.webp)

Listen To Our Podcast🎧

Introduction

NIST 800-63 identity assurance levels sit at the center of every serious identity verification decision in regulated finance. Whether you're onboarding a new retail banking customer, verifying a high-value wire transfer originator, or granting privileged access to a core banking system, the NIST 800-63-4 framework gives you a structured vocabulary for answering one fundamental question: how confident do you need to be that this person is who they claim to be?

NIST 800-63 identity assurance levels sit at the center of every serious identity verification decision in regulated finance.

The challenge is that most teams treat IAL and AAL selection as a compliance checkbox rather than a risk architecture decision. They pick IAL2 because their auditor mentioned it, or they default to IAL1 because it's faster. Both approaches create gaps. This guide breaks down the IAL and AAL tiers, maps them to real fintech and banking scenarios, and explains what NIST 800-63-4's revisions actually change for your digital identity proofing program.

- What Are NIST 800-63 Identity Assurance Levels?

- Understanding Authenticator Assurance Levels

- How Do You Pick the Right IAL for Your Fintech Use Case?

- Digital Identity Proofing: What NIST 800-63A Requires

- Synthetic Identity Fraud and the IAL Gap

Onboard Customers in Seconds

What Are NIST 800-63 Identity Assurance Levels?

NIST 800-63 identity assurance levels define the degree of confidence a relying party can have in a verified identity. The framework, published by the National Institute of Standards and Technology, splits identity into three documents: SP 800-63A (identity proofing), SP 800-63B (authentication), and SP 800-63C (federation). When practitioners talk about IAL, they mean the proofing component in 800-63A.

IAL1, IAL2, and IAL3: The Core Tiers

IAL1 requires no identity proofing. Any attributes provided by the applicant are self-asserted and unverified. This is appropriate for low-risk services where binding a real-world identity to an account isn't necessary.

IAL2 requires that the claimed identity exists in the real world and that the applicant is its rightful owner. It permits both remote and in-person verification and is the minimum standard for most regulated financial services. Remote IAL2 proofing can rely on document verification, biometric comparison, and liveness detection fraud controls.

IAL3 requires in-person or supervised remote proofing conducted by a trained representative, physical or biometric comparison to authoritative sources, and binding to a hardware authenticator. It applies when account misuse could cause severe harm: large credit facilities, high-limit trading accounts, or access to sensitive personal data at scale.

How IAL Differs from AAL

IAL answers "who is this person?" AAL answers "how strongly is this session tied to that verified identity?" A user can be proofed at IAL2 but authenticate daily at AAL1 (a password). That gap creates real risk. The NIST framework expects you to match AAL to the sensitivity of each transaction, not just to the IAL level set at enrollment. Many compliance teams conflate the two and end up over-investing in proofing or under-investing in runtime authentication controls.

Understanding Authenticator Assurance Levels

AAL governs the authentication mechanisms required during each session. Getting this wrong is where account takeover fraud and session hijacking most commonly emerge in identity verification fintech deployments.

AAL1, AAL2, and AAL3 Compared

| AAL | Requirement | Common Mechanism |

|---|---|---|

| AAL1 | Single factor | Password, PIN |

| AAL2 | Multi-factor authentication | OTP app + password, push notification |

| AAL3 | Hardware MFA | FIDO2 hardware key, PIV card |

AAL2 is the practical minimum for applications where account compromise has direct financial consequences. AAL3 applies to privileged administrative access, large-value account actions, or where regulations explicitly reference FIPS 140-2 Level 2 hardware authenticators.

When AAL3 Is Actually Required

AAL3 comes up less often than vendors suggest. In practice, it applies to: system administrators with privileged access to core banking infrastructure, signing officers on accounts above defined transaction thresholds, and federal program contexts that reference specific hardware authentication standards. For most customer-facing financial flows, AAL2 with phishing-resistant MFA satisfies both NIST guidance and examiner expectations.

