.webp)

Introduction

SAR filing best practices 2026 have shifted considerably as regulators sharpen their expectations for suspicious activity reporting quality, not just volume. If your compliance program is still built around filing as many SARs as possible with minimal narrative detail, the approach is likely generating examination findings without generating useful intelligence. This suspicious activity report guide covers the regulatory updates that matter this year, how to build an efficient filing process that holds up under scrutiny, and what AML compliance software can realistically automate. The goal is a practical reference for compliance officers and BSA analysts, not a recap of every regulatory memo published since January.

- What Is a Suspicious Activity Report and Why Filing Quality Matters

- SAR Filing Requirements 2026: Key Regulatory Updates

- How to Build a BSA/AML Compliance Checklist That Passes Scrutiny

- AML Compliance Software: What Actually Matters in 2026

- KYC Automation and Enhanced Due Diligence in 2026

Onboard Customers in Seconds

What Is a Suspicious Activity Report and Why Filing Quality Matters

A Suspicious Activity Report is a mandatory disclosure filed with FinCEN when a financial institution detects transactions or patterns that may indicate money laundering, fraud, terrorist financing, or other BSA-covered crimes. The obligation covers banks, credit unions, broker-dealers, money services businesses, casinos, and a growing number of fintech companies operating as money transmitters or prepaid card issuers.

What examiners focus on in 2026 is not the number of SARs filed but their quality: complete narratives, accurate transaction data, correct beneficiary identification, and timely submission. A SAR filed on time with a vague or incomplete narrative often results in the same examination finding as a SAR filed late.

