, with each hop making tracing harder. For compliance teams, the challenge is knowing when a corporate structure is a normal multinational arrangement versus a purposeful obfuscation.

The 25% Ownership Threshold Explained

FinCEN's CDD Rule sets a 25% equity ownership threshold: any natural person owning 25% or more of a legal entity customer must be identified and verified. There's also a control prong, requiring identification of at least one individual who exercises control regardless of ownership percentage. The EU's 4th and 5th Anti-Money Laundering Directives use the same 25% threshold as a starting point but allow member states to go lower. Some jurisdictions use 10% for higher-risk sectors.

FinCEN's CDD Rule sets a 25% equity ownership threshold: any natural person owning 25% or more of a legal entity customer must be identified and verified.

The threshold isn't a safe harbor. If your institution has information suggesting that someone with 18% ownership is the controlling mind behind an entity, ignoring that person because they fall below the 25% line creates a real defensibility problem in any examination.

If your institution has information suggesting that someone with 18% ownership is the controlling mind behind an entity, ignoring that person because they fall below the 25% line creates a real defensibility problem in any examination.

The Regulatory Framework Behind Ultimate Beneficial Owner Verification Requirements

Ultimate beneficial owner verification requirements didn't emerge from a single rule. They're the product of overlapping global and domestic frameworks that compliance teams need to read together.

In the United States, the core requirements come from the Bank Secrecy Act and its implementing regulations, including FinCEN's CDD Rule and the CTA. The CTA created a Beneficial Ownership Information (BOI) reporting regime requiring most companies formed or registered to do business in the US to report UBO data to FinCEN. That data becomes available to authorized government agencies and, in limited circumstances, financial institutions. For banks trying to cross-reference their own CDD data against the FinCEN BOI database, the technical integration is still maturing.

Internationally, FATF Recommendation 24 covers transparency and beneficial ownership of legal persons. The EU's AML Package, finalized in 2024, created a new EU Anti-Money Laundering Authority (AMLA) and strengthened UBO register requirements across member states. The EU AI Act, which comes into full force across 2025-2026, creates new obligations for AI-based customer due diligence tools used in financial services, which matters for any institution deploying automated UBO verification workflows.

FinCEN's CDD Rule and the 2024 Beneficial Ownership Update

The 2016 CDD Rule established four pillars: customer identification, beneficial owner identification, understanding the nature and purpose of customer relationships, and ongoing monitoring. Many institutions treated beneficial owner identification as a checkbox at account opening and didn't build systems to update that data when ownership structures changed. FinCEN's updated guidance makes clear that ownership changes during the customer lifecycle must trigger re-verification workflows, not just wait for the next annual review cycle.

EU AI Act Financial Services: Emerging UBO Obligations

The eu ai act financial services implications for UBO verification are still being worked through by compliance teams across Europe. AI systems used for CDD and identity verification fall under the Act's high-risk AI category, which means pre-deployment conformity assessments, ongoing logging requirements, and human oversight mandates. For any institution using automated UBO screening, this creates new documentation obligations that sit alongside existing AML obligations, requiring vendors and in-house tools to maintain audit trails in a format that satisfies both sets of regulators simultaneously.

How Ultimate Beneficial Owner Verification Works in Practice

The mechanical process of ultimate beneficial owner verification breaks into three stages: collection, verification, and ongoing monitoring.

Collection means gathering ownership and control information from the customer. For legal entity customers, this typically involves a self-certification form. The customer declares who the beneficial owners are, provides identification documents for each, and attests to the accuracy of the information. Self-certification is a weak control in isolation. Customers can lie, and institutions that rely entirely on customer attestation without independent verification build a policy that looks good on paper but doesn't hold up in examinations.

