.webp)

Listen To Our Podcast🎧

Introduction

Operational risk management banking AI is no longer a speculative investment. It is the baseline for staying competitive and compliant. Banks, insurers, and fintechs face fraud attempts that outpace rule-based systems, regulatory expectations that require documented AI decision trails, and operational costs that compound every time a new point solution gets added to an aging stack. A new generation of AI-native risk platforms is solving all three problems from a single control plane. This post explains how, and what the migration looks like for institutions that have spent years accumulating disconnected tools.

- Why Operational Risk in Banking Is Harder Than It Looks

- Point Solutions vs Platform: The Hidden Cost of Fragmentation

- What a Unified Risk Platform Actually Delivers

- AI Agents and Operational Risk: Automating What Rules Cannot Handle

- Why Explainable AI Is Non-Negotiable for Compliance

Onboard Customers in Seconds

Why Operational Risk in Banking Is Harder Than It Looks

Operational risk covers every threat to a financial institution that is not credit or market risk: fraud, compliance failures, cyber incidents, process breakdowns, and third-party failures. The Basel Committee on Banking Supervision defines it as the risk of loss from inadequate or failed internal processes, people, systems, or external events. Despite being one of the three main Pillar 1 risk categories under Basel III, it remains the least automated category at most institutions.

The honest answer to why is that operational risk is messy. Unlike credit risk, it does not reduce to a clean probability distribution. A payment fraud attempt, a sanctions screening miss, and a rogue API endpoint are all operational failures, but they look nothing alike, sit in different teams' dashboards, and historically triggered different response workflows.