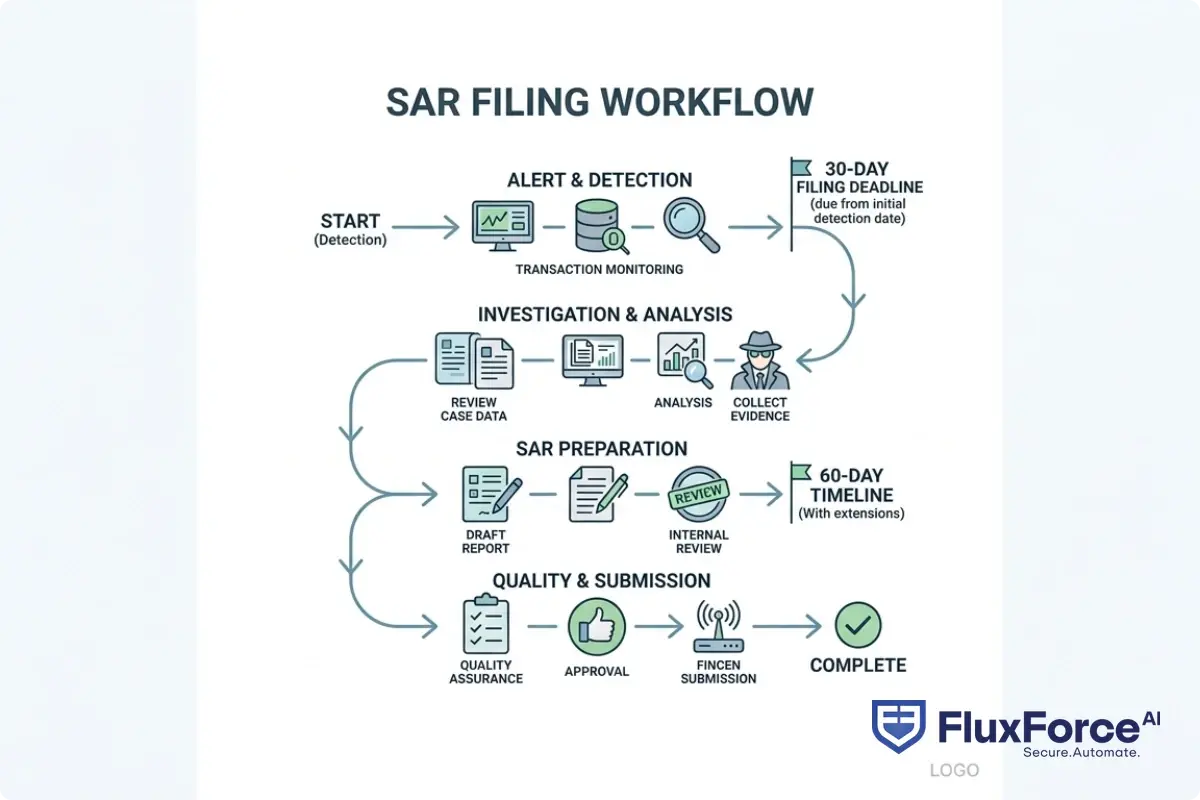

Who Must File and the 30/60-Day Rule

Filing deadlines run from the date suspicious activity is detected, not the date of the underlying transaction. The standard window is 30 calendar days, extending to 60 days when no suspect has been identified. Banks, money services businesses, and broker-dealers each operate under slightly different threshold rules, so your BSA AML compliance checklist should specify the applicable regulation (31 CFR Part 1020, 1022, or 1023) for each business line your program covers.

Late SARs are among the most common examination findings. Tracking the time from alert generation to SAR submission is a basic metric that every program should monitor monthly.

What Makes a High-Quality SAR Narrative

A strong SAR narrative answers who, what, when, where, how, and why in plain English. FinCEN's feedback consistently flags vague language ("transaction was inconsistent with customer profile"), missing transaction details, and narratives copied verbatim from prior filings without reflecting current activity. Aim for 250-400 words, include specific dollar amounts and dates, and explain why the activity is suspicious rather than merely describing what happened. FinCEN has published narrative guidance on its website that is worth reviewing annually.

SAR Filing Requirements 2026: Key Regulatory Updates

SAR filing requirements 2026 reflect two significant developments: expanded BSA obligations for digital asset service providers and increased examiner attention to continuing activity SAR programs. Both require process changes that go beyond policy updates.

Digital Assets and the BSA Reporting Expansion

FinCEN's recent rulemaking has brought cryptocurrency exchanges, digital asset custodians, and certain blockchain-based payment processors more firmly under BSA reporting requirements. If your institution handles digital asset transactions, the monitoring and filing process mirrors traditional payment rails: document your detection methodology, set risk-based thresholds, and file when activity meets the suspicious activity standard. Anti money laundering technology vendors have added blockchain analytics to their transaction monitoring suites, but the governance requirements are identical to those for wire transfers and ACH. The detection logic differs; the compliance framework does not.

Continuing Activity SARs and the 90-Day Cycle

When suspicious activity is ongoing, institutions must file continuing activity SARs at 90-day intervals for as long as the behavior continues. This is one of the most common gaps in community bank and fintech SAR programs: case management workflows close cases after the initial filing, and no one sets the 90-day follow-up. Add calendar triggers to every open SAR case, and specify in your procedures who reviews and approves continuing SARs before submission. The gap between initial SAR and required follow-up filing is a finding that examiners catch consistently.

CTR Filing Rules and the Structuring Connection

CTR filing rules require Currency Transaction Reports for cash transactions over $10,000. CTRs and SARs serve different regulatory purposes but interact directly in practice. A customer who consistently deposits $9,500 in cash to stay under the reporting threshold is committing structuring under 31 U.S.C. § 5324, and that pattern is itself a SAR trigger independent of whether a CTR was ever filed. Your transaction monitoring rules should flag structuring behavior as a distinct alert type, not merely as a CTR-adjacent issue.

CTR filing rules require Currency Transaction Reports for cash transactions over $10,000.

How to Build a BSA/AML Compliance Checklist That Passes Scrutiny

A practical BSA AML compliance checklist is the operational backbone of a SAR program, translating regulatory requirements into concrete steps that every analyst follows consistently.

