.webp)

Listen To Our Podcast🎧

Introduction

Multi-agent AI systems in finance are changing how large institutions handle fraud detection, identity verification, and regulatory compliance at scale. Rather than routing every risk decision through a single model, banks and fintechs now deploy networks of specialized agents that split the work, share findings, and reach consensus before acting. The difference in outcomes is measurable: institutions using multi-agent architectures report reducing manual review queues by 60 to 70% while cutting false positive rates significantly.

The difference in outcomes is measurable: institutions using multi-agent architectures report reducing manual review queues by 60 to 70% while cutting false positive rates significantly.

This post breaks down how these systems work in practice: how agents coordinate across KYC workflows, liveness detection fraud prevention, and synthetic identity fraud detection. It also covers the control mechanisms that keep agent decisions auditable, and why a zero trust security framework is the right pairing for this kind of architecture.

- What Are Multi-Agent AI Systems in Finance?

- How Coordination Works Across Specialized Agents

- Identity Verification Fintech: Where Multi-Agent AI Delivers Speed

- Biometric Identity Verification and Liveness Detection

- Detecting Synthetic Identity Fraud with Agent Consensus

Onboard Customers in Seconds

What Are Multi-Agent AI Systems in Finance?

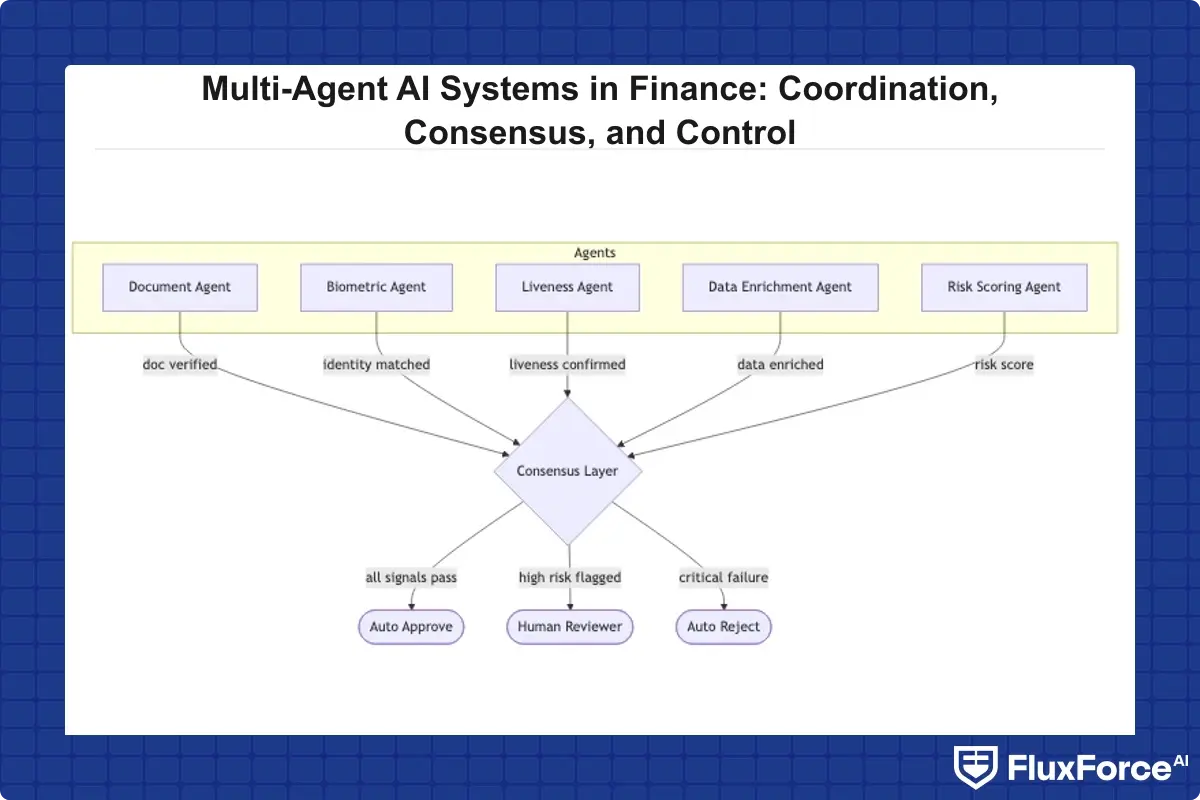

Multi-agent AI systems in finance consist of multiple specialized AI models working in parallel, each handling a distinct aspect of a financial decision. One agent might assess document authenticity. Another evaluates behavioral signals. A third cross-references sanctions databases. Each produces a verdict, and a coordination layer aggregates those verdicts into a final output.

