.webp)

Listen To Our Podcast🎧

Introduction

RegTech compliance automation is reshaping how banks, fintechs, and insurers handle anti money laundering technology, but the headline most vendors push is wrong. Software is not replacing compliance teams. It is removing the parts of the job that exhausted them, freeing analysts to do the work that actually catches financial crime. In our experience working with mid-sized banks and fintechs, the teams that scaled best in the last two years are the ones that paired RegTech compliance automation with experienced analysts, not the ones that tried to swap people for platforms.

This is the honest case for augmentation over replacement, with specifics on SAR filing, KYC automation, and where humans still beat the machine.

- Why the "RegTech Will Replace Compliance Teams" Narrative Misses the Point

- What RegTech Compliance Automation Actually Does in 2026

- Where Humans Still Outperform the Machine

- The BSA AML Compliance Checklist for Augmented Teams

- How SAR Filing Efficiency Actually Improves

Onboard Customers in Seconds

Why the "RegTech Will Replace Compliance Teams" Narrative Misses the Point

Walk into any compliance conference and you will hear vendors promise headcount reduction. Talk to the Chief Compliance Officer at a community bank and you will hear something different: alerts up 4x in five years, regulators expecting faster SAR filing, and a team that has not grown since 2021. The pressure is real. The answer is not fewer humans.

The math regulators actually look at

FinCEN received over 4.6 million Suspicious Activity Reports in 2023, according to FinCEN SAR statistics. Behind every filing sits a human decision: was this activity suspicious enough to escalate, and can we defend the narrative if examined? RegTech compliance automation can route, score, and pre-fill, but the signature on the SAR is still a person's professional judgment.

What "automation" really replaces

It replaces copy-paste between systems. It replaces 40-minute manual lookups of beneficial ownership data. It replaces alert queues sorted by alphabetical order instead of risk. None of that was the analyst's high-value work. It was the work that burned them out.

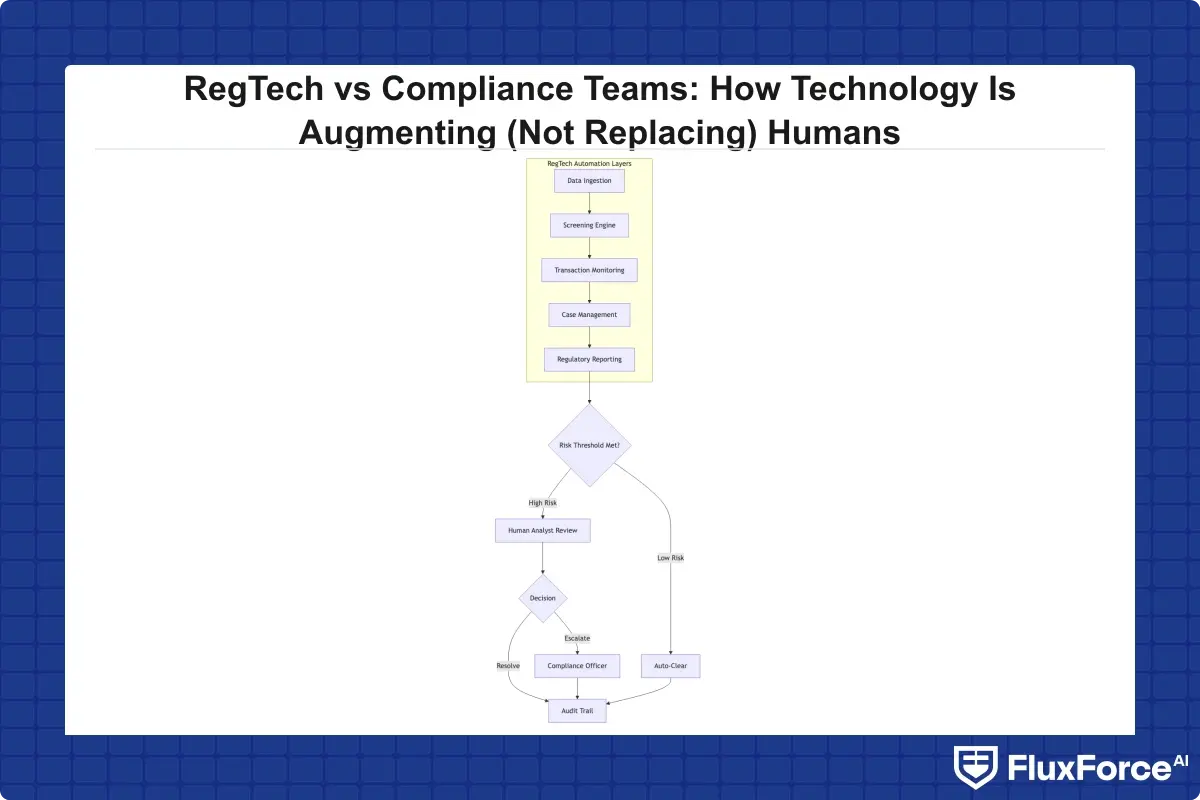

What RegTech Compliance Automation Actually Does in 2026

The modern aml compliance software stack is narrower in ambition than the 2019 pitch decks suggested, and far more useful. It does four things well.

