.webp)

Listen To Our Podcast🎧

Introduction

Reusable digital identity is no longer a theoretical construct sitting in a standards body workgroup: financial institutions are actively building the infrastructure now, and early pilot deployments are already demonstrating measurable reductions in onboarding friction. The premise is straightforward. A person proves who they are once, through a rigorous document check and biometric capture, and that verified credential travels with them across every subsequent institution or service interaction. No fresh passport upload. No new selfie. No duplicate compliance cost. This article walks through what reusable digital identity actually requires to work, why synthetic identity fraud and deepfake threats complicate the picture, and what enterprise compliance and security teams need to evaluate before committing to a specific architecture.

- What Is Reusable Digital Identity and Why Does It Matter?

- The Real Cost of Fragmented Identity Verification in Fintech

- How Reusable Digital Identity Works in Practice

- Synthetic Identity Fraud: The Threat Reusable ID Must Address

- Zero Trust Financial Services and Reusable Identity

Onboard Customers in Seconds

What Is Reusable Digital Identity and Why Does It Matter?

Reusable digital identity refers to a verified identity credential that an individual establishes once and can present to multiple relying parties (banks, insurers, fintechs) without repeating the full verification process. Think of it as a portable proof of identity with a cryptographic signature confirming it was issued by an accredited verifier and has not been tampered with since.

The difference from traditional KYC is structural. In the traditional model, each institution holds its own copy of verification data, runs its own checks, and bears its own compliance cost. With reusable digital identity, a trusted identity provider holds the verified credential, and downstream institutions query it through a standardized identity verification API rather than re-running the entire proofing sequence.

The Problem with Repeating KYC Checks

The average regulated financial institution performs full document verification, biometric capture, and sanctions screening at every new customer relationship. For a customer who banks with three institutions and holds two insurance policies, that is five separate KYC events for what is, legally and factually, one person. Each event takes anywhere from 4 to 15 minutes of active user time, and industry data consistently shows that abandonment during lengthy KYC flows costs financial services firms hundreds of millions annually in lost conversions alone. The friction is measurable, the duplication is obvious, yet the industry has been slow to act because the coordination problem is genuinely hard.

Each event takes anywhere from 4 to 15 minutes of active user time, and industry data consistently shows that abandonment during lengthy KYC flows costs financial services firms hundreds of millions annually in lost conversions alone.

