.webp)

Listen To Our Podcast🎧

Introduction

Perpetual KYC is rewriting the compliance playbook for banks, fintechs, and every regulated institution still locked into the cycle of annual customer reviews. The traditional model made sense when customer behavior was predictable and transaction volumes were manageable. Neither of those conditions holds today. Financial crime has grown faster and more adaptive than the scheduled review was ever designed to catch. This post covers what perpetual KYC means in practice, how it connects to SAR filing, BSA/AML compliance, and enhanced due diligence, and what concrete steps institutions of different sizes can take to implement it in 2026.

This post covers what perpetual KYC means in practice, how it connects to SAR filing, BSA/AML compliance, and enhanced due diligence, and what concrete steps institutions of different sizes can take to implement it in 2026.

- Why Annual KYC Reviews Fail in a Dynamic Risk Environment

- What Is Perpetual KYC and How Does It Actually Work?

- How KYC Automation Powers Perpetual Monitoring

- AML Compliance Implications for Banks and Fintechs

- SAR Filing Efficiency Under a Perpetual KYC Model

Onboard Customers in Seconds

Why Annual KYC Reviews Fail in a Dynamic Risk Environment

The annual review was always a compromise. Compliance teams couldn't monitor every customer continuously, so they segmented by risk tier and scheduled periodic checks. High-risk customers got reviewed annually; low-risk customers sometimes every three to five years. That system worked reasonably well when customer behavior was relatively stable.

The problem is that stability no longer holds. A retail customer might open a personal account, start a side business, receive international wires, and join the board of a charity with PEP-adjacent donors all within eighteen months. None of that shows up in an annual review cycle unless the review happens to fall in exactly the right window.

The Cost of Snapshot Compliance

Snapshot compliance means your institution sees a photograph of customer risk, not a video. Financial crime typologies evolve faster than fixed review schedules. According to FinCEN guidance on beneficial ownership, institutions must update customer information when they become aware of changes. Under a periodic review model, compliance teams often are not aware of changes because they are not actively looking between cycles.

The practical cost shows up in suspicious activity report filings. Teams relying on periodic reviews often file SARs based on information that is weeks or months out of date, reducing their investigative value and creating regulatory exposure.

How Risk Profiles Change Between Review Cycles

A useful way to frame this: a bank with one million retail customers, where just two percent experience a material risk profile change each quarter, has twenty thousand customers whose updated status will not appear until the next scheduled review. For community banks, the number is smaller but the regulatory obligation is identical. The Financial Action Task Force (FATF) has consistently emphasized that a risk-based approach requires continuous calibration, not a fixed schedule.

What Is Perpetual KYC and How Does It Actually Work?