Transaction monitoring with adaptive thresholds

Rule engines that learned only from static thresholds produced false-positive rates north of 95% at most banks. Newer systems built on supervised models, trained on confirmed SARs, push that down to 70-80%, still high, but the alerts that survive are richer. The analyst opens a case that already has counterparty risk scores, peer-group comparisons, and historical context attached.

Rule engines that learned only from static thresholds produced false-positive rates north of 95% at most banks.

KYC automation for onboarding and refresh

Kyc automation in 2026 looks less like a chatbot and more like an orchestration layer: document capture, liveness, sanctions screening, adverse media, beneficial ownership unwrap, and ongoing monitoring all running in parallel and surfacing exceptions to a human reviewer. We have written before about KYC and AML strategies for compliance officers in insurance, and the same pattern applies in banking: kyc automation 2026 is exception-based, not approval-based.

Sanctions and adverse media screening

Name-matching has improved enough that the analyst's job has shifted from "is this the same person" to "is this hit material to the relationship." That is a judgment call, not a string-comparison.

Regulatory reporting and CTR filing rules

Ctr filing rules under the BSA require reporting cash transactions over $10,000, and the aggregation logic for structured transactions is exactly the kind of deterministic work software should own end-to-end. Most banks still have analysts manually reconciling CTR exceptions. That is a fixable problem.

Ctr filing rules under the BSA require reporting cash transactions over $10,000, and the aggregation logic for structured transactions is exactly the kind of deterministic work software should own end-to-end.

Where Humans Still Outperform the Machine

This is the part vendors skip. There are specific compliance tasks where experienced analysts produce materially better outcomes than any model, and pretending otherwise leads to regulatory findings.

Writing the SAR narrative

A SAR narrative is a legal document. It must describe who, what, when, where, why, and how in language an investigator can act on. Models produce passable first drafts; they do not produce defensible final filings. Sar filing best practices still require an analyst to verify entities, reconcile timelines, and write the rationale in their own voice.

Judgment on ambiguous typologies

Trade-based money laundering, nested correspondent banking, third-party processor abuse, these are pattern-recognition problems where context matters more than data volume. An analyst who has worked five similar cases will outperform a model trained on millions of unrelated alerts.

Regulator-facing explanation

When an OCC examiner asks why a particular alert was disposed without filing, the answer cannot be "the model said so." It has to be a documented chain of reasoning a human walked through.

The BSA AML Compliance Checklist for Augmented Teams

If you are reshaping your aml compliance fintech program around augmentation rather than replacement, here is a working bsa aml compliance checklist we use with clients. This is also useful as a bsa aml compliance checklist for community banks running lean teams.

1. Map every manual step to a decision point

Distinguish data movement (automate) from judgment (keep human). If an analyst is copying account numbers into a spreadsheet, that is data movement. If they are deciding whether layering is occurring, that is judgment.

2. Build an aml risk assessment guide tied to your customer base

A generic risk model trained on industry data will miss what makes your portfolio unique. Tune by geography, product, and channel. The FFIEC BSA/AML Examination Manual is the source of truth for what examiners expect here.

3. Tier your alerts before analysts see them

Low-risk auto-dispositions with documented logic, medium-risk to junior analysts, high-risk to senior reviewers. This is where most fintech bsa aml small team setups get the biggest win.

4. Document the model, not just the output

Model risk management under SR 11-7 applies to any aml compliance software that influences SAR filing decisions. Keep validation records, drift monitoring, and override logs.

5. Build a feedback loop from SAR outcomes

When FinCEN or law enforcement requests follow-up on a filing, that signal should retrain your models. Most teams never close this loop.