How a Verified Identity Credential Works

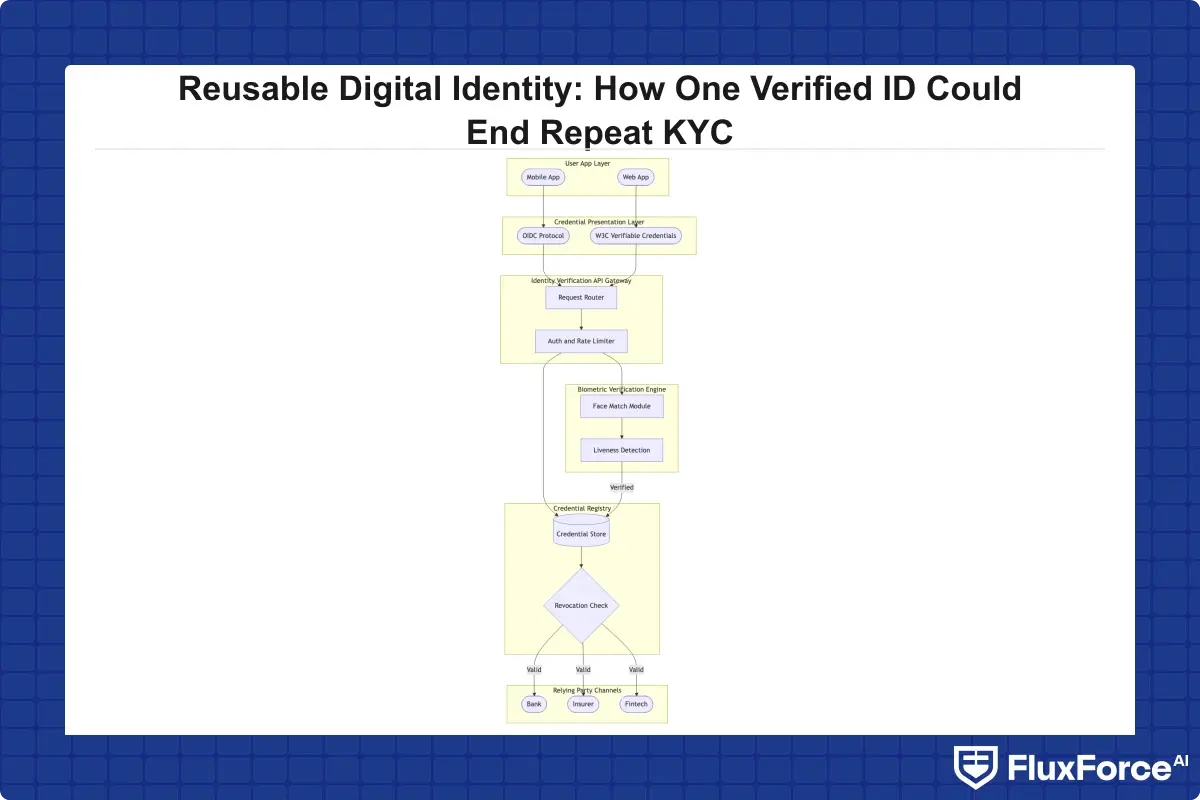

A verified identity credential contains three elements: the proofing outcome (identity confirmed at a given assurance level), the biometric binding (a hash that links the credential to a specific person's biometric data without storing the raw biometric), and a validity signal (either an expiry timestamp or a real-time revocation check). When a new institution needs to verify the user, it queries the credential provider through an identity verification API, receives a signed attestation, and records the result. The underlying document image and biometric template never leave the original proofing system, which matters for both privacy compliance and security architecture.

The Real Cost of Fragmented Identity Verification in Fintech

Identity verification fintech vendors have made substantial improvements in the speed and accuracy of individual checks. The problem is not the quality of any single check: it is that the industry runs thousands of redundant checks on the same individuals every day. That redundancy has hard costs (verification fees, compliance headcount, document storage) and soft costs (customer drop-off, slower time-to-revenue, and the accumulated privacy risk of holding sensitive document images across dozens of separate systems).

KYC Onboarding Speed: What the Numbers Show

KYC onboarding speed is one of the most closely watched operational metrics in digital banking right now. Manual review pipelines average 3 to 7 business days for complex cases. AI-assisted pipelines with automated document classification and biometric matching clear straightforward cases in under 90 seconds. When a reusable digital identity credential is available, that time collapses further: the institution skips document capture entirely and queries the credential directly. Pilot programs in the EU under eIDAS 2.0 have demonstrated same-session onboarding for returning customers across participating institutions, which is a significant shift from the current multi-day norm.

Compliance Overhead That Compounds Over Time

Every institution holding its own KYC data is also holding its own compliance liability: document retention policies, subject access request obligations under GDPR, and ongoing sanctions re-screening against stored profiles. The overhead compounds as the customer relationship ages. Reusable digital identity shifts much of that burden back to the original identity provider, which is purpose-built to manage it. For a compliance team at a mid-sized bank processing 50,000 customer records annually, that represents a meaningful reduction in both risk surface and operational cost. The case for digital identity proofing consolidation is ultimately a cost reduction argument as much as it is a user experience one.

For a compliance team at a mid-sized bank processing 50,000 customer records annually, that represents a meaningful reduction in both risk surface and operational cost.

How Reusable Digital Identity Works in Practice

Moving from concept to implementation requires decisions across four layers: the proofing standard (what assurance level the original check must meet), the biometric identity verification method, the liveness detection approach, and the identity verification API design.

Biometric Identity Verification as the Foundation

Biometric identity verification is the anchor of any reusable credential. The original proofing event must capture a biometric sample (typically a facial scan) that is then bound to the credential with sufficient precision to reject a different person presenting the same document. The National Institute of Standards and Technology's Digital Identity Guidelines (NIST SP 800-63) define three Identity Assurance Levels, with IAL2 and IAL3 requiring supervised remote or in-person biometric verification. Any reusable credential intended for financial services onboarding should meet at least IAL2. Institutions accepting credentials that only meet IAL1 (self-asserted, no biometric) are accepting a level of identity risk that most compliance frameworks would not support for regulated account opening.