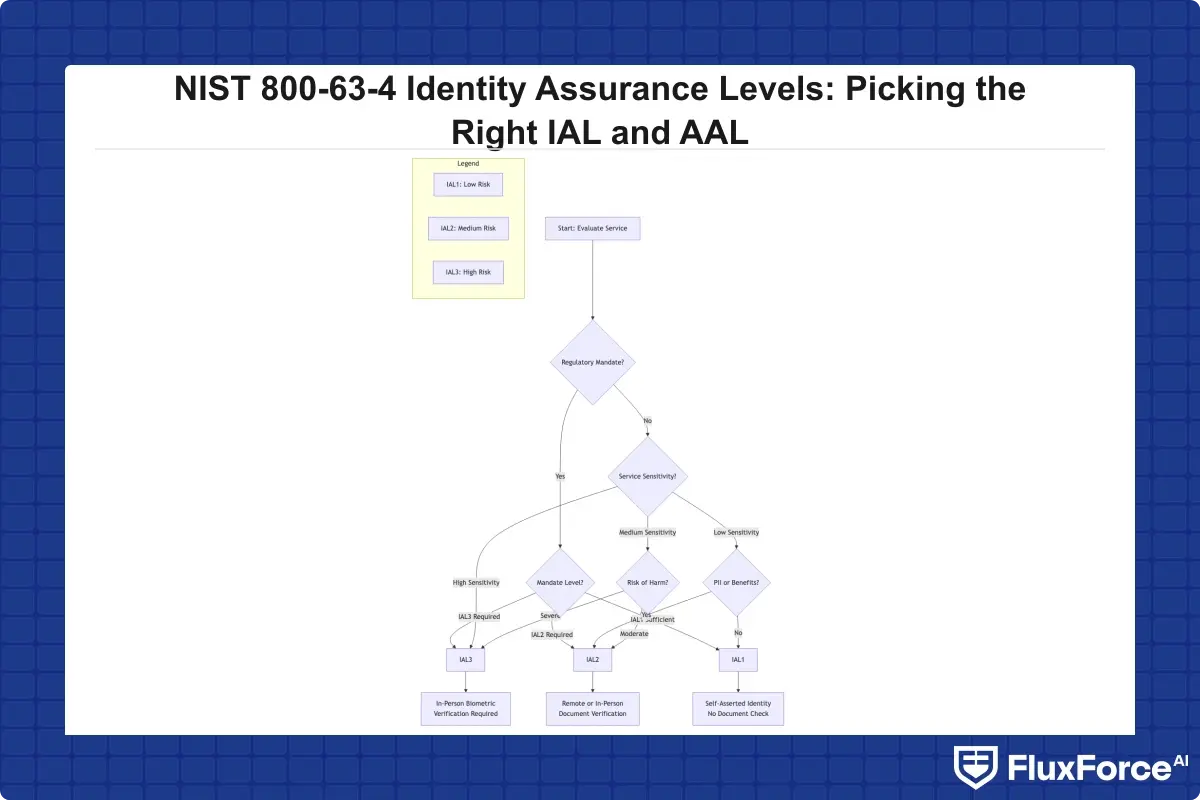

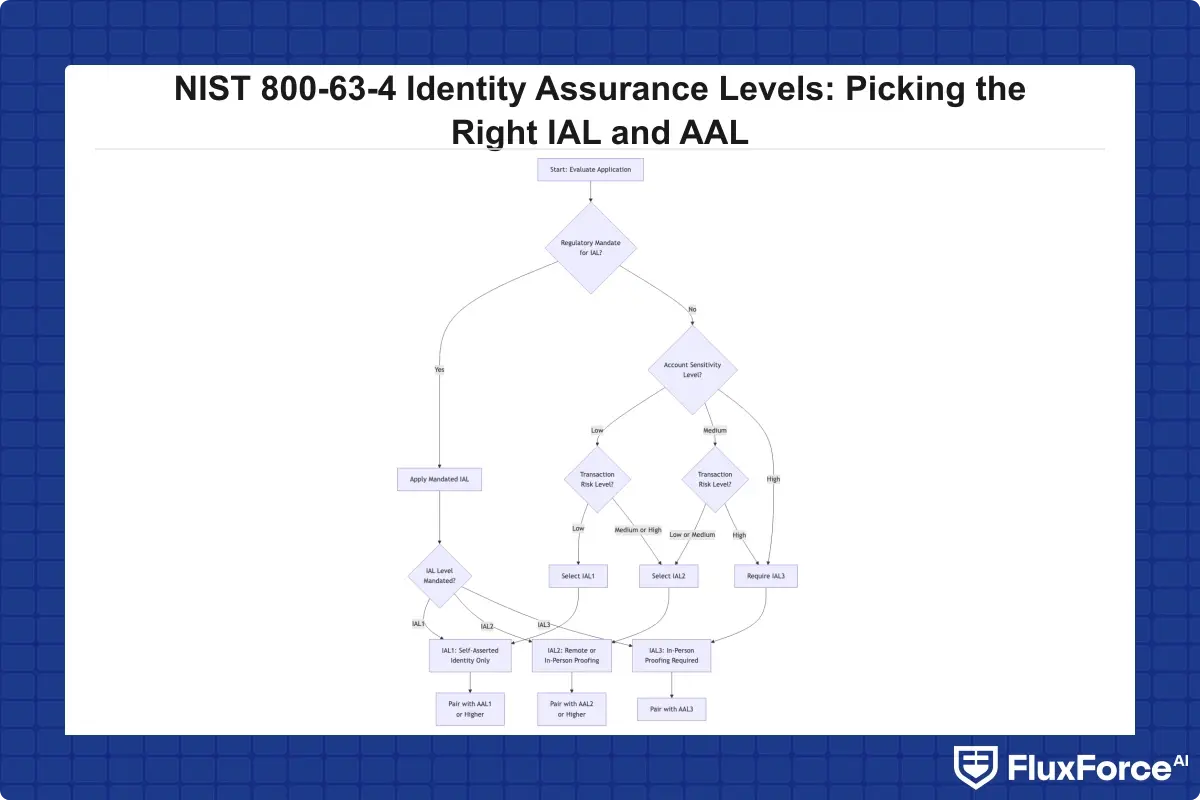

How Do You Pick the Right IAL for Your Fintech Use Case?

The honest answer is that there is no single right answer. IAL selection is a risk-based decision, and NIST deliberately avoids mandating specific IAL levels for specific service types. What the framework provides is a risk assessment methodology, refined in 800-63-4, that asks: what is the harm if a fraudulent identity is accepted, and what is the harm if a legitimate identity is incorrectly rejected?

IAL1: When Self-Assertion Is Sufficient

IAL1 is appropriate when the service has no monetary value, the harm from a fake identity is minimal, and no regulatory requirements mandate proofing. Think anonymous content browsing, early-stage product demos, or newsletter subscriptions. No financial service handling real money should operate at IAL1 for account creation.

IAL2: The Standard for Most Financial Services

IAL2 is where the majority of identity verification fintech work happens. It covers retail banking account opening, payment wallet creation, loan applications, insurance policy issuance, and most consumer-facing regulated services. The NIST 800-63-4 revision clarifies that remote IAL2 proofing can be accomplished through:

- Document verification against authoritative sources

- Biometric comparison (facial match to the photo on a presented identity document)

- Liveness detection to prevent presentation attacks

- Knowledge-based or credit bureau checks as supplemental signals

For most fintechs, integrating IAL2-compliant flows via a third-party identity verification api is significantly faster than building in-house. KYC onboarding speed becomes a competitive factor once you've established the IAL2 floor, and the goal is accuracy without unnecessary friction.