The Scale of the Problem

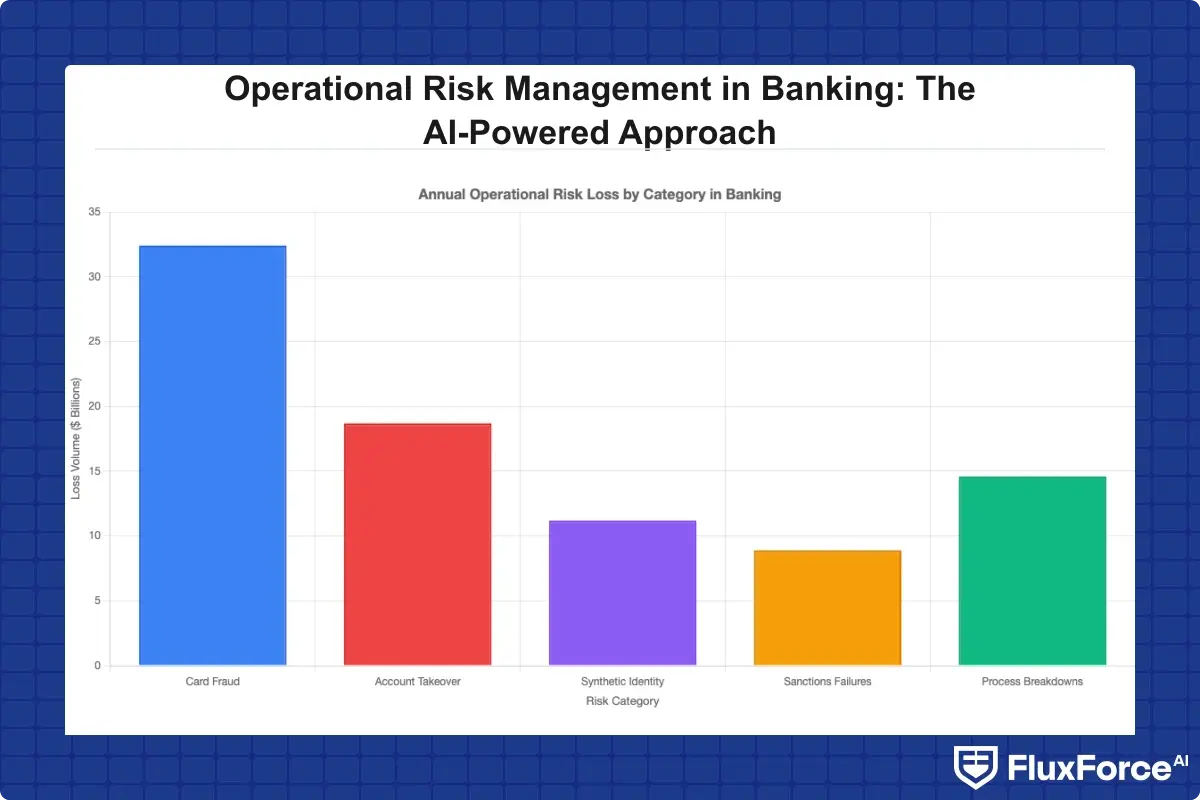

According to the Financial Stability Board's work on AI in financial services, financial institutions globally report that manual risk processes consume 30-40% of compliance team capacity on tasks that could be automated. Fraud losses continue to climb year-over-year, with card fraud, account takeover, and synthetic identity attacks leading the categories. The institutions managing these costs best share one characteristic: they treat fraud, compliance, and identity verification as a unified problem rather than three separate departments.

According to the Financial Stability Board's work on AI in financial services, financial institutions globally report that manual risk processes consume 30-40% of compliance team capacity on tasks that could be automated.

Where Traditional Systems Fall Short

Rule-based systems were built for known attack patterns. The moment a fraud typology shifts slightly, a rules engine either misses it or fires a false positive that wastes analyst time. Most banks run dozens of these engines in parallel, each tuned by a different team, each producing alerts that land in separate queues. The result is that an analyst might review the same suspicious customer across three systems without a single unified view. That describes the operational reality at many banks carrying more than five years of technology debt.

Point Solutions vs Platform: The Hidden Cost of Fragmentation

The debate around point solutions vs platform financial services has sharpened as AI capabilities have matured. The argument for specialized tools used to be that best-of-breed beat integrated suites on every individual capability. That argument is harder to sustain now, because the value in modern risk management comes from data sharing across domains, not from any single algorithm's isolated performance.

How Point Solutions Create Blind Spots

A fraud detection tool that cannot see identity verification signals will always have a blind spot. A KYC system that does not feed transaction monitoring will miss account takeover patterns that only become visible when onboarding data and live transaction behavior are compared together. Every integration boundary between point solutions is a potential detection gap, and these gaps are exactly where sophisticated fraud networks operate.

This is the core argument for a fraud compliance identity platform: not that any individual module is necessarily better than a specialist tool, but that the system as a whole performs better when components share a data model and decision context. The consolidation argument is fundamentally about signal quality, not just cost reduction.

The Integration Tax Nobody Budgets For

Here is the cost that almost never appears in vendor evaluations: maintaining integrations between six to ten point solutions requires dedicated engineering capacity. Every API version change, every new data field from a compliance vendor, every schema update from a fraud tool creates work. At a mid-sized bank, this integration maintenance can consume 20-30% of a risk technology team's capacity. That is capacity not spent on detection improvements, not spent on regulatory projects, and not spent on reducing false positives.

At a mid-sized bank, this integration maintenance can consume 20-30% of a risk technology team's capacity.

When you add up licensing fees across vendors, integration overhead, and analyst time wasted on fragmented alert queues, the total cost of running a fragmented risk stack frequently exceeds that of a consolidated platform. This is the core economic case for vendor consolidation fintech teams rarely surface until they complete a full cost accounting.