This is different from a single model that tries to do everything. When one model handles document review, biometric identity verification, and AML screening simultaneously, it tends to underperform on all three. Specialization matters, and multi-agent design makes specialization economically practical at production scale.

How Agents Divide Responsibility in Risk Workflows

A typical KYC onboarding workflow in a multi-agent system assigns agents to distinct tasks:

- Document Agent: Verifies ID documents, checks for tampering, and extracts structured data fields

- Biometric Agent: Runs biometric identity verification, including face matching against the document photo

- Liveness Agent: Runs liveness detection fraud checks to confirm the person is physically present

- Data Enrichment Agent: Cross-references extracted identity data against credit bureaus, watchlists, and public records

- Risk Scoring Agent: Aggregates all signals and produces a final risk score

Each agent can be updated or replaced independently. When deepfake detection banking standards improve, you update the liveness agent without rebuilding the rest of the pipeline.

The Role of Consensus Mechanisms

Consensus is what separates a multi-agent system from a collection of independent models. Before a final decision is issued, agents must agree above a defined confidence threshold. If the document agent passes an application but the liveness agent flags it, the system does not auto-approve. It escalates to a human reviewer or triggers additional verification steps.

This is not just good engineering. It is a regulatory requirement in many jurisdictions. Regulators expect explainable, consistent decision-making, and consensus mechanisms provide exactly that kind of traceable logic.