IAL3: High-Value and High-Sensitivity Accounts

IAL3 is expensive and creates friction. Use it where the cost of a fraudulent account clearly outweighs onboarding friction: broker-dealer accounts with discretionary trading authority, healthcare accounts with access to full medical records, large business account signatories, and any use case where a regulator has explicitly referenced supervised remote or in-person proofing requirements.

Digital Identity Proofing: What NIST 800-63A Requires

SP 800-63A governs the digital identity proofing process. The 800-63-4 revision introduced substantive changes that compliance teams need to understand, particularly around remote proofing at IAL2.

SP 800-63A governs the digital identity proofing process.

Remote vs. In-Person Proofing Under NIST 800-63-4

The revision made remote supervised proofing a more clearly defined pathway. Key changes include:

- Unattended remote proofing at IAL2 now has explicit requirements for document authentication, selfie comparison, and liveness detection fraud controls

- Trusted referee provisions allow organizations to use third-party identity service providers certified under approved trust frameworks

- Continuous attribute validation is recognized, meaning the proofing assertion doesn't have to occur in a single session

- Equity and accessibility considerations are now explicitly factored into process design, which matters for fair lending compliance

An IAL2 process that systematically fails certain demographic groups isn't just a reputational problem; it creates regulatory exposure under fair lending and anti-discrimination frameworks.