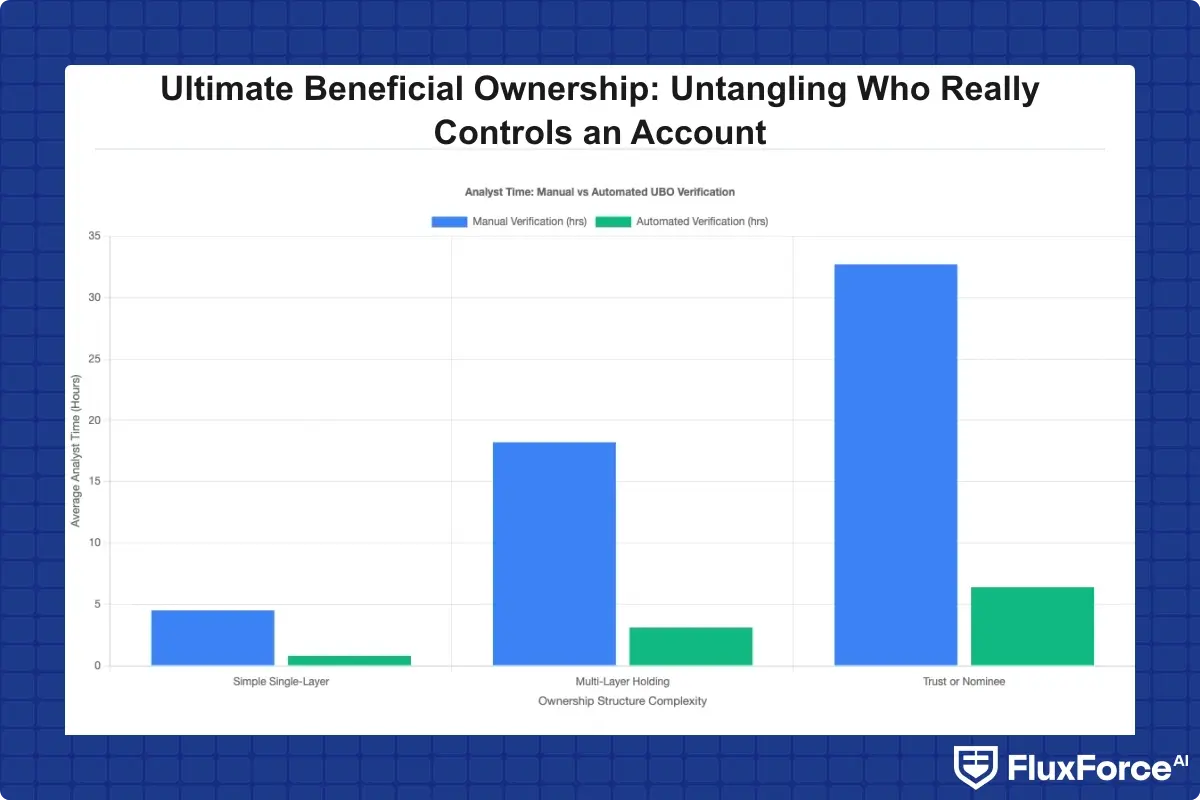

Verification means independently corroborating what the customer told you. This involves checking the identified natural persons against identity documents, government databases, and third-party data sources. For higher-risk entities, it means going further: pulling corporate registry records, checking UBO registers where they exist, and using anti money laundering technology to screen ownership graphs against sanctions lists and adverse media. A thorough verification process can take four to eight hours for a complex multi-jurisdiction entity, which is why manual processes don't scale.

Ongoing monitoring is where most programs have historically been weakest. Ownership changes after account opening, and systems that treat UBO as a one-time onboarding task will miss those changes. Triggering event-based re-verification when a customer reports an ownership change, when media monitoring surfaces a relevant news item, or when periodic review cycles kick in is where ongoing monitoring and AML screening tools provide the clearest operational value.