How Coordination Works Across Specialized Agents

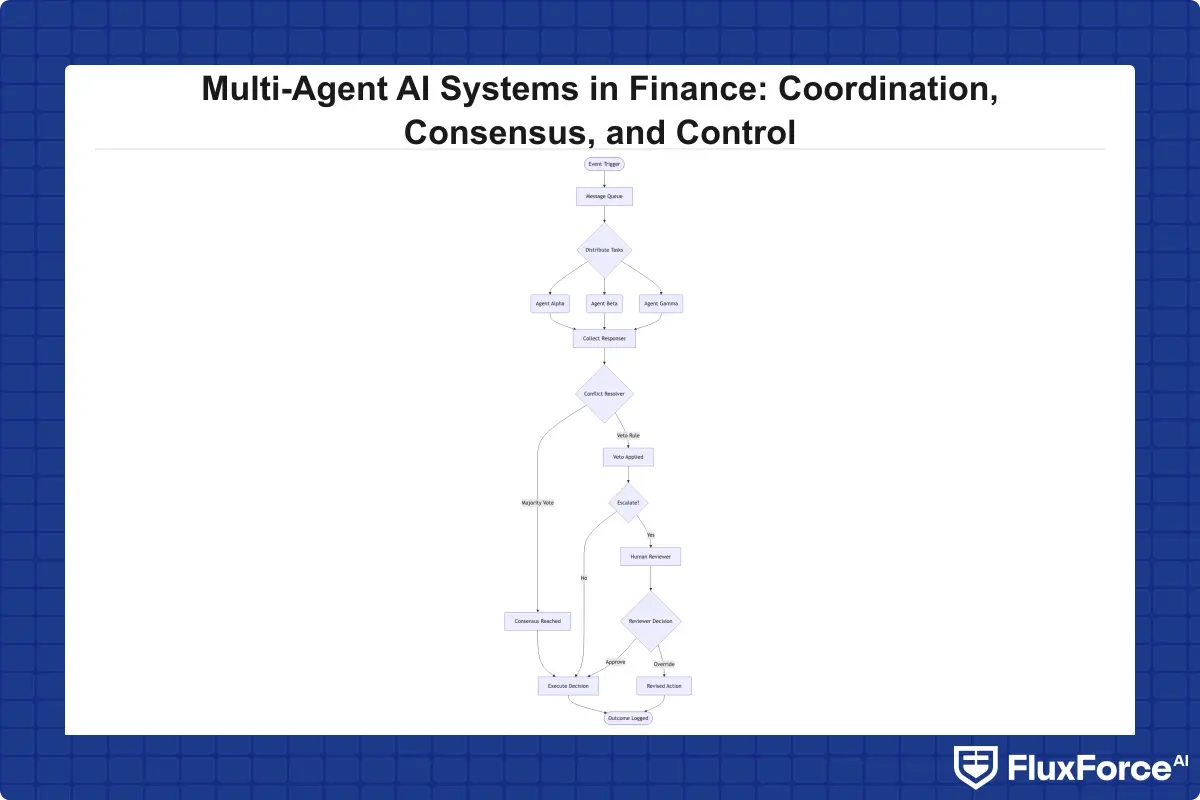

The coordination layer is the part of multi-agent AI systems in finance that most teams underestimate. Getting individual agents to work accurately is solvable. Getting them to communicate, share context, and resolve disagreements in real time is the genuinely hard part.

Event-Driven Agent Communication

Most production financial systems use event-driven architectures to coordinate agents. An identity verification api triggers the document agent when a user submits a photo ID. The document agent publishes its output to a message queue. The biometric agent and data enrichment agent consume that output and begin their work in parallel. The risk scoring agent waits for all upstream agents to publish before aggregating.

This approach has a practical latency advantage. Running agents in parallel rather than in sequence is how teams achieve kyc onboarding speed that competes with consumer expectations. A verification flow that once took 48 hours can complete in under 90 seconds with this architecture.

When Agents Disagree: Conflict Resolution Protocols

Conflict resolution is a design decision that needs to be explicit before deployment. Common approaches include:

- Majority vote: If three out of five agents flag risk, the application is flagged

- Weighted consensus: Agents with higher accuracy on a given signal type carry more weight in the final decision

- Veto rules: Certain agents, such as a sanctions screening agent, have hard veto authority regardless of other agent outputs

- Escalation thresholds: Disagreements above a defined confidence gap route automatically to human review

The choice depends on the risk tolerance and regulatory context of the institution. Insurance carriers often use different weights than retail banks because the cost of a false negative differs substantially across product types.

Identity Verification Fintech: Where Multi-Agent AI Delivers Speed

Identity verification fintech has always struggled with the tradeoff between thoroughness and speed. Manual review is thorough but slow. Automated single-model checks are fast but miss edge cases. Multi-agent systems offer a third option: automated, parallel, and accurate.

KYC Onboarding Speed: From Days to Minutes

The impact on kyc onboarding speed is the most consistently cited benefit of multi-agent design in digital identity proofing. Traditional KYC processes in established banks involve document collection, manual data entry, sanctions screening, and human review, a process that routinely takes 3 to 7 business days. Multi-agent systems that use a dedicated identity verification api for each step can compress this to minutes.

The practical result is lower abandonment rates at onboarding. Research from McKinsey on financial services digital transformation shows that customer drop-off during onboarding correlates directly with time-to-decision. Cutting onboarding from days to minutes has a measurable impact on conversion, particularly for mobile-first customers.

For institutions building this capability, KYC and AML automation via multi-agent identity verification platforms offers a production-grade approach to digital identity proofing that integrates with existing core banking systems.

How Identity Verification APIs Enable Real-Time Decisions

An identity verification api is the integration surface through which multi-agent systems exchange data with external verification sources. A well-designed API layer allows agents to query credit bureaus, document authentication services, biometric matching engines, and sanctions databases in parallel, without each agent waiting for the previous call to complete.

The design principle here is idempotency: each API call should produce the same result if called multiple times, and agents should be able to retry failed calls without corrupting the state of the overall decision. This is where many internal builds fail. Teams build capable agents but underestimate the complexity of the API orchestration layer underneath them.