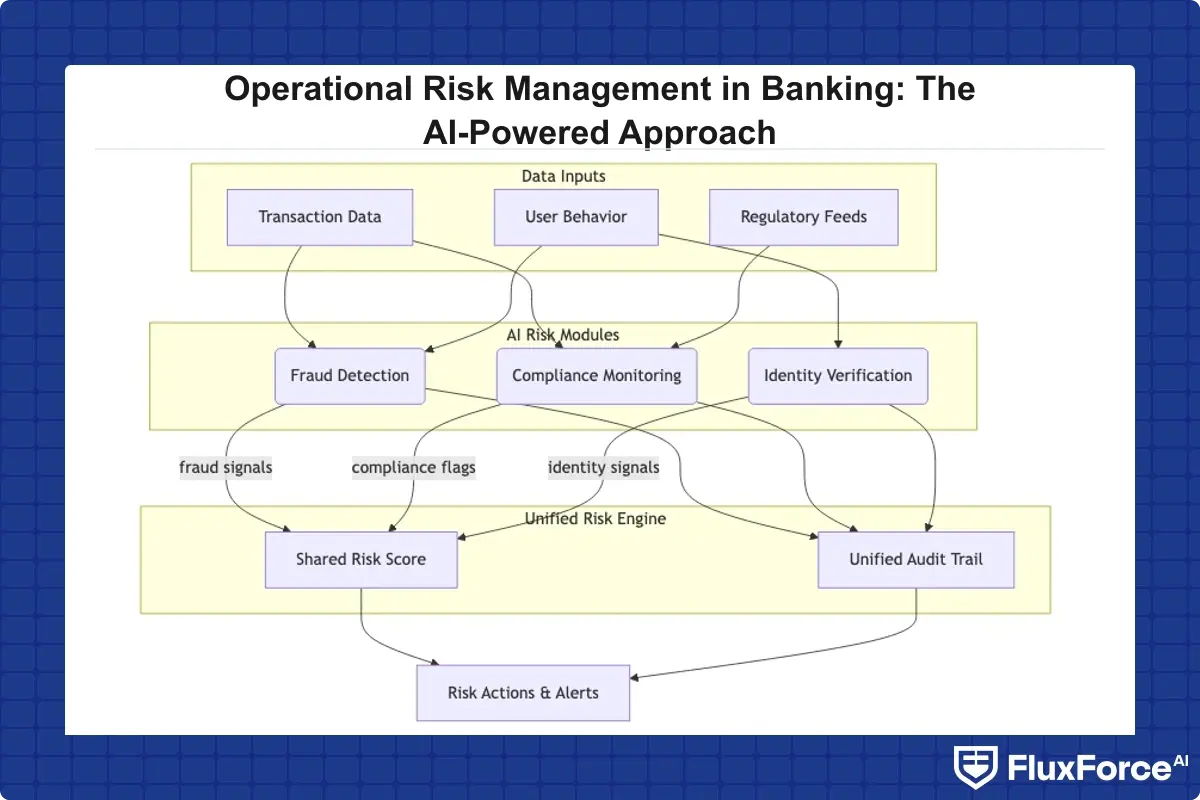

What a Unified Risk Platform Actually Delivers

A unified risk platform is not a dashboard that aggregates data from separate systems. The distinction matters: aggregation still leaves underlying decision logic siloed. A true unified platform shares a common data model, runs AI models that see signals across fraud, compliance, and identity simultaneously, and produces a single risk score with a single audit trail.

Real-Time Detection Across Fraud, Compliance, and Identity

The practical effect is measurable. When a transaction triggers a fraud signal, the platform can simultaneously check whether the account has recent KYC anomalies, whether the counterparty appears on a sanctions watchlist, and whether the device fingerprint matches prior legitimate sessions. That correlation happens in milliseconds on a unified data model. On a fragmented stack, it requires an analyst to pull three separate reports, by which point the window to stop the transaction has typically closed.

The FluxForce fraud detection software works on exactly this principle: a shared risk fabric where fraud signals, compliance checks, and identity data all feed the same decision engine, rather than running in parallel silos. Deploying this way means fewer missed threats and fewer false positives, because the model has more context for every decision it makes.

For institutions focused on card-level fraud specifically, the card fraud analytics approach applies the same unified-context logic to the patterns that affect card-present and card-not-present channels.

AI Audit Trail and Accountability

Regulatory examiners want to see not just outcomes but reasoning. An ai audit trail automation capability means every decision the system makes is logged with the inputs, the model version, the confidence score, and the action taken. This is a baseline requirement for institutions operating under SR 11-7 guidance, DORA, or similar model risk management frameworks. A unified platform generates this audit trail natively. Stitching together audit logs from five separate vendor systems is a compliance project in itself, one that frequently delays regulatory submissions and creates documentation gaps that examiners notice.

AI Agents and Operational Risk: Automating What Rules Cannot Handle

The shift from rule-based to AI-powered risk management is one level of progress. The next level is the use of ai agents financial services deployments that plan, execute, and adapt across multi-step workflows without requiring human initiation for each action. This is where operational risk management banking AI is headed, and institutions that get there first will have a meaningful capacity advantage over competitors still running static rule sets.