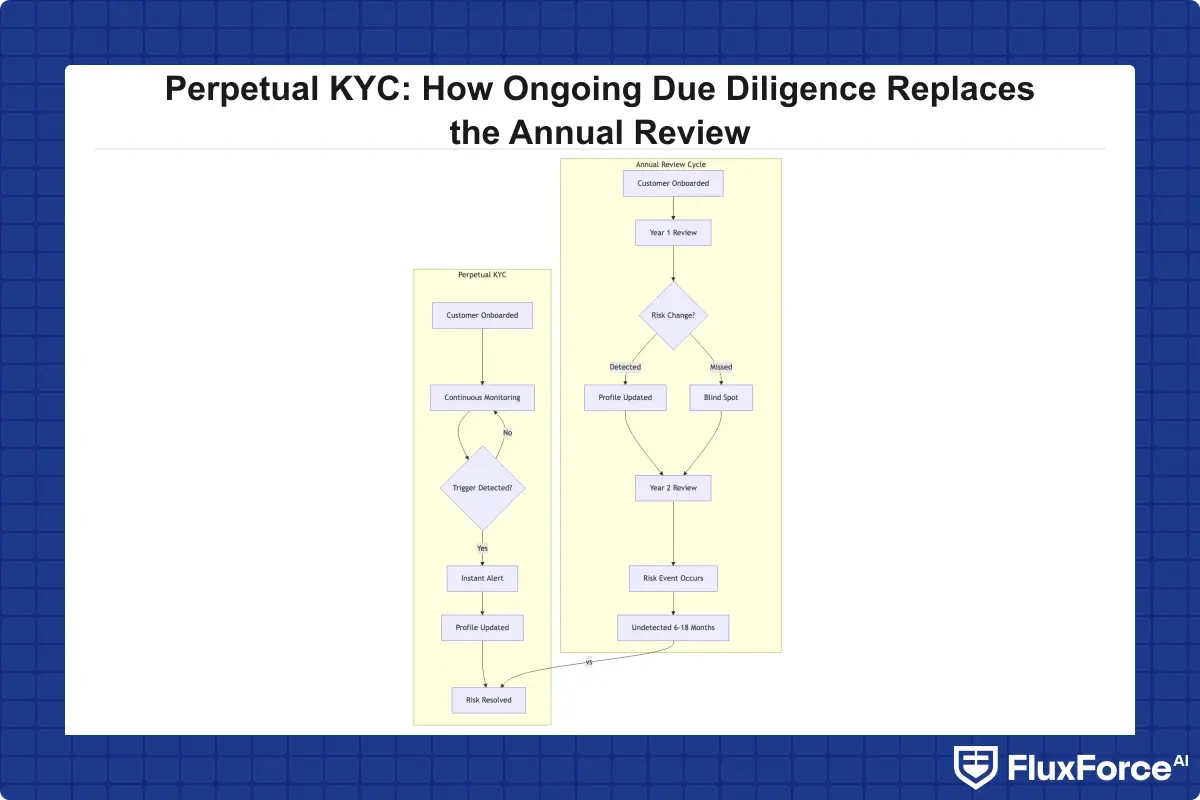

Perpetual KYC is a compliance model where customer due diligence updates continuously in response to real-world triggers, rather than on a fixed calendar schedule. Instead of reviewing a customer file every twelve months, the system monitors data signals (transaction patterns, adverse media, sanctions list changes, beneficial ownership updates) and re-evaluates risk whenever a relevant event occurs.

The concept is also called dynamic KYC or event-driven KYC. The defining feature is that reviews are triggered by risk, not by time.

Continuous Data Feeds vs. Periodic Refresh

Traditional CDD relies on a point-in-time data pull: collect documents at onboarding, refresh them at the next scheduled review. Perpetual KYC connects to live data sources, including sanctions screening databases, PEP lists, corporate registry feeds, and internal transaction monitoring outputs. When any of those sources flags a change, the system either automatically updates the customer risk score or routes the file for human review, depending on the severity of the event.

This is where kyc cdd requirements for banks get more demanding. Regulators in the US, UK, and EU increasingly expect institutions to demonstrate that their CDD processes can detect risk changes in near real-time, not just at annual intervals. Following an enhanced due diligence guide calibrated for continuous monitoring means documenting not just what data was collected, but when the collection was triggered and what threshold was crossed.

How pKYC Differs from Traditional CDD

| Dimension | Traditional CDD | Perpetual KYC |

|---|---|---|

| Review trigger | Fixed schedule | Risk event |

| Data freshness | Point-in-time | Near real-time |

| Analyst workload | Periodic spikes | Distributed, lower peaks |

| False negative risk | High | Lower |

| Technology requirement | Low | High |

The enhanced due diligence process changes under this model too. EDD is not a separate workflow run on a different schedule; it is a more intensive version of the same continuous monitoring that applies to all customers, with additional data sources and lower alert thresholds. For context on how EDD principles connect to identity verification in financial services, the post on AML risk checks in policy issuance covers the relevant intersection of KYC and claims workflows.

How KYC Automation Powers Perpetual Monitoring

Perpetual KYC is operationally impossible without technology. No compliance team can manually review customer data every time a sanctions list is updated or a transaction pattern shifts. KYC automation is what makes continuous monitoring achievable at scale.

Real-Time Data Triggers and Automated Workflows

The practical architecture of a pKYC system involves three layers: data ingestion (pulling feeds from external sources and internal systems), a risk-scoring engine (recalculating risk scores based on new data), and a workflow layer (routing files for human review, auto-approving low-risk changes, or escalating alerts). This is what separates aml compliance software purpose-built for pKYC from legacy platforms designed around scheduled batch reviews.

For institutions exploring this model, the regulatory compliance automation capabilities of modern platforms address this orchestration challenge directly, connecting data triggers to compliance workflows without requiring manual intervention at each step.