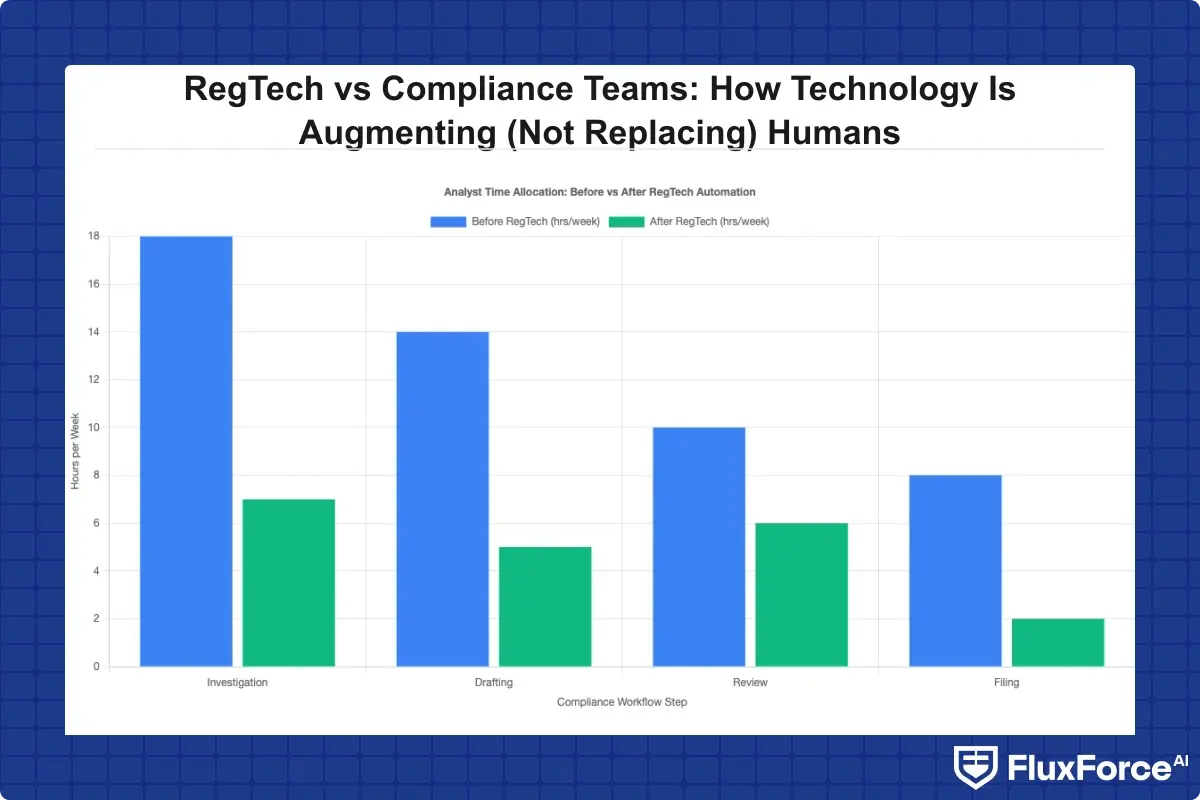

How SAR Filing Efficiency Actually Improves

Sar filing efficiency is the metric most compliance leaders are measured on, and it is widely misunderstood. Cutting time per SAR by 30% sounds good until you realize narrative quality dropped and your regulator noticed.

Cutting time per SAR by 30% sounds good until you realize narrative quality dropped and your regulator noticed.

The real bottleneck is investigation, not drafting

In our deployments, analysts spend roughly 70% of their SAR time on investigation (pulling data, building timelines, verifying counterparties) and 30% on drafting. Anti money laundering technology that focuses on the drafting step misses the bigger opportunity.

What a good suspicious activity report guide looks like in practice

A practical suspicious activity report guide should pre-assemble the investigation packet: transaction history with annotations, KYC file with refresh dates, prior alerts on the same entity, network graph of counterparties, and screening hits. The analyst arrives at the case with the materials already organized.

Sar filing requirements 2026

FinCEN's modernization program is pushing toward structured data submission and stricter narrative quality expectations. Sar filing requirements 2026 will reward teams that can produce complete, evidence-linked narratives, not faster shallow ones.

KYC and CDD: Where Automation Earns Its Keep

Kyc cdd requirements banks face have expanded significantly. Beneficial ownership under the Corporate Transparency Act, enhanced due diligence on correspondent accounts, ongoing monitoring of relationship changes, none of this scales with manual review.

Onboarding: the 90-second decision

For low-risk retail customers, kyc automation should produce a decision in under two minutes with no human touch. The exception path routes documents that fail liveness, sanctions hits, and PEP matches to a reviewer.