Core Elements of the Checklist

Every BSA AML compliance checklist for a SAR program should cover: alert triage criteria and escalation thresholds, investigation documentation standards, filing deadline tracking from detection to submission, SAR narrative quality review before filing, and five-year recordkeeping for SARs and supporting case files. The FFIEC BSA/AML Examination Manual is the most detailed reference for what examiners expect at each stage, and it is updated periodically as regulatory guidance evolves. Align your checklist to the manual's examination procedures directly so there is no gap between what examiners look for and what your program documents.

Risk-Based Calibration

Not every alert warrants the same investigation depth. A risk-based approach directs analyst time toward high-risk indicators: high-value cross-border transactions, rapid fund movement inconsistent with customer profile, and activity that contradicts the stated business purpose. Document your risk scoring methodology explicitly. When an examiner asks how you decided a particular alert did not warrant a SAR, "analyst judgment" without a documented decision framework is an examination finding. The decision not to file is as important to document as the decision to file.

AML Risk Assessment Guide for Your Program

An aml risk assessment guide evaluates your institution's products, services, customers, and geographic exposure against known financial crime typologies. The output is a written document approved by your board and reviewed by examiners at the start of every exam cycle. FATF's risk-based approach guidance provides the international framework that most U.S. regulators reference when evaluating the quality of institutional risk assessments. Update the document at least annually or whenever your product or customer mix changes significantly.

AML Compliance Software: What Actually Matters in 2026

The market for AML compliance software has grown considerably, with platforms now claiming to automate everything from transaction monitoring to SAR narrative generation. No software removes the need for human judgment on the decision to file, but the right tool meaningfully improves SAR filing efficiency and reduces time spent on low-value alert triage.

Anti Money Laundering Technology Core Features

Anti money laundering technology in 2026 falls into three practical categories: transaction monitoring engines, case management platforms, and KYC or identity verification tools. Core evaluation criteria include real-time vs. batch processing capability, rule-based vs. machine learning detection, case management with complete audit trails, SAR pre-population functionality, and how the system handles regulatory updates. Anti money laundering technology 2026 increasingly incorporates graph analytics to surface networks of related accounts that individual transaction-level rules miss entirely. Point-in-time transaction analysis alone is no longer adequate for catching sophisticated layering schemes.