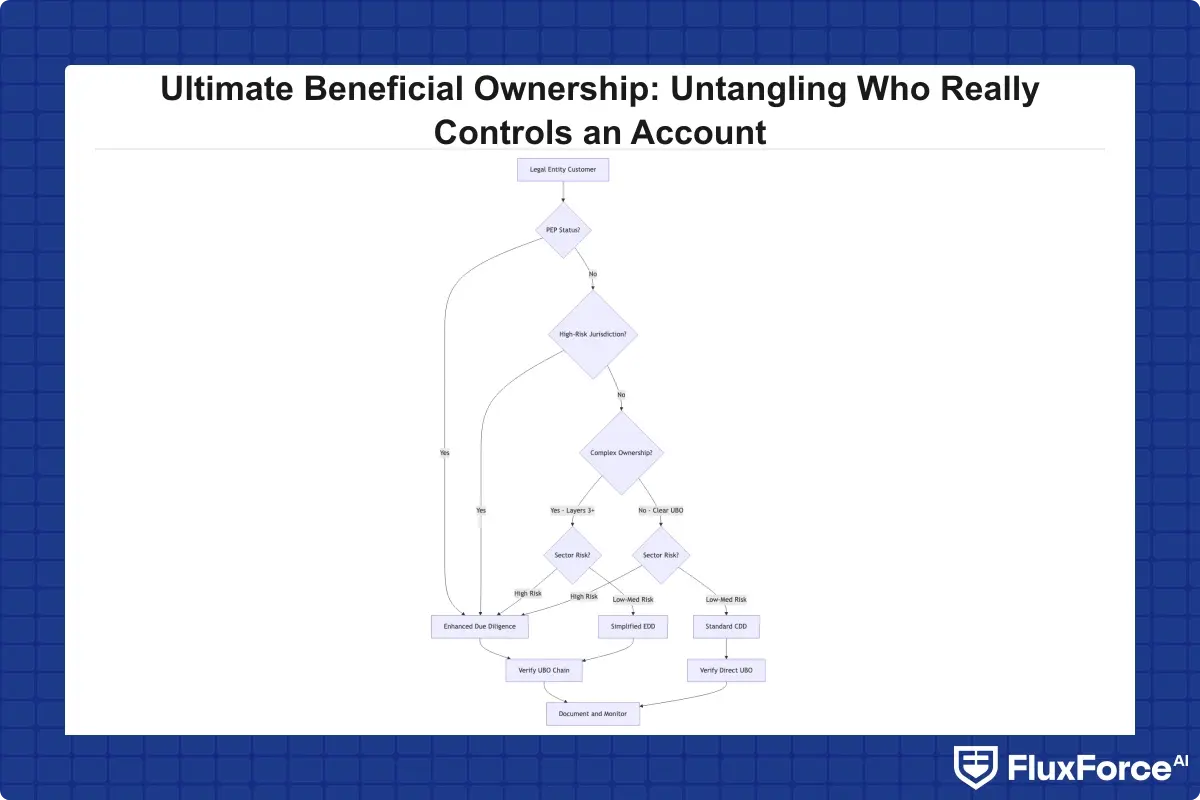

Enhanced Due Diligence Guide for High-Risk Entities

Not every UBO investigation requires the same depth. An enhanced due diligence guide for UBO should include: verification of source of wealth for each beneficial owner, adverse media search across major news databases, direct customer outreach to understand the rationale for a complex ownership structure, and escalation to senior management sign-off. Enhanced due diligence is triggered by risk factors: the customer involves a politically exposed person, the ownership structure includes high-risk jurisdictions, the business type is in an elevated-risk sector, or transaction patterns suggest heightened risk. Complex EDD cases at mid-size institutions routinely take multiple days even with experienced analysts, which is a real resource constraint that automation can help address.

KYC CDD Requirements Banks Must Meet Before Onboarding

The kyc cdd requirements banks must satisfy before onboarding a legal entity customer include: formation documents, operating agreements or bylaws where relevant, identification and verification of all beneficial owners meeting the ownership or control thresholds, and a risk assessment that shapes the monitoring profile for the account. For community banks onboarding commercial customers with multiple subsidiaries, meeting these requirements manually for every account is a substantial operational load. The honest answer is that most community banks are one or two examiners away from a Matters Requiring Attention on UBO documentation.

AML Compliance for Fintechs: UBO on Small Teams

Aml compliance fintech teams face UBO challenges that are structurally different from large bank programs. A fintech with 15 people in compliance doesn't have the headcount to run the manual review processes a regional bank uses. They also tend to onboard business customers faster, sometimes in minutes, which creates real friction between customer experience goals and the verification rigor that AML compliance requires.

The fintech bsa aml small team problem is genuinely hard. FinCEN expects the same quality of UBO identification regardless of whether the institution is a $500 billion bank or a Series B payments startup. The obligations don't scale with headcount, but the risk of getting it wrong, in regulatory penalties, exam findings, and reputational damage, absolutely scales with the size of the book.

FinCEN expects the same quality of UBO identification regardless of whether the institution is a $500 billion bank or a Series B payments startup.

Fintech BSA AML on a Small Team: Where Things Break

The failure points are predictable. First, UBO forms that rely on self-certification without any automated cross-referencing against business registry data. Second, no mechanism to capture ownership changes mid-lifecycle. Third, manual SAR filing workflows that don't have bandwidth to review complex ownership chains before a reporting deadline. Fourth, inconsistent risk scoring for legal entities, because the scoring model was built for consumer accounts and never adequately extended to business accounts with layered structures.