Liveness Detection and Deepfake Defense

Liveness detection fraud is the category that keeps identity architects up at night. A credential bound to a stolen or synthesized face photograph is essentially worthless. Modern liveness detection systems combine active challenges (asking the user to blink or turn their head) with passive analysis (detecting the micro-reflections and depth cues that distinguish a live face from a printed image or screen replay). Deepfake detection banking is now a specific sub-discipline: generative adversarial networks have made synthetic faces good enough to fool human reviewers, so the detection pipeline must include frame-level artifact analysis and 3D depth estimation. Organizations considering reusable digital identity for high-value transactions should verify that the underlying proofing system has been independently tested against Tier-2 presentation attacks, not just basic spoofing.

The Role of Identity Verification APIs

The identity verification API layer determines how easily a reusable credential integrates into an institution's existing onboarding flow. A well-designed API returns a structured response including the assurance level achieved, the biometric match score threshold (without the raw score, for privacy), the sanctions and PEP screening outcome, and a credential validity signal. Institutions should look for APIs supporting OpenID Connect for Verifiable Credentials, the emerging standard for interoperability across identity networks. The FluxForce KYC/AML automation platform connects biometric proofing, sanctions screening, and API delivery into a single workflow, reducing the integration surface that compliance teams must manage across multiple point solutions.

Synthetic Identity Fraud: The Threat Reusable ID Must Address

Reusable digital identity does not automatically solve synthetic identity fraud. It reframes the problem in an important way, but institutions need to understand exactly how, because the attack vectors that defeat poorly implemented reusable systems are different from the ones that defeat traditional KYC.

Synthetic Identity Fraud Detection in Real-Time

Synthetic identity fraud detection is one of the harder problems in financial crime because synthetic identities are not stolen: they are manufactured. A fraudster combines a real government identifier (often from a child or someone with a thin credit file) with fabricated personal details to create a profile that passes many automated checks. The Federal Reserve's research on synthetic identity fraud identified it as the fastest-growing form of financial crime in the United States. A reusable credential helps because it binds the identity to a biometric at the point of proofing. If that original proofing is rigorous, the synthetic profile either fails upfront (because the fraudster cannot produce a matching face) or gets flagged when the biometric binding check runs at a downstream institution. For a deeper analysis of real-time detection techniques, see the guide on detecting synthetic identity fraud in real time.

The Federal Reserve's research on synthetic identity fraud identified it as the fastest-growing form of financial crime in the United States.

Why Traditional KYC Misses Synthetic Identities

Traditional KYC processes rely heavily on document authenticity checks and database lookups. If the fabricated profile has a plausible credit history and a genuine document number, the lookup passes. The missing layer is biometric binding: without it, there is no way to confirm that the person presenting the identity today is the same person who established it. Reusable digital identity closes this gap at the credential issuance stage. The fraudster would need to defeat biometric identity verification and liveness detection at the proofing institution before obtaining a credential that passes downstream checks. That is a substantially harder attack surface to exploit than a simple document forgery, which explains why the industry sees reusable credentials as a long-term tool for reducing synthetic fraud losses.

Zero Trust Financial Services and Reusable Identity

A reusable digital identity credential is not a static pass. It should be treated as a dynamic trust signal re-evaluated at each transaction context, which aligns directly with zero trust financial services principles.

Applying a Zero Trust Security Framework to Identity

The zero trust security framework holds that no user, device, or credential should be implicitly trusted based on network location or prior authentication. For identity verification, this means the credential is validated every time it is presented, not just at initial onboarding. The credential provider performs a real-time revocation check, the relying party verifies the biometric binding is still intact, and the session context (device fingerprint, geographic location, transaction risk score) factors into the trust decision. Banks adopting this model find it aligns well with zero trust security architecture strategies for banking operations that treat identity as a continuous control rather than a one-time gate.

Continuous Verification Beyond the Onboarding Gate

Zero trust for identity does not stop at onboarding. The same biometric binding that anchors the original credential can support step-up authentication during high-risk transactions: a wire transfer above a defined threshold, a new payee registration, or an account settings change. This continuous verification model is what separates a reusable identity system from a simple single sign-on arrangement. For institutions already running continuous user verification architectures, adding a portable credential layer is a natural extension of the existing zero trust posture rather than a separate initiative.