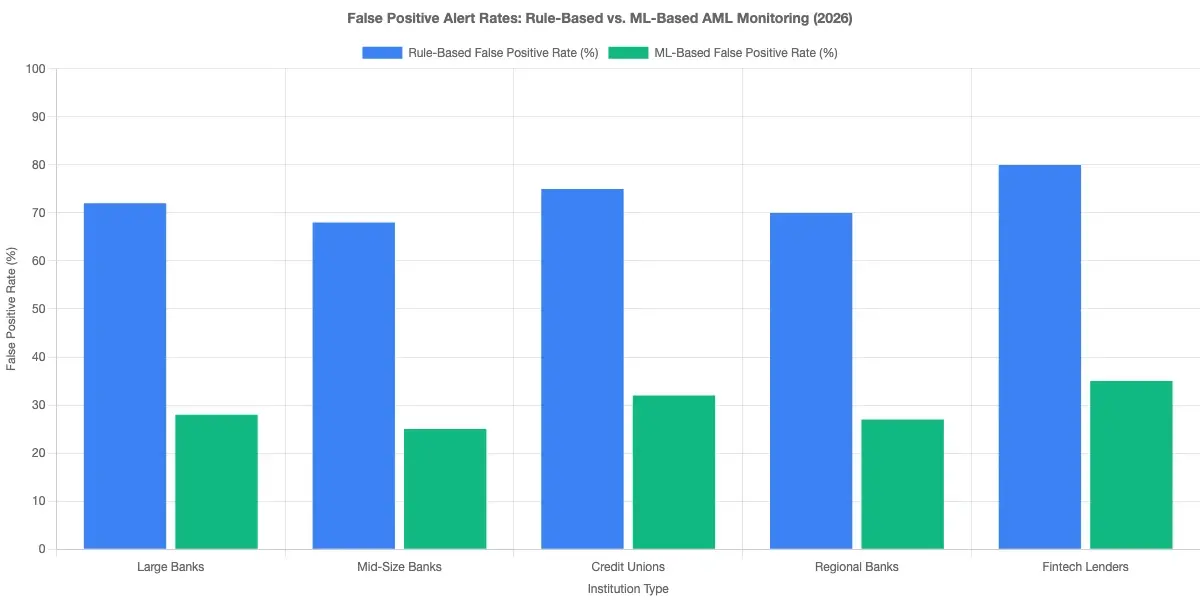

How AML Compliance Software Reduces False Positives

Traditional rule-based transaction monitoring generates false positive rates commonly cited between 90% and 95%. Analysts spend the majority of their time clearing alerts that turn out to be routine customer behavior. AML compliance software with machine learning reduces alert volume by 30-50% for institutions with sufficient historical data to train models effectively. The critical question to press vendors on: what is the false negative rate, and how is it measured independently? A 40% reduction in alert volume means nothing if legitimate suspicious activity is being filtered out in the process.

Traditional rule-based transaction monitoring generates false positive rates commonly cited between 90% and 95%.

Integration and Data Requirements

Any AML compliance software deployment will surface data quality problems you did not know existed: missing counterparty identifiers, incomplete customer records, inconsistent account numbering across core banking systems. These gaps degrade model performance and create audit trail deficiencies. Before selecting a vendor, run a data completeness audit on your core transaction and customer data. The integration project typically takes three to six times longer than the procurement process suggested it would.