Enhanced due diligence guide for high-risk customers

For correspondent banks, MSBs, and high-net-worth clients, the enhanced due diligence guide your team follows should require human review of source-of-wealth documentation, site visits where applicable, and senior management sign-off. Automation prepares the file; humans make the call.

Ongoing monitoring beyond annual refresh

The old model of annual KYC refresh is gone. Modern systems watch for trigger events: change in beneficial ownership, sudden transaction pattern shifts, adverse media. The right regulatory compliance automation approach treats KYC as a continuous process rather than a periodic checkbox, which is what examiners increasingly expect.

Building the Augmented Compliance Team

The organizational design question matters as much as the technology. Three patterns work.

Pattern 1: Pod-based investigations

Small pods of 3-5 analysts share a senior reviewer and a dedicated data analyst. The pod owns a customer segment end-to-end. This works well at community banks and mid-size fintechs.

Pattern 2: Specialty queues

Separate teams for transaction monitoring, sanctions, and KYC, with cross-training rotations. Better for larger banks where typology depth matters.

Pattern 3: Hybrid managed services

Core decisions stay in-house, while overflow alert review goes to a managed service. Common in fintech bsa aml small team setups where headcount is constrained but volumes are spiky.

In all three, the technology layer is the same. The org design is what changes. We covered related ground in our piece on manual compliance versus AI automation tradeoffs.

Regulatory Pressure Is Pushing Both Ways

Regulators want faster reporting and better quality, which is a tension. They are also moving on AI governance itself.

EU AI Act financial services implications

The eu ai act financial services rules classify many AML and credit-decisioning models as high-risk, requiring documented risk management, human oversight, and transparency. The European Commission's AI Act overview is the primary reference. For US-headquartered banks with EU operations, this is not optional.

US guidance is converging

The interagency statement on innovative approaches to BSA/AML compliance and the OCC's model risk guidance both point in the same direction: automation is welcome, but the human in the loop is non-negotiable for material decisions.

A Realistic Implementation Path

If your team is starting this journey, here is what we recommend based on what has worked.

Months 1-3: Instrument and measure

Before touching tooling, measure where analyst time actually goes. Most teams are surprised. Once you have a baseline, you can prioritize automation by minutes-saved-per-week, not vendor pitch.

Months 4-9: Automate the data layer

The single biggest win is unifying customer, transaction, and screening data into one investigation view. This is plumbing work, not AI work, and it delivers more value than any model.

Months 10-18: Add adaptive monitoring and case management

Only after the data layer is solid should you layer in ML-driven scoring and tiered case routing. Otherwise you are putting a smart model on top of bad data, which is how false positives explode.

Months 18+: Continuous improvement

Feedback loops, model validation, and analyst training become the recurring work. Compliance programs are never "done."

For teams working through related programs, our guide on rolling out regulatory compliance agents in 90 days walks through a faster sprint pattern for specific use cases.

The Honest Limitations

A few things RegTech compliance automation will not fix, and pretending otherwise damages credibility with your team and your regulator.

It will not fix a weak risk assessment. If the underlying typology coverage is wrong, faster alerts on the wrong patterns just produce more noise.

It will not survive poor data quality. Garbage in, garbage out is more true in AML than anywhere else, because the consequences are enforcement actions.

It will not replace the senior analyst who has seen 200 SAR filings and can spot structuring by reading three lines of a statement. That person is your most valuable asset. Build the program around them.

- Walk into any compliance conference and you will hear vendors promise headcount reduction.

- The modern aml compliance software stack is narrower in ambition than the 2019 pitch decks suggested, and far more useful.

- If you are reshaping your aml compliance fintech program around augmentation rather than replacement, here is a working bsa aml compliance checklist we use with clients.

- Sar filing efficiency is the metric most compliance leaders are measured on, and it is widely misunderstood.

- Kyc cdd requirements banks face have expanded significantly.

Onboard Customers in Seconds

Conclusion

RegTech compliance automation is the most useful thing to happen to compliance teams in a decade, and the framing that matters is augmentation. The aml compliance software that earns its keep removes data drudgery, organizes investigations, and routes alerts by risk, so analysts can spend their judgment where it counts: on the SAR narrative, the ambiguous typology, and the regulator-facing explanation. Teams that adopt this mindset hit better sar filing efficiency without sacrificing quality, scale their kyc automation 2026 programs without ballooning headcount, and stay defensible under examination. If your program is still being sold to you as headcount reduction, push back. The right question is what your best analysts could do if they got their time back.

If you want to see how this works in practice for your bsa aml compliance checklist, our team at FluxForce builds these programs with banks and fintechs every quarter. Reach out and we will walk you through it.

Share this article