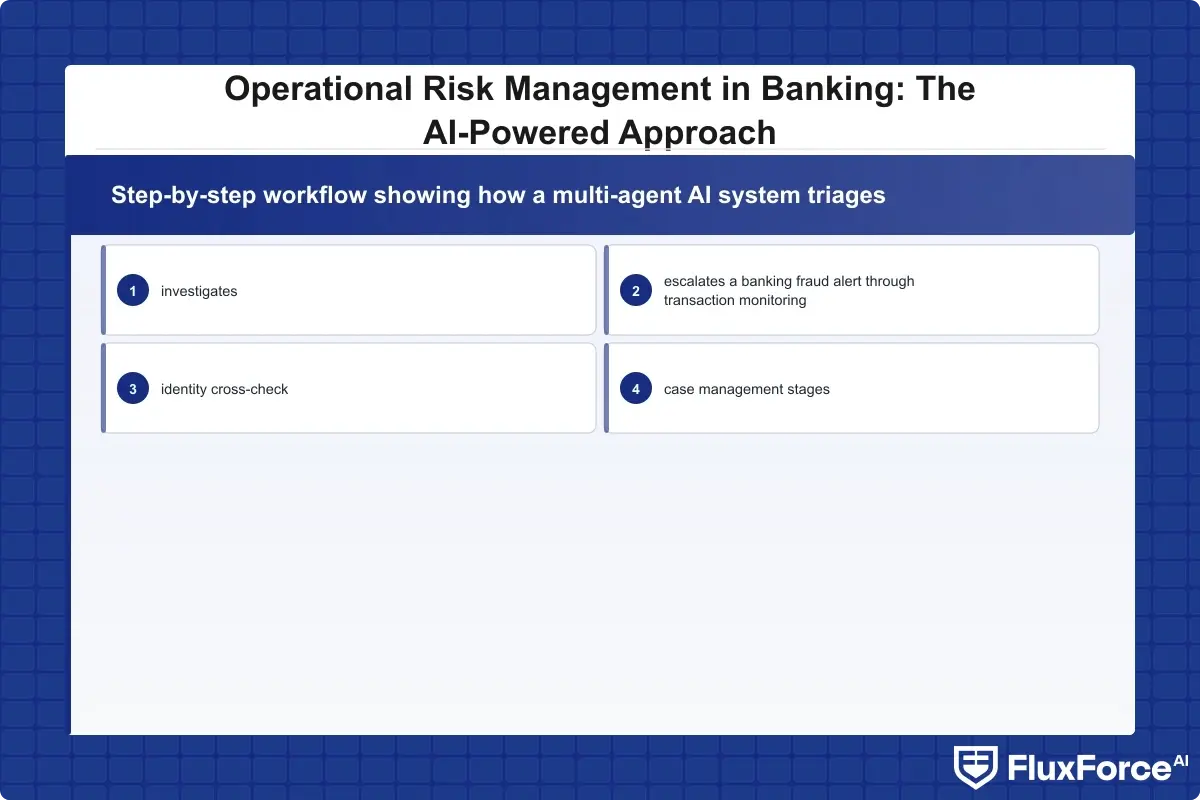

How Multi-Agent AI Systems Work in Banking

A multi agent ai system for risk management typically involves specialized agents with defined scopes. One agent monitors transaction patterns, another investigates identity anomalies, and a third handles draft regulatory report generation. These agents coordinate by passing structured context between them. When the transaction monitoring agent flags an account, it hands off its findings to the identity agent, which cross-checks onboarding history and device behavior, then passes a combined risk assessment to a case management agent that decides whether to escalate to a human or resolve automatically.

This is qualitatively different from a rules engine. The agents adapt their investigation path based on what they find, rather than following a fixed decision tree. They also update their pattern recognition based on confirmed fraud cases, which means the system improves without waiting for a scheduled model retrain cycle.

AI Agent Fraud Detection in Practice

AI agent fraud detection at production scale means the system handles the first-pass investigation on every alert. An analyst only sees cases where the agent's confidence score falls below a defined threshold, or where policy requires human sign-off for cases above a dollar amount or involving sanctioned geographies. XAI fraud detection capabilities mean every agent decision carries an explanation the compliance team can review and defend. Agentic AI deployments in fraud detection have produced false positive reductions of up to 80%, which translates directly into analyst capacity recovered and redeployed toward higher-judgment investigations.

Agentic AI deployments in fraud detection have produced false positive reductions of up to 80%, which translates directly into analyst capacity recovered and redeployed toward higher-judgment investigations.

Why Explainable AI Is Non-Negotiable for Compliance

Explainability is where many AI implementations in banking stall. A model that detects fraud with 95% accuracy is not deployable if the institution cannot explain to a regulator or a customer why a specific decision was made. This is where explainable ai finance principles translate from theoretical best practice into a concrete regulatory requirement, one that affects model approval timelines, audit findings, and customer dispute resolution outcomes.