Biometric Identity Verification and Liveness Detection

Biometric identity verification has become the standard for digital identity proofing in regulated financial services. A document photo alone is no longer sufficient. Regulators and fraud teams have converged on biometrics as the reliable signal because documents can be forged but a live person cannot be replicated at scale.

Liveness Detection Fraud Prevention in Practice

Liveness detection fraud refers to attacks where someone presents a photo, video, or mask to a biometric check rather than their actual face. Passive liveness detection systems analyze texture, depth cues, and micro-movement patterns to distinguish a live person from a presentation attack. Active liveness systems prompt the user to perform specific actions, such as blinking or turning the head, that are harder to spoof.

The gap between passive and active detection matters in production. For low-risk onboarding scenarios, passive liveness is usually sufficient. For high-value account openings or large transactions, active liveness detection becomes the defensible standard under most regulatory frameworks. Most institutions need both, deployed based on the risk tier of the specific use case.

Multi-Modal Biometric Checks

A single biometric signal is easier to spoof than a combination of signals. Multi-agent systems that run facial recognition, voice analysis, and behavioral biometrics in parallel create a higher bar for attackers. If a fraudster presents a high-quality deepfake video, the facial recognition agent might pass it, but the behavioral biometric agent, which analyzes typing cadence, mouse movement, and session timing patterns, flags anomalies.

This layering is the practical rationale behind multi-agent design for biometric identity verification. No single check is sufficient by itself; the system's reliability comes from combining signals that are independently difficult to simultaneously spoof.