Digital Identity Proofing Standards and Regulatory Alignment

Any enterprise deploying reusable digital identity needs clarity on which standards govern acceptable proofing methods and how those standards map to regulatory requirements in their jurisdiction.

NIST and eIDAS: Setting the Identity Assurance Bar

NIST SP 800-63-3 and the EU's eIDAS 2.0 regulation are the two dominant frameworks for digital identity proofing in financial services. NIST defines IAL1 (self-asserted), IAL2 (evidence-supported with remote or in-person proofing), and IAL3 (in-person with biometric collection at the highest assurance level), with financial services typically requiring IAL2 at minimum. eIDAS 2.0 introduces the European Digital Identity Wallet, a standardized credential container usable across EU member states without re-proofing. For institutions operating cross-border, building a reusable identity system that maps to both frameworks from the start is significantly cheaper than retrofitting compliance later, particularly given that eIDAS assurance level High corresponds closely to NIST IAL3.

How Reusable ID Supports AML and KYC Compliance

The question compliance officers often raise is whether a relying institution can depend on another institution's KYC check for AML purposes. The honest answer is: it depends on the jurisdiction and the contractual framework. Financial Action Task Force guidance on digital identity allows institutions to rely on third-party verification under certain conditions, but the relying institution retains responsibility for the customer relationship. Reusable digital identity frameworks built on certified credential providers address this by making the proofing methodology auditable and the assurance level machine-readable. For insurance and other regulated sectors, the parallel challenge around AML in policy issuance is examined in detail in the guide on KYC and AML identity verification for claims teams.

What Banks and Fintechs Need to Build a Reusable ID Stack

Building a reusable identity capability is not a single product purchase. It requires integration decisions across the proofing layer, the credential storage layer, and the relying party query layer.

Choosing an Identity Verification API for Scale

An identity verification API must handle volume spikes without degrading latency or accuracy. Key criteria include: SLA-guaranteed response times under 300ms for credential queries, support for OIDC and W3C Verifiable Credentials standards, geographic data residency options for GDPR compliance, and a transparent false acceptance rate (FAR) specification for the underlying biometric engine. Teams evaluating suppliers should ask specifically about performance on presentation attacks and what the independently audited FAR is at the supplier's recommended operating threshold. For CISOs managing supplier risk across multiple identity technology vendors, the framework for high-risk supplier validation and KYC due diligence applies directly to identity technology partnerships.

Integration Considerations for Enterprise Teams

The integration path depends on whether the institution is building a new onboarding flow from scratch or retrofitting an existing one. Greenfield builds can adopt the credential query model from day one, inserting the identity verification API call in place of the document capture step for users who present a valid credential. Legacy retrofits are more complex: the existing flow typically has hard-coded document handling logic, and inserting a credential path requires a routing layer that checks credential availability before falling back to traditional proofing. Most enterprise teams find that a phased rollout, starting with new-to-bank digital customers before extending to existing customers, delivers measurable kyc onboarding speed improvements within the first quarter of deployment without disrupting established customer journeys.

- Reusable digital identity refers to a verified identity credential that an individual establishes once and can present to multiple relying parties (banks, insurers, fintechs) without repeating the full verification process.

- Identity verification fintech vendors have made substantial improvements in the speed and accuracy of individual checks.

- Moving from concept to implementation requires decisions across four layers: the proofing standard (what assurance level the original check must meet), the biometric identity verification method, the liveness detection approach, and the identity verification API design.

- Reusable digital identity does not automatically solve synthetic identity fraud.

- A reusable digital identity credential is not a static pass.

Onboard Customers in Seconds

Conclusion

Reusable digital identity solves a problem that every compliance officer, CISO, and onboarding product manager in financial services knows intimately: verified identity data already exists, yet institutions keep asking customers to prove themselves again from scratch. The goal is not just better convenience. It is building a verification infrastructure resistant to synthetic identity fraud, capable of supporting zero trust financial services architectures, and aligned with the emerging regulatory standards under NIST and eIDAS 2.0. The institutions that move first will gain a measurable advantage in digital identity proofing efficiency, compliance cost reduction, and customer trust. The technology is ready. The standards are converging. The question for enterprise teams is whether their integration roadmap reflects that reality yet.

Share this article