The Problem with Black Box AI in Regulated Environments

Black box ai compliance risk is a real operational liability. A model that ingests 400 features and produces a risk score without interpretable reasoning creates several simultaneous problems. Regulators cannot validate that the model does not embed protected characteristics as proxies. Customers flagged or declined have legal explanation rights in most jurisdictions under GDPR, FCRA, and equivalent frameworks. Internal audit cannot sign off on a model they cannot interrogate. The operational risk of deploying an opaque AI model often exceeds the risk the model was designed to manage.

The NIST AI Risk Management Framework treats explainability as a core trustworthiness dimension. Regulators in the EU, UK, and US have all issued guidance reinforcing this requirement for algorithmic decision-making in financial services. Banks deploying AI for fraud flagging, credit decisions, or customer screening need explainability built into the architecture at the model design stage, not added as an afterthought when examiners request documentation.

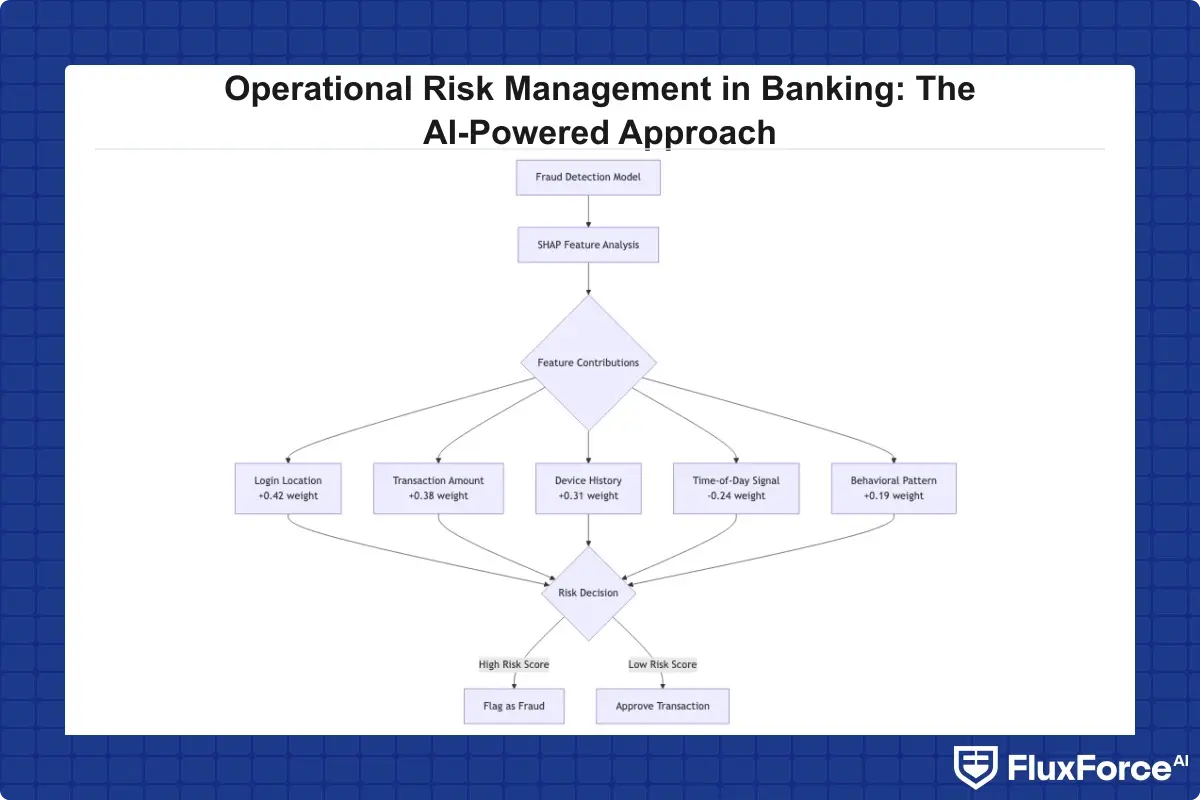

How SHAP Values Help Regulators Understand AI Decisions

SHAP values (SHapley Additive exPlanations) are the most widely adopted technique for explainable ai compliance in financial services. Shap values explained for regulators look like this: for a given fraud decision, the model reports that the risk score was driven 35% by an unusual login location, 28% by a transaction amount outside the customer's historical range, 20% by a previously unseen device, and the remainder by smaller corroborating signals. That breakdown is auditable, defensible, and communicable to an examiner who has never seen the underlying model code.