The fifth failure point, often overlooked, is training. A fintech analyst who reviews 50 consumer KYC cases a day may not recognize the red flags specific to legal entity beneficial ownership, because those patterns look different from synthetic identity fraud or account takeover indicators.

AML Risk Assessment Guide for Resource-Constrained Fintechs

An aml risk assessment guide for a small fintech team should distinguish clearly between inherent risk and residual risk. Inherent risk for a legal entity customer is driven by the nature of the business, the jurisdictions involved, the ownership structure complexity, and expected transaction patterns. Residual risk factors in the controls applied: what verification steps ran, what screening was done, and what the monitoring rules look like. For high inherent risk customers, a lean compliance team still needs to document that residual risk reduction is real, not just assumed. This is precisely why regulatory compliance automation has become a critical investment area for growth-stage fintechs trying to stay ahead of exam risk without hiring their way to compliance.

BSA/AML Compliance Checklist: What Banks Must Verify for Each Account

A practical bsa aml compliance checklist for legal entity accounts should cover the following items before the account goes active.

- Collect articles of incorporation or organization

- Identify all natural persons owning 25% or more (or a lower threshold where risk-based policy requires it)

- Identify at least one control person

- Collect government-issued ID for each beneficial owner and control person

- Verify identity against at least one independent source, not just the customer's attestation

- Screen all identified persons against the OFAC SDN list, FinCEN 314(a) list, and PEP databases

- Run adverse media searches on beneficial owners and the entity itself

- Assess source of funds and expected transaction profile

- Assign a risk rating and document the basis for that rating

- Set monitoring rules appropriate to the assigned risk rating

For bsa aml compliance community banks, this list tends to be executed manually through spreadsheets and a core banking system that was never designed for this workflow. The result is inconsistent documentation, which creates the gaps examiners find.

What Goes on a BSA AML Compliance Checklist for Community Banks

Community banks face specific examination pressure from OCC, FDIC, or Federal Reserve examiners who look hard at BSA compliance during safety and soundness reviews. The most common finding is documentation deficiency: the bank did the work but can't show it. A well-structured checklist should capture not just what was collected but when, by whom, and what decision it supported. Digitizing this in purpose-built aml compliance software rather than a shared drive of PDFs is the difference between a clean examination and an extended supervisory conversation about remediation timelines.

Tiered Verification: When Standard CDD Isn't Enough

Some accounts need more than the standard four-prong CDD process. Triggers for tiered verification include: complex ownership structures with more than two layers, beneficial owners in FATF grey-listed or black-listed jurisdictions, any PEP as a beneficial owner or family member, and industries with elevated money laundering typology exposure like real estate, money services businesses, or cryptocurrency. The same layered ownership complexity that creates UBO challenges in banking surfaces in insurance and supply chain contexts too. The post on KYC and AML verification for insurance claims directors covers how beneficial ownership issues appear in policy issuance, which is worth reading alongside this one.

SAR Filing and CTR Filing Rules: When UBO Data Triggers Reporting

UBO data is not just an onboarding control. It feeds directly into the ongoing monitoring and reporting obligations that define the operational core of any AML program.

SAR filing is required within 30 days of detecting suspicious activity, with a 60-day extension available if no suspect has been identified. Sar filing efficiency depends heavily on having accurate UBO data at the point of investigation. When an analyst flags a transaction as potentially suspicious, the first question is usually: who is the actual human being benefiting from this activity? If the beneficial owner records are incomplete, the SAR narrative is weaker, the investigation takes longer, and the filing deadline gets tight.

SAR Filing Best Practices When Ownership Structures Are Opaque

A suspicious activity report guide for complex entity cases should start with ownership chain mapping. Before writing the SAR narrative, the analyst needs a clear picture of the beneficial ownership structure and what the flagged transaction pattern looks like in that context. Sar filing best practices include: naming all identified beneficial owners in the SAR subject fields, documenting what verification was done and what gaps remain, cross-referencing prior SARs on the same entity or related persons, and coordinating with the BSA Officer before filing on cases involving a complex or ambiguous ownership structure. The sanctions screening automation strategy covers the adjacent challenge of keeping sanctions data current, which is directly relevant to SAR cases where a beneficial owner may be on a designated list.

Suspicious Activity Report Guide: Documenting UBO Red Flags

Red flags specific to UBO include: a customer refusing to identify beneficial owners, providing identification documents that don't match corporate registry records, changing the named beneficial owners shortly after a large transaction, or having beneficial owners in jurisdictions that don't match the stated business rationale. Any one of these alone may not be sufficient for a SAR, but each should be documented in the customer's risk file and weighed in combination with observed transaction behavior. The key is building a file that tells a coherent story, because a SAR narrative built on scattered notes rarely survives regulatory scrutiny.