Biometric Identity Verification and Liveness Detection

Biometric identity verification at IAL2 requires comparing a live selfie to the photo on a presented identity document. The real challenge is the liveness detection layer. A static photo of a driver's license held up to a phone camera doesn't constitute adequate biometric proofing. NIST 800-63-4 expects organizations to implement controls that resist:

- Presentation attacks (printed photos or displayed images held to a camera)

- Injection attacks (pre-recorded video fed directly into the camera stream)

- Deepfake generation (AI-generated faces that match the document photo)

Deepfake detection banking has become a serious operational concern in 2025-2026. Commercially available face-swap tools now produce outputs that defeat older liveness detection fraud systems. Organizations relying on passive liveness checks alone may be materially non-compliant with the intent of IAL2, even if they technically complete the document verification step.

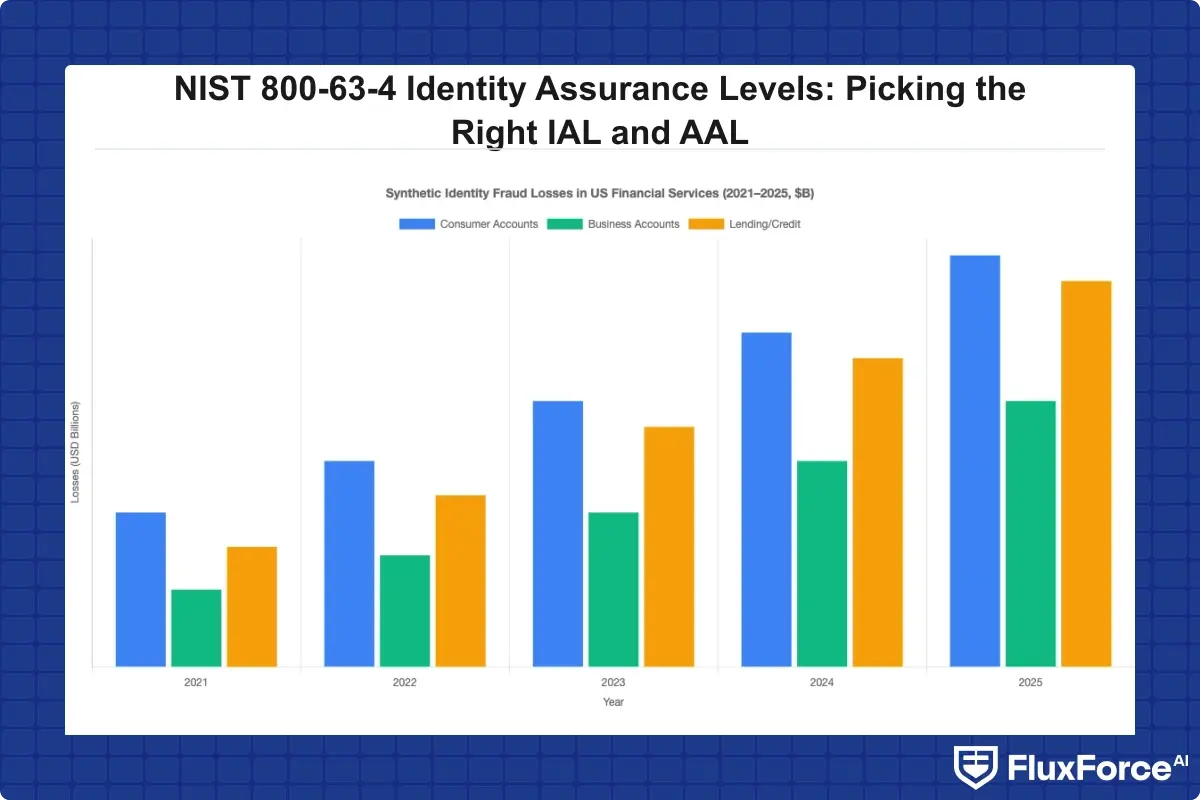

Synthetic Identity Fraud and the IAL Gap

Synthetic identity fraud is the construction of a fictitious identity using a mix of real and fabricated data. It's the fastest-growing financial crime category and it exploits the gap between weak proofing controls at the IAL1 and IAL2 boundary.