KYC Automation and Enhanced Due Diligence in 2026

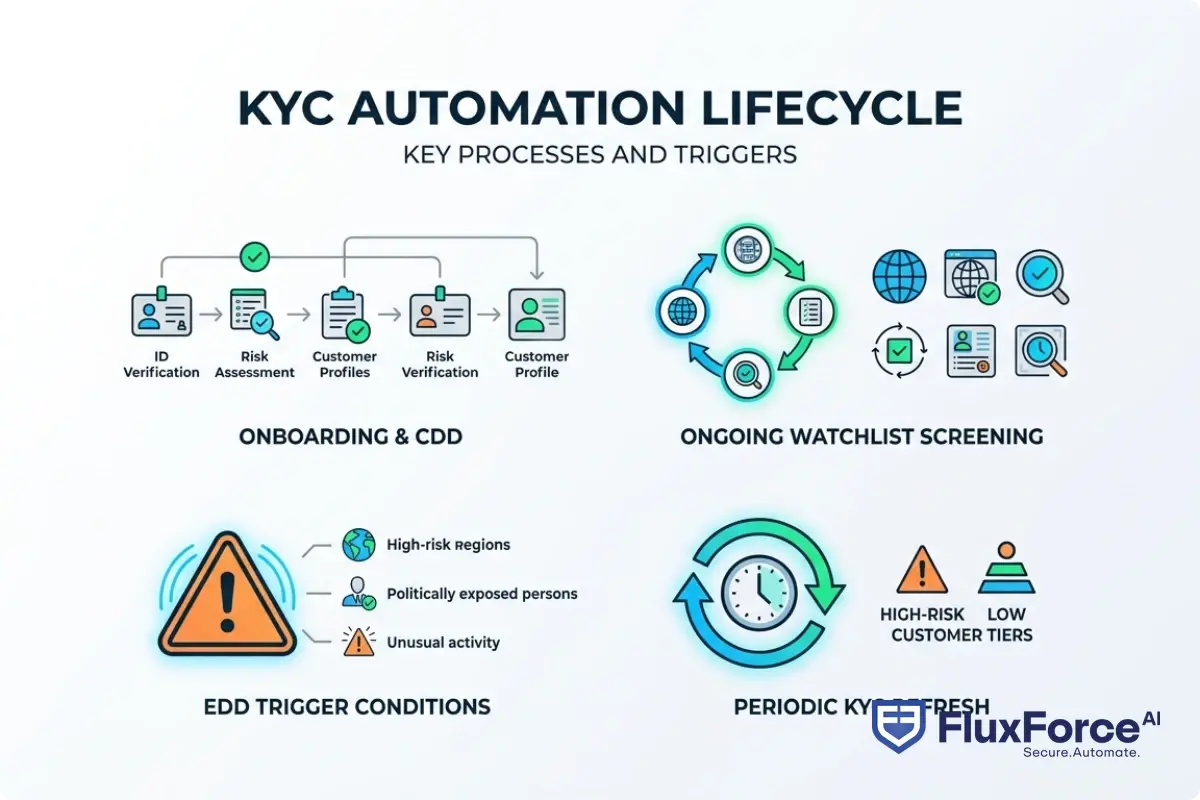

KYC automation 2026 is operational at most financial institutions for onboarding workflows, but the depth and reliability of that automation varies significantly by customer risk tier and the quality of the underlying data.

KYC CDD Requirements for Banks

KYC CDD requirements for banks in the U.S. are governed by FinCEN's Customer Due Diligence Rule, which requires collecting and verifying the identity of beneficial owners of legal entity customers, specifically anyone with 25% or more ownership interest plus one controlling person. The Corporate Transparency Act's beneficial ownership registry provides a new verification pathway, though private-sector access for real-time lookup remains limited in 2026. Ask your KYC automation vendor for their roadmap on integrating FinCEN beneficial ownership database access as that access expands over the coming 12 months.

are governed by FinCEN's Customer Due Diligence Rule, which requires collecting and verifying the identity of beneficial owners of legal entity customers, specifically anyone with 25% or more ownership interest plus one controlling person.

Enhanced Due Diligence Guide for High-Risk Customers

Enhanced due diligence (EDD) applies to politically exposed persons, customers in high-risk jurisdictions, correspondent banking relationships, and private banking clients. A practical enhanced due diligence guide for 2026 specifies the additional information collected for each high-risk category (source of wealth, source of funds, relationship purpose, expected transaction volume), the approval authority required to onboard or retain the relationship, and the review frequency. KYC automation tools handle the workflow and data collection efficiently at scale, but the risk judgment at the EDD level requires a human reviewer with documented decision authority.

Ongoing Monitoring and KYC Refresh

KYC automation 2026 delivers its clearest efficiency gains in ongoing monitoring: automated sanctions and PEP watchlist screening, behavioral scoring relative to the customer's stated profile, and event-triggered KYC refresh when risk indicators change. Governance matters here. Model drift in behavioral scoring creates blind spots over time. Build periodic validation into your model oversight schedule, including back-testing against known typologies to confirm the system is still flagging the patterns it was trained on.

SAR Filing Best Practices for Fintechs and Community Banks

AML compliance fintech programs and community bank BSA programs share similar resource constraints, and both operate under examination standards that do not adjust for institution size.

Fintech BSA AML with a Small Team

The most common failure mode in a fintech BSA AML small team program is an alert volume that exceeds the team's capacity to work cases within the 30-day filing window. Before deploying any new monitoring rule, estimate the alert volume it will generate and verify you have analyst capacity to close those cases before the deadline. Filing fewer, higher-quality SARs almost always produces better examination outcomes than high-volume, low-quality filings. AML compliance fintech teams should also maintain a documented escalation path from the BSA officer to legal counsel for fact patterns that fall outside existing typologies, particularly for digital asset-related activity.

BSA AML Compliance for Community Banks

BSA AML compliance community banks are expected to meet the same examination standards as large institutions. What examiners accept is a well-documented, risk-based program: written justification for where monitoring thresholds are set, a risk assessment calibrated to the bank's specific customer base and products, and a corrective action history showing the program identifies and addresses gaps proactively. A community bank with 15 thorough, well-documented SARs is in better examination shape than one with 200 low-quality filings and no written rationale for its monitoring approach.