CTR Filing Rules and Structuring Patterns to Watch

CTR filing rules require a Currency Transaction Report for cash transactions exceeding $10,000 in a single business day. The UBO angle is structuring risk: breaking transactions into smaller amounts to avoid the reporting threshold is harder to detect when compliance teams don't have clear ownership maps. If two accounts are controlled by the same beneficial owner, aggregate transaction monitoring across those accounts is required. Without accurate UBO data linking the two accounts, the structuring pattern is invisible to the monitoring system. Sar filing requirements 2026 updates are expected to tighten documentation timelines for digital asset-related suspicious activity, adding additional pressure on UBO data quality for crypto-adjacent customers.

KYC Automation 2026: Anti Money Laundering Technology That Makes UBO Tractable

The reason UBO verification has been so operationally expensive is that the process was almost entirely manual: PDF forms, document uploads, manual screening queries, human review of corporate registry records across multiple jurisdictions. Kyc automation changes the economics substantially.

Modern aml compliance software platforms can pull beneficial ownership data from registered agent databases, corporate registries, and the FinCEN BOI database in near real-time. They construct ownership graphs automatically, flagging circular ownership structures and identifying the natural persons at the end of every ownership chain. They screen the full ownership graph against sanctions lists, PEP databases, and adverse media sources in seconds rather than hours. For compliance teams running kyc automation 2026 evaluations, the key questions are: how does the system handle multi-jurisdiction entities, how does it manage ownership chain depth, and what's the false positive rate on sanctions screening?

Anti Money Laundering Technology 2026: Key Capabilities

Anti money laundering technology 2026 in the UBO space should include at minimum: automated beneficial ownership graph construction, real-time corporate registry data integration across key jurisdictions, risk scoring that accounts for jurisdictional risk and ownership complexity, integrated PEP and sanctions screening, and audit-ready documentation of every verification step. Detection accuracy matters, but so does explainability. An examiner who asks how a system determined that a person was not a beneficial owner needs a documented answer, not a black-box model output. The analysis in how agentic AI cuts compliance false positives covers how AI-driven tools reduce alert noise in adjacent risk domains, which applies directly to UBO screening alert management.

SAR Filing Requirements 2026 and What Automated Systems Track

Sar filing requirements 2026 will place greater emphasis on the quality of supporting documentation, not just the timeliness of filing. Automated systems that log every screening query, every ownership graph snapshot, and every risk rating change create the evidentiary record that makes a SAR narrative credible and defensible. The EU AI Act obligations for high-risk AI systems in financial services also require logging of model outputs and human review checkpoints. Institutions deploying automated UBO tools need to factor compliance with both AML rules and AI governance requirements into procurement decisions, because a tool that satisfies one regulator but not the other creates its own category of risk.

- Ultimate beneficial ownership refers to the natural persons who, directly or indirectly, own or control a legal entity.

- Ultimate beneficial owner verification requirements didn't emerge from a single rule.

- The mechanical process of ultimate beneficial owner verification breaks into three stages: collection, verification, and ongoing monitoring.

- Aml compliance fintech teams face UBO challenges that are structurally different from large bank programs.

- A practical bsa aml compliance checklist for legal entity accounts should cover the following items before the account goes active.

Onboard Customers in Seconds

Conclusion

Ultimate beneficial owner verification is one of the few AML controls that genuinely tests whether a compliance program is serious or just well-documented. Shell companies, layered ownership, and cross-jurisdictional structures exist throughout the legitimate economy, but they're also the standard toolkit of financial crime. Institutions that get UBO right, by building accurate ownership maps at onboarding, keeping them current through the customer lifecycle, and using that data to sharpen SAR filing and transaction monitoring, are in a fundamentally different position than those treating UBO as a one-time checkbox.

The operational reality for most compliance teams is that doing this well at scale requires aml compliance software and kyc automation 2026 capabilities that handle the graph complexity and screening volume that manual processes cannot. The regulatory direction, from FinCEN's BOI database to AMLA in Europe to EU AI Act obligations for automated CDD tools, is pushing institutions toward more systematic and auditable UBO processes. Teams that build that infrastructure now will be ahead of the next examination cycle, not scrambling to explain gaps in it.

Share this article