How Synthetic Identity Fraud Exploits Weak Proofing

A synthetic identity typically uses a real Social Security number (often belonging to a minor or elderly person with a thin credit file) paired with a fabricated name, date of birth, and address. Because the SSN is real, many credit bureau lookups return a match. A document verification step that only checks whether a document format is authentic won't catch this: the fraudster presents a genuine-format ID carrying the synthetic data.

Synthetic identity fraud detection at IAL2 requires layering signals: document authenticity, selfie liveness, credit bureau consistency, address verification, phone number intelligence, and behavioral signals during the application flow. No single check is sufficient. For a detailed look at how AI systems approach this problem in real time, Detecting Synthetic Identity Fraud in Real-Time covers the technical architecture for catching these identities before account opening.

Synthetic Identity Fraud Detection at IAL2 and Beyond

At IAL2, the NIST framework allows use of third-party data sources to corroborate identity claims. The practical implication: treat your identity verification api as an orchestration layer, not a single-vendor point solution. An effective IAL2 synthetic fraud check draws from:

- Document chip data (for NFC-enabled passports and newer ID cards)

- Liveness and facial comparison scores

- SSN issuance date vs. claimed applicant age

- Phone number age and ownership history

- Device fingerprint and behavioral biometrics during the onboarding session

Organizations that miss synthetic identities at IAL2 are almost always treating it as a document verification exercise rather than a multi-signal corroboration process.

Deepfake Detection and Liveness Fraud in Banking

The deepfake problem deserves its own treatment because it's changing the IAL2 threat model faster than most compliance frameworks have adapted.

Why Liveness Detection Fraud Is an IAL2 Priority

Liveness detection fraud attacks the selfie comparison step of biometric identity verification. Traditional active liveness (blink, turn your head) was defeated by replay attacks years ago. Modern passive liveness uses texture analysis, depth estimation, and micro-expression detection to distinguish real faces from artifacts. But deepfake generation tools now produce outputs that defeat some commercial passive liveness systems.

NIST 800-63-4 doesn't prescribe specific liveness technologies. It requires that organizations assess their threat model and select controls proportionate to the risk. For a bank deploying remote IAL2 account opening, a liveness system that satisfied examiner review in 2020 may not provide equivalent assurance in 2026. The NIST 800-63 identity assurance levels framework is intentionally technology-agnostic, which puts the burden of keeping up with the threat landscape squarely on the organization.

Practically, organizations should:

- Use ISO 30107-3 certified liveness solutions, this standard addresses presentation attack detection specifically and is what examiners ask about

- Layer injection attack detection alongside passive liveness, because the two attack classes require different technical controls

- Retain biometric comparison scores (not raw biometric data) for audit purposes, per your data retention policy

- Set score thresholds that reflect your risk appetite, not vendor defaults, a 90% match threshold means different things for a $500 account vs. a $500,000 account

- Monitor post-onboarding behavioral signals, synthetic and deepfake-onboarded accounts often show characteristic spending patterns that differ from legitimate customers

The Banking Access Controls: Zero Trust Security Architecture Strategy for Banking Ops Heads post covers how these biometric controls integrate with broader enterprise access management architectures.

Building an Identity Verification API Stack for IAL Compliance

Most organizations don't build identity proofing infrastructure from scratch. They assemble it from vendor components via APIs. The selection and integration of these components is where IAL compliance either holds together or breaks down.

Most organizations don't build identity proofing infrastructure from scratch.

What to Look for in an Identity Verification API

An identity verification api stack for IAL2 needs to cover:

- Document authentication: Automated checks for tampered documents, expired IDs, format anomalies, and barcode or chip validation

- Facial biometrics: 1:1 match against the document photo with a calibrated similarity score

- Liveness detection: ISO 30107-3 tested, with explicit protection against injection attacks

- Data enrichment: SSN verification, address validation, phone intelligence, and sanctions or PEP screening

- Orchestration logic: Routing different applicant populations through different check sequences based on risk signals

- Audit trail: Timestamped records of every check, every score, and every decision for regulatory examination

For organizations implementing KYC/AML automation at scale, the orchestration layer generates the most value. Static sequential checks are slow and produce unnecessary false positives. Dynamic orchestration that adjusts the check sequence based on early signals dramatically improves both KYC onboarding speed and proofing accuracy simultaneously.