KYC Automation Tools in 2026

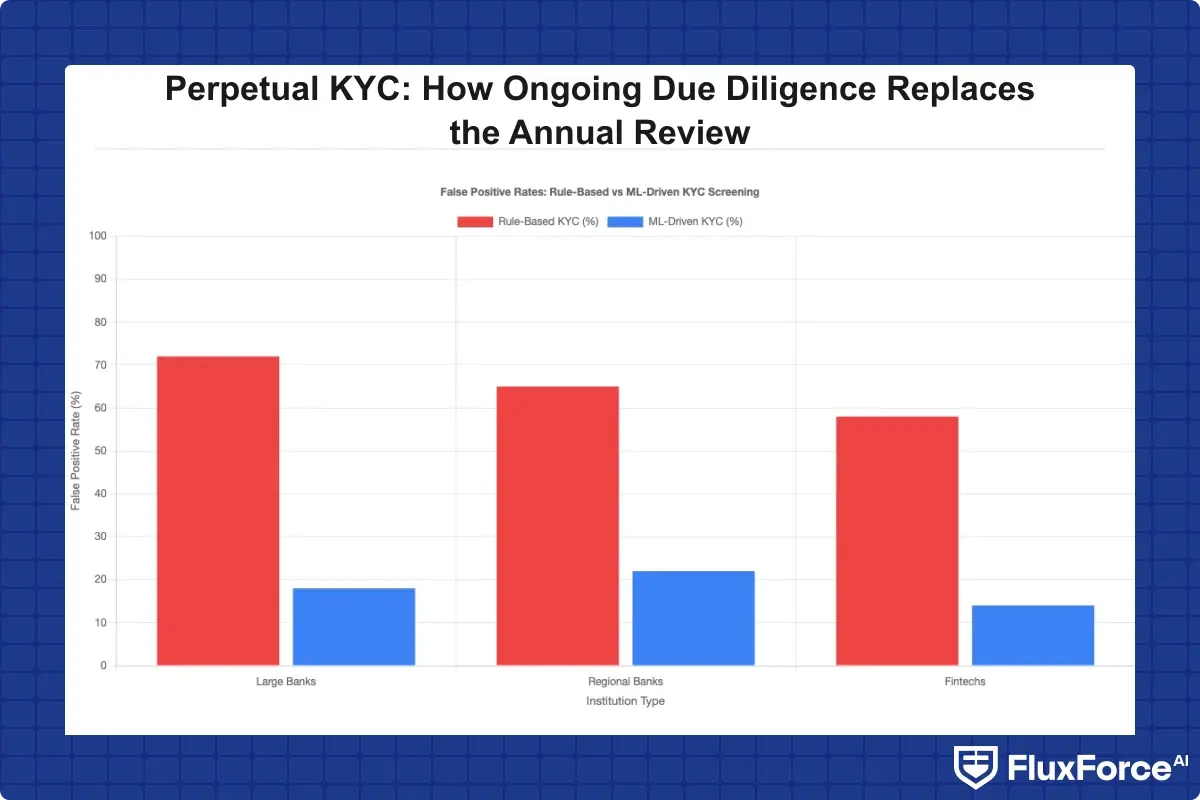

The anti money laundering technology landscape in 2026 looks different from even three years ago. Machine learning models now handle name-matching and adverse media screening with significantly fewer false positives than rule-based systems. Natural language processing extracts risk signals from unstructured sources like news articles and court records. API-driven integrations mean that corporate registry updates in one jurisdiction can trigger an automated review of every connected customer within minutes.

The honest answer is that kyc automation 2026 is not one tool; it is a stack. Institutions need a transaction monitoring system, a screening platform, a CDD management layer, and a case management system, all exchanging data in real time. Getting that integration right is harder than buying any individual component.

The honest answer is that kyc automation 2026 is not one tool; it is a stack.

AML Compliance Implications for Banks and Fintechs

Perpetual KYC changes the operational model for aml compliance programs, not just the technology stack. Compliance officers need to rethink how they structure teams, how they measure program effectiveness, and how they document risk assessments for regulators.

What Changes in Your AML Compliance Program

The biggest shift is from batch work to continuous work. Under a periodic review model, compliance analysts have predictable, calendar-driven workloads. Under perpetual KYC, the workload is event-driven, which means it is less predictable but more evenly distributed. Alert queues become smaller and more current. The files that reach analysts contain fresher data. Working through an updated aml risk assessment guide helps compliance teams structure this transition, since the process touchpoints change significantly when moving from scheduled to event-driven reviews.

For aml compliance fintech organizations, this shift matters particularly. Many fintechs onboard customers rapidly and at scale, which means customer risk profiles can drift significantly in the months after onboarding. A fintech that opens ten thousand accounts a month and reviews them annually is running a materially different risk program than one monitoring those accounts continuously.