Detecting Synthetic Identity Fraud with Agent Consensus

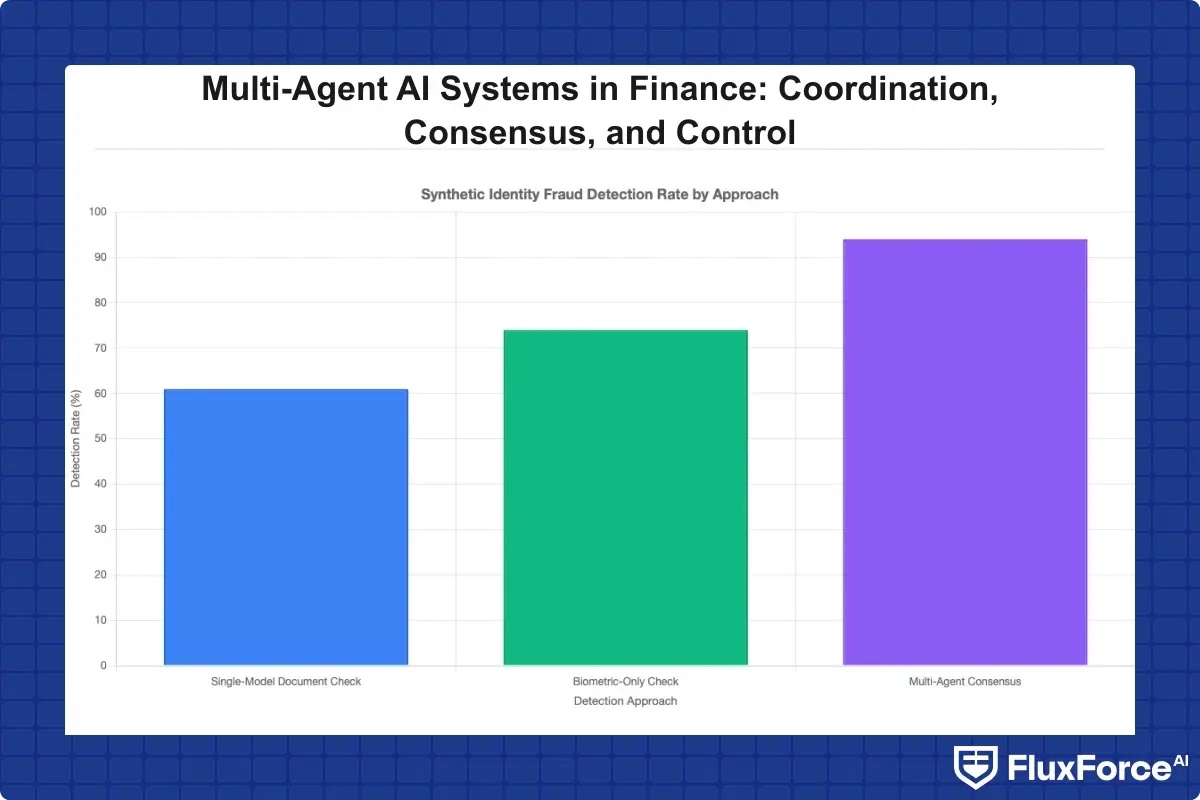

Synthetic identity fraud detection is one of the clearest use cases for multi-agent consensus in financial services. Synthetic identities combine real and fabricated data to create a new persona, designed specifically to pass individual verification checks. They often have plausible credit histories, real SSNs from children or deceased individuals, and consistent behavioral patterns built up over months.

Single-model checks fail against synthetic identities because each individual data point looks legitimate. Multi-agent consensus catches them because agents look for internal consistency across all signals simultaneously, which is something a single model optimized for throughput cannot do reliably.

How Multi-Agent Systems Spot Fabricated Identities

A synthetic identity fraud detection pipeline in a multi-agent system typically works as follows:

- The document agent verifies the ID but also extracts metadata including font consistency, microprint quality, and embedded data fields

- The biometric agent confirms the face match but also analyzes image artifacts that suggest digital manipulation

- The data enrichment agent cross-references the SSN issue date against the stated age of the applicant

- The behavioral agent flags if the application was submitted from device fingerprints associated with previously rejected applications

- The risk scoring agent looks for "credit-invisible" applicants who appear suddenly with a full credit file

The consensus layer flags the application if any two agents independently raise concerns the others cannot explain. This is how the system catches what FluxForce describes as the "sleeper pattern" in detecting synthetic identity fraud in real-time: identities built slowly over months to avoid detection thresholds.

Synthetic Identity Fraud Detection at Onboarding

The most cost-effective time to catch synthetic identities is at onboarding, before the fraudster establishes an account relationship. Once a synthetic identity has an active account, the cost of detection and remediation increases substantially. Multi-agent systems that flag inconsistencies at the point of digital identity proofing are significantly more cost-effective than post-approval monitoring alone.

NIST's Digital Identity Guidelines (SP 800-63-3) provide the foundational framework that most financial institutions reference when designing identity proofing systems, and multi-agent architectures align naturally with the identity assurance levels NIST defines.

Zero Trust Financial Services and Agent Architecture

Zero trust financial services architecture operates on one core principle: never assume a user, device, or system is trustworthy by default. Every access request is verified, every session is monitored, and trust is never granted based on network location alone. Multi-agent AI systems fit naturally into this model because they provide continuous, evidence-based verification rather than a one-time check at the front door.

Zero Trust Security Framework for Identity Flows

A zero trust security framework applied to identity verification means authentication is not a one-time event at login. It is continuous. An agent monitors transaction patterns throughout a session and can trigger re-verification if behavior deviates from the established baseline. Banks implementing this approach have reported significant reductions in account takeover fraud because attackers who pass initial authentication are caught by in-session behavioral checks.

The key implementation detail is that zero trust verification agents must operate without introducing latency that users notice. The practical target is sub-100ms response times for behavioral checks. This requires agents that run inference close to the user rather than routing every decision through a central server.

For further context on how zero trust architectures apply to banking operations, the analysis of Zero Trust Security Architecture Strategy for Banking Operations covers operational implementation in depth, including access control design and session management.

Continuous Verification vs. Perimeter Defense

Perimeter defense, the idea that you verify once at the edge and then trust everything inside, has been failing for years. It fails because attackers who get past the perimeter can move laterally without being challenged. The multi-agent approach under a zero trust security framework challenges that assumption directly: every significant action is verified, not just the first login.

For compliance officers, the operational benefit is a continuous audit trail. Every agent decision is logged with the signals that drove it. This is precisely what regulators want to see when they conduct examinations, and what makes multi-agent architectures defensible in regulatory reviews.

Deepfake Detection Banking: The Emerging Threat Tier

Deepfake detection banking is no longer a theoretical concern for financial services teams. Banks are now encountering deepfake attacks in account opening flows, video-based KYC calls, and voice authentication systems. The quality of commercially available deepfake tooling has improved to the point where standard biometric checks can be fooled without specialist infrastructure to counter them.