KYC Onboarding Speed vs. Assurance Tradeoffs

The common assumption is that IAL2 means slow onboarding. In practice, the bottleneck is almost never the proofing technology. It's the workflow design. Teams that run all checks sequentially, route any flag to manual review, and require re-upload on document quality failures create long average onboarding times not because IAL2 is inherently slow, but because their orchestration isn't designed for throughput.

Modern identity verification fintech stacks achieve sub-60-second IAL2 onboarding by running document and liveness checks in parallel, using automated pre-screening to catch bad captures before submission, and routing low-risk applicants (clean documents, high biometric match, no adverse data signals) to instant approval. Manual review queues should handle genuinely ambiguous cases, not every applicant who triggers a partial watchlist name match. The AML Risk Checks in Policy Issuance: KYC/AML & Identity Verification Strategy post examines these same orchestration patterns in the insurance context, where IAL2 requirements overlap directly with underwriting workflows.

Zero Trust and NIST 800-63-4: Why They Go Together

NIST 800-63-4 governs identity proofing and authentication. Zero trust governs ongoing access decisions. They're complementary frameworks, and organizations that treat them separately end up with proofing rigor at enrollment that disappears during session management.

Zero Trust Security Framework Alignment with IAL and AAL

The zero trust security framework principle of "never trust, always verify" applies directly to authenticated sessions. An IAL2-proofed user who authenticates at AAL1 and is then granted persistent access to financial data without re-verification is a zero trust failure, regardless of how thorough the initial proofing was.

NIST SP 800-207, which defines zero trust architecture, aligns with 800-63-4 in several ways: continuous authentication signals correspond to AAL session management requirements, least-privilege access requires knowing the IAL of the authenticated subject, and device trust signals supplement the AAL assessment for policy decisions.

Zero Trust Financial Services Implementation

In zero trust financial services deployments, the integration between NIST 800-63-4 and a zero trust architecture works like this: the identity proofing system establishes the IAL and creates a bound authenticator. The authentication system validates AAL on each session. The policy engine consults both the IAL claim and real-time risk signals (location, device, transaction type, time of day) to make an access decision. No session is automatically trusted after initial authentication.

For organizations building this integration, the Zero Trust + Agentic AI: The New Normal for Banking Security post covers how AI-driven continuous verification extends the NIST framework into real-time transaction monitoring. The High-Risk Supplier Validation: KYC/AML & Identity Verification Strategy for CISOs piece addresses how IAL concepts apply to third-party and supplier verification, not just customer onboarding in financial services.

- NIST 800-63 identity assurance levels define the degree of confidence a relying party can have in a verified identity.

- AAL governs the authentication mechanisms required during each session.

- The honest answer is that there is no single right answer.

- SP 800-63A governs the digital identity proofing process.

- Synthetic identity fraud is the construction of a fictitious identity using a mix of real and fabricated data.

Onboard Customers in Seconds

Conclusion

Picking the right NIST 800-63 identity assurance level isn't a one-time decision. It's an ongoing architecture choice that needs to track your threat environment, regulatory posture, and the specific risk profile of each service you offer. IAL2 is the practical minimum for any regulated financial service, but IAL2 implemented without adequate liveness detection fraud controls, without synthetic identity fraud detection signals, and without matching AAL coverage during session management doesn't deliver IAL2 assurance in practice.

The organizations getting this right treat digital identity proofing as a living program rather than a deployment checkpoint. They review biometric identity verification thresholds as the deepfake detection banking threat shifts. They measure KYC onboarding speed alongside proofing accuracy rather than trading one for the other. And they align their identity verification fintech stack to the zero trust security framework principles that govern what happens after enrollment, not just during it. If you're assessing your current IAL and AAL alignment, the starting point is an honest gap analysis against the NIST 800-63-4 requirements for your specific service categories.

Share this article