AML Compliance Software That Supports pKYC

Not all aml compliance software handles continuous monitoring. Legacy platforms were built around scheduled batch jobs: pull customer data once a night, run screening, generate a report. That architecture is incompatible with perpetual KYC, which requires event-driven processing. When evaluating software, compliance leaders should ask whether the platform supports webhook-based triggers from external data sources, and whether risk scores can be recalculated in near real-time rather than overnight.

For related reading on how automated compliance integrates with broader security architecture, the post on sanctions screening automation for CISOs covers the detection and workflow layers in useful detail.

SAR Filing Efficiency Under a Perpetual KYC Model

One of the clearest measurable benefits of perpetual KYC is what it does to suspicious activity report quality and sar filing efficiency. This connection gets overlooked in most pKYC discussions, which tend to focus on onboarding and monitoring rather than downstream reporting.

Continuous monitoring surfaces suspicious patterns earlier. Under a periodic review model, a customer who begins structuring cash transactions in month three of a twelve-month review cycle will not be flagged until month twelve. That is nine months of transaction history the institution has already processed before anyone examines the pattern closely. Under perpetual KYC, the transaction monitoring system flags the pattern in month three, giving investigators a much cleaner, shorter window to analyze.

How Continuous Monitoring Improves SAR Filing

The suspicious activity report guide published by FinCEN states that SARs should be filed within 30 days of identifying a suspicious transaction, or 60 days if additional investigation is needed. Perpetual KYC makes it easier to meet sar filing requirements 2026 because the identification date is earlier and more precisely documented. When an automated alert triggered by a specific data event initiates the investigation, there is a clear timestamp for when suspicious activity was first identified.

Sar filing best practices under a perpetual model include documenting the specific trigger that initiated the review, the data sources consulted, and the risk score change that occurred. This creates a cleaner audit trail than the periodic review model, where reconstructing why a customer was flagged at a particular time can be genuinely difficult.

SAR Filing Requirements and Best Practices for 2026

Under sar filing requirements 2026, regulators increasingly expect SAR narratives to include context about the customer's recent risk history, not just the specific transaction at issue. Continuous monitoring generates that context automatically. Analysts working with a perpetual KYC system can pull a complete risk timeline for any customer, showing every data event, risk score change, and review action over the customer's lifetime. That timeline is exactly what examiners look for when evaluating whether an institution's sar filing process is genuinely risk-based rather than calendar-based.

BSA/AML Compliance Checklist for Perpetual KYC Implementation

Moving to a perpetual KYC model requires updating your BSA/AML program documentation. Regulators expect institutions to have written policies and procedures describing how their CDD process works. If your procedures still describe a periodic review schedule, you are documenting a process different from the one you are actually running.

Core Elements of a pKYC BSA/AML Program

A practical bsa aml compliance checklist for perpetual KYC should cover these eight elements:

- Data source inventory: List every external and internal data source feeding the monitoring system, including update frequency and how changes are ingested.

- Risk trigger definitions: Document which events trigger an automated risk score recalculation (sanctions match, adverse media hit, beneficial ownership change, transaction threshold breach).

- Escalation thresholds: Define which score changes or alert types require human review versus automatic update.

- Review SLAs: Document how long analysts have to close an escalated alert, typically 24 to 72 hours for high-risk events.

- SAR filing timelines: Document how the 30-day SAR filing clock is measured under the continuous monitoring model.

- CTR filing rules: Confirm that currency transaction report obligations are handled separately from the pKYC workflow, since ctr filing rules apply on a per-transaction basis regardless of the customer's overall risk profile.

- Model validation schedule: Document how and when the risk-scoring model is validated and updated.

- Training program: Describe how analysts are trained on the event-driven workflow, which is operationally different from periodic review work.

Adapting the Checklist for Community Banks

Bsa aml compliance community banks face different constraints than large institutions. Dedicated technology teams and enterprise compliance platform budgets are rare at smaller institutions. But perpetual KYC does not require a massive technology investment; it requires prioritization. Most community banks can implement event-driven monitoring for their highest-risk customers (high-volume cash businesses, customers with SAR history, politically exposed persons) while continuing periodic reviews for the lower-risk majority. That hybrid approach delivers most of the risk management benefit at a fraction of the full implementation cost.

How Small Fintech Teams Can Implement Perpetual KYC

Fintech bsa aml small team environments present a genuine challenge. The compliance function might be three or four people managing hundreds of thousands of accounts. Full perpetual KYC in that environment sounds operationally impossible. It is not, but it requires making deliberate choices about automation and prioritization.