This is what ai model explainability regulators ask for during model risk reviews: not a black-box score with an accuracy claim, but a documented reasoning chain tied to observable inputs. Institutions with this capability built into their ai security operations platform can respond to regulatory model inquiries in hours rather than weeks. XAI fraud detection using SHAP, LIME, or Integrated Gradients means compliance teams can review the reasoning behind every automated decision and confirm no disallowed features are driving outcomes. For teams also managing API-level risk exposures, the API security strategy for CISOs in banking covers how explainability requirements extend to API access control decisions as well.

Human-in-the-Loop AI: Designing for Accountability

The goal of AI in operational risk is not full automation. It is optimal automation: AI handles what it can handle confidently, and humans handle what requires judgment, accountability, or regulatory sign-off. Human in the loop ai banking is the practical framework for making that boundary explicit, auditable, and adjustable as institutional confidence in the models grows.

Setting Thresholds with Configurable AI Autonomy

Configurable ai autonomy means institutions set decision rules by risk category, customer segment, and transaction type. A low-value card transaction with a 0.97 legitimacy confidence score clears automatically. A high-value wire to a new counterparty in a high-risk jurisdiction with a borderline confidence score routes to a senior analyst. The policy is explicit, logged, and adjustable without a model retrain. The override logic is transparent: analysts can see what the AI recommended, why, and which threshold triggered the escalation.

This architecture lets institutions start conservatively (route all cases above a threshold to human review) and systematically increase automation as they build empirical confidence across different risk categories. Compliance examiners can review the autonomy policy, audit the threshold adjustment history, and verify that humans remained in the loop for high-risk case types. The configurable ai autonomy model also satisfies the SR 11-7 requirement for ongoing model monitoring: the threshold data itself becomes evidence that the system is being governed. For a detailed breakdown of where automation is appropriate versus where it creates compliance exposure, the manual compliance vs AI automation analysis covers the specific decision points with regulatory context.

Vendor Consolidation and Operational Risk: Building a Leaner Stack

Vendor consolidation fintech discussions often center on cost savings. The capability argument is equally strong. When risk data lives in one platform, AI models have more signal per decision. When alert queues are unified, analysts have more context per case. When regulatory reporting flows from a single source of truth, submissions are faster and documentation gaps are less likely to emerge during examinations.

What to Look for in a Consolidated Risk Platform

The right ai security operations platform covers transaction monitoring, identity verification, sanctions and PEP screening, device intelligence, and behavioral analytics, all connected through a shared data model and a unified case management interface. It exposes decision logic through a single API layer and produces audit trails that satisfy model risk management review requirements without requiring additional tooling.

The trap is a vendor that markets their product as unified but has assembled it through acquisitions without actually consolidating the underlying data model. Ask directly: do fraud signals and compliance signals share the same event store? Can a compliance analyst query fraud case history without switching between systems? If the answers come with qualifications, the platform is still fragmented under the hood, and the vendor consolidation fintech benefit disappears in practice. For teams evaluating how zero trust principles interact with AI-driven risk management, the analysis of Zero Trust combined with agentic AI for banking security explores how both approaches reinforce each other when deployed from a single platform.

- Operational risk covers every threat to a financial institution that is not credit or market risk: fraud, compliance failures, cyber incidents, process breakdowns, and third-party failures.

- The debate around point solutions vs platform financial services has sharpened as AI capabilities have matured.

- A unified risk platform is not a dashboard that aggregates data from separate systems.

- The shift from rule-based to AI-powered risk management is one level of progress.

- Explainability is where many AI implementations in banking stall.

Onboard Customers in Seconds

Conclusion

Operational risk management banking AI is not one technology or one deployment model. It is a commitment to treating fraud, compliance, and identity as interconnected problems on a shared data foundation, powered by models that explain their decisions and escalate to humans when judgment is required. The institutions getting this right are not necessarily those with the most sophisticated individual tools. They are the ones that have consolidated their risk stack around a unified risk platform, invested in explainable ai finance capabilities their regulators can interrogate, and built configurable autonomy policies their compliance teams can maintain and defend. The practical starting point is an honest audit: map your current point solutions, measure the integration overhead, and determine whether your analysts have a single view of each customer's risk profile. If the answer is no, the consolidation case makes itself.

Share this article