Shared Services and Third-Party BSA Programs

Several core processors and specialized compliance vendors offer BSA compliance shared services to community banks and credit unions. The arrangement can be cost-effective, but the compliance responsibility stays with your institution. You remain accountable for every SAR filed under your name, the adequacy of your risk assessment, and the completeness of your case documentation. Build active oversight governance if you use a managed BSA service rather than treating it as a fully delegated function.

How Anti Money Laundering Technology 2026 Is Changing the Compliance Function

Anti money laundering technology 2026 is evolving faster than regulatory guidance in some areas, which creates genuine efficiency opportunities alongside real governance risks for institutions that adopt new tools without adequate oversight structures.

AI and Machine Learning in Transaction Monitoring

Machine learning models in transaction monitoring detect novel typologies that rule-based systems miss, adapt to evolving customer behavior, and surface entity relationship networks that traditional alert logic cannot process. They also require explainability for regulatory purposes. If your model flags a transaction as suspicious, you need to explain why in a SAR narrative that an examiner and a federal prosecutor can follow. The EU AI Act financial services provisions classify AML transaction monitoring as a high-risk AI application, requiring documented conformity assessments, human oversight procedures, and decision audit logs. Even for U.S. institutions not directly subject to the EU AI Act, these documentation practices set a useful standard for demonstrating model governance to domestic examiners.

What EU AI Act Compliance Means Practically

EU AI Act financial services requirements for high-risk systems include pre-deployment risk assessments, ongoing model drift monitoring, documented human oversight requirements, and audit logs for algorithmic decisions. If your institution uses a vendor whose AML model is deployed across EU-regulated entities, these requirements affect your vendor oversight process now. Ask vendors for their conformity assessment documentation and their change notification process when models are retrained or updated. The documentation standard is a useful baseline regardless of jurisdiction.

Building a Program That Holds Up Long-Term

The most durable AML compliance programs are built for examination readiness, not just operational throughput. SAR filing efficiency matters, but a program that files quickly and cannot explain its detection methodology to an examiner is still a failed program. Build policy documentation that reflects actual practice, run controls testing on a scheduled basis, and maintain a written corrective action log. Examiners weigh proactive gap identification and documented remediation heavily when assessing program maturity. When you find issues before the exam, fix them and document the fix.

- A Suspicious Activity Report is a mandatory disclosure filed with FinCEN when a financial institution detects transactions or patterns that may indicate money laundering, fraud, terrorist financing, or other BSA-covered crimes.

- SAR filing requirements 2026 reflect two significant developments: expanded BSA obligations for digital asset service providers and increased examiner attention to continuing activity SAR programs.

- A practical BSA AML compliance checklist is the operational backbone of a SAR program, translating regulatory requirements into concrete steps that every analyst follows consistently.

- The market for AML compliance software has grown considerably, with platforms now claiming to automate everything from transaction monitoring to SAR narrative generation.

- KYC automation 2026 is operational at most financial institutions for onboarding workflows, but the depth and reliability of that automation varies significantly by customer risk tier and the quality of the underlying data.

Onboard Customers in Seconds

Conclusion

SAR filing best practices 2026 require compliance teams to operate on two tracks simultaneously: staying current on regulatory updates including digital asset obligations, beneficial ownership data access, and AI governance requirements, while tightening the operational fundamentals that examiners measure directly. AML compliance software and kyc automation tools reduce manual workload substantially, but only when the underlying data quality and governance structure support them. For fintech BSA AML programs and BSA AML compliance community banks managing obligations with lean teams, the practical priority is a well-documented, risk-based approach over high filing volumes. Audit your false positive rate, your average time from detection to filing, and your SAR narrative quality on a quarterly basis. Those three metrics tell you where your program actually stands.

Share this article