Fintech BSA/AML Challenges with Limited Headcount

The core problem for small teams is alert volume. If the system generates ten alerts a day requiring human review, a two-person compliance team can handle that. If it generates two hundred, the backlog grows faster than the team can clear it. The goal for fintech teams is to automate as many low-risk decisions as possible and reserve human review for genuinely ambiguous or high-risk cases.

This is where the aml compliance fintech use case for machine learning is clearest: not replacing analysts, but handling the triage work that currently occupies most of their time. The post on how agentic AI reduces false positives in compliance screening covers the detection mechanics that apply equally to KYC and fraud workflows.

Using Technology to Bridge the Gap

For fintech teams evaluating anti money laundering technology for the first time, the right starting point is not the most sophisticated platform available; it is the one that integrates cleanly with existing data sources and surfaces accurate alerts without overwhelming the team. A platform generating three precise alerts per day is more operationally valuable than one generating three hundred that each require manual triage before any real investigation can begin.

The transition also affects sar filing efficiency for small teams. Those that move to continuous monitoring typically find SAR narratives improve because each investigation starts from a cleaner, more current dataset. The time from alert to filed SAR often shortens even if the overall process feels more demanding during the initial transition period.

For organizations thinking about how to structure the broader compliance technology stack, the post on manual compliance vs. AI automation provides a useful framework for deciding which compliance decisions to automate and which to keep with human analysts.

The EU AI Act and Anti-Money Laundering Technology in 2026

The eu ai act financial services implications for compliance technology are still being worked out, but one thing is already clear: AI-driven KYC and AML systems face new documentation and transparency requirements. Under the EU AI Act, high-risk AI systems (which likely include AML screening and risk-scoring systems used to make decisions about customers) must be registered, documented, and subject to conformity assessments before deployment.

What the EU AI Act Means for Financial Services Compliance

For compliance officers running AI-driven pKYC systems, the EU AI Act regulatory framework specifically addresses explainability, which is a real challenge for black-box machine learning models used in sanctions screening and risk scoring. Institutions that have already invested in explainable AI models are better positioned than those running opaque systems. Model validation and documentation work that was previously a regulatory best practice is now, for EU institutions, becoming a legal requirement with defined timelines and audit obligations.

Anti-Money Laundering Technology Trends in 2026

Anti money laundering technology 2026 is developing along three main directions simultaneously. First, more institutions are adopting federated learning approaches, where models train on cross-institutional patterns without sharing underlying customer data. Second, graph analytics is becoming standard for detecting network-level financial crime patterns that individual transaction monitoring misses entirely. Third, regulatory reporting itself is becoming more automated, with direct data feeds from compliance systems to regulators replacing periodic batch submissions.

Anti money laundering technology 2026 is developing along three main directions simultaneously.

All three trends reinforce the move toward perpetual KYC. A compliance program built on periodic reviews struggles to feed real-time data to regulators, detect network-level patterns, or participate in federated learning models. The technology is pulling institutions toward continuous monitoring regardless of whether they have made a deliberate strategic decision to adopt it.

For related reading on how real-time detection applies equally to fraud and compliance, the post on detecting synthetic identity fraud in real-time covers detection architectures with significant overlap with pKYC monitoring systems.

- The annual review was always a compromise.

- Perpetual KYC is a compliance model where customer due diligence updates continuously in response to real-world triggers, rather than on a fixed calendar schedule.

- Perpetual KYC is operationally impossible without technology.

- Perpetual KYC changes the operational model for aml compliance programs, not just the technology stack.

- One of the clearest measurable benefits of perpetual KYC is what it does to suspicious activity report quality and sar filing efficiency.

Onboard Customers in Seconds

Conclusion

Perpetual KYC is not a future aspiration; for well-resourced institutions, it is already operational. For community banks and fintech teams with limited compliance headcount, it is a direction rather than an overnight transformation. The core argument is straightforward: annual reviews create predictable blind spots in customer risk assessment, and those blind spots are where financial crime operates. Continuous monitoring does not eliminate risk, but it closes the window between when a customer's behavior changes and when your aml compliance program detects it.

The practical path toward perpetual KYC starts with your highest-risk customers and your most mature data sources. Update your BSA/AML documentation to reflect event-driven processes. Evaluate whether your compliance software supports real-time triggers or only batch processing. Think carefully about how sar filing workflows change when you have a continuous audit trail rather than a periodic snapshot. The annual review had a good run, but in 2026, continuous due diligence is where regulatory expectations, technology capabilities, and risk realities are all pointing.

Share this article