Why Static Image Checks No Longer Work

Static image-based biometric checks compare a selfie against a document photo. A high-quality deepfake can produce a photorealistic face that passes this comparison with current threshold settings. The defense requires moving beyond static analysis to dynamic signals: micro-expressions, skin texture at the pixel level, inconsistencies in lighting across the face, and physiological signals such as subtle color changes from blood flow.

Multi-agent systems are better positioned to run these checks because the checks can be distributed across specialized agents running in parallel. A deepfake detection agent focused on physiological signals runs alongside the standard biometric agent, rather than replacing it. The combination catches attacks that neither would catch independently.

For organizations evaluating how deepfake risks intersect with broader API security controls, the API Security Strategies for CISOs in Banking covers the exposure surface in financial APIs that deepfake-enabled fraud increasingly targets.

Digital Identity Proofing at Scale with Identity Verification APIs

Scaling digital identity proofing is where multi-agent architecture shows its clearest operational advantage over single-model approaches. A single model that handles document verification, biometric matching, and liveness detection simultaneously becomes a bottleneck under high load. Multi-agent systems scale horizontally: add capacity to whichever agent is under pressure without modifying the others.

Building an Identity Verification API Strategy

An effective identity verification api strategy for a financial institution involves three design decisions:

- Modularity: Each verification step should be callable as an independent API endpoint, allowing agents to be updated, replaced, or scaled independently without touching the rest of the pipeline

- Orchestration: A central orchestration layer manages which agents run, in what sequence, and how results are aggregated, including conflict resolution logic

- Fallback handling: When an agent or external API is unavailable, defined fallback behavior prevents both failing open (approving by default, which is dangerous) and failing closed (blocking all traffic, which harms conversion)

The identity verification api approach also allows institutions to combine vendor-provided agents with internally built ones. A bank might use a specialist vendor for liveness detection fraud prevention while running its own sanctions screening agent internally. The orchestration layer does not care where each agent runs; it cares only about the output format and response time.

Scaling Multi-Agent Identity Verification Infrastructure

Multi-agent systems scale horizontally because each agent is an independent service. When liveness detection checks spike at peak hours, you scale the liveness agent independently without touching the document or sanctions screening agents. This operational flexibility is what identity verification fintech teams cite most often: the ability to add capacity where load concentrates without a full system rebuild.

This design also simplifies vendor transitions. If a better deepfake detection banking solution becomes available, you swap out the relevant agent and update the orchestration layer. The rest of the pipeline continues running without modification.

For compliance teams, connecting this infrastructure to automated AML risk checks creates end-to-end coverage from onboarding through ongoing transaction monitoring, as detailed in the AML Screening Strategy for Payments Risk Officers framework.

- Multi-agent AI systems in finance consist of multiple specialized AI models working in parallel, each handling a distinct aspect of a financial decision.

- The coordination layer is the part of multi-agent AI systems in finance that most teams underestimate.

- Identity verification fintech has always struggled with the tradeoff between thoroughness and speed.

- Biometric identity verification has become the standard for digital identity proofing in regulated financial services.

- Synthetic identity fraud detection is one of the clearest use cases for multi-agent consensus in financial services.

Onboard Customers in Seconds

Conclusion

Multi-agent AI systems in finance are not a future state. They are in production at major banks, fintechs, and insurers today. The core insight is that specialized agents coordinating toward consensus outperform single models trying to do everything, particularly in high-stakes decisions involving identity verification fintech workflows, fraud detection, and AML screening.

The institutions getting the most from this architecture treated coordination, conflict resolution, and audit logging as first-class design concerns, not afterthoughts. Pairing multi-agent identity verification with a zero trust security framework gives compliance and security teams both the kyc onboarding speed needed for competitive positioning and the control required for regulatory examination readiness.

If your institution is evaluating how to structure an agent-based identity and compliance stack, start by defining what each agent is responsible for and what the consensus rules look like when they disagree. That design decision shapes everything downstream.

Share this article